Key Insights

The Poland Life and Non-Life Insurance Market is projected for significant expansion, anticipating a Compound Annual Growth Rate (CAGR) of 7.19% between 2025 and 2033. This growth trajectory is propelled by rising disposable incomes, heightened risk management awareness among Polish consumers, and government-led financial inclusion initiatives. Digital distribution channels further enhance market accessibility. The market encompasses life, health, motor, and property insurance, distributed through online platforms, agents, and brokers. Key players include Powszechny Zakład Ubezpieczen SA, Ergo Hestia SA, Warta SA, Uniqa SA, Generali SA, Compensa SA, Interrisk SA, Aviva SA, and Wiener SA. The competitive environment is evolving with the rise of Insurtech and innovative offerings. Despite economic fluctuations and regulatory considerations, sustained economic growth and a burgeoning middle class ensure a positive market outlook.

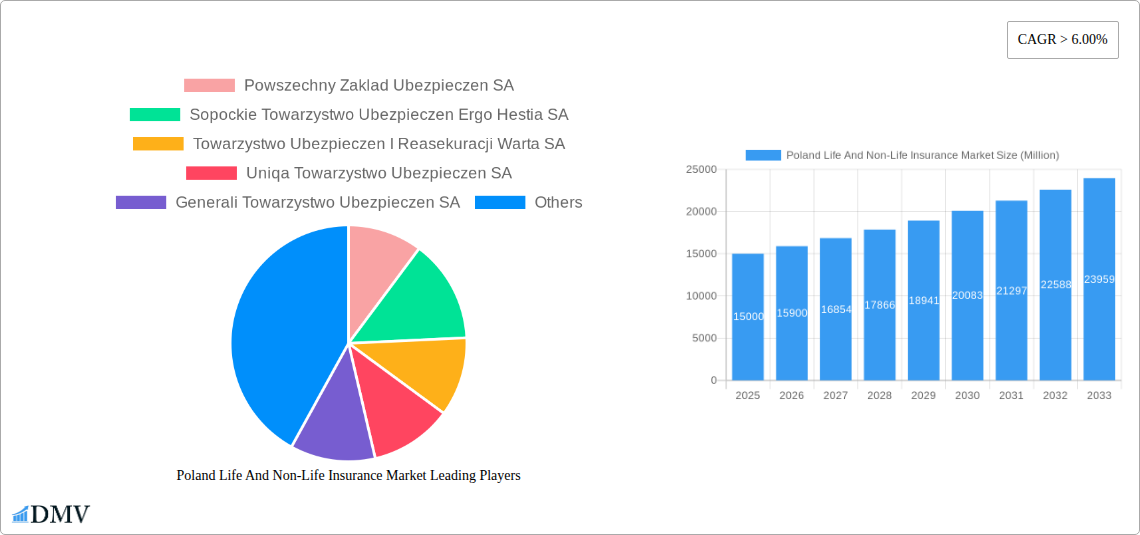

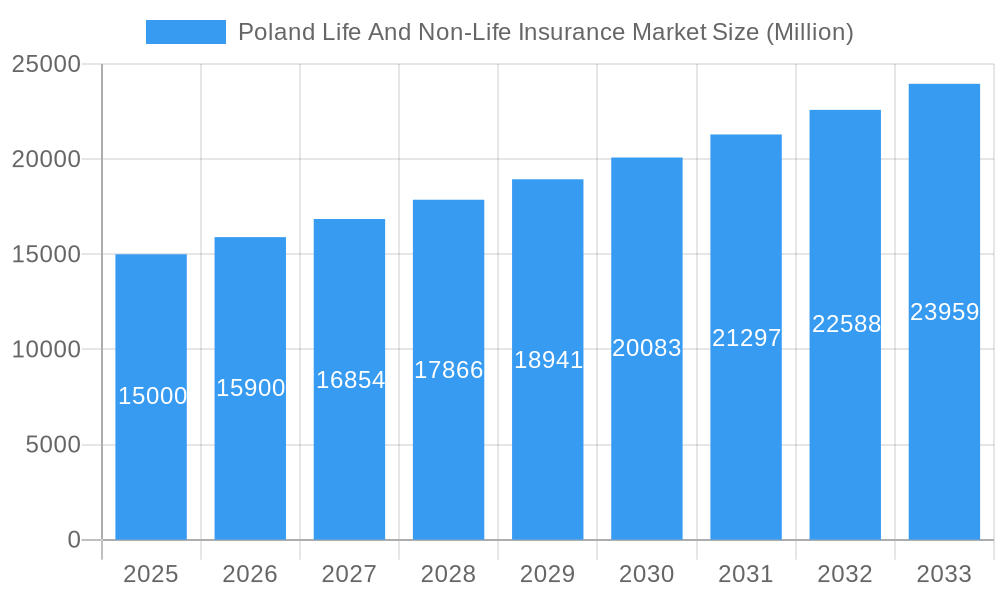

Poland Life And Non-Life Insurance Market Market Size (In Billion)

Continued growth in the Polish insurance sector is supported by urbanization, an aging population's demand for health and long-term care coverage, and the increasing availability of cost-effective insurance solutions. This presents substantial investment opportunities. Potential challenges include insurance fraud and the necessity for improved customer education to foster trust and transparency. Intense competition demands ongoing digital transformation and product customization to meet evolving consumer needs. The 2025-2033 forecast period offers a prime growth opportunity. Detailed regional analysis of urban and rural demographics will provide deeper market insights.

Poland Life And Non-Life Insurance Market Company Market Share

Poland Life and Non-Life Insurance Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the Poland Life and Non-Life Insurance Market, offering a comprehensive overview of its current state, future trajectory, and key players. With a study period spanning 2019-2033, a base year of 2025, and a forecast period from 2025-2033, this report is an indispensable resource for stakeholders seeking to understand and capitalize on opportunities within this dynamic market. The report meticulously examines market size, segmentation, competitive landscape, and emerging trends, offering valuable insights for strategic decision-making. All financial values are presented in Millions.

Poland Life And Non-Life Insurance Market Market Composition & Trends

This section delves into the intricate composition and evolving trends within the Polish life and non-life insurance market. We analyze market concentration, revealing the dominance of key players and their respective market shares. Innovation catalysts, including technological advancements and regulatory changes, are examined alongside their impact on market dynamics. The regulatory landscape, including its impact on market growth and competition, is meticulously assessed. We explore substitute products and their influence on market share, along with a detailed analysis of end-user profiles and their evolving insurance needs. Finally, we investigate mergers and acquisitions (M&A) activities, providing data on deal values and their strategic implications. The report also includes an in-depth examination of the impact of these M&A deals, with data on their size and strategic implications (xx Million in total M&A deal value for the period 2019-2024).

- Market Share Distribution: Powszechny Zakład Ubezpieczeń SA holds an estimated xx% market share, followed by Warta SA with xx%, Ergo Hestia SA with xx%, and other players. The distribution is expected to shift slightly by 2033, with increased competition from digital insurers.

- M&A Activity: Significant M&A activity has been observed in recent years, with transactions totaling approximately xx Million during 2019-2024. Future M&A activity is predicted to focus on consolidation and expansion into digital services.

- Regulatory Landscape: The Polish Financial Supervision Authority (KNF) plays a key role in shaping market dynamics, with regulations focused on consumer protection and financial stability.

- Innovation Catalysts: Digitalization, personalized insurance offerings, and the rising demand for innovative risk management solutions are key innovation drivers.

Poland Life And Non-Life Insurance Market Industry Evolution

This section provides a comprehensive overview of the evolutionary path of Poland's life and non-life insurance market. We meticulously chart market growth trajectories, pinpointing key periods of expansion and contraction. Technological advancements, such as the rise of InsurTech and digital distribution channels, are deeply examined, alongside their impact on consumer behavior and industry efficiency. The evolving demands of consumers, including preferences for personalized products and enhanced customer service, are also thoroughly analyzed. The sector witnessed a Compound Annual Growth Rate (CAGR) of xx% between 2019 and 2024, with projections of a xx% CAGR from 2025-2033. This growth is fueled by increasing insurance awareness, rising disposable incomes, and expanding digital adoption across different consumer segments.

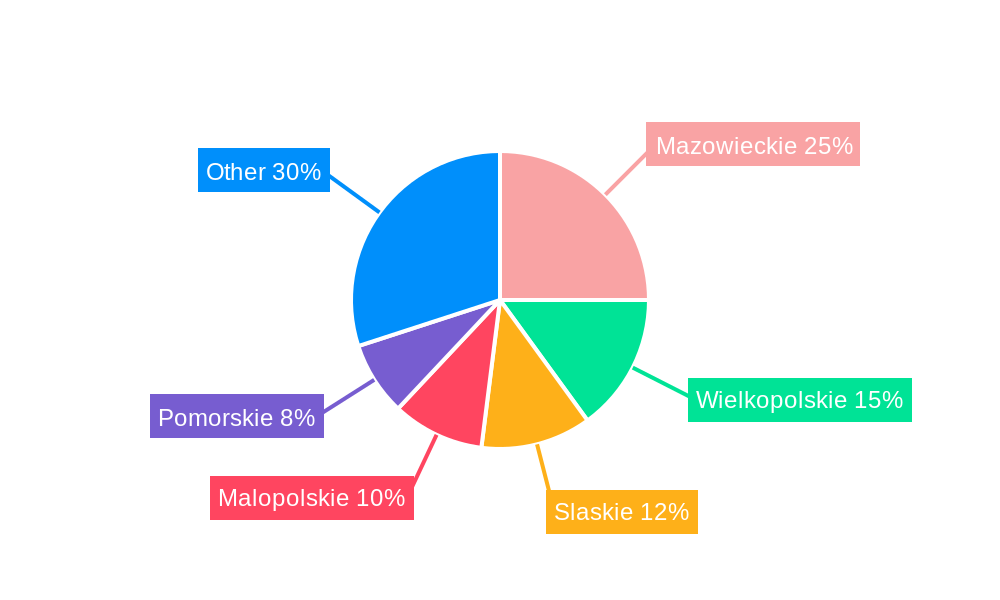

Leading Regions, Countries, or Segments in Poland Life And Non-Life Insurance Market

This section identifies the dominant regions, countries, or segments within the Polish life and non-life insurance market. Detailed analysis provides a deep understanding of the factors driving this dominance. We also consider growth potential in other regions or segments. The urban areas of major cities like Warsaw, Krakow, and Gdansk constitute the most dominant segments, contributing to a significant percentage of the market’s overall revenue.

- Key Drivers of Urban Area Dominance:

- Higher disposable incomes and increased insurance awareness.

- Greater access to technology and digital distribution channels.

- Concentrated population density, facilitating cost-effective operations.

- Stringent regulatory frameworks driving industry standards.

The dominance of urban areas is expected to persist throughout the forecast period due to continued economic growth and technological advancements, but a steady increase in penetration in rural areas is projected.

Poland Life And Non-Life Insurance Market Product Innovations

This section explores the landscape of product innovation within the Polish insurance market, focusing on specific examples of novel products and services. The report analyses the unique selling propositions (USPs) of these innovations and evaluates their performance metrics. Key trends include the rise of digital-first products and personalized offerings catered to specific customer needs, with a growing emphasis on technological integration for enhanced customer experiences. These innovations are largely driven by digitalization and the increasing demand for personalized services, leading to more efficient and customer-centric product offerings.

Propelling Factors for Poland Life And Non-Life Insurance Market Growth

Several key factors are driving the growth of the Polish life and non-life insurance market. These include increasing government initiatives promoting financial inclusion, technological advancements enabling efficient and personalized offerings, improving financial literacy among citizens, and rising demand for insurance driven by a growing middle class. The macroeconomic environment, characterized by steady GDP growth and increasing disposable incomes, also supports market expansion.

Obstacles in the Poland Life And Non-Life Insurance Market Market

Despite significant growth potential, the Polish insurance market faces several challenges. These include regulatory hurdles that impact operational efficiency and product development, heightened competitive pressures from both domestic and international players, and the need to address consumer trust issues. Economic fluctuations also present a risk, impacting consumer spending and insurance demand.

Future Opportunities in Poland Life And Non-Life Insurance Market

The future of the Polish life and non-life insurance market presents substantial growth opportunities. Untapped market segments, especially in rural areas, offer immense potential. Technological advancements, such as AI and big data analytics, can further enhance operational efficiency, personalization, and risk assessment. The expanding digital ecosystem and the rising adoption of mobile and online channels for insurance sales present significant opportunities for innovation.

Major Players in the Poland Life And Non-Life Insurance Market Ecosystem

- Powszechny Zakład Ubezpieczeń SA

- Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- Towarzystwo Ubezpieczeń I Reasekuracji Warta SA

- Uniqa Towarzystwo Ubezpieczen SA

- Generali Towarzystwo Ubezpieczen SA

- Compensa Towarzystwo Ubezpieczen SA

- Interrisk Towarzystwo Ubezpieczen SA

- Aviva Towarzystwo Ubezpieczen Na Zycie SA

- Wiener Towarzystwo Ubezpieczen SA

- Ergo Hestia SA

Key Developments in Poland Life And Non-Life Insurance Market Industry

- May 2023: Generali reaches agreement to dispose of Generali Deutschland Pensionskasse to Frankfurter Leben. This divestiture is expected to streamline Generali's operations and focus resources on core markets.

- March 2023: Allianz Polska launches a fully digital process for selling individual life insurance policies. This innovation significantly enhances customer experience and operational efficiency.

Strategic Poland Life And Non-Life Insurance Market Market Forecast

The Polish life and non-life insurance market is poised for robust growth driven by factors such as increasing penetration rates, evolving consumer needs, and technological advancements. Continued digital transformation and the expansion of product offerings to cater to the diversifying needs of the Polish population will significantly influence future market expansion. The market is expected to witness strong growth in the coming years, exceeding xx Million by 2033.

Poland Life And Non-Life Insurance Market Segmentation

-

1. Insurance Type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non Life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Others

-

1.1. Life Insurance

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Others

Poland Life And Non-Life Insurance Market Segmentation By Geography

- 1. Poland

Poland Life And Non-Life Insurance Market Regional Market Share

Geographic Coverage of Poland Life And Non-Life Insurance Market

Poland Life And Non-Life Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non Life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Others

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Poland Life And Non-Life Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6.1.1. Life Insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non Life Insurance

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Others

- 6.1.1. Life Insurance

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Powszechny Zaklad Ubezpieczen SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Towarzystwo Ubezpieczen I Reasekuracji Warta SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Uniqa Towarzystwo Ubezpieczen SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Generali Towarzystwo Ubezpieczen SA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Compensa Towarzystwo Ubezpieczen SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Interrisk Towarzystwo Ubezpieczen SA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Aviva Towarzystwo Ubezpieczen Na Zycie SA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Wiener Towarzystwo Ubezpieczen SA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Ergo Hestia SA**List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Powszechny Zaklad Ubezpieczen SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Poland Life And Non-Life Insurance Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Life And Non-Life Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Insurance Type 2020 & 2033

- Table 2: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Insurance Type 2020 & 2033

- Table 5: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Poland Life And Non-Life Insurance Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Life And Non-Life Insurance Market?

The projected CAGR is approximately 7.19%.

2. Which companies are prominent players in the Poland Life And Non-Life Insurance Market?

Key companies in the market include Powszechny Zaklad Ubezpieczen SA, Sopockie Towarzystwo Ubezpieczen Ergo Hestia SA, Towarzystwo Ubezpieczen I Reasekuracji Warta SA, Uniqa Towarzystwo Ubezpieczen SA, Generali Towarzystwo Ubezpieczen SA, Compensa Towarzystwo Ubezpieczen SA, Interrisk Towarzystwo Ubezpieczen SA, Aviva Towarzystwo Ubezpieczen Na Zycie SA, Wiener Towarzystwo Ubezpieczen SA, Ergo Hestia SA**List Not Exhaustive.

3. What are the main segments of the Poland Life And Non-Life Insurance Market?

The market segments include Insurance Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Tax Benefits and Incentives; Changing Risk Perception; Increasing Motorization.

6. What are the notable trends driving market growth?

Non Life Insurance Policies Generate Higher Premium Revenue in Poland.

7. Are there any restraints impacting market growth?

Tax Benefits and Incentives; Changing Risk Perception; Increasing Motorization.

8. Can you provide examples of recent developments in the market?

May 2023: Generali reaches agreement to dispose of Generali Deutschland Pensionskasse to Frankfurter Leben

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Life And Non-Life Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Life And Non-Life Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Life And Non-Life Insurance Market?

To stay informed about further developments, trends, and reports in the Poland Life And Non-Life Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence