Key Insights

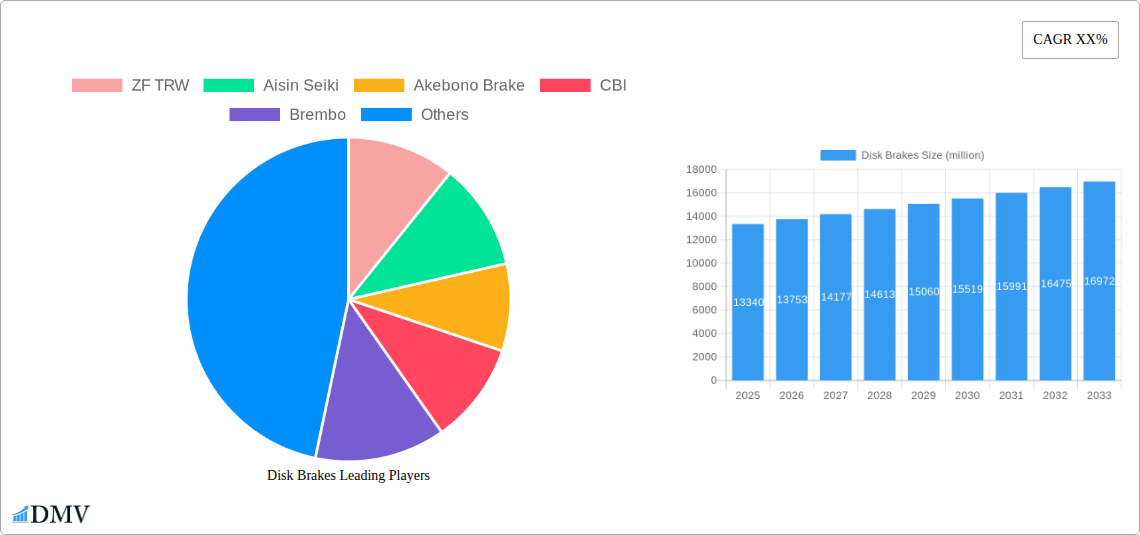

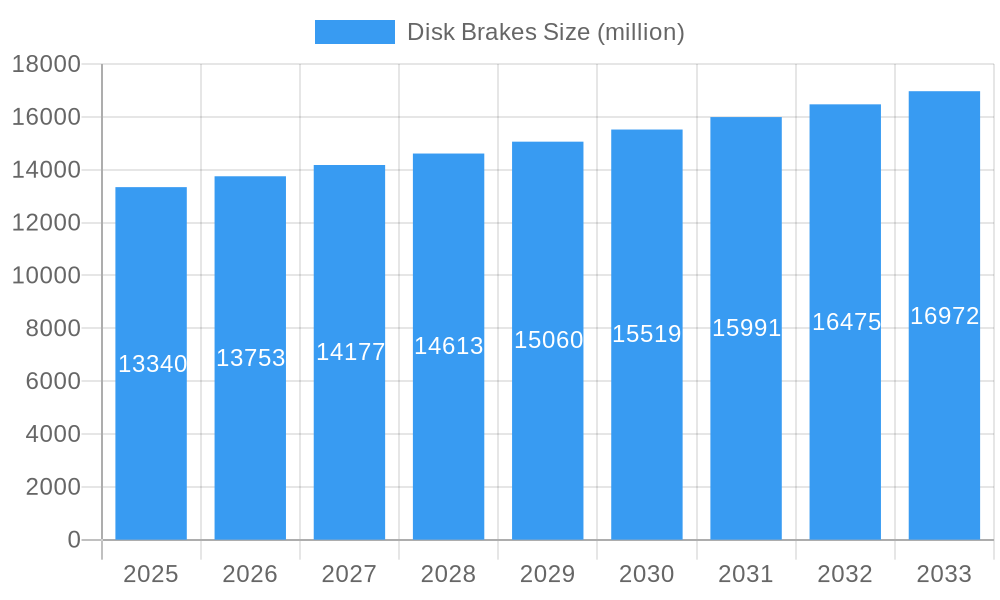

The global disk brake market is poised for significant growth, projected to reach USD 13,340 million by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 3.1% through 2033. This expansion is primarily driven by the increasing global vehicle production across passenger cars, commercial vehicles, and motorcycles. The escalating demand for enhanced vehicle safety features and the continuous technological advancements in braking systems, such as the development of lighter, more efficient, and corrosion-resistant disk brake components, are key catalysts for this upward trajectory. Furthermore, stricter automotive safety regulations worldwide are compelling manufacturers to integrate advanced braking solutions, further fueling market demand. The growing adoption of electric vehicles (EVs) also contributes to this trend, as regenerative braking systems often work in conjunction with traditional disk brakes, creating a synergistic demand.

Disk Brakes Market Size (In Billion)

The market segmentation reveals a dominant share held by the Passenger Cars application segment, owing to the sheer volume of passenger vehicle production. However, the Commercial Vehicles segment is expected to witness robust growth driven by the increasing adoption of advanced braking systems in heavy-duty trucks and buses to comply with stringent safety mandates. Innovations in materials science, leading to lighter and more durable brake components, and the development of intelligent braking systems that offer predictive maintenance and enhanced performance, are emerging trends shaping the market landscape. Despite the positive outlook, factors such as the relatively higher cost of disk brake systems compared to drum brakes, particularly in certain emerging markets, and the potential disruption from entirely new braking technologies in the long term, present potential restraints to market expansion. However, the overwhelming focus on safety and performance in the automotive industry is expected to mitigate these challenges.

Disk Brakes Company Market Share

Here is your SEO-optimized and insightful report description for Disk Brakes, designed for maximum visibility and stakeholder engagement.

Disk Brakes Market Composition & Trends

The global disk brakes market is characterized by a dynamic interplay of innovation, stringent regulatory frameworks, and evolving end-user demands. Market concentration is moderately fragmented, with key players like ZF TRW, Aisin Seiki, Akebono Brake, and Brembo holding significant market share, collectively accounting for an estimated XXX million in revenue in 2025. Continuous innovation is a critical catalyst, driven by the pursuit of enhanced safety, lighter materials, and improved braking performance. The regulatory landscape, particularly concerning automotive safety standards and emissions, significantly influences product development and market entry. While direct substitute products are limited, advancements in regenerative braking systems for electric vehicles present a competitive consideration. End-user profiles span a diverse spectrum, from individual passenger car owners prioritizing safety and performance to fleet managers of commercial vehicles seeking durability and reduced maintenance costs. M&A activities, valued in the hundreds of millions, have played a pivotal role in shaping the market, with recent deals indicating a consolidation trend focused on expanding technological capabilities and market reach. For instance, the acquisition of smaller, specialized component manufacturers by larger entities often aims to integrate advanced materials or novel manufacturing processes. This strategic consolidation is expected to continue as companies seek to optimize their product portfolios and leverage economies of scale in a competitive global environment.

- Market Share Distribution: Key players such as ZF TRW, Aisin Seiki, and Brembo are projected to hold a substantial portion of the market, with an estimated XXX million in collective revenue for the base year 2025.

- M&A Deal Values: Recent strategic acquisitions and mergers are estimated to have involved transactions ranging from tens to hundreds of millions, reflecting consolidation and expansion strategies.

- Innovation Catalysts: Ongoing research and development in areas like advanced materials (e.g., carbon-ceramic), smart braking systems, and weight reduction are driving market advancements.

- Regulatory Influence: Global safety mandates and environmental regulations are increasingly shaping the design and performance specifications of disk brake systems.

- End-User Diversification: Demand originates from passenger cars, commercial vehicles, motorcycles, and specialized sectors like rail and aircraft.

Disk Brakes Industry Evolution

The disk brakes industry has undergone a remarkable evolution, driven by an insatiable demand for enhanced automotive safety, performance, and efficiency. Throughout the historical period of 2019–2024, the market witnessed a steady upward trajectory, fueled by increasing vehicle production globally and a growing awareness among consumers regarding the critical role of effective braking systems. The base year of 2025 marks a significant juncture, with an estimated market size of XXX million, poised for sustained growth during the forecast period of 2025–2033. This growth is intrinsically linked to technological advancements that have redefined the capabilities of disk brakes. Early disk brake systems, while a significant improvement over drum brakes, have been progressively refined. Modern disk brakes incorporate sophisticated materials, advanced caliper designs, and integrated electronic systems that deliver superior stopping power, fade resistance, and reduced wear. The shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) has introduced new dynamics, necessitating the development of disk brake systems that can effectively integrate with regenerative braking technologies. This integration requires precise control and optimization to ensure seamless transitions between friction braking and regenerative energy capture, thereby maximizing efficiency and range. Consumer demands have also evolved, with a growing preference for quieter operation, longer lifespan, and aesthetically pleasing brake components, particularly in the premium vehicle segment. Furthermore, advancements in manufacturing processes, including precision machining and material science, have enabled the production of lighter, more durable, and cost-effective disk brake components. The industry's commitment to research and development has been paramount, with a continuous focus on improving heat dissipation, reducing unsprung mass, and enhancing overall braking predictability and responsiveness. This relentless pursuit of innovation ensures that disk brake technology remains at the forefront of vehicle safety and performance, adapting to the evolving needs of the automotive landscape. The global adoption of advanced driver-assistance systems (ADAS) also plays a crucial role, as these systems often rely on the precise and rapid actuation capabilities of advanced disk brake systems for functionalities like automatic emergency braking (AEB). The increasing complexity of vehicle electronics and the integration of sensors and actuators demand disk brake systems that are not only robust but also highly responsive and controllable. The market's trajectory is also influenced by global economic factors, infrastructure development, and consumer purchasing power, all of which contribute to the overall demand for vehicles and, consequently, for their critical braking components. The historical growth rate, averaging an impressive XX% annually from 2019 to 2024, is projected to continue its robust expansion, reaching an estimated XXX million by 2033, underscoring the indispensable nature of disk brake technology in modern transportation.

Leading Regions, Countries, or Segments in Disk Brakes

The global disk brakes market is dominated by the Passenger Cars segment, driven by the sheer volume of production and consumption of these vehicles worldwide. This dominance is further amplified by stringent safety regulations across major automotive markets and a consistent consumer demand for enhanced driving experience, which includes reliable and high-performance braking. Within this application segment, the Floating Caliper Type of disk brakes remains the most prevalent due to its cost-effectiveness, simplicity, and widespread adoption across various vehicle platforms.

Key drivers contributing to the dominance of Passenger Cars and Floating Caliper types include:

- Mass Production & Economies of Scale: The automotive industry's reliance on mass production techniques for passenger cars allows manufacturers to leverage economies of scale in producing floating caliper disk brake systems, thereby reducing per-unit costs and making them highly accessible.

- Regulatory Mandates: Global vehicle safety standards, such as those enforced by NHTSA in the US and UNECE regulations in Europe, mandate advanced braking capabilities, pushing for the widespread adoption of disk brakes in all passenger vehicles. The increasing focus on pedestrian safety and collision avoidance systems further necessitates the precision and responsiveness offered by disk brakes.

- Consumer Expectations: Modern car buyers expect a high level of safety and performance. The smooth, powerful, and predictable braking provided by disk brakes has become a benchmark, influencing purchasing decisions and OEM specifications.

- Technological Advancements in Floating Calipers: Continuous innovation in floating caliper design, including improved sealing mechanisms, lighter materials, and enhanced piston actuation, has further cemented their position. These advancements have allowed them to meet the performance demands of increasingly heavier and faster passenger vehicles, including the growing segment of electric vehicles.

- Adaptability to EV Powertrains: While regenerative braking is crucial for EVs, traditional friction braking remains essential for full braking capability and emergency stops. Floating caliper designs are adaptable to the integration with EV architectures, providing a reliable backup and complement to regenerative systems. The market for EVs, a rapidly expanding segment within passenger cars, therefore continues to drive demand for advanced disk brake solutions.

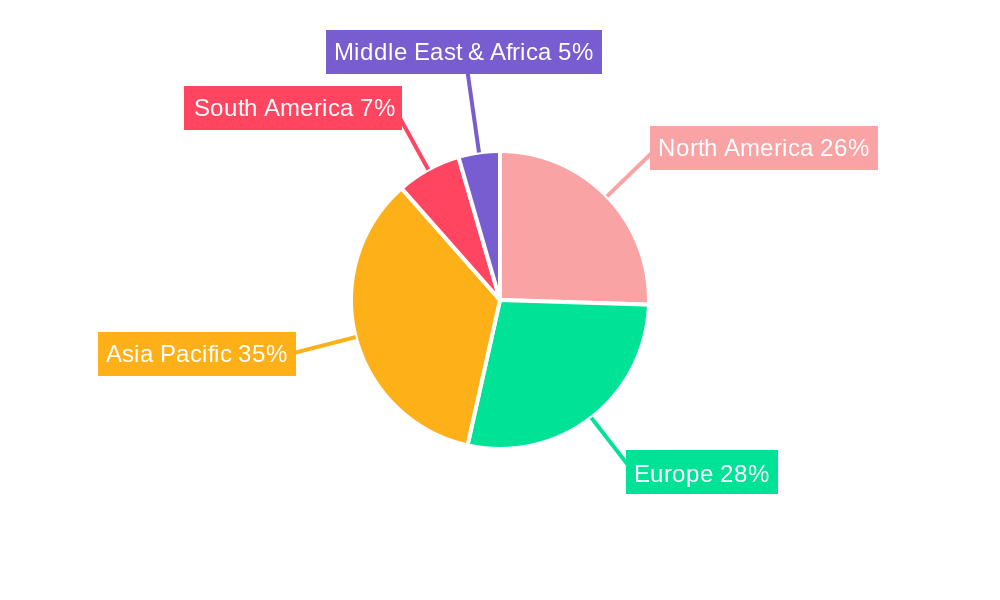

Regionally, Asia Pacific emerges as a leading hub for disk brake manufacturing and consumption, owing to its status as the world's largest automotive market. Countries like China, Japan, and South Korea, with their massive vehicle production volumes and growing domestic demand for passenger vehicles, significantly contribute to the regional dominance. The presence of major automotive manufacturers and a robust supply chain infrastructure further solidify Asia Pacific's leading position. North America and Europe also represent substantial markets, driven by stringent safety standards, a high per-capita vehicle ownership, and a strong focus on technological innovation in the automotive sector. The ongoing transition to electric mobility across these regions is also expected to drive the demand for advanced disk brake systems that can effectively integrate with hybrid and electric powertrains.

Disk Brakes Product Innovations

Recent disk brake product innovations are revolutionizing vehicle safety and performance. Manufacturers are increasingly focusing on lightweight materials like aluminum alloys and advanced composites to reduce unsprung mass, thereby enhancing handling and fuel efficiency. Developments in high-performance friction materials offer superior stopping power and fade resistance, even under extreme conditions. Furthermore, the integration of smart technologies, such as embedded sensors for wear monitoring and predictive maintenance alerts, is becoming a key selling proposition. Electromechanical braking (EMB) systems, while still in early adoption stages, represent a significant leap forward, offering faster response times and greater integration with autonomous driving features. The pursuit of quieter operation and reduced brake dust emissions is also a prominent area of innovation, addressing both consumer comfort and environmental concerns.

Propelling Factors for Disk Brakes Growth

The disk brakes market is propelled by several key factors. Increasing global vehicle production, particularly in emerging economies, directly translates to higher demand for braking systems. Stringent automotive safety regulations worldwide are a significant driver, mandating the adoption of advanced braking technologies like disk brakes for enhanced vehicle safety. The growing adoption of electric and hybrid vehicles necessitates sophisticated braking solutions, including disk brakes that can effectively complement regenerative braking. Furthermore, consumer demand for improved performance, durability, and comfort in vehicles pushes manufacturers to invest in and incorporate advanced disk brake technologies.

Obstacles in the Disk Brakes Market

Despite robust growth, the disk brakes market faces several obstacles. The high cost of advanced materials and manufacturing processes can be a barrier, especially for entry-level vehicles and in price-sensitive markets. Supply chain disruptions, as experienced globally in recent years, can impact the availability of raw materials and components, leading to production delays and increased costs. Intense competition among established players and emerging manufacturers can put pressure on profit margins. Additionally, while disk brakes are superior to drum brakes, ongoing research into alternative braking technologies and the increasing reliance on regenerative braking in EVs presents a long-term competitive consideration.

Future Opportunities in Disk Brakes

Significant future opportunities lie in the continued expansion of the electric vehicle market, which demands innovative disk brake solutions that integrate seamlessly with regenerative braking. The development of lighter, more compact, and intelligent braking systems catering to the evolving needs of autonomous driving and advanced driver-assistance systems (ADAS) presents a lucrative avenue. Furthermore, emerging markets with a rapidly growing automotive sector offer substantial potential for market penetration. Opportunities also exist in developing sustainable and eco-friendly braking materials and in offering predictive maintenance solutions through connected vehicle technologies.

Major Players in the Disk Brakes Ecosystem

- ZF TRW

- Aisin Seiki

- Akebono Brake

- CBI

- Brembo

- Continental

- APG

- Mando

- Knorr-Bremse

- Nissin Kogyo

- Wabco

- Haldex

- Shandong Aoyou

- Hayes Disc Brake

- Knott Brake

- SRAM

- Sheldon Brown

- EBC Brakes

- SilverBack HD

- Ausco Products

- Eaton

- PJ Trailers

- AL-KO

- Meritor

Key Developments in Disk Brakes Industry

- 2023: Launch of advanced lightweight aluminum alloy calipers by Brembo, reducing unsprung mass by XX%.

- 2023: ZF TRW introduces new friction materials for enhanced durability and reduced wear in commercial vehicles.

- 2022: Akebono Brake announces development of a novel brake pad compound for improved wet braking performance in motorcycles.

- 2022: Continental invests heavily in R&D for electromechanical braking (EMB) systems, projecting mass production by 2028.

- 2021: Knorr-Bremse acquires a leading supplier of brake control systems for rail applications, expanding its integrated solutions.

- 2021: Shandong Aoyou focuses on expanding its production capacity for disk brake assemblies targeting the growing EV market in China.

- 2020: EBC Brakes introduces a new range of performance brake discs with improved thermal dissipation properties.

- 2019: Mando showcases an integrated braking system for autonomous vehicles, combining disk brakes with advanced sensor technology.

Strategic Disk Brakes Market Forecast

The strategic forecast for the disk brakes market is exceptionally positive, driven by the unwavering demand for enhanced vehicle safety and performance across all mobility segments. The ongoing transition to electric vehicles will be a pivotal growth catalyst, requiring sophisticated disk brake systems that can integrate with regenerative braking technologies. Continued advancements in material science and smart technology integration will unlock new opportunities for lighter, more durable, and intelligent braking solutions. Emerging economies and the expanding commercial vehicle sector will further contribute to market expansion, solidifying the indispensable role of disk brakes in the future of transportation. The market is poised for sustained growth, with an estimated reach of XXX million by 2033.

Disk Brakes Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

- 1.3. Motocycles and Scooters

- 1.4. Rail and Aircraft

- 1.5. Other

-

2. Types

- 2.1. Opposed Piston Type

- 2.2. Floating Caliper Type

Disk Brakes Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Disk Brakes Regional Market Share

Geographic Coverage of Disk Brakes

Disk Brakes REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.1.3. Motocycles and Scooters

- 5.1.4. Rail and Aircraft

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Opposed Piston Type

- 5.2.2. Floating Caliper Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.1.3. Motocycles and Scooters

- 6.1.4. Rail and Aircraft

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Opposed Piston Type

- 6.2.2. Floating Caliper Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.1.3. Motocycles and Scooters

- 7.1.4. Rail and Aircraft

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Opposed Piston Type

- 7.2.2. Floating Caliper Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.1.3. Motocycles and Scooters

- 8.1.4. Rail and Aircraft

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Opposed Piston Type

- 8.2.2. Floating Caliper Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.1.3. Motocycles and Scooters

- 9.1.4. Rail and Aircraft

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Opposed Piston Type

- 9.2.2. Floating Caliper Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Disk Brakes Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.1.3. Motocycles and Scooters

- 10.1.4. Rail and Aircraft

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Opposed Piston Type

- 10.2.2. Floating Caliper Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ZF TRW

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Aisin Seiki

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Akebono Brake

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CBI

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Brembo

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Continental

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 APG

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mando

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Knorr-Bremse

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Nissin Kogyo

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Wabco

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Haldex

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Shandong Aoyou

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Hayes Disc Brake

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Knott Brake

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 SRAM

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Sheldon Brown

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 EBC Brakes

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 SilverBack HD

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ausco Products

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Eaton

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 PJ Trailers

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 AL-KO

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Meritor

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.1 ZF TRW

List of Figures

- Figure 1: Global Disk Brakes Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Disk Brakes Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Disk Brakes Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Disk Brakes Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Disk Brakes Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Disk Brakes Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Disk Brakes Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Disk Brakes Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Disk Brakes Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Disk Brakes Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Disk Brakes Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Disk Brakes Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Disk Brakes Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Disk Brakes Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Disk Brakes Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Disk Brakes Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Disk Brakes Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Disk Brakes Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Disk Brakes Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Disk Brakes Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Disk Brakes Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Disk Brakes Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Disk Brakes Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Disk Brakes Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Disk Brakes Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Disk Brakes Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Disk Brakes Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Disk Brakes Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Disk Brakes Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Disk Brakes Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Disk Brakes Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Disk Brakes Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Disk Brakes Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Disk Brakes Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Disk Brakes Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Disk Brakes Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Disk Brakes Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Disk Brakes Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Disk Brakes Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Disk Brakes Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Disk Brakes?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the Disk Brakes?

Key companies in the market include ZF TRW, Aisin Seiki, Akebono Brake, CBI, Brembo, Continental, APG, Mando, Knorr-Bremse, Nissin Kogyo, Wabco, Haldex, Shandong Aoyou, Hayes Disc Brake, Knott Brake, SRAM, Sheldon Brown, EBC Brakes, SilverBack HD, Ausco Products, Eaton, PJ Trailers, AL-KO, Meritor.

3. What are the main segments of the Disk Brakes?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Disk Brakes," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Disk Brakes report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Disk Brakes?

To stay informed about further developments, trends, and reports in the Disk Brakes, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence