Key Insights

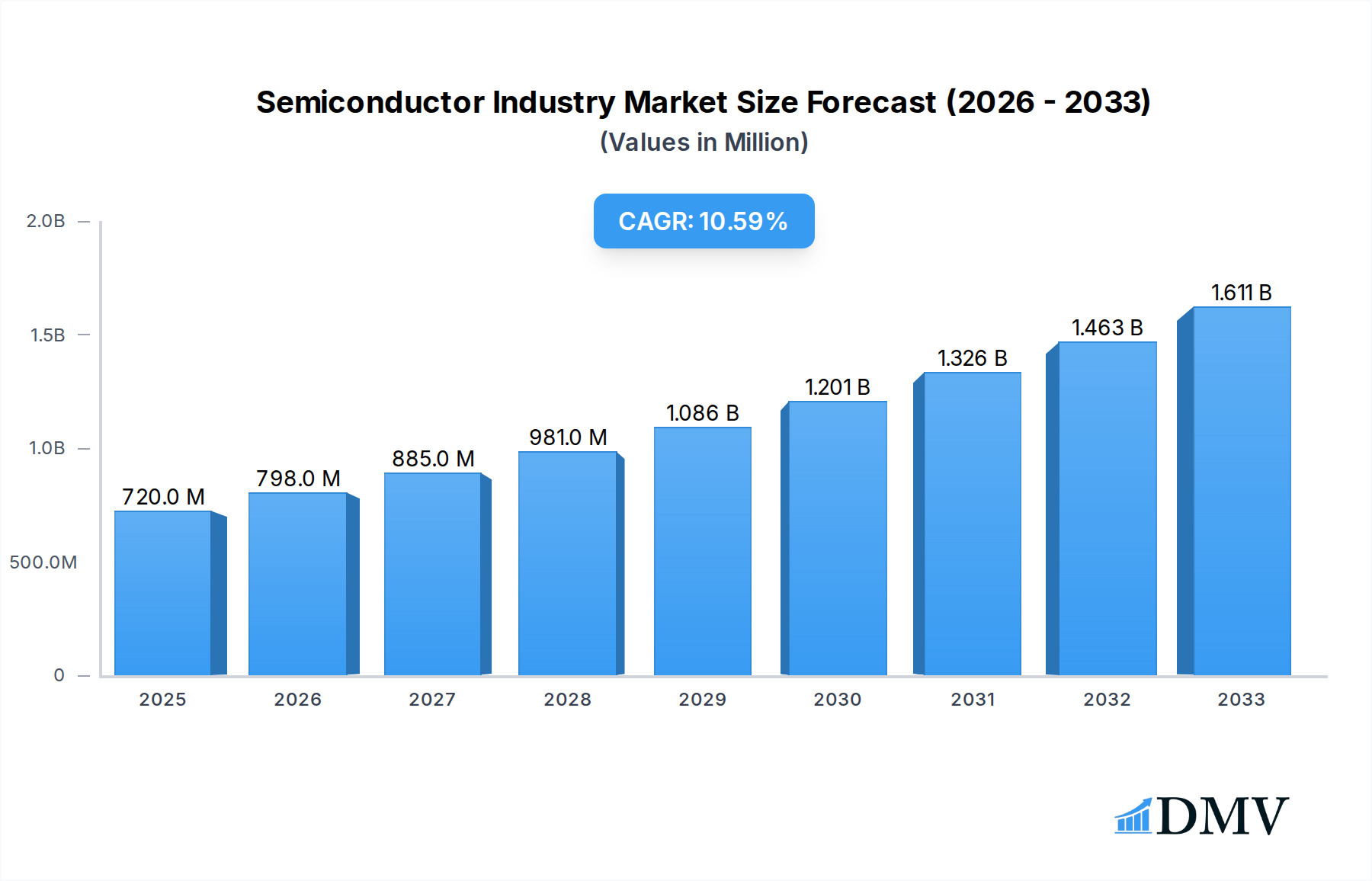

The global Semiconductor Industry is poised for remarkable expansion, projected to reach a market size of $720 million by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 10.86% over the forecast period of 2025-2033. This robust growth is fueled by escalating demand across various sectors, including artificial intelligence, 5G deployment, the Internet of Things (IoT), and the automotive industry's increasing reliance on advanced electronics. The proliferation of smart devices and the continuous innovation in computing power are creating sustained momentum for semiconductor sales. Key growth drivers include the rising adoption of advanced packaging technologies, the development of next-generation semiconductor materials, and significant investments in front-end and back-end semiconductor equipment. Geographically, Asia is expected to dominate the market, owing to the concentration of manufacturing hubs and strong consumer demand for electronic goods.

Semiconductor Industry Market Size (In Million)

The market segmentation reveals a dynamic landscape, with Integrated Circuits leading within Semiconductor Devices, while Front-end Equipment holds significant sway in Semiconductor Equipment. Semiconductor Materials are critically important for both fabrication and packaging processes, underscoring the industry's reliance on innovation at every stage. Out-of-fab (OOF) services are also gaining traction, indicating a trend towards specialized outsourcing in the semiconductor value chain. Despite the optimistic outlook, the industry faces restraints such as volatile raw material prices, geopolitical tensions impacting supply chains, and intense competition. However, the persistent need for more powerful, efficient, and smaller semiconductor components, coupled with ongoing research and development in areas like advanced lithography and novel materials, ensures a strong trajectory for the Semiconductor Industry in the coming years.

Semiconductor Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Semiconductor Industry, a critical sector underpinning modern technology. Spanning the historical period of 2019-2024, with a base year of 2025 and a forecast period extending to 2033, this research delves into market dynamics, technological advancements, and strategic opportunities. The report assesses the market's projected growth to exceed $1.5 Trillion by 2033, driven by surging demand for AI, 5G, IoT, and advanced computing. Discover key insights into semiconductor manufacturing, integrated circuits, semiconductor equipment, and semiconductor materials, crucial for stakeholders including semiconductor companies, investors, and policymakers.

Semiconductor Industry Market Composition & Trends

The global semiconductor market exhibits a dynamic and increasingly consolidated structure, driven by significant investments and technological innovation. Key players are investing heavily in advanced fabrication processes and packaging technologies to meet the escalating demand for high-performance integrated circuits and discrete semiconductors. Mergers and acquisitions (M&A) continue to shape the competitive landscape, with recent deals valued in the hundreds of billions aimed at acquiring cutting-edge intellectual property and expanding market reach. Regulatory frameworks are also evolving, with governments worldwide implementing incentives to bolster domestic semiconductor manufacturing capabilities. The rise of specialized optoelectronics and sensors further diversifies the market, catering to niche applications across automotive, healthcare, and consumer electronics.

- Market Concentration: Dominated by a few large players in semiconductor foundry and semiconductor equipment markets.

- Innovation Catalysts: Extreme Ultraviolet (EUV) lithography, advanced packaging, and novel material science.

- Regulatory Landscapes: Government incentives (e.g., US CHIPS Act) and trade policies influencing global supply chains.

- Substitute Products: Limited for core semiconductor functionalities, but innovation drives improved performance and efficiency.

- End-User Profiles: Broad, encompassing data centers, automotive, consumer electronics, telecommunications, and industrial sectors.

- M&A Activities: Strategic acquisitions focusing on technology acquisition and market consolidation, with deal values reaching billions of dollars.

Semiconductor Industry Industry Evolution

The semiconductor industry has undergone a remarkable evolution, transforming from a niche technology sector to a foundational pillar of the global economy. Over the historical period of 2019-2024, the market witnessed consistent growth, fueled by the exponential rise in data generation and consumption. The forecast period of 2025-2033 is poised for even more accelerated expansion, with projections indicating a compound annual growth rate (CAGR) of approximately 7.5%. This growth trajectory is intrinsically linked to rapid technological advancements, particularly in artificial intelligence (AI), machine learning, and the Internet of Things (IoT). Consumer demands are increasingly sophisticated, requiring more powerful, efficient, and specialized chips. The development of next-generation memory solutions, advanced processors, and specialized application-specific integrated circuits (ASICs) are key indicators of this evolution. Furthermore, the strategic importance of secure and resilient semiconductor supply chains has become a paramount concern for nations, leading to significant government investments and policy initiatives aimed at onshore and nearshore manufacturing capabilities. The continuous miniaturization of transistors, following Moore's Law, although facing physical limits, continues to drive innovation in front-end equipment and fabrication techniques, pushing the boundaries of computational power and energy efficiency. The increasing complexity of chip design and manufacturing necessitates substantial capital expenditure, estimated in the tens of billions of dollars for leading-edge fabs. The adoption of advanced back-end equipment for testing and packaging also plays a crucial role in ensuring product quality and performance, with market segments like OSAT (Outsourced Semiconductor Assembly and Test) experiencing significant growth.

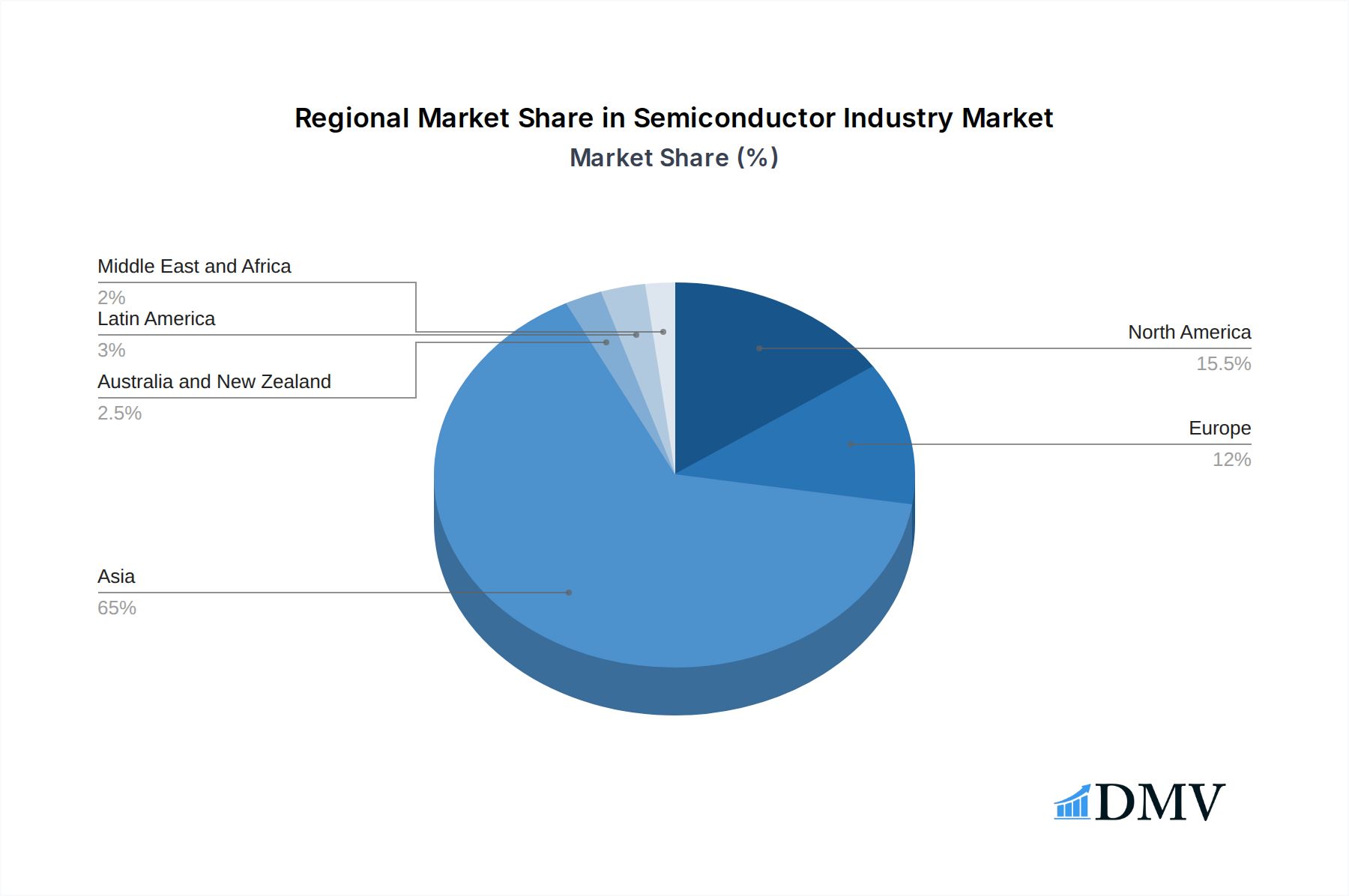

Leading Regions, Countries, or Segments in Semiconductor Industry

The global semiconductor industry landscape is characterized by distinct regional dominance and segment leadership, driven by a confluence of technological expertise, investment, and government support. Taiwan Semiconductor Manufacturing Company (TSMC) Limited remains the undisputed leader in the Semiconductor Foundry Market, accounting for over 50% of the global foundry revenue in 2025. This dominance is attributed to its cutting-edge process technologies, massive scale of operations, and long-standing relationships with fabless semiconductor companies. Consequently, Taiwan stands as the leading country in semiconductor manufacturing and foundry services.

In the Semiconductor Equipment market, the United States and Japan hold significant sway. Applied Materials Inc, Lam Research Corporation, and Tokyo Electron Limited are among the top global providers of front-end equipment, crucial for wafer fabrication. Their innovative technologies enable the production of increasingly complex integrated circuits and discrete semiconductors. The back-end equipment segment, vital for assembly and testing, is also highly competitive, with companies like Advantest Corporation and Teradyne Inc holding substantial market share.

The Semiconductor Devices market is more fragmented, with major players like Samsung Electronics Co Ltd, Intel Corporation, and SK Hynix Inc leading in memory chips and processors. Qualcomm Incorporated and Broadcom Inc are dominant forces in the mobile and connectivity segments, particularly for integrated circuits. The demand for advanced optoelectronics is growing, driven by applications in communication and display technologies.

The Semiconductor Materials segment, encompassing fabrication chemicals, silicon wafers, and packaging materials, is led by companies such as Sumitomo Chemical Co Ltd, Resonac Holding Corporation, and Dow Chemical Co (Dow Inc ). The quality and innovation in these materials directly impact the performance and reliability of finished semiconductor products.

- Dominant Segment: Semiconductor Foundry Market, primarily driven by TSMC.

- Leading Country: Taiwan, due to its unparalleled foundry capabilities.

- Key Drivers in Foundry: Access to leading-edge process nodes (e.g., 3nm, 2nm), high capacity, and strong customer relationships.

- Leading Regions in Equipment: United States and Japan for front-end and back-end equipment.

- Investment Trends: Significant government incentives in the US, Europe, and Asia to build domestic manufacturing capacity.

- Regulatory Support: Policies like the US CHIPS Act aim to reshore critical semiconductor production and R&D.

- Emerging Segments: Growing demand for specialized sensors for automotive and industrial applications, and advanced optoelectronics for 5G and AI.

Semiconductor Industry Product Innovations

The semiconductor industry is defined by relentless product innovation, pushing the boundaries of performance, efficiency, and functionality. The adoption of Extreme Ultraviolet (EUV) lithography by companies like Micron Technology, Inc. for its 1-gamma node DRAM signifies a major leap in fabrication techniques, enabling smaller and more powerful memory chips. This technology is crucial for next-generation AI applications and high-performance computing. Innovations in advanced packaging, such as chiplets and 3D stacking, are allowing for greater integration and performance gains in integrated circuits. The development of novel materials, including wide-bandgap semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN), is revolutionizing power electronics, leading to more efficient electric vehicles and power supplies. These advancements are critical for meeting the ever-increasing demands of data-intensive applications and sustainable energy solutions.

Propelling Factors for Semiconductor Industry Growth

The semiconductor industry is experiencing robust growth driven by several key factors. The insatiable demand for processing power in Artificial Intelligence (AI) and Machine Learning (ML) applications is a primary catalyst, requiring advanced integrated circuits and specialized processors. The rapid expansion of 5G networks globally necessitates high-performance chips for both infrastructure and consumer devices, boosting the market for semiconductor devices. The proliferation of the Internet of Things (IoT) is creating a massive market for low-power, high-efficiency sensors and connectivity chips. Furthermore, government initiatives and substantial investments worldwide, exemplified by the US CHIPS Act, are stimulating domestic semiconductor manufacturing and R&D, creating significant market opportunities. The ongoing digital transformation across all industries also fuels the demand for computing power and advanced semiconductor solutions.

Obstacles in the Semiconductor Industry Market

Despite its strong growth trajectory, the semiconductor industry faces several significant obstacles. Supply chain disruptions, exacerbated by geopolitical tensions and natural disasters, continue to pose a risk to production and availability, leading to price volatility and extended lead times. The intense competition and high capital expenditure required for leading-edge fabrication facilities create substantial barriers to entry for new players. Regulatory challenges, including trade restrictions and export controls, can fragment the global market and hinder collaboration. The increasing complexity of chip design and manufacturing demands highly skilled talent, leading to potential labor shortages in critical areas. Furthermore, the environmental impact of semiconductor manufacturing, including water and energy consumption, is an area of increasing scrutiny and regulatory pressure.

Future Opportunities in Semiconductor Industry

The future of the semiconductor industry is brimming with opportunities. The continued evolution of Artificial Intelligence (AI), particularly in areas like generative AI and edge AI, will drive demand for highly specialized and powerful processors and memory. The expansion of the Electric Vehicle (EV) market will fuel the need for advanced power semiconductors, sensors, and connectivity solutions. The metaverse and extended reality (XR) technologies present a new frontier for high-performance graphics processing units (GPUs) and immersive display technologies, requiring innovations in optoelectronics and integrated circuits. The push for greater energy efficiency and sustainability will create opportunities for novel materials and power management solutions. Investments in emerging markets and the development of localized semiconductor manufacturing capabilities will also open new avenues for growth and diversification.

Major Players in the Semiconductor Industry Ecosystem

- Advantest Corporation

- Amkor Technology Inc

- Applied Materials Inc

- ASML Holding NV

- ASE Technology Holding Co Ltd

- BASF SE

- Broadcom Inc

- Dow Chemical Co (Dow Inc )

- GlobalFoundries Inc

- Henkel AG & Co KGaA

- Hua Hong Semiconductor Limited

- Indium Corporation

- Intel Corporation

- Jiangsu Changjiang Electronics Technology Co Ltd

- King Yuan Electronics Co Ltd

- KLA Corporation

- Kyocera Corporation

- Lam Research Corporation

- LG Chem Ltd

- Mediatek Inc

- Micron Technology Inc

- Powerchip Technology Corporation

- Powertech Technology Inc

- Qualcomm Incorporated

- Resonac Holding Corporation

- Samsung Electronics Co Ltd

- Samsung Foundry (Samsung Electronics Co Ltd)

- Screen Holdings Co Ltd

- Semiconductor Manufacturing International Corporation (SMIC)

- SK Hynix Inc

- Sumitomo Chemical Co Ltd

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- Tianshui Huatian Technology Co Ltd

- Teradyne Inc

- Texas Instruments Incorporated

- Tokyo Electron Limited

- Tongfu Microelectronics Co Ltd

- United Microelectronics Corporation (UMC)

Key Developments in Semiconductor Industry Industry

- May 2023: Micron Technology, Inc. announced its adoption of Extreme Ultraviolet (EUV) technology for its 1-gamma node DRAM production at its Hiroshima fab, making it the first in Japan. Micron anticipates investing up to JPY 500 billion (USD 4.5 billion) in this technology over the coming years, supported by the Japanese government, to drive innovation in generative AI applications.

- March 2023: SK Hynix, a leading memory chip manufacturer, commenced plans for a USD 15 billion semiconductor chip facility in the US. This investment is significantly influenced by the US CHIPS Act, which provides USD 52.7 billion in federal incentives to attract advanced chip production to the United States.

Strategic Semiconductor Industry Market Forecast

The semiconductor industry is poised for sustained and robust growth, driven by an indispensable role in powering technological advancements. Future market expansion will be significantly propelled by the exponential growth of Artificial Intelligence (AI), requiring increasingly sophisticated integrated circuits and semiconductor equipment. The ongoing 5G rollout and the pervasive adoption of the Internet of Things (IoT) will continue to create substantial demand for specialized semiconductor devices. Furthermore, strategic investments by governments worldwide to bolster domestic semiconductor manufacturing capabilities will create new opportunities and reshape global supply chains. The report forecasts the market to exceed $1 Trillion in the coming years, presenting significant opportunities for innovation, expansion, and strategic partnerships across all segments of the semiconductor ecosystem, from fabrication to packaging.

Semiconductor Industry Segmentation

-

1. Semiconductor Devices

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

- 1.4. Integrated Circuits

-

2. Semiconductor Equipment

- 2.1. Front-end Equipment

- 2.2. Back-end Equipment

-

3. Semiconductors Materials

- 3.1. Fabrication

- 3.2. Pacakging

- 4. Semiconductor Foundry Market

- 5. Outso

Semiconductor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Semiconductor Industry Regional Market Share

Geographic Coverage of Semiconductor Industry

Semiconductor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.86% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 5.2.1. Front-end Equipment

- 5.2.2. Back-end Equipment

- 5.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 5.3.1. Fabrication

- 5.3.2. Pacakging

- 5.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 5.5. Market Analysis, Insights and Forecast - by Outso

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia

- 5.6.4. Australia and New Zealand

- 5.6.5. Latin America

- 5.6.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 6. Semiconductor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 6.2.1. Front-end Equipment

- 6.2.2. Back-end Equipment

- 6.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 6.3.1. Fabrication

- 6.3.2. Pacakging

- 6.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 6.5. Market Analysis, Insights and Forecast - by Outso

- 6.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 7. North America Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 7.1.1. Discrete Semiconductors

- 7.1.2. Optoelectronics

- 7.1.3. Sensors

- 7.1.4. Integrated Circuits

- 7.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 7.2.1. Front-end Equipment

- 7.2.2. Back-end Equipment

- 7.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 7.3.1. Fabrication

- 7.3.2. Pacakging

- 7.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 7.5. Market Analysis, Insights and Forecast - by Outso

- 7.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 8. Europe Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 8.1.1. Discrete Semiconductors

- 8.1.2. Optoelectronics

- 8.1.3. Sensors

- 8.1.4. Integrated Circuits

- 8.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 8.2.1. Front-end Equipment

- 8.2.2. Back-end Equipment

- 8.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 8.3.1. Fabrication

- 8.3.2. Pacakging

- 8.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 8.5. Market Analysis, Insights and Forecast - by Outso

- 8.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 9. Asia Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 9.1.1. Discrete Semiconductors

- 9.1.2. Optoelectronics

- 9.1.3. Sensors

- 9.1.4. Integrated Circuits

- 9.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 9.2.1. Front-end Equipment

- 9.2.2. Back-end Equipment

- 9.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 9.3.1. Fabrication

- 9.3.2. Pacakging

- 9.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 9.5. Market Analysis, Insights and Forecast - by Outso

- 9.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 10. Australia and New Zealand Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 10.1.1. Discrete Semiconductors

- 10.1.2. Optoelectronics

- 10.1.3. Sensors

- 10.1.4. Integrated Circuits

- 10.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 10.2.1. Front-end Equipment

- 10.2.2. Back-end Equipment

- 10.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 10.3.1. Fabrication

- 10.3.2. Pacakging

- 10.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 10.5. Market Analysis, Insights and Forecast - by Outso

- 10.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 11. Latin America Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 11.1.1. Discrete Semiconductors

- 11.1.2. Optoelectronics

- 11.1.3. Sensors

- 11.1.4. Integrated Circuits

- 11.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 11.2.1. Front-end Equipment

- 11.2.2. Back-end Equipment

- 11.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 11.3.1. Fabrication

- 11.3.2. Pacakging

- 11.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 11.5. Market Analysis, Insights and Forecast - by Outso

- 11.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 12. Middle East and Africa Semiconductor Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 12.1.1. Discrete Semiconductors

- 12.1.2. Optoelectronics

- 12.1.3. Sensors

- 12.1.4. Integrated Circuits

- 12.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 12.2.1. Front-end Equipment

- 12.2.2. Back-end Equipment

- 12.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 12.3.1. Fabrication

- 12.3.2. Pacakging

- 12.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 12.5. Market Analysis, Insights and Forecast - by Outso

- 12.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Powerchip Technology Corporation

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Henkel AG & Co KGaA

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Lam Research Corporation

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Samsung Foundry (Samsung Electronics Co Ltd)

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Sumitomo Chemical Co Ltd

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Indium Corporation

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Advantest Corporation

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 KLA Corporation

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Teradyne Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Vendor Market Share - Semiconductor Equipment Market

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 United Microelectronics Corporation (UMC)

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Micron Technology Inc

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Tongfu Microelectronics Co Ltd

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Kyocera Corporation

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Applied Materials Inc

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Tianshui Huatian Technology Co Ltd

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 LG Chem Ltd

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 Vendor Market Share - OSAT Marke

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 Samsung Electronics Co Ltd

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.20 ASE Technology Holding Co Ltd

- 13.1.20.1. Company Overview

- 13.1.20.2. Products

- 13.1.20.3. Company Financials

- 13.1.20.4. SWOT Analysis

- 13.1.21 Screen Holdings Co Ltd

- 13.1.21.1. Company Overview

- 13.1.21.2. Products

- 13.1.21.3. Company Financials

- 13.1.21.4. SWOT Analysis

- 13.1.22 Hua Hong Semiconductor Limited

- 13.1.22.1. Company Overview

- 13.1.22.2. Products

- 13.1.22.3. Company Financials

- 13.1.22.4. SWOT Analysis

- 13.1.23 Tokyo Electron Limited

- 13.1.23.1. Company Overview

- 13.1.23.2. Products

- 13.1.23.3. Company Financials

- 13.1.23.4. SWOT Analysis

- 13.1.24 Broadcom Inc

- 13.1.24.1. Company Overview

- 13.1.24.2. Products

- 13.1.24.3. Company Financials

- 13.1.24.4. SWOT Analysis

- 13.1.25 BASF SE

- 13.1.25.1. Company Overview

- 13.1.25.2. Products

- 13.1.25.3. Company Financials

- 13.1.25.4. SWOT Analysis

- 13.1.26 Vendor Market Share - Semiconductor Devices Market

- 13.1.26.1. Company Overview

- 13.1.26.2. Products

- 13.1.26.3. Company Financials

- 13.1.26.4. SWOT Analysis

- 13.1.27 Jiangsu Changjiang Electronics Technology Co Ltd

- 13.1.27.1. Company Overview

- 13.1.27.2. Products

- 13.1.27.3. Company Financials

- 13.1.27.4. SWOT Analysis

- 13.1.28 Qualcomm Incorporated

- 13.1.28.1. Company Overview

- 13.1.28.2. Products

- 13.1.28.3. Company Financials

- 13.1.28.4. SWOT Analysis

- 13.1.29 Semiconductor Manufacturing International Corporation (SMIC)

- 13.1.29.1. Company Overview

- 13.1.29.2. Products

- 13.1.29.3. Company Financials

- 13.1.29.4. SWOT Analysis

- 13.1.30 SK Hynix Inc

- 13.1.30.1. Company Overview

- 13.1.30.2. Products

- 13.1.30.3. Company Financials

- 13.1.30.4. SWOT Analysis

- 13.1.31 ASML Holding NV

- 13.1.31.1. Company Overview

- 13.1.31.2. Products

- 13.1.31.3. Company Financials

- 13.1.31.4. SWOT Analysis

- 13.1.32 Texas Instruments Incorporated

- 13.1.32.1. Company Overview

- 13.1.32.2. Products

- 13.1.32.3. Company Financials

- 13.1.32.4. SWOT Analysis

- 13.1.33 Powertech Technology Inc

- 13.1.33.1. Company Overview

- 13.1.33.2. Products

- 13.1.33.3. Company Financials

- 13.1.33.4. SWOT Analysis

- 13.1.34 King Yuan Electronics Co Ltd7 2 Vendor Market Share

- 13.1.34.1. Company Overview

- 13.1.34.2. Products

- 13.1.34.3. Company Financials

- 13.1.34.4. SWOT Analysis

- 13.1.35 Resonac Holding Corporation

- 13.1.35.1. Company Overview

- 13.1.35.2. Products

- 13.1.35.3. Company Financials

- 13.1.35.4. SWOT Analysis

- 13.1.36 Amkor Technology Inc

- 13.1.36.1. Company Overview

- 13.1.36.2. Products

- 13.1.36.3. Company Financials

- 13.1.36.4. SWOT Analysis

- 13.1.37 Vendor Market Share - Semiconductor Foundry Market

- 13.1.37.1. Company Overview

- 13.1.37.2. Products

- 13.1.37.3. Company Financials

- 13.1.37.4. SWOT Analysis

- 13.1.38 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 13.1.38.1. Company Overview

- 13.1.38.2. Products

- 13.1.38.3. Company Financials

- 13.1.38.4. SWOT Analysis

- 13.1.39 Intel Corporation

- 13.1.39.1. Company Overview

- 13.1.39.2. Products

- 13.1.39.3. Company Financials

- 13.1.39.4. SWOT Analysis

- 13.1.40 GlobalFoundries Inc

- 13.1.40.1. Company Overview

- 13.1.40.2. Products

- 13.1.40.3. Company Financials

- 13.1.40.4. SWOT Analysis

- 13.1.41 Dow Chemical Co (Dow Inc )

- 13.1.41.1. Company Overview

- 13.1.41.2. Products

- 13.1.41.3. Company Financials

- 13.1.41.4. SWOT Analysis

- 13.1.42 Mediatek Inc

- 13.1.42.1. Company Overview

- 13.1.42.2. Products

- 13.1.42.3. Company Financials

- 13.1.42.4. SWOT Analysis

- 13.1.1 Powerchip Technology Corporation

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Semiconductor Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Semiconductor Industry Share (%) by Company 2025

List of Tables

- Table 1: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 2: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 3: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 4: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 5: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 6: Semiconductor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 8: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 9: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 10: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 11: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 12: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 14: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 15: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 16: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 17: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 18: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 20: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 21: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 22: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 23: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 24: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 26: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 27: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 28: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 29: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 30: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 32: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 33: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 34: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 35: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 36: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2020 & 2033

- Table 38: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2020 & 2033

- Table 39: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2020 & 2033

- Table 40: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2020 & 2033

- Table 41: Semiconductor Industry Revenue Million Forecast, by Outso 2020 & 2033

- Table 42: Semiconductor Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Industry?

The projected CAGR is approximately 10.86%.

2. Which companies are prominent players in the Semiconductor Industry?

Key companies in the market include Powerchip Technology Corporation, Henkel AG & Co KGaA, Lam Research Corporation, Samsung Foundry (Samsung Electronics Co Ltd), Sumitomo Chemical Co Ltd, Indium Corporation, Advantest Corporation, KLA Corporation, Teradyne Inc, Vendor Market Share - Semiconductor Equipment Market, United Microelectronics Corporation (UMC), Micron Technology Inc, Tongfu Microelectronics Co Ltd, Kyocera Corporation, Applied Materials Inc, Tianshui Huatian Technology Co Ltd, LG Chem Ltd, Vendor Market Share - OSAT Marke, Samsung Electronics Co Ltd, ASE Technology Holding Co Ltd, Screen Holdings Co Ltd, Hua Hong Semiconductor Limited, Tokyo Electron Limited, Broadcom Inc, BASF SE, Vendor Market Share - Semiconductor Devices Market, Jiangsu Changjiang Electronics Technology Co Ltd, Qualcomm Incorporated, Semiconductor Manufacturing International Corporation (SMIC), SK Hynix Inc, ASML Holding NV, Texas Instruments Incorporated, Powertech Technology Inc, King Yuan Electronics Co Ltd7 2 Vendor Market Share, Resonac Holding Corporation, Amkor Technology Inc, Vendor Market Share - Semiconductor Foundry Market, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, GlobalFoundries Inc, Dow Chemical Co (Dow Inc ), Mediatek Inc.

3. What are the main segments of the Semiconductor Industry?

The market segments include Semiconductor Devices, Semiconductor Equipment, Semiconductors Materials, Semiconductor Foundry Market, Outso.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Needs of Consumer Electronic Devices Boosting the Manufacturing Prospects; Proliferation of AI. IoT. and Connected Devices Across Industry Verticals; Increased Applications of Semiconductors in Automotive; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Discrete Semiconductors to Hold Significant Market Share in the Semiconductor Devices Segment.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions Resulting in Semiconductor Chip Shortage; Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment; Vertical Integration is One of the Significant Concerns of OSAT Players.

8. Can you provide examples of recent developments in the market?

May 2023: Micron Technology, Inc. announced its adoption of Extreme Ultraviolet (EUV) technology, a sophisticated patterning technique for producing its 1-gamma node DRAM. Given the pivotal role of its Hiroshima fab in advancing the 1-gamma node, Micron became the first semiconductor manufacturer to introduce EUV technology to Japan for manufacturing purposes. Over the upcoming years, Micron anticipates investing up to JPY 500 billion (USD 4.5 billion) in 1-gamma process technology. Supported by the Japanese government, this investment aims to fuel the next wave of end-to-end technological innovation, especially in the rapidly evolving field of generative artificial intelligence (AI) applications."

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence