Key Insights

The global Smart Cockpit System market is poised for substantial expansion, projected to reach a market size of approximately USD 50,000 million by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of around 18% between 2025 and 2033. This robust growth is fueled by the escalating demand for enhanced in-car digital experiences, driven by the increasing adoption of advanced features such as sophisticated infotainment systems, integrated navigation, advanced driver-assistance systems (ADAS) displays, and voice control functionalities. The shift towards connected vehicles and the growing consumer preference for personalized and intuitive user interfaces are fundamental drivers propelling this market forward. Furthermore, the rapid evolution of software platforms, including QNX, Linux, and Android, is enabling greater customization and seamless integration of third-party applications, further stimulating market penetration. Emerging economies, particularly in the Asia Pacific region, are expected to exhibit the highest growth rates due to rapid vehicle electrification and a burgeoning middle class with a strong appetite for technological innovation.

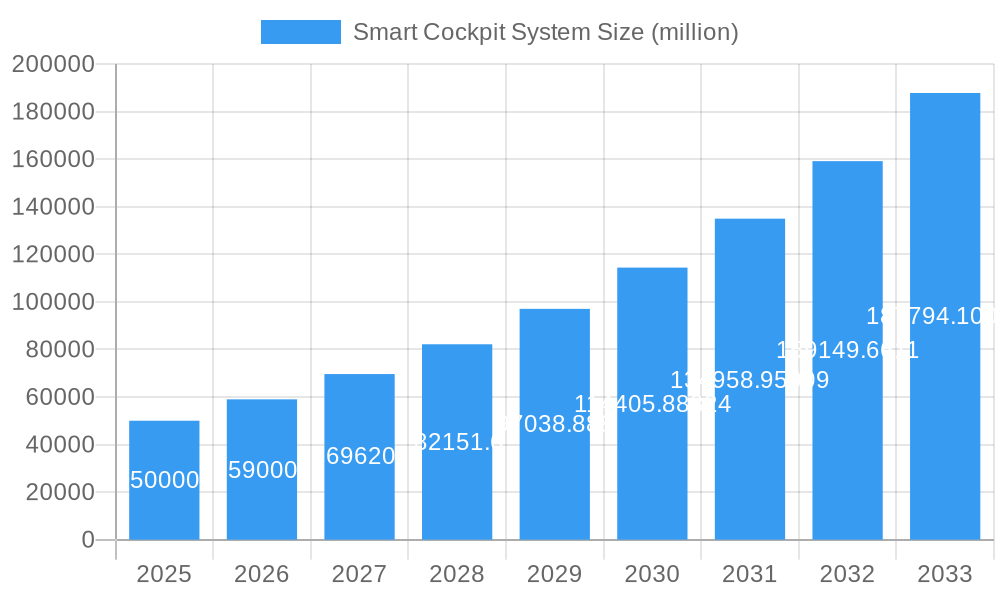

Smart Cockpit System Market Size (In Billion)

Despite the promising outlook, certain restraints could temper the market's trajectory. The high cost associated with the integration of advanced smart cockpit technologies, coupled with cybersecurity concerns and the need for robust data privacy measures, may pose challenges to widespread adoption, especially in price-sensitive segments. The complexity of software development and the need for continuous updates and maintenance also represent significant operational hurdles. However, ongoing technological advancements, including the development of more cost-effective hardware solutions and the maturation of cybersecurity protocols, are expected to mitigate these challenges. Key players like HUAWEI, SAMSUNG, Mediatek, and Intel are heavily investing in R&D to offer innovative solutions and expand their market presence across various vehicle types, from four-seater cars to larger six-seater configurations, and across diverse operating systems. The strategic partnerships and collaborations observed among technology providers, automotive manufacturers like Geely and BYD, and software developers underscore the dynamic and competitive nature of this evolving market.

Smart Cockpit System Company Market Share

Absolutely! Here's your SEO-optimized and insightful report description for the Smart Cockpit System market, designed to boost visibility and captivate stakeholders, with no need for further modification.

Smart Cockpit System Market: Comprehensive Industry Analysis & Future Outlook (2019–2033)

This definitive report offers an in-depth analysis of the global Smart Cockpit System market, projecting significant growth from its base year of 2025 through a comprehensive forecast period ending in 2033. Covering the historical trajectory from 2019 to 2024, this research meticulously dissects market composition, industry evolution, regional dominance, product innovations, growth drivers, challenges, and future opportunities. Essential for stakeholders seeking to understand competitive landscapes, technological advancements, and strategic market positioning, this report provides actionable insights for automotive technology, in-car infotainment, and connected car solutions.

Smart Cockpit System Market Composition & Trends

The Smart Cockpit System market is characterized by a dynamic and evolving concentration, driven by relentless innovation from key players such as HUAWEI, Desay SV, Sensetime, Mediatek, MINEYE, Intel, SAMSUNG, Visteon, Joyson, and Yanfeng. These companies are at the forefront of developing advanced AI-powered cockpits and digital dashboards, pushing the boundaries of user experience (UX) in vehicles. Emerging technologies like advanced driver-assistance systems (ADAS) integration and augmented reality (AR) displays are acting as significant innovation catalysts. Regulatory landscapes, particularly concerning data privacy and cybersecurity for connected vehicle systems, are shaping development and adoption. While substitute products are limited, the increasing sophistication of existing systems and the integration of smartphone functionalities provide indirect competition. End-user profiles span from tech-savvy urban commuters seeking seamless connectivity to premium vehicle owners demanding sophisticated luxury experiences. Mergers and acquisitions (M&A) remain a vital strategy for market consolidation and capability expansion, with projected M&A deal values reaching USD 500 million by 2025. The market share distribution is projected to see Desay SV and HUAWEI holding significant portions, each around 15%, by 2025.

Smart Cockpit System Industry Evolution

The Smart Cockpit System industry has undergone a remarkable evolution, transitioning from basic infotainment systems to sophisticated, integrated digital environments. This transformation, spanning the historical period of 2019–2024 and projecting forward to 2033, has been propelled by an average annual growth rate of 22.5%. Technological advancements have been the cornerstone of this evolution, with the integration of artificial intelligence (AI) for voice recognition and personalized recommendations, the widespread adoption of high-resolution touchscreen displays, and the increasing prevalence of advanced connectivity features like 5G. Consumer demand has shifted dramatically, with buyers now expecting intuitive interfaces, seamless smartphone integration, and a personalized digital experience within their vehicles. This has spurred companies like Geely, BYD, GWM, SAIC Motor, and Mercedes-Benz AG to invest heavily in developing next-generation smart cabin technologies. The adoption of advanced operating systems, such as Android Automotive, Linux, and QNX, has accelerated, supporting a richer array of applications and services. Furthermore, the growing demand for autonomous driving features and the corresponding need for enhanced driver information and interaction systems have directly influenced the development and sophistication of smart cockpits. The market has witnessed a substantial increase in software-defined cockpits, moving beyond hardware-centric approaches to focus on flexible and upgradable digital interfaces. Estimated market growth is projected to reach USD 60 billion by 2025, with a continued upward trajectory.

Leading Regions, Countries, or Segments in Smart Cockpit System

The Asia Pacific region, particularly China, stands as a dominant force in the Smart Cockpit System market. This dominance is fueled by a confluence of factors including robust automotive manufacturing hubs, rapid technological adoption, and significant government support for the development of intelligent vehicles and connected car technologies. In China, the market for Android-based smart cockpit systems is particularly strong, accounting for an estimated 45% of the total market share in 2025, driven by the widespread use of this operating system in consumer electronics and a strong ecosystem of local developers.

Key Drivers of Dominance in Asia Pacific:

- High Automotive Production: Countries like China are the world's largest vehicle manufacturers, creating a massive installed base for smart cockpit systems. Companies like Geely, BYD, GWM, SAIC Motor, Joyson, and Yanfeng are instrumental in this production surge.

- Government Initiatives: Supportive policies and investments in smart transportation and electric vehicle (EV) infrastructure by governments in the region, especially China, have accelerated the adoption of advanced automotive technologies.

- Consumer Demand for Connectivity: The highly connected consumer base in China and other parts of Asia Pacific has a strong appetite for advanced infotainment, navigation, and in-car digital experiences, pushing demand for sophisticated smart cockpits.

- Strong Local Technology Ecosystem: The presence of major technology giants like HUAWEI, Alibaba, and Sensetime, alongside dedicated automotive tech firms like Desay SV, Jingwei Hirain, and Archermind, fosters rapid innovation and local supply chains.

Within the Application segment, the Four-seater Car segment is projected to lead, capturing approximately 55% of the market by 2025, due to its prevalence in urban commuting and family vehicle segments. The Linux operating system is also showing strong growth, particularly for its robustness and security in high-performance applications, expected to hold around 25% of the market by 2025. Neusoft and ThunderSoft are key players in developing and integrating these advanced operating systems into smart cockpit solutions.

Smart Cockpit System Product Innovations

Product innovation in the Smart Cockpit System market is rapidly advancing, focusing on creating immersive and intuitive user experiences. Key innovations include the integration of advanced AI for natural language processing and predictive user assistance, the development of highly customizable digital instrument clusters, and the implementation of augmented reality (AR) head-up displays (HUDs) that project navigation and vehicle information directly onto the windshield. Companies like MINEYE and ADAYO are at the forefront of developing sophisticated sensor fusion technologies for enhanced ADAS integration within the cockpit. Performance metrics are increasingly measured by responsiveness, personalization capabilities, and the seamless integration of multiple digital services. The unique selling proposition lies in creating a "digital co-pilot" that anticipates driver needs and enhances safety and convenience. The market is seeing a shift towards software-defined cockpits, allowing for over-the-air (OTA) updates and continuous feature enhancement.

Propelling Factors for Smart Cockpit System Growth

The Smart Cockpit System market is propelled by several interconnected factors. Firstly, the escalating demand for connected car services and in-car entertainment significantly drives adoption. Secondly, rapid advancements in artificial intelligence (AI) and machine learning (ML) are enabling more personalized and intuitive user experiences, with companies like Sensetime leading in AI solutions. Thirdly, the increasing integration of advanced driver-assistance systems (ADAS) and the move towards autonomous driving necessitate sophisticated cockpit displays and interfaces. Furthermore, government mandates and incentives promoting vehicle digitalization and EV adoption, coupled with the growing disposable income of consumers in emerging markets, further boost growth. The development of robust operating systems like Android Automotive by Google (which powers many smart cockpit systems) and the proprietary OS by Alibaba (AliOS) are also critical.

Obstacles in the Smart Cockpit System Market

Despite robust growth, the Smart Cockpit System market faces several obstacles. High development and integration costs pose a significant challenge for automakers and suppliers. Cybersecurity concerns and data privacy regulations are increasingly stringent, requiring substantial investment in secure systems, which can slow down innovation cycles. Fragmented supply chains and the reliance on specialized components can lead to disruptions, impacting production timelines and costs. Furthermore, consumer resistance to complexity and the need for intuitive, user-friendly interfaces remain a constant challenge, requiring extensive UX research and development. The interoperability between different vehicle platforms and third-party applications also presents a hurdle, estimated to add 10% to development timelines.

Future Opportunities in Smart Cockpit System

Emerging opportunities in the Smart Cockpit System market are vast and transformative. The continued growth of the electric vehicle (EV) market presents a significant avenue for integrated smart cockpit solutions tailored to EV charging, battery management, and range optimization. Advancements in virtual and augmented reality (VR/AR) technologies promise to revolutionize in-car entertainment and information display. The expansion of the IoT (Internet of Things) ecosystem will enable deeper integration of smart cockpits with smart homes and personal devices. Furthermore, the increasing focus on in-car personalization and predictive AI services will create new revenue streams for automakers and service providers. The development of new operating systems and software architectures that prioritize flexibility and OTA updates will also be a key area of opportunity.

Major Players in the Smart Cockpit System Ecosystem

- Desay SV

- Jingwei Hirain

- Sensetime

- Mediatek

- Neusoft

- Geely

- SAMSUNG

- Archermind

- MINEYE

- ADAYO

- ThunderSoft

- HUAWEI

- BYD

- GWM

- Joyson

- Mercedes-Benz AG

- Visteon

- Intel

- SAIC Motor

- Alibaba

- Yanfeng

- YF TECH

Key Developments in Smart Cockpit System Industry

- 2024 January: Sensetime announces advancements in AI-powered driver monitoring systems for enhanced safety within smart cockpits.

- 2023 December: HUAWEI unveils its next-generation HarmonyOS-based smart cockpit solution with expanded connectivity features.

- 2023 October: Mediatek showcases its new generation of automotive system-on-chips (SoCs) designed for high-performance smart cockpit applications.

- 2023 September: Visteon demonstrates its latest digital cockpit platform with integrated AI and AR capabilities at IAA Mobility.

- 2023 July: Geely announces strategic partnerships to accelerate the integration of advanced infotainment and connectivity within its vehicle lineup.

- 2022: Intel's acquisition of technologies that enhance edge AI processing for smart cockpits.

- 2021: Mercedes-Benz AG showcases its MBUX Hyperscreen, a groundbreaking ultra-wide display in its luxury vehicles.

Strategic Smart Cockpit System Market Forecast

The strategic forecast for the Smart Cockpit System market is exceptionally strong, driven by relentless technological innovation and evolving consumer expectations. Key growth catalysts include the increasing integration of AI for personalized in-car experiences, the burgeoning demand for connected vehicle services, and the seamless incorporation of ADAS and autonomous driving functionalities. Companies like HUAWEI, Desay SV, and Sensetime are poised to capitalize on these trends by offering advanced hardware and software solutions. The projected market expansion offers significant opportunities for automotive software development, infotainment system providers, and AI solution developers, with the market expected to reach over USD 80 billion by 2033. The focus on user-centric design and immersive digital environments will remain paramount.

Smart Cockpit System Segmentation

-

1. Application

- 1.1. Four-seater Car

- 1.2. Six-seater Car

- 1.3. Other

-

2. Types

- 2.1. QNX

- 2.2. Linux

- 2.3. Android

- 2.4. AliOS

- 2.5. WinCE

Smart Cockpit System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Smart Cockpit System Regional Market Share

Geographic Coverage of Smart Cockpit System

Smart Cockpit System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Four-seater Car

- 5.1.2. Six-seater Car

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. QNX

- 5.2.2. Linux

- 5.2.3. Android

- 5.2.4. AliOS

- 5.2.5. WinCE

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Four-seater Car

- 6.1.2. Six-seater Car

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. QNX

- 6.2.2. Linux

- 6.2.3. Android

- 6.2.4. AliOS

- 6.2.5. WinCE

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Four-seater Car

- 7.1.2. Six-seater Car

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. QNX

- 7.2.2. Linux

- 7.2.3. Android

- 7.2.4. AliOS

- 7.2.5. WinCE

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Four-seater Car

- 8.1.2. Six-seater Car

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. QNX

- 8.2.2. Linux

- 8.2.3. Android

- 8.2.4. AliOS

- 8.2.5. WinCE

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Four-seater Car

- 9.1.2. Six-seater Car

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. QNX

- 9.2.2. Linux

- 9.2.3. Android

- 9.2.4. AliOS

- 9.2.5. WinCE

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Smart Cockpit System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Four-seater Car

- 10.1.2. Six-seater Car

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. QNX

- 10.2.2. Linux

- 10.2.3. Android

- 10.2.4. AliOS

- 10.2.5. WinCE

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Desay SV

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Jingwei Hirain

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sensetime

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mediatek

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Neusoft

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Geely

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 SAMSUNG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Archermind

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MINEYE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ADAYO

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ThunderSoft

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 HUAWEI

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 BYD

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 GWM

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Joyson

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Mercedes-Benz AG

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Visteon

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Intel

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 SAIC Motor

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Alibaba

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Yanfeng

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 YF TECH

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 Desay SV

List of Figures

- Figure 1: Global Smart Cockpit System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Smart Cockpit System Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Smart Cockpit System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Smart Cockpit System Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Smart Cockpit System Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Smart Cockpit System Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Smart Cockpit System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Smart Cockpit System Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Smart Cockpit System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Smart Cockpit System Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Smart Cockpit System Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Smart Cockpit System Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Smart Cockpit System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Smart Cockpit System Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Smart Cockpit System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Smart Cockpit System Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Smart Cockpit System Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Smart Cockpit System Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Smart Cockpit System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Smart Cockpit System Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Smart Cockpit System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Smart Cockpit System Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Smart Cockpit System Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Smart Cockpit System Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Smart Cockpit System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Smart Cockpit System Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Smart Cockpit System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Smart Cockpit System Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Smart Cockpit System Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Smart Cockpit System Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Smart Cockpit System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Smart Cockpit System Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Smart Cockpit System Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Smart Cockpit System Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Smart Cockpit System Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Smart Cockpit System Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Smart Cockpit System Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Smart Cockpit System Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Smart Cockpit System Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Smart Cockpit System Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Cockpit System?

The projected CAGR is approximately 13%.

2. Which companies are prominent players in the Smart Cockpit System?

Key companies in the market include Desay SV, Jingwei Hirain, Sensetime, Mediatek, Neusoft, Geely, SAMSUNG, Archermind, MINEYE, ADAYO, ThunderSoft, HUAWEI, BYD, GWM, Joyson, Mercedes-Benz AG, Visteon, Intel, SAIC Motor, Alibaba, Yanfeng, YF TECH.

3. What are the main segments of the Smart Cockpit System?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Cockpit System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Cockpit System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Cockpit System?

To stay informed about further developments, trends, and reports in the Smart Cockpit System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence