Key Insights

The European coal market, despite the global transition to renewables, retains significant presence in power generation and industrial sectors. The market, valued at 42.6 billion in 2025, is projected to grow at a Compound Annual Growth Rate (CAGR) of 1.9% through 2033. This moderate growth is influenced by consistent demand in cement and steel production, particularly in Germany and Poland. However, renewable energy adoption, environmental regulations, and carbon neutrality goals limit expansion. Anthracite and bituminous coal dominate due to high energy density for power generation. Lignite faces pressure from lower efficiency and higher emissions. Leading companies like Jastrzębska Spółka Węglowa SA and RWE are optimizing operations, exploring carbon capture, and diversifying. Key markets include Germany, Poland, and the UK, driven by existing mining infrastructure and energy needs.

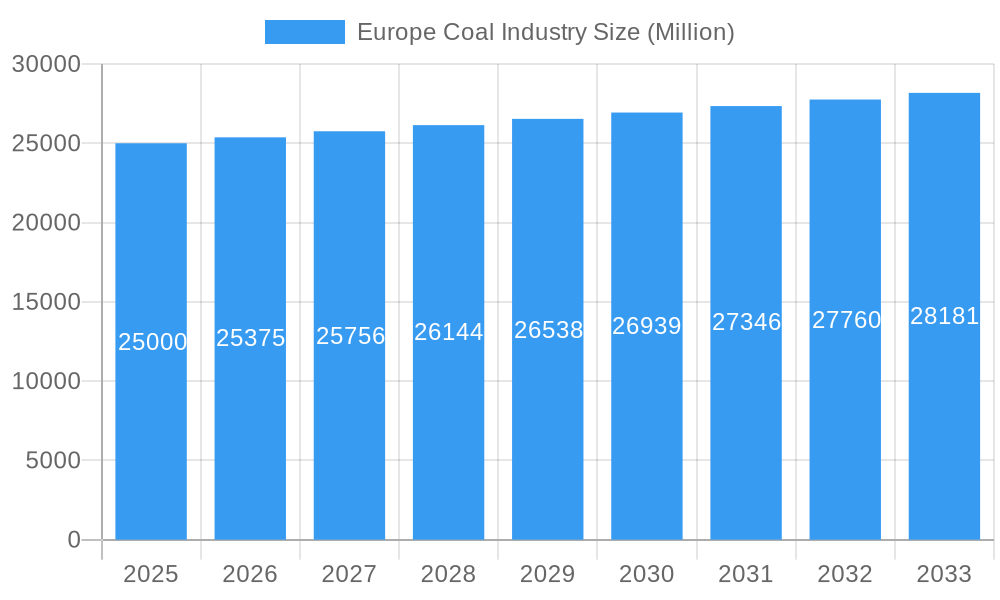

Europe Coal Industry Market Size (In Billion)

The future of the European coal market depends on policy, technology, and global energy prices. While a long-term phase-out is probable, near-term demand is tied to economic growth, energy security, and the pace of the renewable energy transition. Strategic focus on sustainability and diversification is crucial. The 'Other Applications' segment anticipates slow growth due to stricter regulations. The competitive landscape features established and smaller players with varied diversification and sustainability investments. Carbon Capture, Utilization, and Storage (CCUS) investment may address environmental concerns and impact growth.

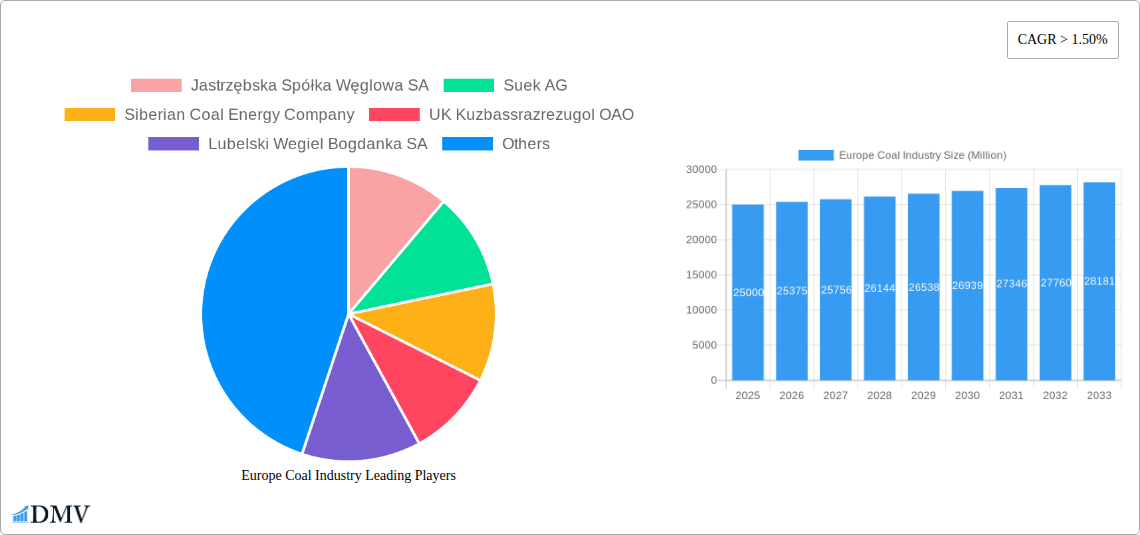

Europe Coal Industry Company Market Share

Europe Coal Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the European coal industry, encompassing market trends, leading players, technological advancements, and future growth projections from 2019 to 2033. With a focus on key segments (Anthracite, Bituminous, Sub-Bituminous, Lignite) and applications (Electricity, Steel, Cement, Other), this report is essential for stakeholders seeking to understand the evolving dynamics of this critical energy sector. The base year is 2025, with estimations for 2025 and forecasts extending to 2033.

Europe Coal Industry Market Composition & Trends

This section delves into the intricate composition of the European coal market, analyzing market concentration, innovation drivers, regulatory shifts, substitute product impacts, end-user behavior, and merger & acquisition (M&A) activities. The study period (2019-2024) provides historical context, while the forecast period (2025-2033) offers crucial future insights.

-

Market Concentration: The European coal market exhibits a moderately concentrated structure, with a few major players commanding significant market share. However, the distribution varies across coal types and regions. For example, approximately 65% of the Bituminous coal market is controlled by the top 5 companies in 2025.

-

Innovation Catalysts: Technological advancements in coal mining and utilization, such as enhanced extraction techniques leveraging automation and AI, and sophisticated carbon capture, utilization, and storage (CCUS) technologies, are driving innovation within the industry. Investment in research and development for cleaner coal combustion and gasification is also gaining traction.

-

Regulatory Landscape: Stringent environmental regulations, including the EU's Green Deal and ambitious carbon emission targets, are profoundly shaping the industry's trajectory. These regulations compel companies to invest in cleaner technologies, explore alternative energy sources, and align with phasedown plans. The evolving regulatory landscape presents both significant challenges and strategic opportunities for adaptation and survival.

-

Substitute Products: The rapid expansion of renewable energy sources like solar and wind power, coupled with advancements in energy storage and nuclear power's role in some national energy mixes, poses a significant challenge, acting as direct substitutes for coal-fired electricity generation. The market share of these substitutes is estimated to reach approximately 75% of the overall energy generation mix by 2033.

-

End-User Profiles: The primary end-users of coal in Europe remain power generation companies, steel manufacturers (for coking coal), and cement producers. However, shifts in energy policy and decarbonization efforts are leading to a gradual decline in demand from the power generation sector, while demand from steel and cement production is expected to be more resilient but influenced by technological advancements and global market dynamics.

-

M&A Activities: The European coal industry has witnessed several strategic M&A activities in recent years, driven by consolidation efforts, divestment of non-core assets, and strategic expansions into related or alternative energy sectors. The total value of M&A deals within the European coal sector reached an estimated €2.5 Billion in 2024. Examples include [specific examples of M&A deals and their values if available, otherwise state "Data unavailable"].

Europe Coal Industry Industry Evolution

This section provides a comprehensive overview of the European coal industry's evolution, encompassing market growth trajectories, technological advancements, and evolving consumer preferences. The analysis covers the period from 2019 to 2033, integrating historical data and future projections. The industry experienced a significant decline in production, approximately 18%, between 2019 and 2024 due to increased regulatory pressure, the growing competitiveness of renewable energy, and national phase-out policies. However, the forecast period shows a slight stabilization or marginal increase in specific segments, with an anticipated annual growth rate of around 0.5% from 2025 to 2033. This growth is driven primarily by increased demand from the steel and cement sectors, which continue to have a significant reliance on coal-based inputs, despite the increasing adoption of renewable energy sources for power generation. Furthermore, technological improvements in extraction efficiency and the development of advanced carbon capture technologies are expected to play a critical role in shaping the industry's future, enabling more environmentally conscious operations. The shift towards cleaner coal technologies, such as integrated gasification combined cycle (IGCC) power plants and improved emissions control systems, is becoming more pronounced, with investments in pilot projects and retrofitting of existing facilities.

Leading Regions, Countries, or Segments in Europe Coal Industry

This section identifies the dominant regions, countries, and segments within the European coal industry, focusing on the four main coal types (Anthracite, Bituminous, Sub-Bituminous, Lignite) and their respective applications.

-

Germany: Remains a significant player, particularly in lignite production and utilization, due to its substantial reserves and established lignite-fired power generation infrastructure. Despite a government push for phase-out, the pragmatic approach to energy security and the cost-effectiveness of lignite for baseload power continue to influence its role in the short to medium term. Key drivers include existing infrastructure, relatively low extraction costs, and energy security considerations.

-

Poland: A major producer and consumer of hard coal (Bituminous and Anthracite), primarily for power generation and industrial use in its steel sector. Strong domestic demand, significant coal reserves, and a commitment to a gradual transition away from coal ensure its continued prominence as a key player in the European market.

-

Lignite: Dominates in terms of production volume across Europe, largely driven by Germany's extensive reserves and its role in electricity generation. The continued operation of lignite power plants, albeit with increasingly stringent environmental controls, sustains demand, especially for baseload power provision.

-

Electricity Generation: Historically the most significant application of coal in Europe, accounting for approximately 55% of total consumption in 2025. This segment is expected to decline gradually over the forecast period as renewable energy sources and other cleaner alternatives gain market share, but it will remain a crucial component of the energy mix in certain regions for grid stability and energy security.

-

Steel Production: Remains a vital application of coal, with coking coal (a type of Bituminous coal) being an essential ingredient in the blast furnace steelmaking process. This segment is anticipated to maintain relatively stable demand, influenced by global steel demand and the pace of adoption of alternative steelmaking technologies like hydrogen-based direct reduction.

-

Cement Manufacturing: Coal contributes significantly to the high heat required in cement production. Demand in this segment is anticipated to remain relatively stable, though it will be subject to increased scrutiny regarding emissions and potential shifts towards alternative fuels or energy-efficient processes.

Key Drivers (for leading regions and segments):

- Significant domestic coal reserves and established industrial infrastructure

- Government policies aimed at ensuring energy security and supporting domestic industries during the transition

- Relatively lower production and operational costs compared to certain alternative fuels in specific contexts

- Well-established supply chains, skilled labor, and industrial clusters

- Continued demand from non-energy sectors like steel and cement manufacturing

Europe Coal Industry Product Innovations

Recent innovations focus on improving extraction efficiency, reducing environmental impact, and enhancing the overall value proposition of coal. This includes advancements in mining technology (like automated systems and improved safety measures), carbon capture and storage (CCS) techniques, and the development of cleaner coal combustion technologies. These innovations aim to increase competitiveness and address growing environmental concerns. Companies are also exploring new applications of coal-derived products, such as high-value chemicals and materials.

Propelling Factors for Europe Coal Industry Growth

Several factors are expected to propel the growth, or at least the continued relevance, of the European coal industry during the forecast period (2025-2033). Despite the accelerating transition to renewable energy, certain critical sectors will continue to rely on coal in the near to medium term, ensuring a stable level of demand. Moreover, significant investments in technological advancements are expected to optimize operational efficiency and minimize environmental impact, making coal a more sustainable option in specific applications. Additionally, potential energy security concerns arising from geopolitical instability and fluctuations in global energy prices could lead to an increased reliance on domestic coal resources in some European countries as a strategic energy reserve and a buffer against supply disruptions.

Obstacles in the Europe Coal Industry Market

The European coal industry faces significant obstacles, including increasingly stringent environmental regulations, which impose stricter emission limits and potentially lead to high compliance costs (estimated at xx Million annually for the industry). Supply chain disruptions, geopolitical instability, and competition from renewable energy sources also pose considerable challenges. Furthermore, public perception and social acceptance of coal mining projects continue to hinder growth in certain areas.

Future Opportunities in Europe Coal Industry

Opportunities lie in technological innovation, particularly in carbon capture utilization and storage (CCUS) technologies that reduce the environmental footprint of coal. Developing high-value byproducts from coal processing is another potential growth area. Furthermore, focusing on export markets where demand for coal remains high could offer growth potential.

Major Players in the Europe Coal Industry Ecosystem

- Jastrzębska Spółka Węglowa SA

- Suek AG

- Siberian Coal Energy Company

- UK Kuzbassrazrezugol OAO

- Lubelski Wegiel Bogdanka SA

- Mechel PAO

- Raspadskaya PAO

- Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG)

- Severstal PAO

Key Developments in Europe Coal Industry Industry

October 2022: The German government approved the expansion of the Garzweiler lignite mine, leading to the displacement of the village of Lutzerath and the planned extraction of 280 Million metric tons of lignite by 2030. This highlights the ongoing tension between energy needs and environmental concerns.

August 2022: Reactivation of the Heyden coal power plant in Germany (875 MW capacity) demonstrates a temporary shift back towards coal-fired power generation due to energy security concerns. This is a short-term response to the energy crisis.

Strategic Europe Coal Industry Market Forecast

The European coal industry is expected to undergo a significant transformation in the coming years. While overall demand is projected to decline gradually, certain segments, particularly in specific regions and applications (such as steel production), will maintain relative stability. Technological innovations and strategic adaptation by major players will play a crucial role in determining the long-term viability and growth potential of the industry. The successful implementation of CCUS technologies could significantly influence the future market dynamics.

Europe Coal Industry Segmentation

-

1. Type

- 1.1. Anthracite

- 1.2. Bituminous

- 1.3. Sub-Bituminous

- 1.4. Lignite

-

2. Application

- 2.1. Electricity

- 2.2. Steel

- 2.3. Cement

- 2.4. Other Applications

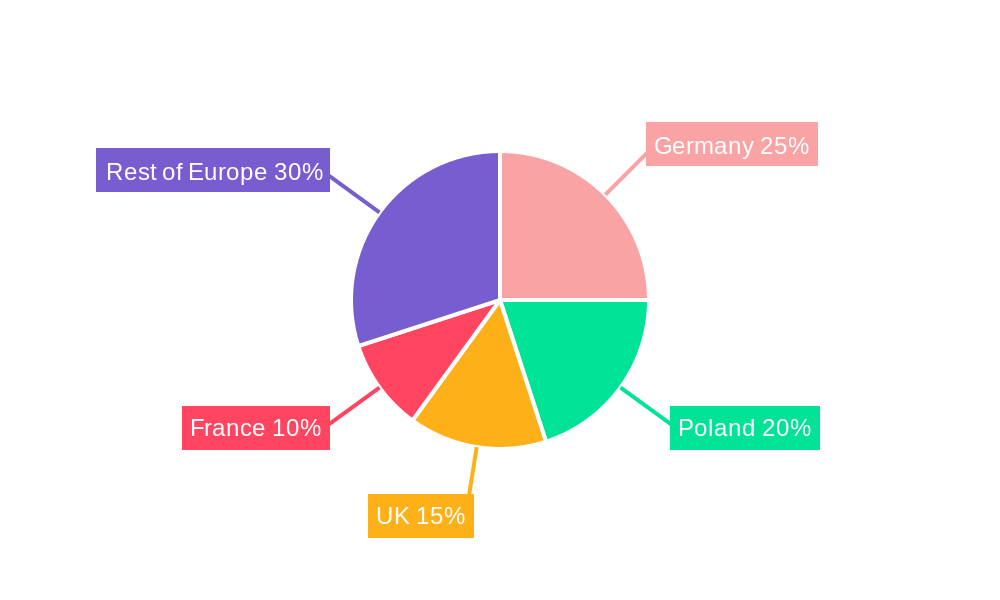

Europe Coal Industry Segmentation By Geography

- 1. Russia

- 2. Germany

- 3. Poland

- 4. Rest of Europe

Europe Coal Industry Regional Market Share

Geographic Coverage of Europe Coal Industry

Europe Coal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Anthracite

- 5.1.2. Bituminous

- 5.1.3. Sub-Bituminous

- 5.1.4. Lignite

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Electricity

- 5.2.2. Steel

- 5.2.3. Cement

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Russia

- 5.3.2. Germany

- 5.3.3. Poland

- 5.3.4. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Coal Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Anthracite

- 6.1.2. Bituminous

- 6.1.3. Sub-Bituminous

- 6.1.4. Lignite

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Electricity

- 6.2.2. Steel

- 6.2.3. Cement

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Russia Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Anthracite

- 7.1.2. Bituminous

- 7.1.3. Sub-Bituminous

- 7.1.4. Lignite

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Electricity

- 7.2.2. Steel

- 7.2.3. Cement

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Germany Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Anthracite

- 8.1.2. Bituminous

- 8.1.3. Sub-Bituminous

- 8.1.4. Lignite

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Electricity

- 8.2.2. Steel

- 8.2.3. Cement

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Poland Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Anthracite

- 9.1.2. Bituminous

- 9.1.3. Sub-Bituminous

- 9.1.4. Lignite

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Electricity

- 9.2.2. Steel

- 9.2.3. Cement

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of Europe Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Anthracite

- 10.1.2. Bituminous

- 10.1.3. Sub-Bituminous

- 10.1.4. Lignite

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Electricity

- 10.2.2. Steel

- 10.2.3. Cement

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Jastrzębska Spółka Węglowa SA

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Suek AG

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Siberian Coal Energy Company

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 UK Kuzbassrazrezugol OAO

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Lubelski Wegiel Bogdanka SA

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Mechel PAO

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Raspadskaya PAO*List Not Exhaustive

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG)

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Severstal PAO

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 Jastrzębska Spółka Węglowa SA

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Europe Coal Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Coal Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: Europe Coal Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Europe Coal Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 9: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 15: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 17: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 19: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 21: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 23: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 27: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 29: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Coal Industry?

The projected CAGR is approximately 1.9%.

2. Which companies are prominent players in the Europe Coal Industry?

Key companies in the market include Jastrzębska Spółka Węglowa SA, Suek AG, Siberian Coal Energy Company, UK Kuzbassrazrezugol OAO, Lubelski Wegiel Bogdanka SA, Mechel PAO, Raspadskaya PAO*List Not Exhaustive, Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG), Severstal PAO.

3. What are the main segments of the Europe Coal Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Renewable Energy Installations 4.; Energy Infrastructure Development.

6. What are the notable trends driving market growth?

Electricity Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Political and Economic Instability.

8. Can you provide examples of recent developments in the market?

October 2022: The German government has an agreement with a German multinational energy company that plans to expand the Garzweiler coal mine over Lutzerath village. The company plans to extract 280 million metric tons of lignite by 2030.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Coal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Coal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Coal Industry?

To stay informed about further developments, trends, and reports in the Europe Coal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence