Key Insights

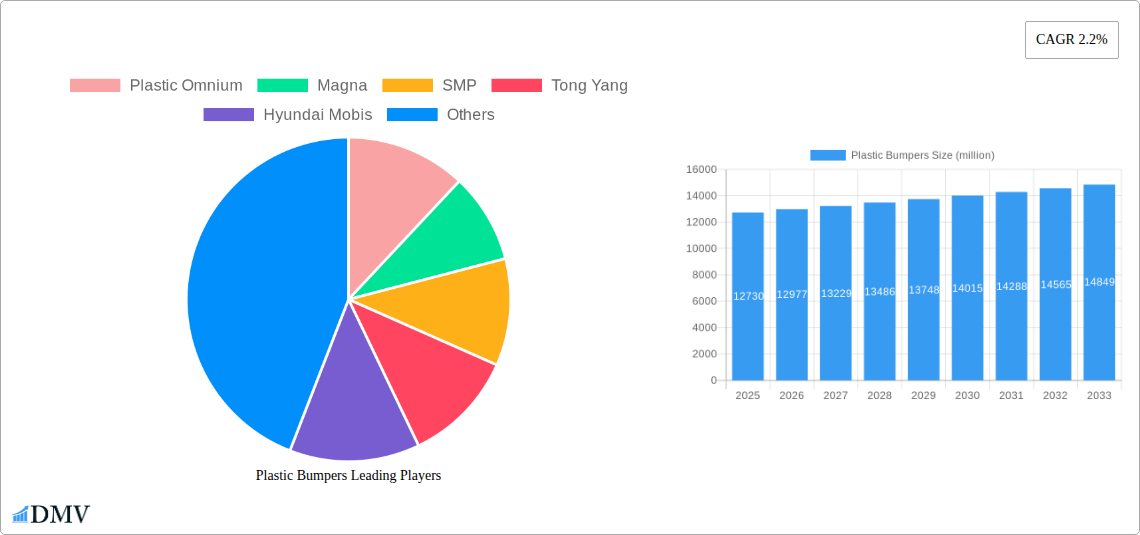

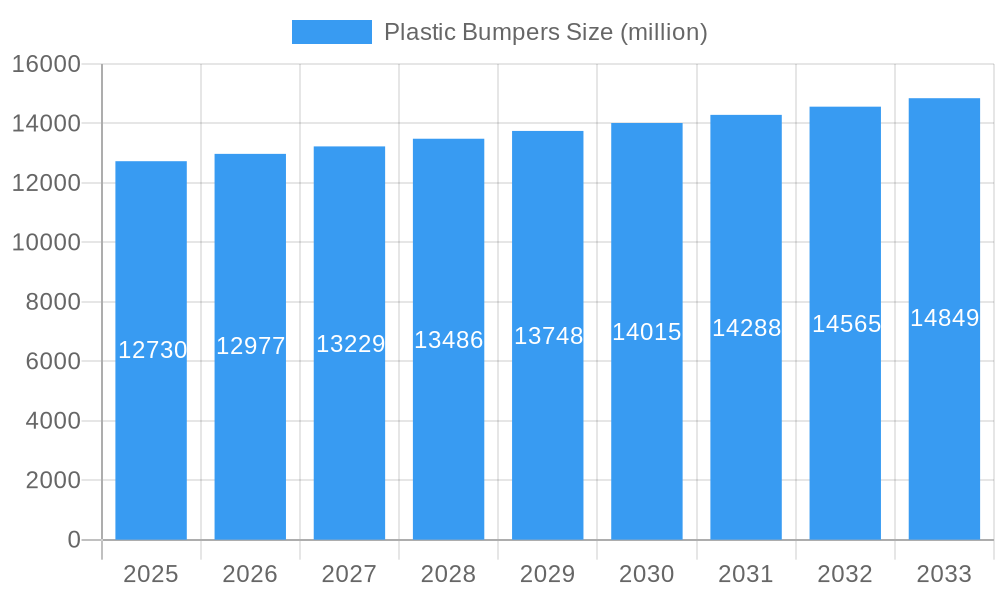

The global plastic bumpers market is poised for steady expansion, projected to reach a substantial valuation of USD 12,730 million. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 2.2% from 2025 to 2033. A primary driver for this market's ascent is the continuous innovation in automotive design, where plastic bumpers offer a compelling combination of lightweight construction, enhanced safety features, and improved aerodynamic efficiency compared to traditional metal alternatives. The increasing demand for fuel-efficient vehicles, both passenger and commercial, directly fuels the adoption of these lighter materials, contributing significantly to the market's positive trajectory. Furthermore, ongoing advancements in polymer technology are enabling the production of more durable, impact-resistant, and aesthetically versatile plastic bumpers, meeting the evolving preferences of automotive manufacturers and consumers alike. The market's segmentation by application into Passenger Vehicles and Commercial Vehicles, and by type into Front Bumpers and Rear Bumpers, highlights the pervasive integration of plastic bumpers across the entire automotive spectrum.

Plastic Bumpers Market Size (In Billion)

The market's future expansion is also influenced by evolving regulatory landscapes and consumer expectations regarding vehicle safety and sustainability. Manufacturers are increasingly investing in research and development to create advanced composite materials that not only meet stringent safety standards but also contribute to a reduced environmental footprint through recyclability and lower manufacturing energy requirements. Key regions such as Asia Pacific, particularly China and India, are expected to exhibit robust growth due to the burgeoning automotive production and increasing per capita income, leading to higher vehicle sales. Europe and North America will continue to be significant markets, driven by a strong focus on advanced safety features and the ongoing trend towards electric and hybrid vehicles, where weight reduction is a critical factor for optimizing range. Leading companies like Plastic Omnium, Magna, and SMP are at the forefront of this innovation, continuously introducing new solutions and expanding their production capacities to cater to the growing global demand for sophisticated and high-performance plastic bumper systems.

Plastic Bumpers Company Market Share

Plastic Bumpers Market Composition & Trends

The global plastic bumpers market is characterized by a moderately consolidated landscape, with key players like Plastic Omnium and Magna holding significant market share, estimated at over $XX million and $XX million respectively. Innovation remains a crucial catalyst, driven by advancements in material science for lightweighting and enhanced impact resistance. Regulatory landscapes, particularly concerning pedestrian safety and emissions reduction, are increasingly shaping product development and material choices. Substitute products, such as composite or metal alternatives, present a limited but evolving competitive threat, primarily in niche applications. End-user profiles are dominated by the automotive industry, with passenger vehicles representing the largest segment, followed by commercial vehicles. Mergers and acquisitions (M&A) activity, though not consistently high, has been strategic, with deals valued in the tens of millions to hundreds of millions of dollars aimed at expanding geographic reach or technological capabilities.

- Market Share Distribution (Estimated):

- Plastic Omnium: XX% (valued at approximately $XX million)

- Magna: XX% (valued at approximately $XX million)

- SMP: XX% (valued at approximately $XX million)

- Tong Yang: XX% (valued at approximately $XX million)

- Hyundai Mobis: XX% (valued at approximately $XX million)

- Key Innovation Catalysts:

- Development of advanced polymers for weight reduction.

- Integration of sensor technologies for advanced driver-assistance systems (ADAS).

- Focus on sustainable materials and manufacturing processes.

- M&A Activity Drivers:

- Geographic expansion into emerging automotive markets.

- Acquisition of specialized technological capabilities.

- Consolidation to achieve economies of scale.

Plastic Bumpers Industry Evolution

The plastic bumpers industry has witnessed a dynamic evolution driven by the relentless pursuit of automotive efficiency, safety, and aesthetics. Over the historical period of 2019–2024, the market experienced steady growth, with an estimated Compound Annual Growth Rate (CAGR) of approximately XX% during this phase. This trajectory was primarily propelled by the increasing global production of vehicles, particularly in emerging economies. The base year of 2025 marks a pivotal point, with the market poised for accelerated expansion. Technological advancements have been instrumental in this evolution. The shift from traditional materials to advanced polymers like polypropylene (PP), thermoplastic polyurethanes (TPU), and acrylonitrile butadiene styrene (ABS) has enabled lighter, more durable, and design-flexible bumpers. These material innovations are critical for meeting stringent fuel efficiency standards and enhancing vehicle performance. Furthermore, the integration of bumpers with active aerodynamic elements and advanced sensor housings for ADAS has transformed them from passive safety components into integral parts of a vehicle's intelligent systems. Consumer demand has also played a significant role, with a growing preference for vehicles that offer sophisticated styling and advanced safety features, both of which are heavily influenced by bumper design and technology. The estimated market size for plastic bumpers in 2025 is projected to reach a substantial $XX million, underscoring the sector's importance. The forecast period of 2025–2033 anticipates a sustained and robust growth trajectory, with an estimated CAGR of XX%, reaching an impressive $XX million by 2033. This growth is expected to be fueled by further advancements in smart bumper technologies, the increasing adoption of electric vehicles (EVs) which often feature optimized aerodynamic designs, and the continuous demand for lightweighting solutions to improve overall vehicle efficiency.

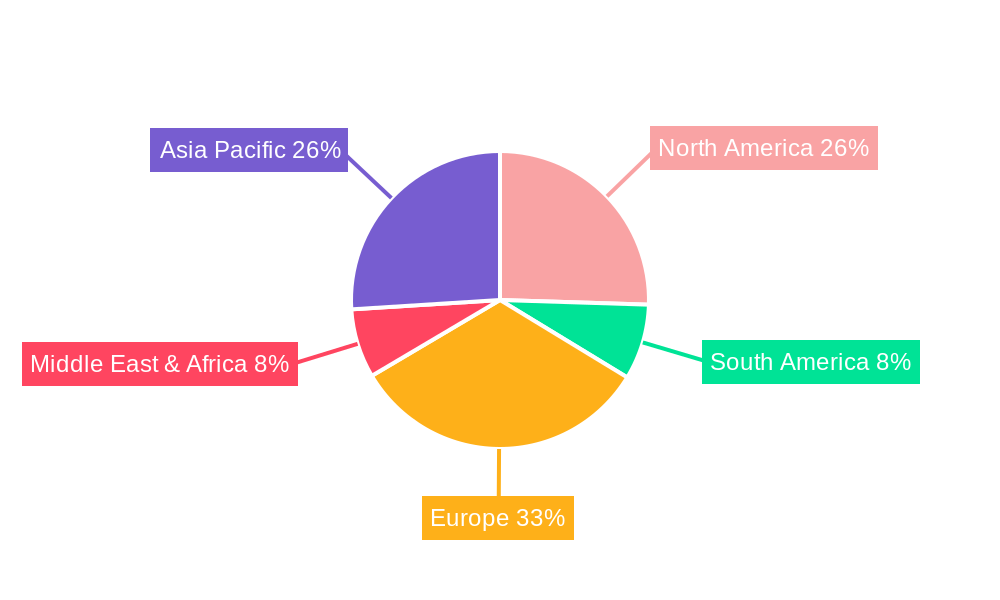

Leading Regions, Countries, or Segments in Plastic Bumpers

The global plastic bumpers market exhibits clear regional dominance and segment leadership, driven by a confluence of manufacturing prowess, vehicle production volumes, and evolving automotive trends. Asia Pacific stands out as the leading region, propelled by the sheer scale of automotive manufacturing in countries like China and India. This dominance is further bolstered by the presence of major automotive hubs and a burgeoning domestic demand for vehicles. Within this region, China alone accounts for a significant portion of global plastic bumper production and consumption, estimated at over XX million units annually.

The application segment of Passenger Vehicles overwhelmingly leads the market. This is attributed to the higher production volumes of passenger cars globally compared to commercial vehicles. Passenger cars are a primary focus for automotive manufacturers seeking to incorporate advanced design aesthetics, safety features, and lightweighting solutions, all of which are strengths of plastic bumpers. The demand for enhanced fuel efficiency and the integration of advanced driver-assistance systems (ADAS) further solidify the passenger vehicle segment's lead.

Within the types of bumpers, the Front Bumper segment is consistently the largest. This is a direct consequence of its critical role in vehicle safety, particularly in collision scenarios. Front bumpers are designed to absorb impact energy, protect pedestrians, and house essential components like headlights, grille elements, and sensor arrays. Their complexity and design freedom offered by plastics make them the preferred choice for this vital application. The rear bumper segment, while significant, typically follows behind the front bumper in market share due to its primary function of impact absorption and aesthetic integration.

- Dominant Region: Asia Pacific

- Key Drivers:

- Largest automotive manufacturing base globally, particularly in China.

- High domestic vehicle sales volume in emerging economies.

- Strong presence of key plastic bumper manufacturers.

- Government initiatives supporting automotive manufacturing and R&D.

- In-depth Analysis: Asia Pacific's leadership is a result of its unparalleled capacity for vehicle production. Countries like China, India, and South Korea are not only major production hubs but also significant consumer markets. The region's automotive supply chain is well-developed, facilitating the efficient production and distribution of plastic bumpers for both domestic and export markets.

- Key Drivers:

- Dominant Application Segment: Passenger Vehicle

- Key Drivers:

- Higher global production volumes of passenger cars.

- Demand for lightweighting to improve fuel efficiency and EV range.

- Integration of aesthetic design elements and advanced safety features.

- Increasing adoption of ADAS requiring complex bumper integration.

- In-depth Analysis: Passenger vehicles represent the largest segment due to their widespread appeal and the continuous innovation in design and technology. Manufacturers prioritize enhancing the appeal and safety of passenger cars, making plastic bumpers an ideal solution due to their moldability and cost-effectiveness for complex shapes.

- Key Drivers:

- Dominant Type: Front Bumper

- Key Drivers:

- Primary safety component for impact absorption and pedestrian protection.

- Housing for headlights, grille, and crucial ADAS sensors.

- Design freedom for aerodynamic and aesthetic integration.

- In-depth Analysis: The front bumper's multifaceted role in vehicle safety and technology integration makes it the most significant type. Its design is crucial for meeting safety regulations and incorporating advanced functionalities, leading to a higher demand and complexity compared to other bumper types.

- Key Drivers:

Plastic Bumpers Product Innovations

Recent product innovations in the plastic bumpers market are heavily focused on enhancing vehicle safety, reducing weight, and integrating smart technologies. Manufacturers are developing bumpers using advanced composite materials and reinforced polymers that offer superior impact absorption while being significantly lighter than traditional materials, contributing to improved fuel efficiency and EV range. Innovations also include the seamless integration of sensors for advanced driver-assistance systems (ADAS), enabling features like adaptive cruise control and automatic emergency braking. Furthermore, there is a growing trend towards modular bumper designs that allow for easier repair and customization, as well as the incorporation of sustainable and recycled plastics to meet environmental regulations and consumer demand for eco-friendly vehicles. These advancements are crucial for maintaining competitiveness and meeting the evolving demands of the automotive industry.

Propelling Factors for Plastic Bumpers Growth

The growth of the plastic bumpers market is propelled by several key factors. Foremost is the increasing global automotive production, particularly in emerging economies, which directly translates to higher demand for vehicle components. The continuous push for lightweighting in the automotive industry, driven by stringent fuel economy regulations and the expansion of electric vehicles, favors the use of plastics over heavier traditional materials. Furthermore, the evolving safety standards and the increasing integration of ADAS technologies necessitate sophisticated bumper designs, which plastics are adept at providing. Economic recovery and rising disposable incomes in many regions also contribute to increased vehicle sales.

Obstacles in the Plastic Bumpers Market

Despite robust growth prospects, the plastic bumpers market faces certain obstacles. Volatile raw material prices, particularly for petrochemical-derived plastics, can impact manufacturing costs and profitability. Increasing regulatory scrutiny concerning the recyclability and end-of-life management of plastics, along with the potential for microplastic pollution, poses a challenge. Supply chain disruptions, as witnessed in recent global events, can lead to production delays and increased lead times. Intense competition among numerous manufacturers also exerts downward pressure on pricing.

Future Opportunities in Plastic Bumpers

Emerging opportunities in the plastic bumpers market are significant and diverse. The accelerating adoption of electric vehicles presents a major avenue for growth, as EVs often require optimized aerodynamic designs and lightweight components, where plastic bumpers excel. The development and widespread adoption of autonomous driving technologies will further drive demand for bumpers integrated with advanced sensor arrays and radar systems. Expansion into untapped emerging automotive markets and the increasing demand for aftermarket and customization solutions also offer substantial growth potential.

Major Players in the Plastic Bumpers Ecosystem

- Plastic Omnium

- Magna

- SMP

- Tong Yang

- Hyundai Mobis

- KIRCHHOFF

- HuaYu Automotive

- Seoyon E-Hwa

- Flex-N-Gate

- Toyoda Gosei

- Jiangnan MPT

- Rehau

- Ecoplastic

- Zhejiang Yuanchi

Key Developments in Plastic Bumpers Industry

- 2023 October: Plastic Omnium announces a new sustainable bumper production facility in Europe, focusing on recycled materials.

- 2023 July: Magna invests $XX million in advanced composite bumper technology for next-generation vehicles.

- 2023 March: SMP launches a lightweight bumper system incorporating integrated sensor technology for enhanced ADAS functionality.

- 2022 December: Hyundai Mobis unveils an innovative front bumper design optimized for EV aerodynamics and pedestrian safety.

- 2022 September: HuaYu Automotive expands its production capacity for plastic bumpers in Southeast Asia to meet growing regional demand.

- 2022 May: Toyoda Gosei develops a new generation of high-impact resistant plastic bumpers using advanced polymer blends.

Strategic Plastic Bumpers Market Forecast

The strategic outlook for the plastic bumpers market remains exceptionally strong, driven by a confluence of accelerating automotive trends. The unwavering demand for lightweighting to enhance fuel efficiency and extend EV range will continue to favor plastic solutions. The rapid evolution and integration of advanced driver-assistance systems (ADAS) and the eventual shift towards autonomous driving will necessitate increasingly complex and technologically advanced bumper designs, a forte of plastic manufacturing. Furthermore, a growing global middle class and continued urbanization in emerging markets are projected to sustain robust vehicle production growth. Investments in sustainable materials and circular economy principles are also anticipated to open new market segments and solidify the industry's long-term viability.

Plastic Bumpers Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Front Bumper

- 2.2. Rear Bumper

Plastic Bumpers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plastic Bumpers Regional Market Share

Geographic Coverage of Plastic Bumpers

Plastic Bumpers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Front Bumper

- 5.2.2. Rear Bumper

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Front Bumper

- 6.2.2. Rear Bumper

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Front Bumper

- 7.2.2. Rear Bumper

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Front Bumper

- 8.2.2. Rear Bumper

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Front Bumper

- 9.2.2. Rear Bumper

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Plastic Bumpers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Front Bumper

- 10.2.2. Rear Bumper

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Plastic Omnium

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Magna

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SMP

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Tong Yang

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hyundai Mobis

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 KIRCHHOFF

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 HuaYu Automotive

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Seoyon E-Hwa

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Flex-N-Gate

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Toyoda Gosei

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jiangnan MPT

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Rehau

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Ecoplastic

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zhejiang Yuanchi

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Plastic Omnium

List of Figures

- Figure 1: Global Plastic Bumpers Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Plastic Bumpers Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Plastic Bumpers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Plastic Bumpers Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Plastic Bumpers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Plastic Bumpers Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Plastic Bumpers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Plastic Bumpers Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Plastic Bumpers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Plastic Bumpers Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Plastic Bumpers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Plastic Bumpers Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Plastic Bumpers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Plastic Bumpers Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Plastic Bumpers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Plastic Bumpers Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Plastic Bumpers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Plastic Bumpers Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Plastic Bumpers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Plastic Bumpers Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Plastic Bumpers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Plastic Bumpers Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Plastic Bumpers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Plastic Bumpers Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Plastic Bumpers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Plastic Bumpers Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Plastic Bumpers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Plastic Bumpers Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Plastic Bumpers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Plastic Bumpers Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Plastic Bumpers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Plastic Bumpers Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Plastic Bumpers Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Plastic Bumpers Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Plastic Bumpers Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Plastic Bumpers Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Plastic Bumpers Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Plastic Bumpers Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Plastic Bumpers Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Plastic Bumpers Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plastic Bumpers?

The projected CAGR is approximately 2.4%.

2. Which companies are prominent players in the Plastic Bumpers?

Key companies in the market include Plastic Omnium, Magna, SMP, Tong Yang, Hyundai Mobis, KIRCHHOFF, HuaYu Automotive, Seoyon E-Hwa, Flex-N-Gate, Toyoda Gosei, Jiangnan MPT, Rehau, Ecoplastic, Zhejiang Yuanchi.

3. What are the main segments of the Plastic Bumpers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plastic Bumpers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plastic Bumpers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plastic Bumpers?

To stay informed about further developments, trends, and reports in the Plastic Bumpers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence