Key Insights

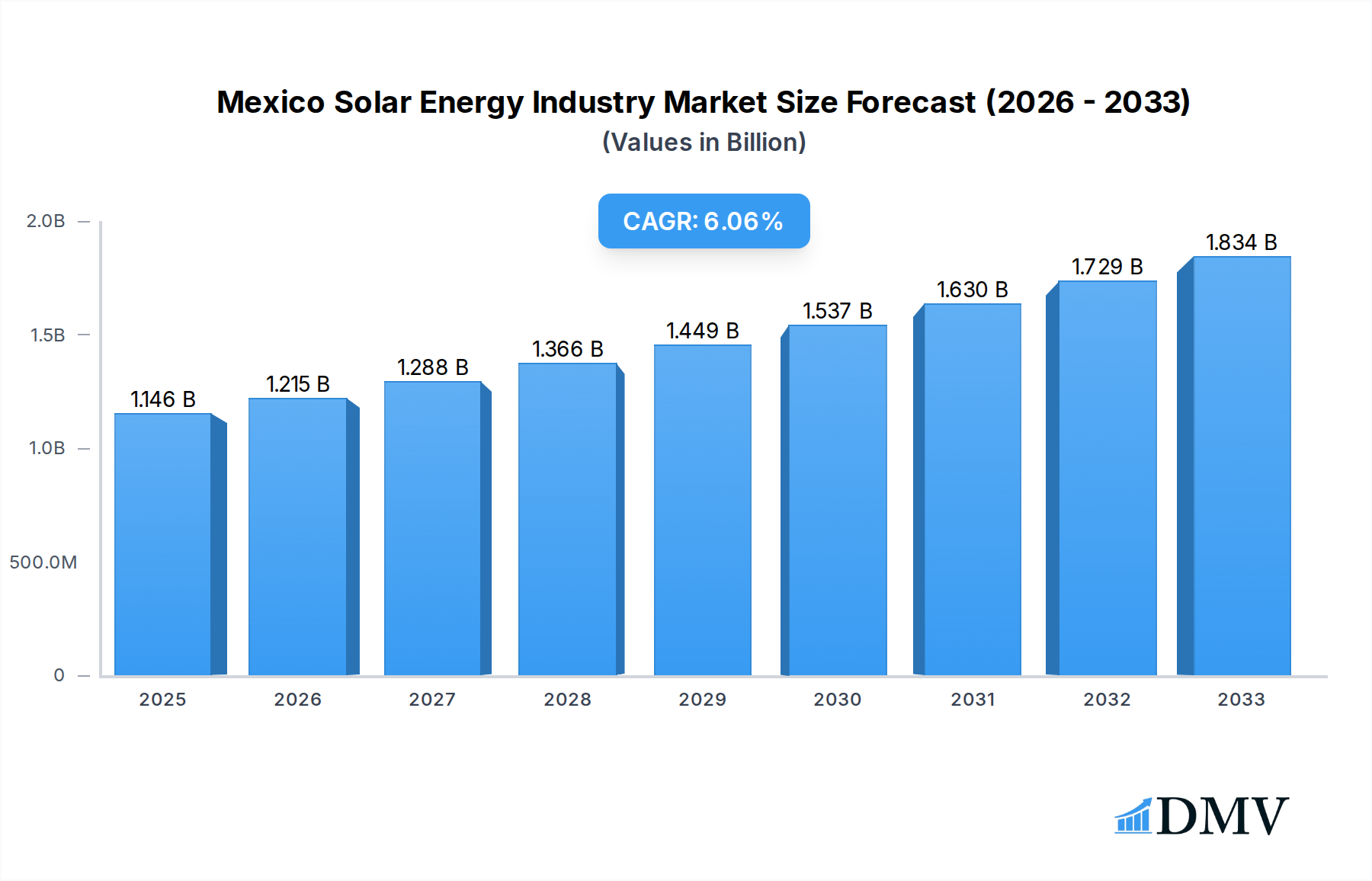

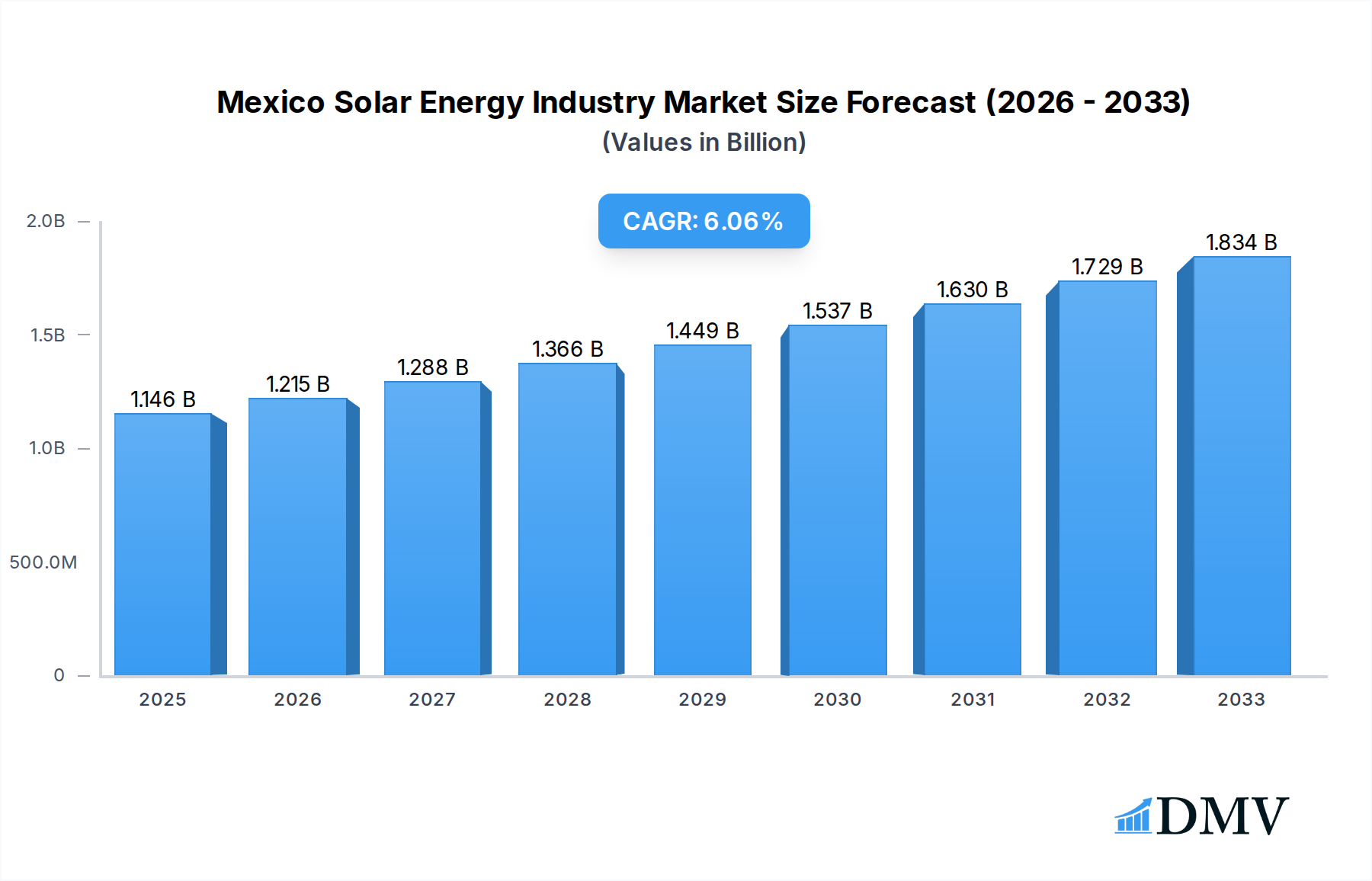

The Mexico Solar Energy Industry is poised for substantial growth, projected to reach an estimated market size of USD 1145.7 million in 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.03% from 2019 to 2033. This expansion is primarily driven by increasing government support for renewable energy, declining solar technology costs, and a growing demand for clean energy solutions across residential, commercial, and utility-scale deployments. Photovoltaic (PV) technology is expected to dominate the market due to its widespread adoption and continuous advancements in efficiency and affordability. The sector benefits from significant investment from key players like Sojitz Corporation, Trina Solar, and Suntech Power, alongside a vibrant ecosystem of solar power plant developers, equipment suppliers, and EPC companies actively contributing to the nation's solar capacity expansion.

Mexico Solar Energy Industry Market Size (In Billion)

The market's upward trajectory is further supported by favorable economic conditions and a growing awareness of climate change imperatives. While emerging trends like energy storage integration and smart grid technologies are set to enhance solar energy's reliability and efficiency, potential challenges such as grid infrastructure limitations and policy uncertainties could temper growth. However, the strong foundational drivers and the active participation of major global and local companies indicate a resilient market. The segment for utility-scale deployments is anticipated to lead in terms of capacity additions, catering to the country's burgeoning energy needs, while residential and commercial sectors will witness steady growth fueled by attractive incentives and cost savings. The strategic importance of solar energy in Mexico's long-term energy security and sustainability goals underpins this optimistic market outlook.

Mexico Solar Energy Industry Company Market Share

Mexico Solar Energy Industry Market Research Report: Forecast to 2033

Explore the dynamic Mexico Solar Energy Industry with our comprehensive market research report. Covering the historical period of 2019–2024 and extending to a forecast period of 2025–2033, this in-depth analysis provides crucial insights for stakeholders in the rapidly expanding renewable energy sector. Our report offers a detailed examination of market composition, trends, industry evolution, regional dominance, product innovations, growth drivers, obstacles, and future opportunities, providing a strategic roadmap for navigating the Mexican solar market. With a base year of 2025, this report is essential for solar power plant developers, equipment suppliers, EPC companies, and investors seeking to capitalize on the immense potential of photovoltaic and CSP technologies.

Mexico Solar Energy Industry Market Composition & Trends

The Mexico Solar Energy Industry is characterized by a moderately concentrated market, driven by significant investment and evolving regulatory frameworks. Key innovation catalysts include advancements in photovoltaic (PV) panel efficiency and the increasing adoption of Concentrated Solar Power (CSP) technologies for utility-scale projects. The regulatory landscape, while dynamic, continues to favor renewable energy growth through supportive policies and incentives. Potential substitute products, such as natural gas, face increasing competition from the declining costs and improving performance of solar solutions. End-user profiles are diversifying, with significant uptake from residential, commercial, and utility-scale segments. Mergers and acquisitions (M&A) activity is a notable trend, indicating a consolidation phase and strategic expansion by major players.

- Market Share Distribution: While precise figures fluctuate, the utility-scale segment currently holds the largest market share, followed by the commercial and residential sectors.

- M&A Deal Values: Recent M&A activities have seen deal values ranging from tens of millions to hundreds of millions of dollars as companies seek to expand their portfolios and integrate vertically.

- Innovation Catalysts: Decreasing Levelized Cost of Energy (LCOE) for solar PV, advancements in battery storage integration, and government-backed renewable energy auctions are key drivers.

- Regulatory Landscape: While some policy shifts have occurred, the long-term commitment to decarbonization and the availability of financing mechanisms remain supportive for industry expansion.

Mexico Solar Energy Industry Industry Evolution

The Mexico Solar Energy Industry has witnessed remarkable evolution throughout the historical period of 2019–2024, setting a strong foundation for robust growth during the forecast period of 2025–2033. Initially, the market was characterized by a nascent stage of development, primarily driven by early adopters and policy incentives aimed at stimulating renewable energy adoption. The utility-scale segment spearheaded this growth, with large-scale solar farms contributing significantly to Mexico's energy mix. Technological advancements, particularly in photovoltaic (PV) technology, have been instrumental in this evolution. The efficiency of solar panels has seen a consistent upward trend, leading to improved energy generation per unit area and a reduction in the overall cost of solar installations. This technological leap has directly impacted the Levelized Cost of Energy (LCOE), making solar power increasingly competitive against traditional fossil fuels.

Consumer demand has also undergone a significant shift. Initially focused on large industrial and utility clients, the demand for solar energy has progressively broadened to encompass the commercial and residential sectors. This expansion is fueled by rising electricity prices, growing environmental awareness, and the availability of financing solutions that make solar accessible to a wider demographic. The base year of 2025 marks a pivotal point where the industry is expected to achieve greater maturity, with established supply chains and a more predictable regulatory environment. This maturity will enable accelerated deployment across all segments. The introduction and refinement of Concentrated Solar Power (CSP) technologies, while still a smaller segment compared to PV, represent another facet of the industry's evolution, offering unique advantages for large-scale energy storage and grid stability.

The market growth trajectory has been impressive, with average annual growth rates in photovoltaic installations consistently exceeding 15% in recent years. This trend is projected to continue, driven by ambitious renewable energy targets and the inherent economic advantages of solar power. The adoption metrics for solar technology have steadily improved, with a significant increase in the installed capacity of solar power plants nationwide. Furthermore, the industry's evolution has been shaped by global trends, including advancements in grid integration technologies, smart metering, and the burgeoning interest in distributed energy resources. As Mexico continues its transition towards a sustainable energy future, the evolution of its solar industry is set to be a defining narrative of its economic and environmental progress.

Leading Regions, Countries, or Segments in Mexico Solar Energy Industry

The Mexico Solar Energy Industry exhibits clear dominance across specific segments and regions, driven by a confluence of economic, regulatory, and geographical factors. The Utility-scale segment stands out as the most dominant segment, accounting for the largest share of installed capacity and investment. This is primarily due to the economies of scale achievable in large solar farms, which attract significant foreign and domestic investment, often facilitated by government tenders and Power Purchase Agreements (PPAs). The regulatory support and land availability in certain regions further bolster the growth of utility-scale projects.

Within the Technology landscape, Photovoltaic (PV) technology overwhelmingly leads, representing over 95% of all solar installations. This dominance is attributed to the continuous reduction in PV panel costs, improvements in efficiency, and the versatility of PV systems, suitable for all deployment scales, from vast utility farms to small residential rooftops. Concentrated Solar Power (CSP), while a significant technology for its energy storage capabilities, remains a niche market in Mexico, primarily explored for large-scale applications where its unique advantages can be leveraged.

Geographically, regions with high solar irradiance and favorable land availability tend to attract the most significant investments. While specific provincial data can vary, states in the northern and central parts of Mexico are generally leading due to their exceptional solar resource potential and existing infrastructure development for large energy projects.

Dominant Deployment Segment: Utility-scale solar projects are the primary drivers of Mexico's solar energy growth, characterized by large-scale solar farms designed to feed directly into the national grid.

- Key Driver: Favorable land availability and access to grid infrastructure for large-scale energy injection.

- Key Driver: Government incentives and competitive bidding processes for utility-scale power generation.

- Key Driver: Significant investment from international developers and independent power producers (IPPs).

Dominant Technology: Photovoltaic (PV) technology is the undisputed leader due to its declining costs, high efficiency, and scalability across all deployment types.

- Key Driver: Continuous innovation leading to lower manufacturing costs and higher energy conversion rates.

- Key Driver: Versatility for both distributed generation (residential, commercial) and utility-scale applications.

- Key Driver: Established global supply chains for PV panels and related components.

Leading Regional Factors: Northern and central Mexico benefit from superior solar irradiance and vast expanses of suitable land for solar farm development.

- Key Driver: High solar insolation levels, maximizing energy generation potential.

- Key Driver: Supportive local government policies and streamlined permitting processes for renewable energy projects.

- Key Driver: Proximity to existing transmission infrastructure for efficient power evacuation.

Mexico Solar Energy Industry Product Innovations

Product innovation in the Mexico Solar Energy Industry is primarily centered on enhancing the efficiency and cost-effectiveness of photovoltaic (PV) systems. Advancements in solar panel technology, including the adoption of bifacial panels and higher-efficiency cell architectures like PERC and TOPCon, are significantly increasing energy yield per square meter. Innovations in inverter technology are also crucial, with smart inverters offering enhanced grid integration, monitoring, and energy management capabilities. Furthermore, the integration of advanced battery storage solutions with solar PV systems is a key development, addressing the intermittency of solar power and enabling greater grid stability and reliable energy supply, especially for commercial and utility-scale deployments.

Propelling Factors for Mexico Solar Energy Industry Growth

The Mexico Solar Energy Industry is propelled by a trifecta of powerful forces: technological advancements, favorable economic conditions, and supportive regulatory frameworks. Technologically, the continuous improvement in photovoltaic (PV) panel efficiency and the declining manufacturing costs have made solar energy increasingly competitive. Economically, the rising cost of conventional energy sources and the growing demand for sustainable power present a compelling case for solar investments. Regulatory support, including renewable energy targets and incentives, further accelerates market penetration across residential, commercial, and utility-scale segments. For instance, government auctions for renewable energy capacity have consistently attracted substantial investment, driving large-scale solar park development.

Obstacles in the Mexico Solar Energy Industry Market

Despite its promising outlook, the Mexico Solar Energy Industry faces several significant obstacles. Regulatory uncertainty and policy shifts can create an unpredictable investment climate, deterring long-term capital commitments. Supply chain disruptions, particularly those affecting the availability and cost of key components like solar panels and inverters, can lead to project delays and increased costs. Intense competition within the market, both from established international players and emerging local companies, can put pressure on profit margins. Furthermore, grid infrastructure limitations in certain regions can hinder the efficient evacuation of power from new solar installations, impacting the economic viability of projects.

Future Opportunities in Mexico Solar Energy Industry

The Mexico Solar Energy Industry is ripe with emerging opportunities. The burgeoning demand for distributed generation presents a significant avenue for residential and commercial solar growth, driven by increasing energy independence aspirations and the desire for cost savings. The continued advancement and cost reduction of battery storage solutions will unlock further potential for reliable solar power integration and grid services. Exploring opportunities in off-grid solar applications for remote communities and expanding the deployment of Concentrated Solar Power (CSP) for industrial heat and electricity generation are also promising areas for future expansion. Furthermore, advancements in solar technology, such as floating solar farms and agri-voltaics, could open up new deployment possibilities.

Major Players in the Mexico Solar Energy Industry Ecosystem

- Sojitz Corporation

- Usol Energy LLC

- Soltec Energias Renovables SL

- Trina Solar Ltd

- Suntech Power Holdings Co

- Martifer Solar SA

- Energia Aljaval SL

- Alten Renewable Energy Developments BV

- Sun Power Corporation

- Jinko Solar Corporation

- Enel Green Power SpA

- Neoen SAS

Key Developments in Mexico Solar Energy Industry Industry

- 2022/08: Enel Green Power SpA announces the commissioning of a new solar PV plant, adding significant capacity to the national grid.

- 2023/01: Trina Solar Ltd expands its supply agreements with major Mexican solar developers, reinforcing its market presence.

- 2023/05: Usol Energy LLC secures funding for several utility-scale solar projects in the northern region, highlighting continued investment in large-scale development.

- 2023/11: Neoen SAS progresses with its large-scale solar farm development, contributing to Mexico's renewable energy targets.

- 2024/02: Soltec Energias Renovables SL introduces innovative solar tracking solutions tailored for the Mexican market, enhancing efficiency for large installations.

- 2024/06: Sun Power Corporation announces partnerships for residential solar installations, indicating growth in the distributed generation segment.

Strategic Mexico Solar Energy Industry Market Forecast

The Mexico Solar Energy Industry is poised for significant and sustained growth, driven by strong underlying fundamentals. The continued decline in solar technology costs, coupled with Mexico's ambitious renewable energy targets, will fuel expansion across all market segments, from residential to utility-scale deployments. The increasing adoption of advanced technologies, including efficient photovoltaic (PV) systems and integrated battery storage, will enhance the reliability and economic competitiveness of solar power. Strategic investments in grid modernization and supportive regulatory policies will be crucial to unlock the full potential of this burgeoning market, positioning Mexico as a leading player in the global renewable energy transition.

Mexico Solar Energy Industry Segmentation

-

1. Deployment

- 1.1. Residential

- 1.2. Commercial

- 1.3. Utility-scale

-

2. Technology

- 2.1. Photovoltaic

- 2.2. CSP

Mexico Solar Energy Industry Segmentation By Geography

- 1. Mexico

Mexico Solar Energy Industry Regional Market Share

Geographic Coverage of Mexico Solar Energy Industry

Mexico Solar Energy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.03% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Utility-scale

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Photovoltaic

- 5.2.2. CSP

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Mexico Solar Energy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Utility-scale

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Photovoltaic

- 6.2.2. CSP

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 1 Sojitz Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 2 Usol Energy LLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Solar Power Plant Developers

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Equipment Suppliers

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 3 Soltec Energias Renovables SL*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 1 Trina Solar Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 1 Suntech Power Holdings Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 2 Martifer Solar SA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 3 Energia Aljaval SL

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 2 Alten Renewable Energy Developments BV

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 4 Sun Power Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 5 Jinko Solar Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 EPC Companies

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 3 Enel Green Power SpA

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 6 Neoen SAS

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 1 Sojitz Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Mexico Solar Energy Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Mexico Solar Energy Industry Share (%) by Company 2025

List of Tables

- Table 1: Mexico Solar Energy Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 2: Mexico Solar Energy Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 3: Mexico Solar Energy Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Mexico Solar Energy Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 5: Mexico Solar Energy Industry Revenue million Forecast, by Technology 2020 & 2033

- Table 6: Mexico Solar Energy Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mexico Solar Energy Industry?

The projected CAGR is approximately 6.03%.

2. Which companies are prominent players in the Mexico Solar Energy Industry?

Key companies in the market include 1 Sojitz Corporation, 2 Usol Energy LLC, Solar Power Plant Developers, Equipment Suppliers, 3 Soltec Energias Renovables SL*List Not Exhaustive, 1 Trina Solar Ltd, 1 Suntech Power Holdings Co, 2 Martifer Solar SA, 3 Energia Aljaval SL, 2 Alten Renewable Energy Developments BV, 4 Sun Power Corporation, 5 Jinko Solar Corporation, EPC Companies, 3 Enel Green Power SpA, 6 Neoen SAS.

3. What are the main segments of the Mexico Solar Energy Industry?

The market segments include Deployment, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 1145.7 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Favorable Government Policies4.; Increasing Demand for Renewable Energy.

6. What are the notable trends driving market growth?

Utility-scale Solar Energy Projects Driving the Renewable Market.

7. Are there any restraints impacting market growth?

4.; Inefficient Grid Infrastructure and A High Number Of Islands in the Country.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mexico Solar Energy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mexico Solar Energy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mexico Solar Energy Industry?

To stay informed about further developments, trends, and reports in the Mexico Solar Energy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence