Key Insights

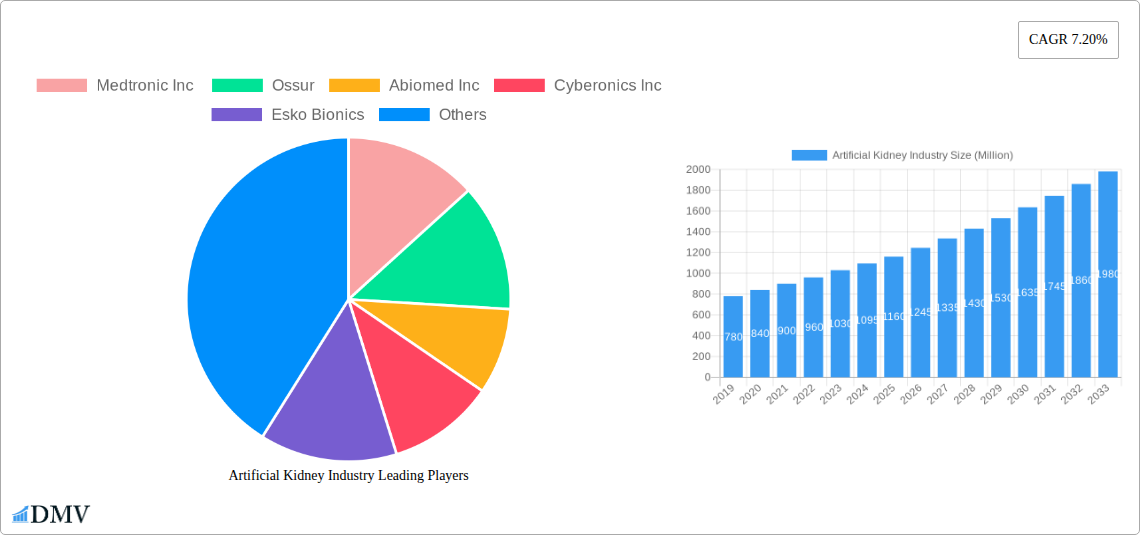

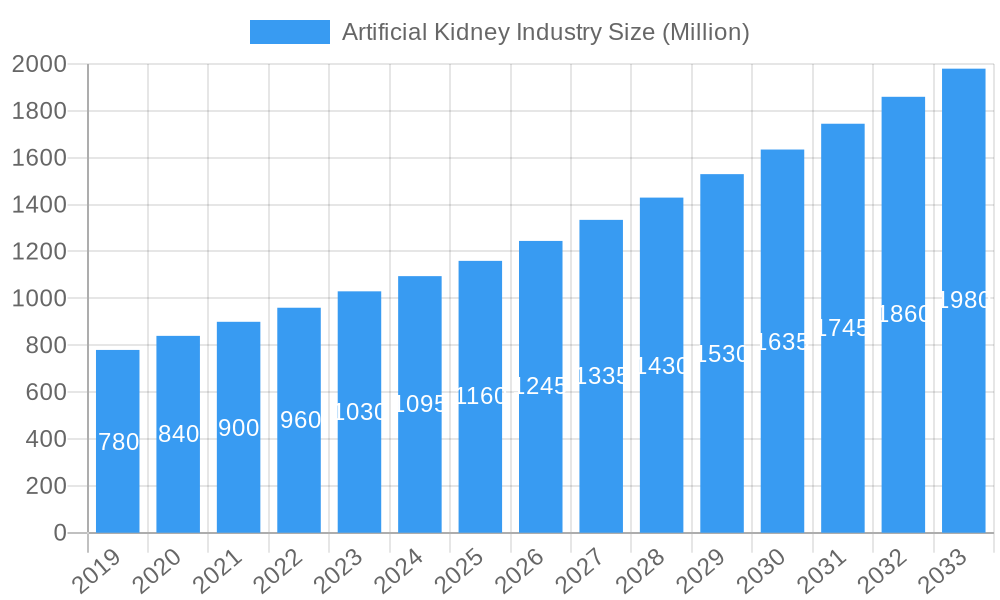

The global Artificial Kidney market is poised for significant expansion, projected to reach $1.16 Billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 7.20% throughout the forecast period of 2025-2033. This substantial growth is propelled by an increasing prevalence of kidney diseases, a rising aging population susceptible to renal complications, and continuous advancements in biomaterials and bioengineering. The market is witnessing a strong demand for artificial organ technologies, with artificial kidneys occupying a crucial segment. Key drivers include the growing need for long-term dialysis solutions and the potential for implantable artificial kidney devices to offer a more convenient and less invasive alternative to traditional treatments. Furthermore, the expanding healthcare infrastructure in emerging economies and increasing patient awareness are also contributing to market dynamism.

Artificial Kidney Industry Market Size (In Million)

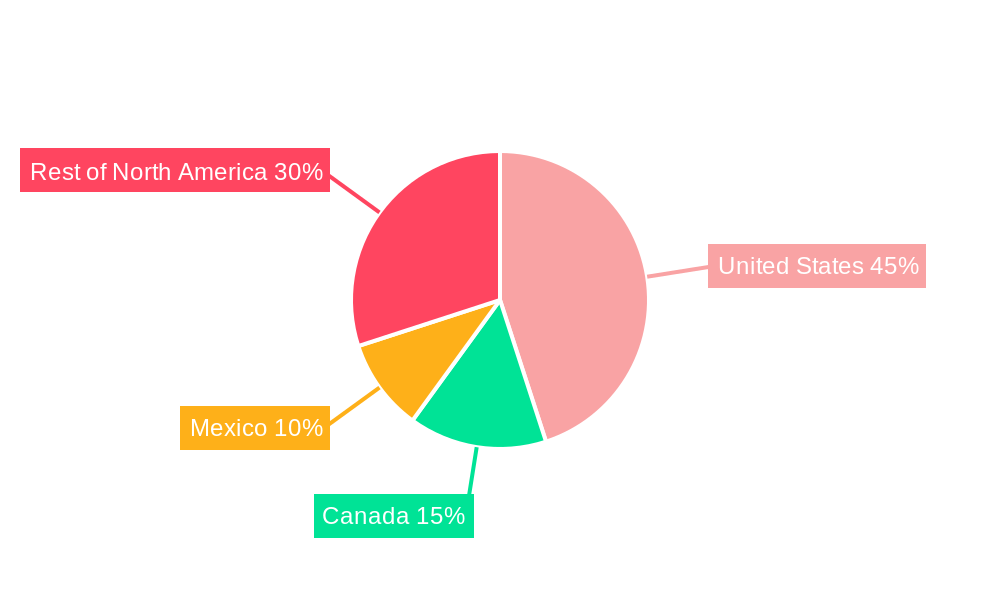

The market is segmented into Artificial Organs and Bionics, with Artificial Kidneys forming a critical sub-segment within Artificial Organs. The growth trajectory is further supported by technological innovations leading to improved biocompatibility, efficiency, and patient outcomes. The United States is expected to be a dominant market, driven by high healthcare spending, advanced research and development, and a large patient pool. Canada and Mexico also represent growing markets, with increasing investments in healthcare technology and a rising incidence of chronic kidney disease. Restraints, such as the high cost of development and manufacturing, regulatory hurdles, and the need for extensive clinical trials, are being progressively addressed through collaborative efforts and technological breakthroughs. Emerging trends include the development of wearable artificial kidneys and regenerative approaches, promising to revolutionize kidney disease management.

Artificial Kidney Industry Company Market Share

This in-depth report provides a definitive analysis of the global Artificial Kidney market, encompassing artificial organs, bionics, and related technologies. Delving into the period from 2019 to 2033, with a base and estimated year of 2025, this research offers unparalleled insights into market dynamics, innovation landscapes, and future growth trajectories. Covering critical segments like Artificial Organs (Artificial Heart, Artificial Kidney, Artificial Lungs, Cochlear Implants, Other Organ Types) and Bionics (Vision Bionics, Ear Bionics, Orthopedic Bionic, Cardiac Bionics), alongside geographical analysis of the United States, Canada, and Mexico, this report is an indispensable tool for stakeholders seeking to navigate the evolving artificial kidney industry. With an estimated market size projected to reach $XX Billion by 2033, driven by advancements in bioartificial kidney development and increasing adoption of advanced cardiac and organ support systems, this report is crucial for strategic decision-making.

Artificial Kidney Industry Market Composition & Trends

The Artificial Kidney industry is characterized by a dynamic and evolving market composition, with a significant focus on groundbreaking innovations and strategic acquisitions. Market concentration is moderate, with key players vying for market share through continuous research and development. Innovation catalysts include the increasing prevalence of chronic kidney disease (CKD), end-stage renal disease (ESRD), and cardiovascular conditions, driving demand for advanced artificial organ solutions. The regulatory landscape is stringent, with bodies like the FDA and EMA playing a crucial role in approving new technologies, thereby influencing market entry and growth. Substitute products, primarily traditional dialysis methods, are gradually being challenged by more sophisticated artificial kidney technologies and bioengineered solutions. End-user profiles are diverse, encompassing hospitals, specialized clinics, research institutions, and a growing number of patients seeking improved quality of life through organ replacement and augmentation. Merger and acquisition (M&A) activities are pivotal in shaping the market, with significant deal values observed as companies aim to consolidate expertise and expand their product portfolios. For instance, recent M&A activities in the broader artificial organ market have seen deals valued in the hundreds of millions of dollars, reflecting a strong consolidation trend. While specific M&A deal values within the pure artificial kidney segment are still emerging, the overall trend indicates a strategic push towards market leadership. The market share distribution for artificial organs is evolving, with artificial kidneys projected to capture a significant portion as bioartificial kidney research advances, potentially reaching XX% of the total artificial organ market by 2033.

Artificial Kidney Industry Industry Evolution

The Artificial Kidney industry has undergone a remarkable evolution, transitioning from rudimentary artificial organ concepts to sophisticated, bio-integrated technologies. The historical period (2019–2024) witnessed steady growth, propelled by advancements in materials science, miniaturization of components, and a growing understanding of biological integration. Early iterations of artificial organs, while life-saving, were often bulky and posed significant challenges for patients. However, the ongoing research and development efforts have significantly improved device functionality, biocompatibility, and patient outcomes. The forecast period (2025–2033) is poised for accelerated growth, driven by several key factors. Technological advancements are at the forefront, with the development of implantable artificial kidneys and advanced ventricular assist devices (VADs) leading the charge. These innovations aim to provide more permanent solutions to organ failure, moving beyond temporary support systems. The market growth trajectory is projected to be robust, with an estimated Compound Annual Growth Rate (CAGR) of XX% during the forecast period. This growth is supported by significant investments in research and development by leading companies, aiming to overcome the complexities of organ rejection and improve long-term device performance. Shifting consumer demands are also playing a crucial role. Patients and their families are increasingly seeking solutions that offer a higher quality of life, greater independence, and fewer hospital visits. This has intensified the focus on developing less invasive, more user-friendly, and more durable artificial organ systems. For instance, the adoption rate of advanced cardiac bionics, a related segment, has seen a XX% increase year-on-year as these devices offer enhanced mobility and reduced reliance on external support. The development of bioartificial kidneys, combining engineered tissues with artificial components, represents a paradigm shift, promising to restore kidney function more comprehensively than current dialysis methods. The successful implantation of early-stage artificial hearts in pediatric patients, as highlighted in recent developments, underscores the expanding scope and increasing success rates of these life-saving technologies. Furthermore, the convergence of artificial intelligence (AI) and biomechanical engineering is unlocking new possibilities for personalized organ support, predicting device failure, and optimizing treatment protocols, further fueling the industry's evolution and growth.

Leading Regions, Countries, or Segments in Artificial Kidney Industry

The Artificial Kidney industry's dominance is currently shared across key geographical regions and specific technology segments, with the United States emerging as a leading powerhouse. This leadership is driven by a confluence of factors, including substantial government and private sector investment in biomedical research, a robust healthcare infrastructure, and a high prevalence of chronic diseases necessitating advanced medical interventions. The U.S. market for artificial organs and bionics is projected to reach $XX Billion by 2033, underscoring its significant role.

Within the segments, the Artificial Organ category, specifically the Artificial Kidney sub-segment, is poised for exponential growth. This surge is attributed to the ongoing breakthroughs in bioartificial kidney development, as exemplified by the Kidney Innovation Accelerator (KidneyX) initiative. The focus on creating a fully functional bioartificial kidney signifies a revolutionary shift, aiming to address the unmet needs of millions suffering from kidney failure.

Key drivers for U.S. dominance include:

- Investment Trends: Significant venture capital and governmental funding are channeled into research institutions and companies developing next-generation artificial organs and bionic technologies. This investment landscape fosters innovation and accelerates product development timelines.

- Regulatory Support: While stringent, the U.S. Food and Drug Administration (FDA) has a well-established pathway for approving innovative medical devices, encouraging companies to bring their advanced solutions to market.

- Patient Demographics: The high incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD) in the U.S. creates a substantial patient pool demanding effective treatment alternatives to dialysis.

- Technological Prowess: American companies are at the forefront of developing sophisticated materials, implantable devices, and bioengineering techniques crucial for artificial kidney and other artificial organ advancements.

The Bionics segment, particularly Cardiac Bionics, also plays a crucial role, with companies like Medtronic Inc. and Abiomed Inc. leading in the development of Ventricular Assist Devices (VADs) and other cardiac support systems. These technologies are vital for patients with advanced heart failure, often serving as a bridge to transplantation or as destination therapy. The successful implantation of a total artificial heart in a child in Canada, with training acquired in the U.S., further highlights the interconnectedness of innovation and the global reach of these life-saving technologies, albeit with the U.S. often serving as a hub for advanced training and development.

Canada and Mexico, while currently having smaller market shares compared to the U.S., are demonstrating promising growth. Canada's commitment to healthcare innovation, as evidenced by the pioneering work at SickKids, positions it as a significant player in pediatric artificial organ development. Mexico's market is growing due to an increasing adoption of medical technologies and a rising prevalence of lifestyle-related diseases.

Looking ahead, the convergence of artificial intelligence, advanced materials, and regenerative medicine within the Artificial Kidney and Artificial Heart segments are expected to drive significant market expansion across all three regions. The successful development of a fully functional bioartificial kidney could fundamentally alter the treatment landscape for kidney disease, making this segment a critical focus for future growth and investment.

Artificial Kidney Industry Product Innovations

Product innovation within the Artificial Kidney industry is rapidly advancing, focusing on enhancing functionality, biocompatibility, and patient quality of life. Key innovations include the development of implantable, wearable, and bio-integrated artificial kidneys designed to mimic natural kidney functions, reducing the need for frequent dialysis treatments. Companies are investing heavily in miniaturization of components, utilizing advanced materials like polymers and biocompatible ceramics, and incorporating smart technologies for real-time monitoring and personalized treatment. For artificial hearts, advancements are centered on more durable, efficient, and less invasive VADs (Ventricular Assist Devices) and total artificial hearts, offering longer patient survival rates and improved mobility. The unique selling proposition for these innovations lies in their ability to restore or augment organ function, thereby significantly improving patient outcomes and reducing the burden of chronic diseases. Technological advancements are also exploring the use of stem cells and tissue engineering to create bioartificial organs, offering the potential for full organ replacement with reduced rejection risks.

Propelling Factors for Artificial Kidney Industry Growth

The growth of the Artificial Kidney industry is propelled by a powerful combination of technological, economic, and regulatory influences.

- Technological Advancements: Breakthroughs in biomaterials, nanotechnology, and bioengineering are enabling the creation of more sophisticated and effective artificial organs and bionic devices. The ongoing development of the bioartificial kidney is a prime example, promising to revolutionize kidney disease treatment.

- Increasing Prevalence of Chronic Diseases: The global rise in conditions like chronic kidney disease (CKD), end-stage renal disease (ESRD), and cardiovascular diseases directly fuels the demand for artificial organ solutions and life-support technologies.

- Growing Healthcare Expenditure: Increased government and private sector spending on healthcare globally, particularly in developed nations, translates to greater investment in advanced medical technologies and procedures.

- Favorable Regulatory Initiatives: Government bodies and health organizations are actively supporting innovation through prize competitions and funding opportunities, such as the KidneyX initiative, accelerating the development and adoption of novel artificial kidney technologies.

Obstacles in the Artificial Kidney Industry Market

Despite its promising trajectory, the Artificial Kidney industry faces significant obstacles that could impede its growth.

- High Development and Manufacturing Costs: The intricate nature of artificial organs and bionic devices leads to substantial research, development, and manufacturing costs, making these technologies expensive and potentially inaccessible to a broader patient population.

- Complex Regulatory Pathways: Navigating the stringent and often lengthy approval processes by regulatory bodies like the FDA and EMA can be a significant hurdle, delaying market entry for innovative products.

- Biocompatibility and Long-Term Performance Challenges: Ensuring long-term biocompatibility, preventing device rejection, and maintaining optimal performance over extended periods remain critical technical challenges that require continuous research and development.

- Limited Awareness and Adoption: In certain regions, awareness of advanced artificial organ technologies is still low, leading to slower adoption rates among healthcare providers and patients. The estimated impact of these barriers could lead to a XX% slower market penetration in some regions without targeted interventions.

Future Opportunities in Artificial Kidney Industry

The Artificial Kidney industry is ripe with future opportunities, driven by emerging technologies and evolving market needs.

- Advancements in Bioartificial Kidneys: The continued development and eventual commercialization of fully functional bioartificial kidneys represent a transformative opportunity, offering a potential cure for kidney failure.

- Personalized Organ Support Systems: The integration of AI and machine learning can lead to the development of personalized artificial organs and bionic devices that adapt to individual patient needs, improving efficacy and reducing complications.

- Expansion into Emerging Markets: As healthcare infrastructure and spending grow in emerging economies, there is a significant opportunity to introduce advanced artificial organ technologies to previously underserved populations.

- Regenerative Medicine Convergence: The synergy between artificial organ technology and regenerative medicine, including stem cell therapies, holds immense potential for creating more integrated and functional bio-prosthetic solutions.

Major Players in the Artificial Kidney Industry Ecosystem

- Medtronic Inc.

- Ossur

- Abiomed Inc.

- Cyberonics Inc.

- Esko Bionics

- Asahi Kasei Medical Co Ltd

- Cochlear Ltd

- Boston Scientific Corporation

- Baxter International Inc.

- Berlin Heart GmbH

Key Developments in Artificial Kidney Industry Industry

- August 2022: The United States Department of Health and Human Services (HHS) and the American Society of Nephrology (ASN) unveiled a fresh prize competition through the Kidney Innovation Accelerator (KidneyX), aiming to advance the development of a fully functional bioartificial kidney. This initiative is poised to significantly accelerate R&D in the artificial kidney segment, fostering innovation and potentially leading to groundbreaking treatments.

- July 2022: In Canada, doctors from SickKids made medical history by successfully implanting one of the first total artificial hearts in a child. This landmark achievement, following training in the United States, highlights advancements in pediatric cardiac bionics and underscores the growing capabilities in complex organ replacement surgeries, impacting the broader cardiac bionics market.

Strategic Artificial Kidney Industry Market Forecast

The strategic forecast for the Artificial Kidney industry is exceptionally positive, driven by continuous technological innovation and a growing global demand for advanced organ support and replacement solutions. The successful development of bioartificial kidneys is anticipated to be a significant market catalyst, potentially transforming the treatment paradigm for millions worldwide. Furthermore, the increasing sophistication of cardiac bionics and other artificial organ technologies will continue to expand the market, offering enhanced quality of life and improved survival rates for patients. Emerging market penetration and the convergence of AI with biomedical engineering present substantial growth opportunities. The industry is projected to witness robust growth, with key players investing heavily in research and development to overcome existing barriers and capitalize on unmet medical needs. The market is expected to reach an estimated $XX Billion by 2033, exhibiting a CAGR of XX% from 2025 to 2033.

Artificial Kidney Industry Segmentation

-

1. Type

-

1.1. Artificial Organ

- 1.1.1. Artificial Heart

- 1.1.2. Artificial Kidney

- 1.1.3. Artificial Lungs

- 1.1.4. Cochlear Implants

- 1.1.5. Other Organ Types

-

1.2. Bionics

- 1.2.1. Vision Bionics

- 1.2.2. Ear Bionics

- 1.2.3. Orthopedic Bionic

- 1.2.4. Cardiac Bionics

-

1.1. Artificial Organ

-

2. Geography

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

Artificial Kidney Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

Artificial Kidney Industry Regional Market Share

Geographic Coverage of Artificial Kidney Industry

Artificial Kidney Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Artificial Organ

- 5.1.1.1. Artificial Heart

- 5.1.1.2. Artificial Kidney

- 5.1.1.3. Artificial Lungs

- 5.1.1.4. Cochlear Implants

- 5.1.1.5. Other Organ Types

- 5.1.2. Bionics

- 5.1.2.1. Vision Bionics

- 5.1.2.2. Ear Bionics

- 5.1.2.3. Orthopedic Bionic

- 5.1.2.4. Cardiac Bionics

- 5.1.1. Artificial Organ

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United States

- 5.2.2. Canada

- 5.2.3. Mexico

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Artificial Kidney Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Artificial Organ

- 6.1.1.1. Artificial Heart

- 6.1.1.2. Artificial Kidney

- 6.1.1.3. Artificial Lungs

- 6.1.1.4. Cochlear Implants

- 6.1.1.5. Other Organ Types

- 6.1.2. Bionics

- 6.1.2.1. Vision Bionics

- 6.1.2.2. Ear Bionics

- 6.1.2.3. Orthopedic Bionic

- 6.1.2.4. Cardiac Bionics

- 6.1.1. Artificial Organ

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United States

- 6.2.2. Canada

- 6.2.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United States Artificial Kidney Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Artificial Organ

- 7.1.1.1. Artificial Heart

- 7.1.1.2. Artificial Kidney

- 7.1.1.3. Artificial Lungs

- 7.1.1.4. Cochlear Implants

- 7.1.1.5. Other Organ Types

- 7.1.2. Bionics

- 7.1.2.1. Vision Bionics

- 7.1.2.2. Ear Bionics

- 7.1.2.3. Orthopedic Bionic

- 7.1.2.4. Cardiac Bionics

- 7.1.1. Artificial Organ

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United States

- 7.2.2. Canada

- 7.2.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Canada Artificial Kidney Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Artificial Organ

- 8.1.1.1. Artificial Heart

- 8.1.1.2. Artificial Kidney

- 8.1.1.3. Artificial Lungs

- 8.1.1.4. Cochlear Implants

- 8.1.1.5. Other Organ Types

- 8.1.2. Bionics

- 8.1.2.1. Vision Bionics

- 8.1.2.2. Ear Bionics

- 8.1.2.3. Orthopedic Bionic

- 8.1.2.4. Cardiac Bionics

- 8.1.1. Artificial Organ

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United States

- 8.2.2. Canada

- 8.2.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Mexico Artificial Kidney Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Artificial Organ

- 9.1.1.1. Artificial Heart

- 9.1.1.2. Artificial Kidney

- 9.1.1.3. Artificial Lungs

- 9.1.1.4. Cochlear Implants

- 9.1.1.5. Other Organ Types

- 9.1.2. Bionics

- 9.1.2.1. Vision Bionics

- 9.1.2.2. Ear Bionics

- 9.1.2.3. Orthopedic Bionic

- 9.1.2.4. Cardiac Bionics

- 9.1.1. Artificial Organ

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United States

- 9.2.2. Canada

- 9.2.3. Mexico

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Medtronic Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Ossur

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Abiomed Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Cyberonics Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Esko Bionics

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Asahi Kasei Medical Co Ltd

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Cochlear Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Boston Scientific Corporation

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Baxter International Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 Berlin Heart GmbH

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.1 Medtronic Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global Artificial Kidney Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Artificial Kidney Industry Volume Breakdown (Piece, %) by Region 2025 & 2033

- Figure 3: United States Artificial Kidney Industry Revenue (Million), by Type 2025 & 2033

- Figure 4: United States Artificial Kidney Industry Volume (Piece), by Type 2025 & 2033

- Figure 5: United States Artificial Kidney Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: United States Artificial Kidney Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: United States Artificial Kidney Industry Revenue (Million), by Geography 2025 & 2033

- Figure 8: United States Artificial Kidney Industry Volume (Piece), by Geography 2025 & 2033

- Figure 9: United States Artificial Kidney Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 10: United States Artificial Kidney Industry Volume Share (%), by Geography 2025 & 2033

- Figure 11: United States Artificial Kidney Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: United States Artificial Kidney Industry Volume (Piece), by Country 2025 & 2033

- Figure 13: United States Artificial Kidney Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: United States Artificial Kidney Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Canada Artificial Kidney Industry Revenue (Million), by Type 2025 & 2033

- Figure 16: Canada Artificial Kidney Industry Volume (Piece), by Type 2025 & 2033

- Figure 17: Canada Artificial Kidney Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Canada Artificial Kidney Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Canada Artificial Kidney Industry Revenue (Million), by Geography 2025 & 2033

- Figure 20: Canada Artificial Kidney Industry Volume (Piece), by Geography 2025 & 2033

- Figure 21: Canada Artificial Kidney Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 22: Canada Artificial Kidney Industry Volume Share (%), by Geography 2025 & 2033

- Figure 23: Canada Artificial Kidney Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Canada Artificial Kidney Industry Volume (Piece), by Country 2025 & 2033

- Figure 25: Canada Artificial Kidney Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Canada Artificial Kidney Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Mexico Artificial Kidney Industry Revenue (Million), by Type 2025 & 2033

- Figure 28: Mexico Artificial Kidney Industry Volume (Piece), by Type 2025 & 2033

- Figure 29: Mexico Artificial Kidney Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Mexico Artificial Kidney Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Mexico Artificial Kidney Industry Revenue (Million), by Geography 2025 & 2033

- Figure 32: Mexico Artificial Kidney Industry Volume (Piece), by Geography 2025 & 2033

- Figure 33: Mexico Artificial Kidney Industry Revenue Share (%), by Geography 2025 & 2033

- Figure 34: Mexico Artificial Kidney Industry Volume Share (%), by Geography 2025 & 2033

- Figure 35: Mexico Artificial Kidney Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Mexico Artificial Kidney Industry Volume (Piece), by Country 2025 & 2033

- Figure 37: Mexico Artificial Kidney Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Mexico Artificial Kidney Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Artificial Kidney Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Artificial Kidney Industry Volume Piece Forecast, by Type 2020 & 2033

- Table 3: Global Artificial Kidney Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Global Artificial Kidney Industry Volume Piece Forecast, by Geography 2020 & 2033

- Table 5: Global Artificial Kidney Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Artificial Kidney Industry Volume Piece Forecast, by Region 2020 & 2033

- Table 7: Global Artificial Kidney Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: Global Artificial Kidney Industry Volume Piece Forecast, by Type 2020 & 2033

- Table 9: Global Artificial Kidney Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 10: Global Artificial Kidney Industry Volume Piece Forecast, by Geography 2020 & 2033

- Table 11: Global Artificial Kidney Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Artificial Kidney Industry Volume Piece Forecast, by Country 2020 & 2033

- Table 13: Global Artificial Kidney Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 14: Global Artificial Kidney Industry Volume Piece Forecast, by Type 2020 & 2033

- Table 15: Global Artificial Kidney Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Global Artificial Kidney Industry Volume Piece Forecast, by Geography 2020 & 2033

- Table 17: Global Artificial Kidney Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: Global Artificial Kidney Industry Volume Piece Forecast, by Country 2020 & 2033

- Table 19: Global Artificial Kidney Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 20: Global Artificial Kidney Industry Volume Piece Forecast, by Type 2020 & 2033

- Table 21: Global Artificial Kidney Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 22: Global Artificial Kidney Industry Volume Piece Forecast, by Geography 2020 & 2033

- Table 23: Global Artificial Kidney Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Artificial Kidney Industry Volume Piece Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Artificial Kidney Industry?

The projected CAGR is approximately 7.20%.

2. Which companies are prominent players in the Artificial Kidney Industry?

Key companies in the market include Medtronic Inc , Ossur, Abiomed Inc, Cyberonics Inc, Esko Bionics, Asahi Kasei Medical Co Ltd, Cochlear Ltd, Boston Scientific Corporation, Baxter International Inc, Berlin Heart GmbH.

3. What are the main segments of the Artificial Kidney Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Incidence of Disabilities and Organ Failures; High Incidence of Road Accidents Leading to Amputations; Technological Advancements in the Artificial Organ and Bionics.

6. What are the notable trends driving market growth?

Artificial Kidney Segment is Estimated to Witness a Healthy Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Expensive Procedures; Risk of Compatibility Issues and Malfunctions.

8. Can you provide examples of recent developments in the market?

August 2022: The United States Department of Health and Human Services (HHS) and the American Society of Nephrology (ASN) unveiled a fresh prize competition through the Kidney Innovation Accelerator (KidneyX). This competition aims to advance the development of a fully functional bioartificial kidney.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Piece.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Artificial Kidney Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Artificial Kidney Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Artificial Kidney Industry?

To stay informed about further developments, trends, and reports in the Artificial Kidney Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence