Key Insights

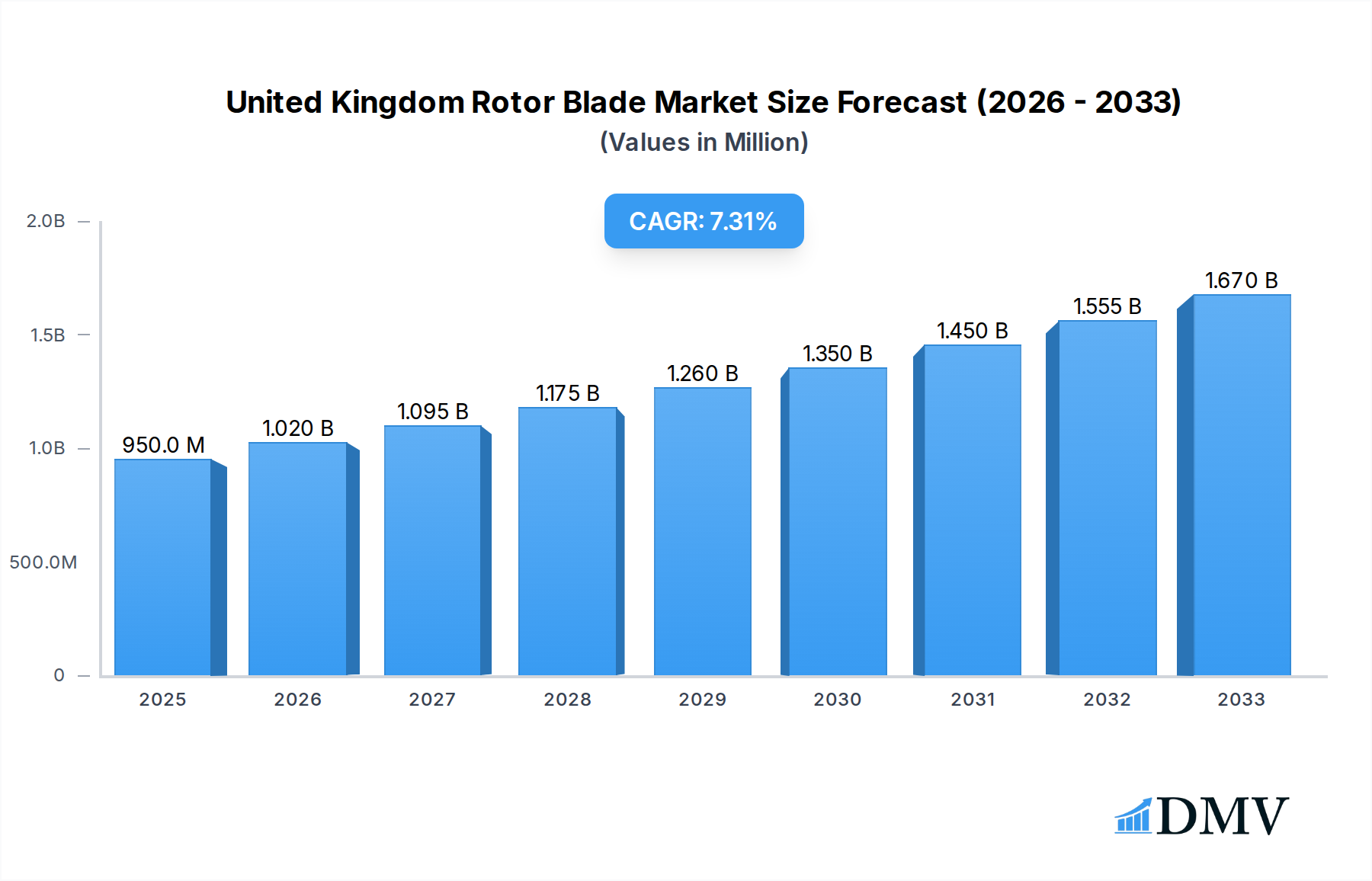

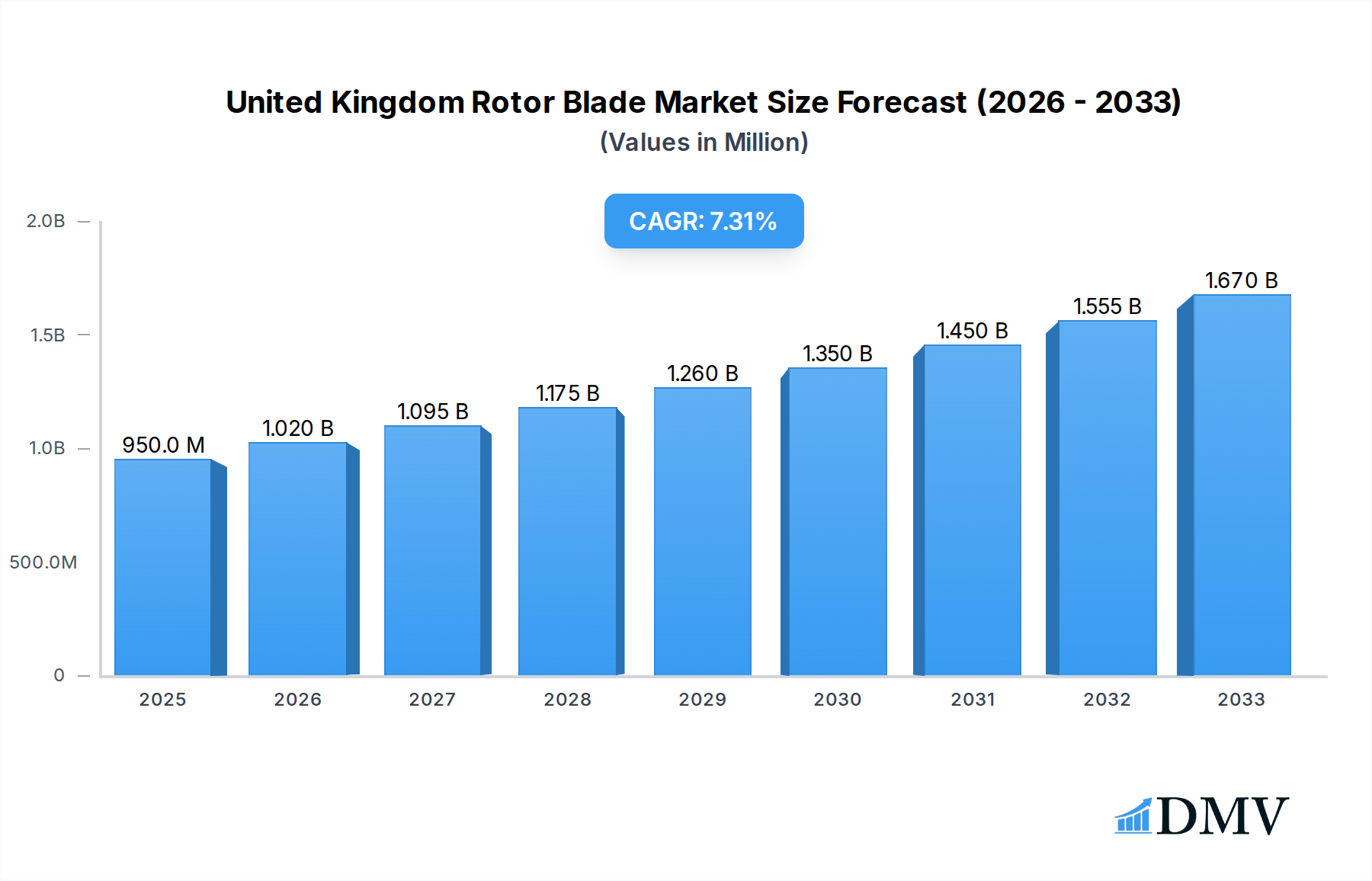

The United Kingdom rotor blade market is poised for significant expansion, with a current market size estimated at £950 million in 2025. This growth is fueled by an impressive Compound Annual Growth Rate (CAGR) of 7.40%, projected to continue through 2033. The increasing demand for renewable energy, driven by ambitious decarbonization targets and government support for offshore wind projects, serves as a primary market driver. Furthermore, technological advancements in blade materials, such as the growing adoption of lighter and more durable carbon fiber composites, are enhancing turbine efficiency and contributing to market expansion. The strategic location of the UK, particularly its extensive coastline ideal for offshore wind farms, positions it as a key player in the global wind energy landscape, further stimulating the rotor blade market.

United Kingdom Rotor Blade Market Market Size (In Million)

The United Kingdom rotor blade market is characterized by dynamic trends and strategic company investments. The dominance of offshore wind installations, which require larger and more sophisticated rotor blades, is a significant trend shaping the market. Companies like Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., and Ørsted A/S are at the forefront, investing heavily in research and development to produce blades optimized for harsh offshore environments. While the market benefits from strong growth drivers, potential restraints include supply chain complexities, the need for specialized infrastructure for transporting and installing larger blades, and evolving regulatory frameworks. However, the overarching commitment to renewable energy and the continuous pursuit of enhanced turbine performance indicate a robust and promising future for the UK's rotor blade sector, with significant opportunities for innovation and investment.

United Kingdom Rotor Blade Market Company Market Share

United Kingdom Rotor Blade Market Market Composition & Trends

The United Kingdom rotor blade market is characterized by a moderate to high degree of concentration, with key players like Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., and Nordex SE holding significant market share. Innovation is a primary catalyst, driven by the continuous pursuit of increased efficiency, durability, and cost reduction in wind turbine blades. The regulatory landscape, underpinned by government targets for renewable energy generation and supportive policies for offshore wind development, plays a crucial role in shaping market dynamics. Substitute products, while not a direct threat to the core rotor blade function, encompass advancements in turbine design and control systems that indirectly impact blade requirements. End-user profiles are predominantly wind farm developers, both onshore and offshore, with a growing interest from utility companies and independent power producers. Merger and acquisition (M&A) activities, though not extensive in recent years, have been instrumental in consolidating market power and expanding technological capabilities. For instance, previous strategic alliances and acquisitions have aimed to secure supply chains and enhance manufacturing prowess.

- Market Share Distribution: Leading companies dominate a substantial portion of the market, with the top three players accounting for an estimated 70% of the market share.

- M&A Deal Values: While specific recent deal values are not publicly disclosed, historical M&A activities in the broader wind energy sector have ranged from hundreds of millions to billions of USD, indicating the strategic importance of component suppliers.

- Innovation Focus: Research and development efforts are concentrated on advanced composite materials, aerodynamic designs, and smart blade technologies.

United Kingdom Rotor Blade Market Industry Evolution

The United Kingdom's rotor blade market has witnessed a dynamic evolution, primarily fueled by the nation's ambitious renewable energy targets and the burgeoning offshore wind sector. Over the study period of 2019–2033, the market has transitioned from a nascent stage to a mature and highly competitive environment. The historical period from 2019 to 2024 saw consistent growth, driven by the installation of new wind farms and the replacement of older, less efficient blades. The base year of 2025 serves as a pivotal point, with an estimated market size of approximately 2,500 million, reflecting the ongoing investments in renewable energy infrastructure. The forecast period of 2025–2033 is projected to experience a robust Compound Annual Growth Rate (CAGR) of around 8.5%, driven by the increasing demand for larger and more powerful wind turbines, particularly in offshore applications. Technological advancements have been a cornerstone of this evolution. The shift towards larger rotor diameters, longer blades, and the utilization of advanced materials like carbon fiber composites have significantly enhanced energy capture efficiency and turbine performance. These advancements are not only driven by the desire for higher energy yields but also by the imperative to reduce the Levelized Cost of Energy (LCOE). The industry has also seen a growing emphasis on blade longevity and reduced maintenance requirements, leading to innovations in coatings, sensor integration for condition monitoring, and design optimization for extreme weather conditions. Consumer demand, in this context, translates to the demand for clean, reliable, and cost-effective energy, which wind power directly addresses. The increasing awareness and commitment to climate change mitigation among both governmental bodies and the general public have further solidified the demand for wind energy and, consequently, for its critical components like rotor blades. The UK's commitment to achieving net-zero emissions by 2050 has been a significant policy driver, leading to substantial investments in wind power capacity, thereby stimulating the demand for rotor blades. Furthermore, the development of specialized manufacturing facilities and the establishment of robust supply chains have played a crucial role in supporting the industry's growth trajectory. The adoption of new manufacturing techniques, such as additive manufacturing for certain components, is also beginning to influence the industry's evolution, promising greater design flexibility and potentially lower production costs.

Leading Regions, Countries, or Segments in United Kingdom Rotor Blade Market

The United Kingdom rotor blade market's dominance is overwhelmingly dictated by its Offshore deployment segment. This pivotal role is a direct consequence of the UK's extensive coastline and strategic geographical positioning, making it a global leader in offshore wind energy generation. The nation's commitment to expanding its offshore wind capacity, evidenced by ambitious government targets and significant private sector investment, has propelled this segment to the forefront.

- Offshore Deployment Dominance: The offshore segment accounts for an estimated 75% of the total market value in 2025, projected to grow to over 80% by 2033. This dominance is fueled by the development of large-scale, high-capacity wind farms in challenging marine environments.

- Investment Trends: Billions of Pounds Sterling are being invested annually in new offshore wind projects, directly translating to substantial demand for high-performance rotor blades capable of withstanding harsh conditions and maximizing energy output.

- Regulatory Support: Favorable policies, including the Contracts for Difference (CfD) scheme, provide long-term revenue certainty for offshore wind projects, de-risking investments and encouraging the deployment of state-of-the-art technologies, including advanced rotor blades.

- Technological Advancements: The development of increasingly longer and lighter blades, often utilizing carbon fiber composites, is specifically tailored for the demands of offshore wind, where larger rotor diameters are crucial for capturing wind energy effectively.

While Onshore deployment remains a significant contributor, its market share is comparatively smaller, estimated at around 20% in 2025. However, growth in this segment is sustained by repowering initiatives and the development of new onshore wind farms in suitable locations.

- Onshore Market Dynamics: The onshore market is driven by a mix of utility-scale projects and smaller community-owned wind farms.

- Repowering Initiatives: Older onshore wind farms are being upgraded with newer, more efficient turbines, leading to a demand for replacement rotor blades.

- Land Availability and Permitting: Challenges related to land availability and the permitting process can sometimes constrain the growth of onshore wind projects compared to offshore.

In terms of Blade Material, Carbon Fiber and Glass Fiber are the dominant materials, with Glass Fiber currently holding a larger market share due to its cost-effectiveness and widespread adoption for onshore applications. However, the Carbon Fiber segment is experiencing robust growth, particularly in offshore wind, where its superior strength-to-weight ratio enables the production of longer and more robust blades required for higher power output.

- Glass Fiber: Represents approximately 60% of the market value in 2025, favored for its balance of performance and cost in a wide range of applications.

- Carbon Fiber: Accounts for roughly 35% of the market value in 2025, but is projected to see higher growth rates due to its critical role in advanced offshore turbine designs.

- Others: Includes hybrid materials and emerging composites, representing a smaller but growing segment driven by ongoing material research and development.

United Kingdom Rotor Blade Market Product Innovations

Product innovations in the UK rotor blade market are predominantly focused on enhancing aerodynamic efficiency, structural integrity, and longevity. Advanced composite materials, including sophisticated carbon fiber and glass fiber blends, are enabling the design of lighter yet stronger blades, leading to increased energy capture and reduced stress on turbine components. Innovations in blade tip designs, such as winglets and serrated edges, are aimed at reducing noise pollution and improving overall aerodynamic performance. Furthermore, the integration of embedded sensors for real-time monitoring of blade health and performance is a growing trend, allowing for predictive maintenance and optimizing operational efficiency. These advancements are crucial for meeting the increasing demands of larger offshore wind turbines and for pushing the boundaries of renewable energy generation.

Propelling Factors for United Kingdom Rotor Blade Market Growth

The United Kingdom rotor blade market is propelled by several key factors. Foremost is the UK's ambitious decarbonization agenda, mandating significant increases in renewable energy capacity, with wind power, especially offshore, at its core. Government policies, such as the Contracts for Difference (CfD) scheme, offer financial certainty for wind farm developers, de-risking investments and stimulating demand for new turbine installations. Technological advancements in blade design and materials, enabling larger, more efficient turbines, are also critical drivers. Growing global awareness of climate change and the economic benefits of renewable energy, including job creation and energy independence, further bolster market growth.

Obstacles in the United Kingdom Rotor Blade Market Market

Despite robust growth, the UK rotor blade market faces several obstacles. The complexity and length of consenting processes for new wind farm developments, particularly offshore, can lead to project delays. Supply chain vulnerabilities, including the availability of raw materials like specialized resins and composite fibers, and manufacturing capacity constraints, can impact production timelines and costs. The significant capital investment required for large-scale offshore wind projects can also be a barrier. Furthermore, evolving environmental regulations and potential public opposition in certain onshore locations can pose challenges. Intense competition among blade manufacturers also exerts downward pressure on prices.

Future Opportunities in United Kingdom Rotor Blade Market

Emerging opportunities in the United Kingdom rotor blade market are significant. The continued expansion of offshore wind capacity, including floating offshore wind technologies, presents a vast avenue for growth, demanding even larger and more specialized rotor blades. Innovations in blade recycling and end-of-life management are becoming increasingly important, creating opportunities for circular economy solutions. The development of smart blades with integrated sensors for advanced diagnostics and control offers potential for improved turbine performance and reduced operational costs. Furthermore, the repowering of aging wind farms with next-generation turbines will sustain demand for replacement blades.

Major Players in the United Kingdom Rotor Blade Market Ecosystem

- Vestas Wind Systems A/S

- Vattenfall AB

- Siemens Gamesa Renewable Energy S A

- Enercon GmbH

- BayWa R E AG

- Orsted A/S

- Nordex SE

Key Developments in United Kingdom Rotor Blade Market Industry

- 2023: Continued investment in port infrastructure to support the construction of larger offshore wind farms and the manufacturing of associated components, including rotor blades.

- 2023: Increased focus on the development of longer and lighter rotor blades, utilizing advanced carbon fiber composites to maximize energy yield from offshore wind turbines.

- 2024: Growing interest in sustainable blade manufacturing processes, including the exploration of bio-based resins and advanced recycling technologies for end-of-life blades.

- 2024: Several key players announced plans for significant capacity expansions in their manufacturing facilities to meet the surging demand for offshore wind turbines.

- 2024: Advancements in blade monitoring technologies, with enhanced integration of sensors for predictive maintenance and real-time performance optimization.

Strategic United Kingdom Rotor Blade Market Market Forecast

The strategic forecast for the United Kingdom rotor blade market is exceptionally positive, underpinned by the nation's unwavering commitment to achieving net-zero emissions and its leading position in offshore wind energy. The continuous push for larger and more efficient wind turbines, particularly for the burgeoning offshore sector, will drive consistent demand for advanced rotor blades. Technological innovations in materials science and aerodynamic design will further enhance performance and cost-effectiveness. Supportive government policies, substantial private sector investment, and the growing imperative for energy security and sustainability collectively create a fertile ground for sustained market expansion and significant growth opportunities in the coming years.

United Kingdom Rotor Blade Market Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

-

2. Blade Material

- 2.1. Carbon Fiber

- 2.2. Glass Fiber

- 2.3. Others

United Kingdom Rotor Blade Market Segmentation By Geography

- 1. United Kingdom

United Kingdom Rotor Blade Market Regional Market Share

Geographic Coverage of United Kingdom Rotor Blade Market

United Kingdom Rotor Blade Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Blade Material

- 5.2.1. Carbon Fiber

- 5.2.2. Glass Fiber

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. United Kingdom Rotor Blade Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Blade Material

- 6.2.1. Carbon Fiber

- 6.2.2. Glass Fiber

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Vestas Wind Systems A/S

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Vattenfall AB

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Siemens Gamesa Renewable Energy S A

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Enercon GmbH6 4 Market Ranking Analysi

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BayWa R E AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Orsted A/S

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nordex SE

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 Vestas Wind Systems A/S

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom Rotor Blade Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United Kingdom Rotor Blade Market Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 2: United Kingdom Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 3: United Kingdom Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 4: United Kingdom Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 5: United Kingdom Rotor Blade Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: United Kingdom Rotor Blade Market Volume K Units Forecast, by Region 2020 & 2033

- Table 7: United Kingdom Rotor Blade Market Revenue Million Forecast, by Location of Deployment 2020 & 2033

- Table 8: United Kingdom Rotor Blade Market Volume K Units Forecast, by Location of Deployment 2020 & 2033

- Table 9: United Kingdom Rotor Blade Market Revenue Million Forecast, by Blade Material 2020 & 2033

- Table 10: United Kingdom Rotor Blade Market Volume K Units Forecast, by Blade Material 2020 & 2033

- Table 11: United Kingdom Rotor Blade Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Rotor Blade Market Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom Rotor Blade Market?

The projected CAGR is approximately 7.40%.

2. Which companies are prominent players in the United Kingdom Rotor Blade Market?

Key companies in the market include Vestas Wind Systems A/S, Vattenfall AB, Siemens Gamesa Renewable Energy S A, Enercon GmbH6 4 Market Ranking Analysi, BayWa R E AG, Orsted A/S, Nordex SE.

3. What are the main segments of the United Kingdom Rotor Blade Market?

The market segments include Location of Deployment, Blade Material.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.95 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Number of Offshore Wind Energy Installations4.; Increased Investments in the Wind Power Sector.

6. What are the notable trends driving market growth?

Offshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Cost of Transportation.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom Rotor Blade Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom Rotor Blade Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom Rotor Blade Market?

To stay informed about further developments, trends, and reports in the United Kingdom Rotor Blade Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence