Key Insights

The North America Industrial Centrifuge Market is projected to reach $10.22 billion by 2025, demonstrating a Compound Annual Growth Rate (CAGR) of 6.7%. This growth is propelled by the escalating demand for advanced separation solutions across numerous industrial verticals. Key growth catalysts include stringent environmental mandates, particularly in water and wastewater treatment, driving the need for sophisticated filtration and purification technologies. The pharmaceutical industry's pursuit of enhanced product purity and the food and beverage sector's focus on superior quality and yield further bolster market expansion. Innovations in centrifuge design, emphasizing energy efficiency and automation, are accelerating adoption. A notable trend is the increasing preference for continuous operation centrifuges in high-volume manufacturing, such as chemical production, due to their superior throughput and cost-effectiveness over batch processing.

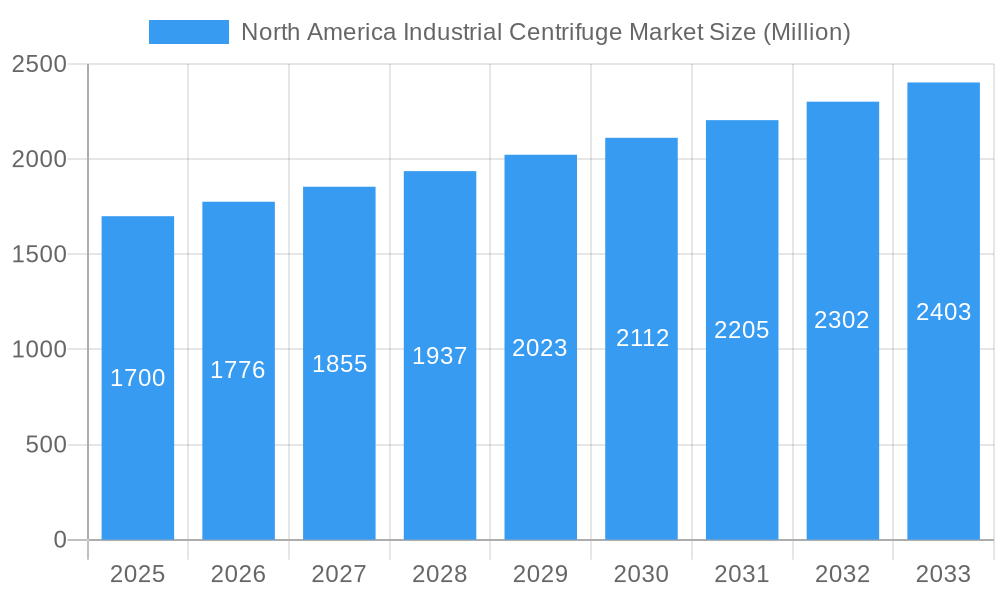

North America Industrial Centrifuge Market Market Size (In Billion)

The North America Industrial Centrifuge Market is segmented primarily by type, with sedimentation and filtering centrifuges holding significant market share. Horizontal centrifuges are prevalent due to their adaptability and capacity for high-volume processing, while vertical centrifuges are utilized in space-constrained environments or for specific separation needs. Technological advancements are leading to the development of specialized centrifuges for niche applications in sectors like mining and power generation. Despite considerable growth potential, high initial capital expenditure and the availability of alternative separation methods may present market challenges. However, the pervasive drive for process optimization, resource recovery, and stringent quality control across North American industries forecasts a dynamic and prosperous outlook for the industrial centrifuge market.

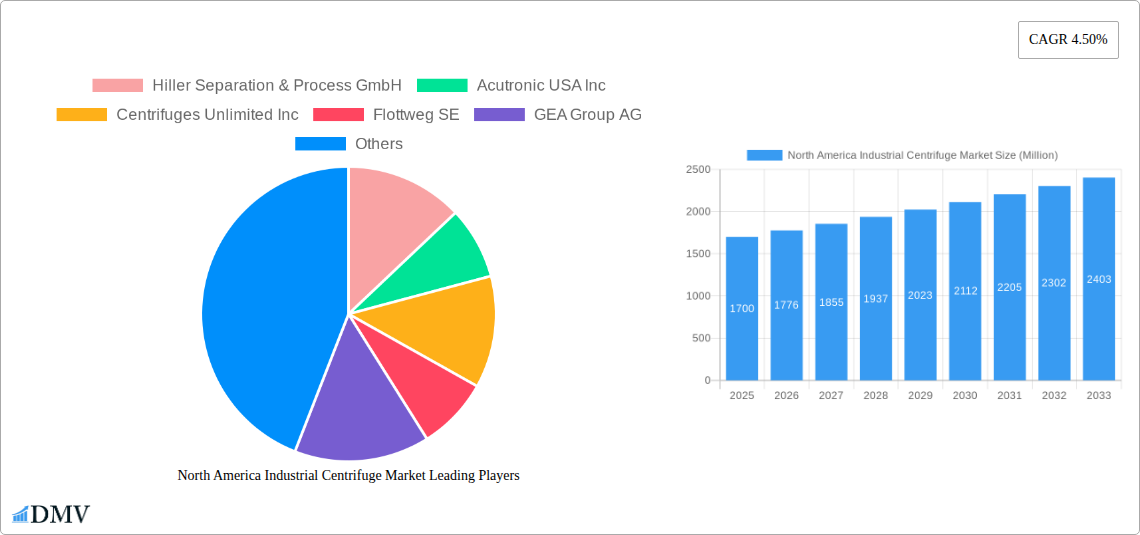

North America Industrial Centrifuge Market Company Market Share

North America Industrial Centrifuge Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides an exhaustive analysis of the North America Industrial Centrifuge Market, delving into its composition, trends, industry evolution, key segments, product innovations, growth drivers, obstacles, future opportunities, major players, and strategic forecasts. With a study period spanning from 2019 to 2033, and a base year of 2025, this report offers critical insights for stakeholders seeking to understand and capitalize on the dynamic industrial centrifuge market in the United States, Canada, and the rest of North America.

North America Industrial Centrifuge Market Market Composition & Trends

The North America Industrial Centrifuge Market is characterized by a moderate to high concentration, driven by innovation and stringent quality standards across various industries. Key catalysts for growth include the increasing demand for efficient solid-liquid separation technologies and the continuous development of advanced centrifuge designs. The regulatory landscape, particularly concerning environmental protection and product purity in sectors like pharmaceuticals and food and beverage, significantly influences market dynamics. Substitute products, such as filtration membranes and decanters, offer alternative separation methods, yet industrial centrifuges maintain a strong competitive edge due to their superior performance and versatility. End-user profiles span a diverse range of industries, each with specific requirements for separation efficiency, capacity, and process integration. Mergers and acquisitions (M&A) play a crucial role in market consolidation and the expansion of product portfolios. Notable M&A activities in the historical period have seen significant deal values, reflecting strategic moves to enhance market presence and technological capabilities. The market share distribution is influenced by leading players' product offerings and geographical reach, with a projected market size of $XXX Million by 2025.

- Market Concentration: Moderate to High, driven by key global and regional manufacturers.

- Innovation Catalysts: Growing demand for efficient separation, advancements in automation and control systems, and stricter regulatory compliance.

- Regulatory Landscapes: Environmental regulations (e.g., wastewater treatment standards) and industry-specific quality control mandates (e.g., FDA, GMP) are pivotal.

- Substitute Products: Filtration membranes, decanters, and other separation technologies, though industrial centrifuges offer distinct advantages.

- End-User Profiles: Diverse, with specific needs from Food and Beverage, Pharmaceutical, Water and Wastewater Treatment, Chemical, Metal and Mining, Power, and Pulp and Paper industries.

- M&A Activities: Significant deal values observed, focusing on market expansion, technology acquisition, and portfolio diversification.

North America Industrial Centrifuge Market Industry Evolution

The North America Industrial Centrifuge Market has witnessed remarkable evolution driven by technological advancements and an ever-increasing demand for efficient separation solutions. From its inception, the industry has been shaped by the pursuit of higher throughput, improved separation precision, and greater energy efficiency. The historical period (2019-2024) showcased a steady upward trajectory, fueled by escalating industrial activity and a growing awareness of the environmental and economic benefits offered by advanced centrifuges. The base year of 2025 positions the market at a significant juncture, with established players and emerging innovators vying for market dominance. Looking ahead into the forecast period (2025-2033), the market is poised for accelerated growth. Key technological advancements have focused on enhancing automation, developing smart centrifuges with integrated diagnostics and predictive maintenance capabilities, and creating more specialized designs tailored to niche applications. The adoption of continuous operation modes has become increasingly prevalent, offering significant advantages in terms of efficiency and cost-effectiveness for high-volume industrial processes. Furthermore, the development of novel materials and enhanced sealing technologies has improved the durability and performance of centrifuges, allowing them to handle increasingly challenging separation tasks. Shifting consumer demands, particularly in the food and beverage and pharmaceutical sectors, for higher purity products and reduced waste have also been instrumental in driving innovation and market expansion. The increasing emphasis on sustainability and resource recovery has further propelled the adoption of centrifuges for applications such as dewatering sludge, recovering valuable materials, and minimizing effluent discharge. The total addressable market is projected to reach $XXX Million by 2033, with a compound annual growth rate (CAGR) of XX.X% during the forecast period.

Leading Regions, Countries, or Segments in North America Industrial Centrifuge Market

The United States stands as the undisputed leader in the North America Industrial Centrifuge Market, driven by its robust industrial base, extensive research and development capabilities, and stringent regulatory frameworks that necessitate advanced separation technologies. The country's diverse economic landscape, encompassing major sectors like pharmaceuticals, chemicals, food and beverage, and water treatment, creates a consistently high demand for various types of industrial centrifuges. The Chemical industry, with its vast array of processes requiring precise separation of solids from liquids or gases, represents a significant segment, closely followed by the Pharmaceutical sector, where product purity and sterile processing are paramount. Within the Type segment, Sedimentation centrifuges continue to dominate due to their versatility and widespread application in bulk material processing, while Filtering centrifuges are gaining traction in applications demanding higher purity and drier solids. The Design segment sees a strong preference for Horizontal Centrifuges for large-scale continuous operations, whereas Vertical Centrifuges find their niche in specialized applications and laboratory settings. The Operation Mode is increasingly leaning towards Continuous centrifuges, offering substantial benefits in terms of throughput and efficiency for industrial-scale production, although Batch centrifuges remain crucial for smaller-scale or specialized processes. The Water and Wastewater Treatment industry is another pivotal growth area, driven by increasing urbanization, stringent environmental regulations, and the need for efficient sludge dewatering and water purification. Government investments in infrastructure and environmental protection further bolster the demand for centrifuges in this segment.

- Dominant Region: United States, accounting for approximately XX% of the North American market share.

- Key Drivers: Extensive industrial base, strong R&D, stringent regulatory environment, significant investment in infrastructure.

- Dominance Factors: Presence of major end-user industries, technological adoption rate, and manufacturing prowess.

- Dominant Industry Segment:

- Chemical Industry: High demand due to diverse separation needs in chemical synthesis, processing, and refining.

- Pharmaceutical Industry: Critical for API purification, sterile processing, and quality control, driving demand for high-precision centrifuges.

- Water and Wastewater Treatment: Growing segment fueled by environmental regulations and infrastructure upgrades, requiring efficient sludge dewatering.

- Dominant Type: Sedimentation Centrifuges, offering broad applicability across various industrial processes.

- Dominant Design: Horizontal Centrifuges, favored for high-capacity continuous operations.

- Dominant Operation Mode: Continuous Operation Mode, offering superior efficiency and throughput for large-scale industrial applications.

North America Industrial Centrifuge Market Product Innovations

Product innovation in the North America Industrial Centrifuge Market is a continuous endeavor, focused on enhancing efficiency, automation, and specialized capabilities. Recent advancements include the development of highly automated and intelligent centrifuges equipped with advanced process control systems for optimized performance and reduced operator intervention. Innovations in materials science have led to the creation of more robust and corrosion-resistant centrifuge components, extending their lifespan and enabling operation in aggressive chemical environments. Furthermore, the integration of sophisticated filtration and separation membranes within centrifuge designs is opening new avenues for achieving higher purity levels in pharmaceutical and fine chemical applications. The introduction of compact, energy-efficient models is also a significant trend, catering to industries with space constraints or those prioritizing sustainability. These innovations translate into superior performance metrics such as increased throughput, reduced energy consumption, and enhanced product yield, making industrial centrifuges indispensable across a spectrum of demanding applications.

Propelling Factors for North America Industrial Centrifuge Market Growth

Several compelling factors are propelling the growth of the North America Industrial Centrifuge Market. The increasing stringency of environmental regulations globally, particularly concerning wastewater treatment and waste minimization, is a significant driver, demanding more efficient separation technologies. Technological advancements in centrifuge design, including automation, improved control systems, and specialized configurations for niche applications, are enhancing their appeal and performance. The robust growth of key end-user industries such as pharmaceuticals, food and beverage, and chemicals, all of which rely heavily on effective solid-liquid separation, further fuels market expansion. Furthermore, the rising emphasis on operational efficiency and cost reduction across industries encourages the adoption of advanced centrifuges that offer higher throughput and lower energy consumption. The increasing focus on resource recovery and circular economy initiatives also presents a growing opportunity for centrifuge manufacturers.

- Environmental Regulations: Stricter compliance demands for wastewater treatment and solid waste management.

- Technological Advancements: Automation, smart controls, and specialized designs for improved efficiency and performance.

- End-User Industry Growth: Expansion in pharmaceutical, food and beverage, chemical, and mining sectors.

- Operational Efficiency: Drive for cost reduction and higher throughput in industrial processes.

- Resource Recovery: Growing focus on circular economy principles and valuable material extraction.

Obstacles in the North America Industrial Centrifuge Market Market

Despite its strong growth trajectory, the North America Industrial Centrifuge Market faces certain obstacles. High initial capital investment for advanced centrifuge systems can be a deterrent for smaller enterprises or those with limited budgets. The complexity of operation and maintenance for some sophisticated models requires specialized training, potentially leading to higher operational costs. Stringent and evolving regulatory compliance requirements across different sectors can necessitate costly upgrades and reconfigurations of existing equipment. Furthermore, supply chain disruptions, as witnessed in recent years, can impact the availability of critical components and lead to production delays, affecting delivery timelines and overall market stability. Intense competition from alternative separation technologies and the presence of established players with significant market share can also pose challenges for new entrants and smaller manufacturers.

- High Initial Capital Investment: Significant upfront costs for advanced centrifuge systems.

- Operational Complexity and Training: Requirement for specialized skills and training for advanced models.

- Evolving Regulatory Landscape: Continuous need for equipment upgrades to meet changing compliance standards.

- Supply Chain Disruptions: Potential for delays in component availability and production schedules.

- Competition from Alternatives: Presence of established substitute separation technologies.

Future Opportunities in North America Industrial Centrifuge Market

The North America Industrial Centrifuge Market is ripe with future opportunities, driven by emerging trends and unmet needs. The increasing demand for sustainable and energy-efficient separation solutions presents a significant avenue for innovation and market penetration. The growing focus on the circular economy is creating opportunities for centrifuges in resource recovery applications, such as extracting valuable materials from industrial waste streams. Advancements in artificial intelligence and machine learning are enabling the development of "smart" centrifuges with predictive maintenance capabilities and enhanced process optimization, offering significant value to end-users. The expansion of specialized industries, such as biotechnology and advanced materials manufacturing, will create demand for highly customized and precise separation technologies. Furthermore, developing countries and regions with developing industrial bases represent untapped markets for industrial centrifuges, offering substantial growth potential.

- Sustainable and Energy-Efficient Solutions: Growing demand for eco-friendly and power-saving technologies.

- Circular Economy Initiatives: Opportunities in resource recovery and waste valorization.

- Smart and Predictive Maintenance: Integration of AI and ML for enhanced operational intelligence.

- Specialized Industry Growth: Demand from biotechnology, advanced materials, and niche manufacturing sectors.

- Emerging Markets: Untapped potential in developing industrial regions.

Major Players in the North America Industrial Centrifuge Market Ecosystem

- Hiller Separation & Process GmbH

- Acutronic USA Inc

- Centrifuges Unlimited Inc

- Flottweg SE

- GEA Group AG

- CentraSep Technologies Inc

- Andritz AG

- Centrisys Corporation

- Alfa Laval AB

Key Developments in North America Industrial Centrifuge Market Industry

- August 2022: GEA launched a new range of pharmaceutical industrial centrifuge systems for North America called Kytero. Kytero is ready for manufacturing. Filter regions can be reduced by 75%. The system requires a standard power connection; intermediate tanks are obsolete. The simple exchange eliminates CIP (clean-in-place) and SIP (sterilize-in-place). This development signifies a significant step towards more integrated and efficient pharmaceutical processing.

- February 2022: Beckman Coulter introduced the Allegra V-15R refrigerated centrifuge. With ten rotor configurations, 50 programmed runs, and a large assortment of adapters, a wide range of workflows and applications may be carried out. This launch broadens the scope of applications for refrigerated centrifuges, catering to diverse laboratory needs.

Strategic North America Industrial Centrifuge Market Market Forecast

The strategic forecast for the North America Industrial Centrifuge Market indicates a robust and sustained growth trajectory driven by technological advancements and increasing industrial demands. The ongoing emphasis on process optimization, waste reduction, and environmental sustainability will continue to fuel the adoption of advanced centrifuge solutions. Innovations in automation and smart technologies will further enhance operational efficiency and reduce lifecycle costs, making centrifuges an even more attractive investment for industries. The expansion of key end-user sectors, coupled with a growing awareness of the benefits of efficient solid-liquid separation, will solidify the market's upward momentum. Opportunities in specialized applications and the potential for new market entries, particularly in areas focused on resource recovery and sustainable processing, will contribute to a dynamic and evolving market landscape. The market is projected to witness consistent expansion, driven by both established players and innovative newcomers addressing specific industrial challenges.

North America Industrial Centrifuge Market Segmentation

-

1. Type

- 1.1. Sedimentaion

- 1.2. Filtering

-

2. Design

- 2.1. Horizontal Centrifuge

- 2.2. Vertical Centrifuge

-

3. Operation Mode

- 3.1. Batch

- 3.2. Continuous

-

4. Industry

- 4.1. Food and Beverage

- 4.2. Pharmaceutical

- 4.3. Water and Wastewater Treatment

- 4.4. Chemical

- 4.5. Metal and Mining

- 4.6. Power

- 4.7. Pulp and Paper

- 4.8. Other Industries

-

5. Geography

- 5.1. United States

- 5.2. Canada

- 5.3. Rest of North America

North America Industrial Centrifuge Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

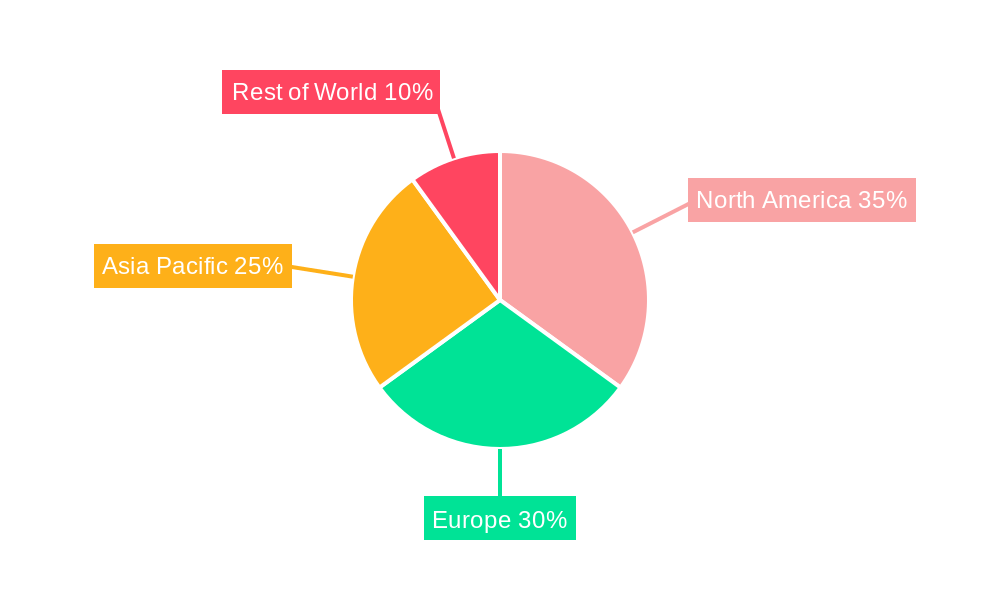

North America Industrial Centrifuge Market Regional Market Share

Geographic Coverage of North America Industrial Centrifuge Market

North America Industrial Centrifuge Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Sedimentaion

- 5.1.2. Filtering

- 5.2. Market Analysis, Insights and Forecast - by Design

- 5.2.1. Horizontal Centrifuge

- 5.2.2. Vertical Centrifuge

- 5.3. Market Analysis, Insights and Forecast - by Operation Mode

- 5.3.1. Batch

- 5.3.2. Continuous

- 5.4. Market Analysis, Insights and Forecast - by Industry

- 5.4.1. Food and Beverage

- 5.4.2. Pharmaceutical

- 5.4.3. Water and Wastewater Treatment

- 5.4.4. Chemical

- 5.4.5. Metal and Mining

- 5.4.6. Power

- 5.4.7. Pulp and Paper

- 5.4.8. Other Industries

- 5.5. Market Analysis, Insights and Forecast - by Geography

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Rest of North America

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. United States

- 5.6.2. Canada

- 5.6.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Industrial Centrifuge Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Sedimentaion

- 6.1.2. Filtering

- 6.2. Market Analysis, Insights and Forecast - by Design

- 6.2.1. Horizontal Centrifuge

- 6.2.2. Vertical Centrifuge

- 6.3. Market Analysis, Insights and Forecast - by Operation Mode

- 6.3.1. Batch

- 6.3.2. Continuous

- 6.4. Market Analysis, Insights and Forecast - by Industry

- 6.4.1. Food and Beverage

- 6.4.2. Pharmaceutical

- 6.4.3. Water and Wastewater Treatment

- 6.4.4. Chemical

- 6.4.5. Metal and Mining

- 6.4.6. Power

- 6.4.7. Pulp and Paper

- 6.4.8. Other Industries

- 6.5. Market Analysis, Insights and Forecast - by Geography

- 6.5.1. United States

- 6.5.2. Canada

- 6.5.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United States North America Industrial Centrifuge Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Sedimentaion

- 7.1.2. Filtering

- 7.2. Market Analysis, Insights and Forecast - by Design

- 7.2.1. Horizontal Centrifuge

- 7.2.2. Vertical Centrifuge

- 7.3. Market Analysis, Insights and Forecast - by Operation Mode

- 7.3.1. Batch

- 7.3.2. Continuous

- 7.4. Market Analysis, Insights and Forecast - by Industry

- 7.4.1. Food and Beverage

- 7.4.2. Pharmaceutical

- 7.4.3. Water and Wastewater Treatment

- 7.4.4. Chemical

- 7.4.5. Metal and Mining

- 7.4.6. Power

- 7.4.7. Pulp and Paper

- 7.4.8. Other Industries

- 7.5. Market Analysis, Insights and Forecast - by Geography

- 7.5.1. United States

- 7.5.2. Canada

- 7.5.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Canada North America Industrial Centrifuge Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Sedimentaion

- 8.1.2. Filtering

- 8.2. Market Analysis, Insights and Forecast - by Design

- 8.2.1. Horizontal Centrifuge

- 8.2.2. Vertical Centrifuge

- 8.3. Market Analysis, Insights and Forecast - by Operation Mode

- 8.3.1. Batch

- 8.3.2. Continuous

- 8.4. Market Analysis, Insights and Forecast - by Industry

- 8.4.1. Food and Beverage

- 8.4.2. Pharmaceutical

- 8.4.3. Water and Wastewater Treatment

- 8.4.4. Chemical

- 8.4.5. Metal and Mining

- 8.4.6. Power

- 8.4.7. Pulp and Paper

- 8.4.8. Other Industries

- 8.5. Market Analysis, Insights and Forecast - by Geography

- 8.5.1. United States

- 8.5.2. Canada

- 8.5.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of North America North America Industrial Centrifuge Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Sedimentaion

- 9.1.2. Filtering

- 9.2. Market Analysis, Insights and Forecast - by Design

- 9.2.1. Horizontal Centrifuge

- 9.2.2. Vertical Centrifuge

- 9.3. Market Analysis, Insights and Forecast - by Operation Mode

- 9.3.1. Batch

- 9.3.2. Continuous

- 9.4. Market Analysis, Insights and Forecast - by Industry

- 9.4.1. Food and Beverage

- 9.4.2. Pharmaceutical

- 9.4.3. Water and Wastewater Treatment

- 9.4.4. Chemical

- 9.4.5. Metal and Mining

- 9.4.6. Power

- 9.4.7. Pulp and Paper

- 9.4.8. Other Industries

- 9.5. Market Analysis, Insights and Forecast - by Geography

- 9.5.1. United States

- 9.5.2. Canada

- 9.5.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Hiller Separation & Process GmbH

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Acutronic USA Inc

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Centrifuges Unlimited Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Flottweg SE

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 GEA Group AG

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 CentraSep Technologies Inc *List Not Exhaustive

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Andritz AG

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Centrisys Corporation

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Alfa Laval AB

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Hiller Separation & Process GmbH

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Industrial Centrifuge Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Industrial Centrifuge Market Share (%) by Company 2025

List of Tables

- Table 1: North America Industrial Centrifuge Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Industrial Centrifuge Market Revenue billion Forecast, by Design 2020 & 2033

- Table 3: North America Industrial Centrifuge Market Revenue billion Forecast, by Operation Mode 2020 & 2033

- Table 4: North America Industrial Centrifuge Market Revenue billion Forecast, by Industry 2020 & 2033

- Table 5: North America Industrial Centrifuge Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: North America Industrial Centrifuge Market Revenue billion Forecast, by Region 2020 & 2033

- Table 7: North America Industrial Centrifuge Market Revenue billion Forecast, by Type 2020 & 2033

- Table 8: North America Industrial Centrifuge Market Revenue billion Forecast, by Design 2020 & 2033

- Table 9: North America Industrial Centrifuge Market Revenue billion Forecast, by Operation Mode 2020 & 2033

- Table 10: North America Industrial Centrifuge Market Revenue billion Forecast, by Industry 2020 & 2033

- Table 11: North America Industrial Centrifuge Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 12: North America Industrial Centrifuge Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: North America Industrial Centrifuge Market Revenue billion Forecast, by Type 2020 & 2033

- Table 14: North America Industrial Centrifuge Market Revenue billion Forecast, by Design 2020 & 2033

- Table 15: North America Industrial Centrifuge Market Revenue billion Forecast, by Operation Mode 2020 & 2033

- Table 16: North America Industrial Centrifuge Market Revenue billion Forecast, by Industry 2020 & 2033

- Table 17: North America Industrial Centrifuge Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 18: North America Industrial Centrifuge Market Revenue billion Forecast, by Country 2020 & 2033

- Table 19: North America Industrial Centrifuge Market Revenue billion Forecast, by Type 2020 & 2033

- Table 20: North America Industrial Centrifuge Market Revenue billion Forecast, by Design 2020 & 2033

- Table 21: North America Industrial Centrifuge Market Revenue billion Forecast, by Operation Mode 2020 & 2033

- Table 22: North America Industrial Centrifuge Market Revenue billion Forecast, by Industry 2020 & 2033

- Table 23: North America Industrial Centrifuge Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 24: North America Industrial Centrifuge Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Industrial Centrifuge Market?

The projected CAGR is approximately 6.7%.

2. Which companies are prominent players in the North America Industrial Centrifuge Market?

Key companies in the market include Hiller Separation & Process GmbH, Acutronic USA Inc, Centrifuges Unlimited Inc, Flottweg SE, GEA Group AG, CentraSep Technologies Inc *List Not Exhaustive, Andritz AG, Centrisys Corporation, Alfa Laval AB.

3. What are the main segments of the North America Industrial Centrifuge Market?

The market segments include Type, Design, Operation Mode, Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.22 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Demand from the Downstream Industry.

6. What are the notable trends driving market growth?

Water and Wastewater Treatment Expected to be the Fastest Growing Market Segment.

7. Are there any restraints impacting market growth?

4.; Adoption of Renewable and Clean Energy Sources.

8. Can you provide examples of recent developments in the market?

August 2022: GEA launched a new range of pharmaceutical industrial centrifuge systems for North America called Kytero. Kytero is ready for manufacturing. Filter regions can be reduced by 75%. The system requires a standard power connection; intermediate tanks are obsolete. The simple exchange eliminates CIP (clean-in-place) and SIP (sterilize-in-place).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Industrial Centrifuge Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Industrial Centrifuge Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Industrial Centrifuge Market?

To stay informed about further developments, trends, and reports in the North America Industrial Centrifuge Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence