Key Insights

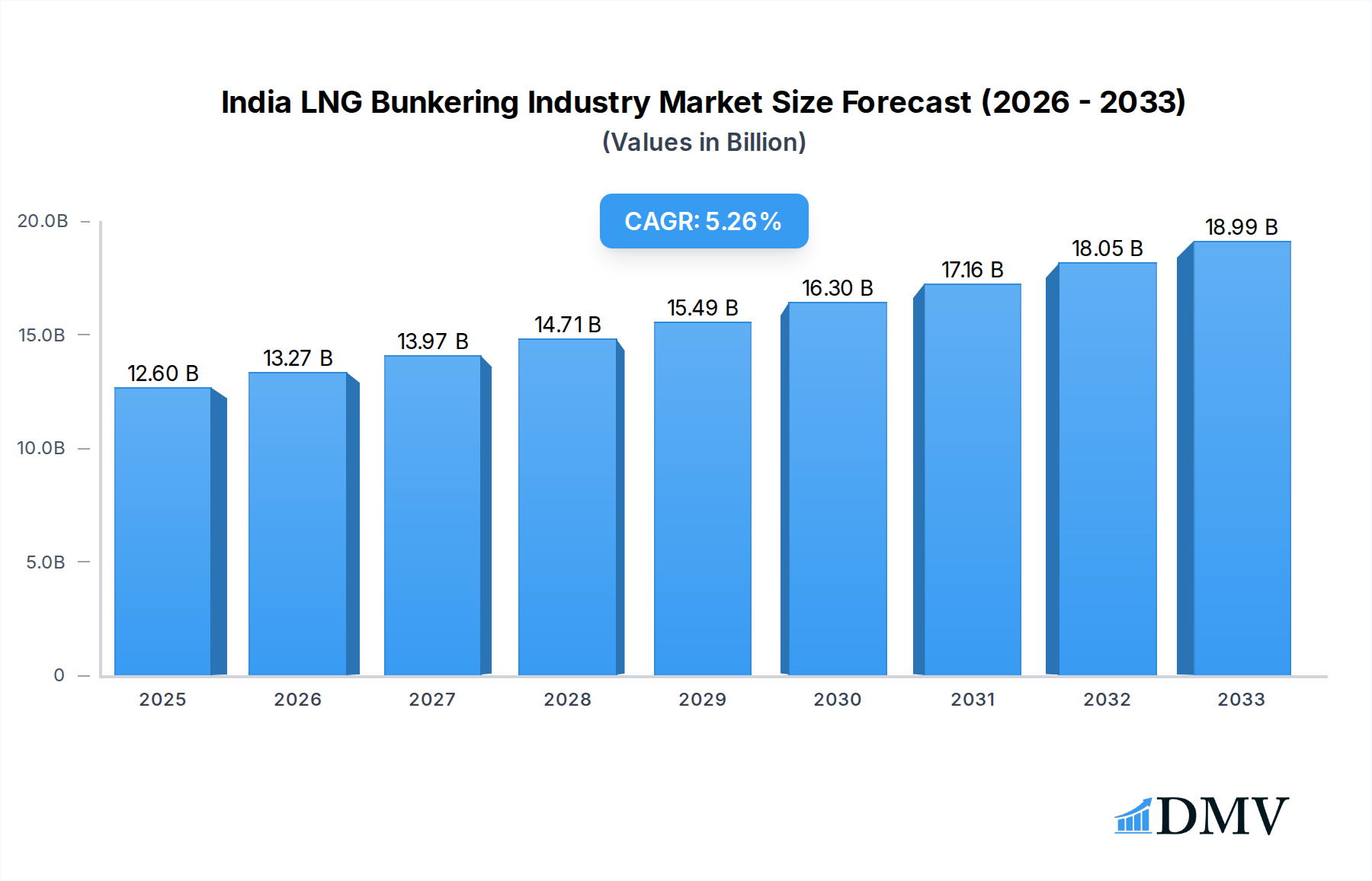

The India LNG Bunkering Industry is poised for substantial growth, projected to reach an estimated USD 12.6 billion by 2025. This expansion is driven by a strong Compound Annual Growth Rate (CAGR) of 5.3%, indicating a dynamic and expanding market. A primary driver for this surge is the increasing adoption of Liquefied Natural Gas (LNG) as a cleaner and more environmentally friendly fuel for maritime vessels, aligning with global decarbonization efforts and stricter emission regulations. The Indian government's proactive stance on promoting LNG infrastructure and encouraging the use of cleaner fuels in the shipping sector, coupled with the country's strategic location as a major global shipping route, further bolsters this growth trajectory. Investments in port infrastructure for LNG bunkering facilities and the development of LNG-powered vessel fleets are also key contributors, creating a robust ecosystem for the industry's advancement.

India LNG Bunkering Industry Market Size (In Billion)

The market is segmented across various end-user fleets, with the Tanker Fleet and Container Fleet expected to be major consumers of LNG bunkering services due to their high operational demands and increasing pressure to comply with environmental standards. The Bulk and General Cargo Fleet, along with Ferries and OSVs (Offshore Support Vessels), also present significant opportunities for growth. Key players like Indian Oil Corporation Ltd., Bharat Petroleum Corp Ltd., Adani Enterprises Ltd., Petronet LNG Ltd., and H-Energy Private Limited are actively investing in expanding their LNG bunkering capabilities and infrastructure across India. The focus on developing comprehensive LNG bunkering networks in major Indian ports will be crucial in overcoming logistical challenges and ensuring a seamless supply chain for ship operators. While the industry benefits from strong drivers, potential challenges related to the initial cost of LNG-powered vessels and the development of a widespread refueling infrastructure need to be strategically addressed to sustain this impressive growth momentum.

India LNG Bunkering Industry Company Market Share

India LNG Bunkering Industry Report: Unlocking Growth and Navigating Future Opportunities (2019–2033)

This comprehensive report delves into the dynamic India LNG bunkering industry, a critical sector poised for significant expansion driven by stringent environmental regulations and the global push towards cleaner shipping fuels. Our analysis, spanning the historical period of 2019–2024, with a base and estimated year of 2025, and extending through a robust forecast period of 2025–2033, provides deep insights into market composition, industry evolution, leading segments, product innovations, growth drivers, prevailing obstacles, and future opportunities. This report is an indispensable resource for stakeholders seeking to understand the Indian marine fuel market, LNG as a marine fuel, LNG bunkering infrastructure in India, and the competitive landscape shaped by key players like Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Adani Enterprises Ltd, Petronet LNG Ltd, and H-Energy Private Limited.

India LNG Bunkering Industry Market Composition & Trends

The India LNG bunkering market exhibits a moderate concentration, with a few prominent players like Petronet LNG Ltd and state-owned oil giants dominating infrastructure development and supply. Innovation is being catalyzed by the growing demand for environmentally compliant fuels and government initiatives promoting LNG adoption in shipping. The regulatory landscape is steadily evolving, with supportive policies aimed at establishing dedicated LNG bunkering facilities and encouraging vessel conversions. Substitute products, primarily traditional marine fuels like High Sulfur Fuel Oil (HSFO) and Low Sulfur Fuel Oil (LSFO), continue to hold market share, but their dominance is waning due to increasing environmental scrutiny. End-users encompass a diverse tanker fleet, container fleet, bulk and general cargo fleet, and specialized vessels like ferries and OSVs. M&A activities are anticipated to increase as companies seek to secure market share and expand their LNG bunkering network in India, with estimated deal values in the hundreds of billions as the market matures. The market share distribution is evolving, with a gradual shift towards LNG as demand for sustainable solutions grows.

- Market Concentration: Moderate, with key players like Petronet LNG Ltd and IOCL leading.

- Innovation Catalysts: Stringent emission norms, government support for cleaner fuels.

- Regulatory Landscape: Evolving with supportive policies for LNG bunkering infrastructure.

- Substitute Products: HSFO, LSFO, facing increasing environmental pressure.

- End-User Profiles: Tanker, Container, Bulk/General Cargo fleets, Ferries, OSVs.

- M&A Activities: Expected to rise, with estimated deal values in the hundreds of billions.

India LNG Bunkering Industry Industry Evolution

The India LNG bunkering industry has witnessed a transformative evolution, driven by a confluence of global environmental mandates and India's commitment to sustainable energy solutions. Over the historical period of 2019–2024, the market has moved from nascent stages to active development, spurred by the International Maritime Organization's (IMO) stringent emission regulations, particularly IMO 2020, which significantly impacted the demand for cleaner marine fuels. The study period of 2019–2033 encapsulates this dynamic growth. In the base year of 2025, the industry is projected to solidify its foundational infrastructure, with significant investments in LNG bunkering terminals and supply chains across major Indian ports. The estimated year of 2025 signifies a crucial point where early adoption trends become more pronounced.

Technological advancements have been pivotal, with the introduction of more efficient LNG-powered vessels and improved LNG bunkering technologies, including truck-to-ship and ship-to-ship transfer methods. These advancements are not only enhancing operational efficiency but also improving safety standards within the Indian shipping industry. Consumer demand has shifted dramatically, with shipowners increasingly prioritizing environmental, social, and governance (ESG) factors, making LNG a more attractive alternative to traditional fossil fuels. This shift is evidenced by an increasing number of vessel conversion projects and new builds designed to operate on LNG. The market growth trajectory is set to accelerate significantly during the forecast period of 2025–2033, projecting a compound annual growth rate (CAGR) of approximately 15-20%. Adoption metrics for LNG-powered vessels are expected to rise from a modest 5% in 2025 to over 25% by 2033. The development of robust LNG supply chains and the establishment of a widespread LNG bunkering network are key to sustaining this growth. Furthermore, government policy support, including incentives for LNG-fueled shipping and the development of LNG regasification terminals, plays a crucial role in shaping the market's future. The industry's evolution is also marked by strategic partnerships between LNG suppliers, port authorities, and shipping companies, fostering a collaborative ecosystem essential for scaling up operations. The increasing focus on decarbonization in shipping further solidifies LNG's role as a transitional fuel, paving the way for its broader acceptance and market expansion in India. The estimated market size in 2025 is projected to be around 2.5 billion USD, with significant expansion expected throughout the forecast period.

Leading Regions, Countries, or Segments in India LNG Bunkering Industry

The India LNG bunkering industry is experiencing rapid growth, with several key regions and end-user segments emerging as dominant forces. The Tanker Fleet segment is a primary driver of this expansion, owing to the sheer volume of liquid cargo transported and the increasing pressure on tanker operators to adopt cleaner fuels to comply with global emissions standards and enhance their corporate sustainability profiles. India's extensive coastline and its position as a major trading hub necessitate a robust and reliable LNG bunkering infrastructure to support these large vessels.

Key drivers for the dominance of the Tanker Fleet segment include:

- Regulatory Compliance: The need to meet stringent international emission regulations (e.g., IMO 2020) directly influences tanker operators' fuel choices.

- Economic Incentives: While initial conversion costs can be high, the long-term operational savings from LNG, coupled with potential lower carbon taxes, make it an attractive option.

- Infrastructure Development: Major ports like Mundra, Hazira, Dahej, and Pipavav are rapidly developing LNG bunkering facilities, creating a conducive environment for tanker bunkering operations.

- Fleet Modernization: Shipping companies are increasingly investing in dual-fuel vessels capable of running on LNG, signaling a long-term commitment to this fuel.

The Container Fleet is another significant segment showing robust growth potential. As global trade continues to expand, the demand for efficient and environmentally responsible container shipping services is rising. Container lines are under immense pressure from cargo owners and consumers to reduce their carbon footprint, making LNG an increasingly viable option. The development of large-scale LNG-powered container ships further bolsters this trend.

The Bulk and General Cargo Fleet also contributes to the growing LNG bunkering market, albeit at a slightly slower pace than tankers and container ships. However, as LNG becomes more accessible and affordable, and as more specialized bunkering solutions are developed, this segment is expected to see a substantial increase in LNG adoption.

The Ferries and OSV (Offshore Support Vessels) segment, while smaller in terms of overall volume, presents unique opportunities. These vessels often operate in specific, well-defined routes or regions, making the planning and execution of LNG bunkering more straightforward. The deployment of LNG-powered ferries for coastal and inter-island transport is a promising area, driven by local environmental concerns and the potential for government support.

The dominance of these segments is further amplified by strategic investments and government policies aimed at establishing India as a leading LNG bunkering hub. The presence of major players like Adani Enterprises Ltd and Petronet LNG Ltd, with their significant investments in port infrastructure and LNG handling capabilities, is critical in supporting this growth. The anticipated market value for these segments collectively is estimated to reach several billions of US dollars by 2033.

India LNG Bunkering Industry Product Innovations

The India LNG bunkering industry is witnessing a wave of innovation focused on enhancing the efficiency, safety, and accessibility of LNG as a marine fuel. Key product innovations include the development of smaller-scale, modular LNG bunkering terminals that can be deployed more rapidly and cost-effectively at various port locations, expanding the LNG bunkering network beyond major hubs. Furthermore, advancements in cryogenic technology are leading to lighter and more efficient LNG storage tanks for both bunkering vessels and ships, improving cargo capacity and operational flexibility. Innovations in LNG fuel supply systems are also enhancing safety protocols, with automated and remote-monitoring systems reducing the risk of human error during bunkering operations. The development of dual-fuel engines that can seamlessly switch between LNG and other fuels is also a significant product innovation, offering shipowners greater operational flexibility and risk mitigation. These advancements are crucial for meeting the evolving demands of the Indian shipping industry and solidifying LNG as a marine fuel.

Propelling Factors for India LNG Bunkering Industry Growth

The India LNG bunkering industry is propelled by a potent combination of factors.

- Environmental Regulations: Stringent global emissions standards, particularly from the IMO, are forcing the shipping industry to adopt cleaner fuels, with LNG being a primary solution.

- Government Support & Initiatives: The Indian government's focus on developing a robust LNG bunkering infrastructure and promoting cleaner energy sources through policies and incentives is a significant growth catalyst.

- Economic Viability: While initial investment is substantial, the long-term cost savings from LNG fuel, coupled with potential carbon pricing mechanisms, are making it economically attractive.

- Technological Advancements: Improvements in LNG-powered engines, bunkering technologies, and supply chain logistics are enhancing the feasibility and safety of using LNG.

- Growing LNG Supply: Increased LNG import capacity and the development of domestic supply chains are ensuring greater availability of the fuel.

Obstacles in the India LNG Bunkering Industry Market

Despite its promising growth, the India LNG bunkering industry faces several significant obstacles.

- High Upfront Investment: Establishing LNG bunkering infrastructure requires substantial capital expenditure, which can be a barrier for smaller players.

- Lack of Widespread Infrastructure: While developing, the current LNG bunkering network is not yet comprehensive across all Indian ports, limiting operational flexibility for vessels.

- Regulatory Uncertainties: Evolving regulations and varying interpretations across different states can create ambiguity and delay investment.

- Safety Concerns & Public Perception: Perceptions around the safe handling and storage of LNG need to be addressed through continuous training and public awareness campaigns.

- Competition from Alternative Fuels: Emerging cleaner fuels and advancements in existing fuel technologies present ongoing competition.

Future Opportunities in India LNG Bunkering Industry

The India LNG bunkering industry is ripe with future opportunities.

- Expansion of Bunkering Infrastructure: Significant potential exists for developing new LNG bunkering terminals and supply points in emerging port clusters.

- Growth in LNG-Powered Vessel Fleets: Increased adoption of LNG-powered ships across various segments will drive demand for bunkering services.

- Development of Coastal Shipping: LNG offers a cleaner alternative for the burgeoning Indian coastal shipping sector, presenting a new market.

- Integration with the Natural Gas Grid: Synergies with India's expanding natural gas pipeline network can optimize LNG supply chains.

- Technological Advancements in Small-Scale LNG: Innovations in smaller, more agile bunkering solutions can unlock opportunities in less developed regions.

Major Players in the India LNG Bunkering Industry Ecosystem

- Indian Oil Corporation Ltd

- Bharat Petroleum Corp Ltd

- Adani Enterprises Ltd

- Petronet LNG Ltd

- H-Energy Private Limited

Key Developments in India LNG Bunkering Industry Industry

- 2019-2020: Initial feasibility studies and pilot projects for LNG bunkering at major Indian ports.

- 2021: Government announces policies to promote LNG as a marine fuel, including infrastructure development incentives.

- 2022: Petronet LNG Ltd and Indian Oil Corporation Ltd announce plans for dedicated LNG bunkering facilities at key ports.

- 2023: Adani Enterprises Ltd enters the fray with significant investments in LNG infrastructure, including bunkering capabilities.

- 2024: H-Energy Private Limited announces expansion plans for its LNG infrastructure, potentially including bunkering services. First commercial LNG bunkering operations commence at select ports.

Strategic India LNG Bunkering Industry Market Forecast

The India LNG bunkering industry is projected for substantial growth, driven by an imperative shift towards decarbonization in the maritime sector. The forecast period (2025–2033) anticipates a robust expansion fueled by increasingly stringent environmental regulations and proactive government policies supporting the development of LNG bunkering infrastructure and the adoption of LNG as a marine fuel. The increasing fleet of LNG-powered vessels, coupled with strategic investments by major players like Petronet LNG Ltd and Adani Enterprises Ltd, will further solidify India's position as a key LNG bunkering hub. While challenges related to infrastructure development and upfront costs persist, the long-term economic and environmental benefits of LNG present compelling opportunities, ensuring a bright future for this critical sector within the Indian shipping industry.

India LNG Bunkering Industry Segmentation

-

1. End-User

- 1.1. Tanker Fleet

- 1.2. Container Fleet

- 1.3. Bulk and General Cargo Fleet

- 1.4. Ferries and OSV

- 1.5. Others

India LNG Bunkering Industry Segmentation By Geography

- 1. India

India LNG Bunkering Industry Regional Market Share

Geographic Coverage of India LNG Bunkering Industry

India LNG Bunkering Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 5.1.1. Tanker Fleet

- 5.1.2. Container Fleet

- 5.1.3. Bulk and General Cargo Fleet

- 5.1.4. Ferries and OSV

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 6. India LNG Bunkering Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 6.1.1. Tanker Fleet

- 6.1.2. Container Fleet

- 6.1.3. Bulk and General Cargo Fleet

- 6.1.4. Ferries and OSV

- 6.1.5. Others

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Indian Oil Corporation Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corp Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Adani Enterprises Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Petronet LNG Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 H-Energy Private Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Indian Oil Corporation Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India LNG Bunkering Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India LNG Bunkering Industry Share (%) by Company 2025

List of Tables

- Table 1: India LNG Bunkering Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 2: India LNG Bunkering Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: India LNG Bunkering Industry Revenue billion Forecast, by End-User 2020 & 2033

- Table 4: India LNG Bunkering Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India LNG Bunkering Industry?

The projected CAGR is approximately 5.3%.

2. Which companies are prominent players in the India LNG Bunkering Industry?

Key companies in the market include Indian Oil Corporation Ltd, Bharat Petroleum Corp Ltd, Adani Enterprises Ltd, Petronet LNG Ltd, H-Energy Private Limited.

3. What are the main segments of the India LNG Bunkering Industry?

The market segments include End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

Ferries and OSV Segment is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India LNG Bunkering Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India LNG Bunkering Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India LNG Bunkering Industry?

To stay informed about further developments, trends, and reports in the India LNG Bunkering Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence