Key Insights

The Application Delivery Controllers (ADC) market is projected to reach $3.6 billion by 2024, exhibiting a Compound Annual Growth Rate (CAGR) of 7.3%. This expansion is driven by the increasing demand for enhanced application performance, scalability, and security across industries. The adoption of cloud-native architectures and microservices necessitates advanced solutions for traffic management. Furthermore, the rise of remote work and digital services amplifies the need for resilient applications, positioning ADCs as essential IT infrastructure. Technological advancements, including integrated security features like Web Application Firewalls (WAF) and Distributed Denial of Service (DDoS) protection, alongside improved load balancing and intelligent traffic management, further fuel market growth. The shift towards Software-Defined Networking (SDN) and Network Function Virtualization (NFV) also contributes to market dynamism, enabling agile application delivery.

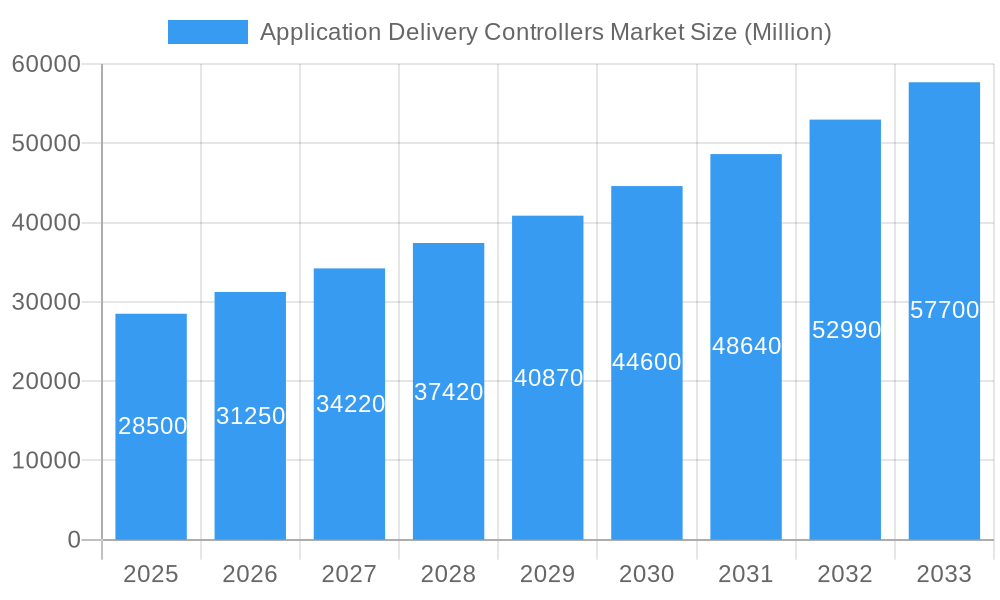

Application Delivery Controllers Market Market Size (In Billion)

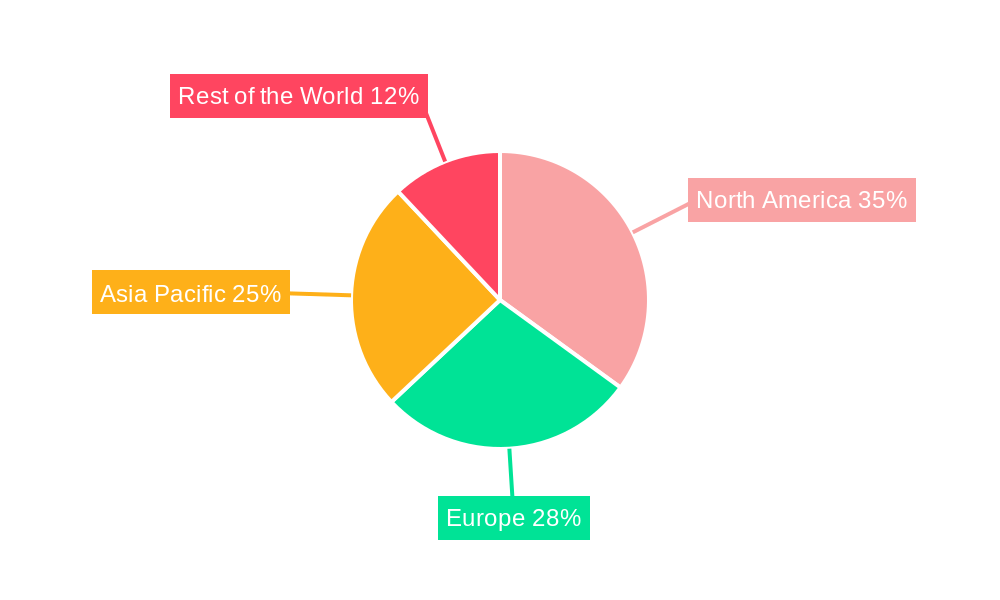

Cloud-based deployments dominate market segmentation, aligning with widespread cloud adoption. Small and Medium Enterprises (SMEs) and Large Enterprises are investing in ADCs for optimal user experiences and digital asset protection. Key end-user verticals, including BFSI, Retail, IT & Telecom, and Healthcare, are leading adoption due to stringent regulatory compliance and application criticality. North America currently leads the market, while the Asia Pacific region shows rapid growth driven by digital transformation initiatives and increasing IT expenditure. Potential restraints include integration complexity with legacy systems and a shortage of skilled professionals. However, continuous innovation in ADC capabilities and growing awareness of their strategic importance are expected to drive sustained market growth.

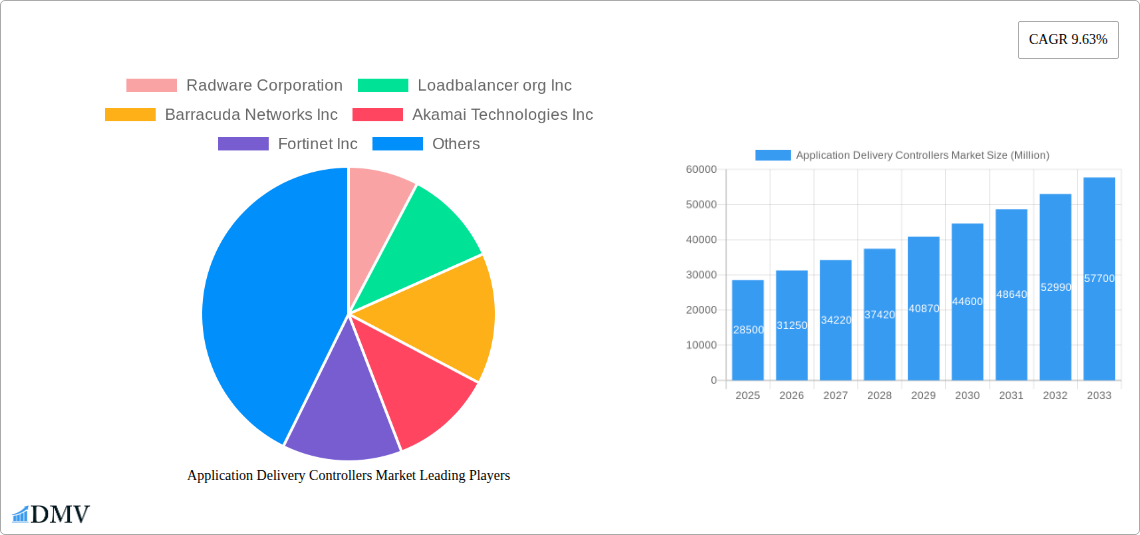

Application Delivery Controllers Market Company Market Share

Application Delivery Controllers Market: Comprehensive Analysis and Future Outlook (2019-2033)

Unlock critical insights into the dynamic Application Delivery Controllers (ADC) market, a vital segment powering resilient and high-performing digital infrastructures. This in-depth report, covering 2019–2033 with a base year of 2025 and a forecast period of 2025–2033, delivers a complete market composition, industry evolution, and strategic forecast. Gain a competitive edge by understanding key growth drivers, emerging opportunities, and the strategic moves of major players like Radware Corporation, Loadbalancer.org Inc, Barracuda Networks Inc, Akamai Technologies Inc, Fortinet Inc, F5 Networks Inc, Piolink Inc, Juniper Networks Inc, Kemp Technologies Inc, A10 Networks Inc, Array Networks Inc, Sangfor Technologies Inc, Citrix Systems Inc, and HAProxy Technologies LLC.

This report is meticulously crafted to address the needs of stakeholders seeking actionable intelligence on ADC solutions, load balancing technologies, application performance optimization, and network security appliances. Whether your focus is on cloud deployment, on-premise infrastructure, SMEs, large enterprises, or specific verticals like BFSI, Retail, IT and Telecom, and Healthcare, this analysis provides unparalleled depth and clarity.

Application Delivery Controllers Market Market Composition & Trends

The Application Delivery Controllers (ADC) market exhibits a moderately consolidated structure, characterized by continuous innovation and strategic partnerships. Key trends include the increasing demand for advanced security features, enhanced application performance, and seamless integration with cloud-native environments. Market share distribution sees dominant players like F5 Networks and Citrix Systems leading, but emerging vendors are carving out significant niches. The ADC market size is projected to reach XX Billion USD by 2025. M&A activities are a constant feature, with deal values averaging in the hundreds of Millions USD, aimed at consolidating market presence and acquiring cutting-edge technologies. For instance, the acquisition of XX by XX for XX Million USD in 2023 highlights this trend.

- Innovation Catalysts: Rise of microservices architecture, demand for containerized application support, increasing IoT deployments, and the growing need for robust DDoS protection.

- Regulatory Landscapes: Evolving data privacy regulations (e.g., GDPR, CCPA) are driving demand for ADCs with enhanced security and compliance features.

- Substitute Products: While other network devices offer some load balancing functionalities, dedicated ADCs provide superior performance, scalability, and advanced application-aware features.

- End-user Profiles: A diverse range of businesses, from agile startups to large enterprises across all sectors, rely on ADCs for mission-critical applications.

- M&A Activities: Focus on acquiring companies with expertise in cloud-native ADCs, AI-driven traffic management, and advanced security capabilities.

Application Delivery Controllers Market Industry Evolution

The Application Delivery Controllers (ADC) market has undergone a significant transformation over the historical period of 2019–2024, driven by the exponential growth of digital services and the increasing complexity of application architectures. Initially focused on basic load balancing and high availability, ADCs have evolved into sophisticated platforms that offer comprehensive application delivery, security, and optimization. The shift towards cloud computing has been a pivotal factor, leading to the widespread adoption of cloud-based ADC solutions and hybrid deployments. This evolution has been fueled by a constant stream of technological advancements, including the integration of machine learning and AI for intelligent traffic management, predictive analytics, and automated security threat detection. The demand for higher application performance, lower latency, and enhanced user experience has also propelled the market forward.

The market growth trajectory has been consistently upward, with an estimated Compound Annual Growth Rate (CAGR) of XX% between 2019 and 2024. Key adoption metrics indicate a strong preference for ADC solutions that can scale dynamically with fluctuating traffic demands, particularly evident in the IT and Telecom and BFSI sectors. The proliferation of web applications, mobile apps, and the Internet of Things (IoT) has created an ever-increasing need for reliable and secure application delivery. Furthermore, the rise of edge computing and the decentralization of IT infrastructure are influencing ADC design and deployment strategies. Companies are increasingly looking for ADCs that can provide consistent security policies and performance across distributed environments. The industry has witnessed a move from hardware-centric solutions towards more software-defined and virtualized ADC offerings, providing greater flexibility and cost-effectiveness. This adaptability is crucial as businesses navigate the complexities of digital transformation and strive to deliver seamless customer experiences in an increasingly competitive landscape. The impact of events like the global pandemic has further accelerated the adoption of robust application delivery infrastructure, as businesses rapidly transitioned to remote work and relied heavily on online services. The focus on business continuity and disaster recovery has cemented the role of ADCs as indispensable components of modern IT architecture.

Leading Regions, Countries, or Segments in Application Delivery Controllers Market

The Application Delivery Controllers (ADC) market is experiencing robust growth across various segments, with distinct regional and deployment preferences shaping its landscape. In terms of deployment, the Cloud segment is emerging as a dominant force, driven by the unparalleled scalability, flexibility, and cost-efficiency it offers. Businesses are increasingly migrating their applications and workloads to public, private, and hybrid cloud environments, necessitating ADCs that can seamlessly integrate and manage traffic within these dynamic ecosystems. The on-premise segment, while still significant, is witnessing a gradual shift towards hybrid models as organizations seek to leverage the best of both worlds.

When considering enterprise size, Large Enterprises represent a substantial market share due to their extensive application portfolios, higher traffic volumes, and greater investment capacity in sophisticated ADC solutions. These enterprises require ADCs capable of handling complex traffic patterns, advanced security protocols, and high availability requirements for their mission-critical operations. However, Small and Medium Enterprises (SMEs) are also a rapidly growing segment, increasingly adopting cloud-based ADC solutions that offer affordability and ease of management, enabling them to compete effectively in the digital space.

Across end-user verticals, the IT and Telecom sector leads the adoption of ADCs, owing to the high volume of data traffic, the need for robust network performance, and the constant innovation in digital services. The BFSI sector follows closely, driven by stringent security requirements, the need for uninterrupted service availability for financial transactions, and compliance with regulatory mandates. The Retail sector is also a significant consumer, with e-commerce growth fueling the demand for performant and secure online shopping experiences. Healthcare is another critical vertical, where ADCs ensure the availability and security of patient data and critical healthcare applications.

- Dominant Deployment: Cloud Deployment is a key growth driver, offering elastic scalability and cost savings. Key factors include the proliferation of SaaS applications, the rise of multi-cloud strategies, and the increasing adoption of containerized workloads.

- Enterprise Size Dominance: Large Enterprises command the largest market share due to their complex infrastructure and critical application needs. Investment trends show significant spending on advanced ADC features like application firewalling and bot management.

- Vertical Leaders:

- IT and Telecom: High demand for bandwidth management, network optimization, and advanced security features. Regulatory support for digital infrastructure development.

- BFSI: Critical need for high availability, low latency, and robust security to protect sensitive financial data and comply with stringent regulations.

- Retail: Focus on seamless e-commerce experiences, efficient traffic management for peak seasons, and enhanced customer engagement.

- Key Drivers for Dominance:

- Technological Advancements: Integration of AI/ML for predictive analytics and automated traffic management.

- Security Imperatives: Growing cyber threats are driving demand for integrated security features within ADCs.

- Digital Transformation Initiatives: Businesses across all sectors are investing in digital capabilities, requiring robust application delivery infrastructure.

Application Delivery Controllers Market Product Innovations

The Application Delivery Controllers (ADC) market is continuously shaped by groundbreaking product innovations that enhance application performance, security, and scalability. Recent advancements include the integration of Artificial Intelligence and Machine Learning for predictive traffic analysis and automated anomaly detection, leading to proactive issue resolution. Software-defined ADCs (SD-ADCs) are gaining traction, offering greater flexibility and agility for cloud-native environments and containerized applications. Furthermore, ADCs are evolving to provide comprehensive web application firewall (WAF) capabilities, advanced bot mitigation, and integrated DDoS protection, addressing the escalating cyber threat landscape. Enhanced SSL/TLS offloading, granular traffic shaping, and intelligent caching mechanisms are also key innovations that significantly improve application responsiveness and user experience.

Propelling Factors for Application Delivery Controllers Market Growth

The Application Delivery Controllers (ADC) market is experiencing robust growth driven by several key factors. The escalating demand for high-performance, always-on applications across all industries is a primary catalyst. This is further amplified by the global shift towards digital transformation, requiring businesses to deliver seamless and secure online experiences to customers and employees. The proliferation of cloud computing and hybrid cloud deployments necessitates sophisticated ADC solutions for efficient traffic management and seamless integration. Additionally, the increasing sophistication of cyber threats, including DDoS attacks and application-layer vulnerabilities, is driving the adoption of ADCs with advanced security features. The growing adoption of microservices and containerized applications also fuels the demand for scalable and agile ADC solutions.

Obstacles in the Application Delivery Controllers Market Market

Despite the significant growth, the Application Delivery Controllers (ADC) market faces several obstacles. The complexity of integrating ADCs with existing legacy infrastructure can be a challenge for some organizations, leading to extended deployment times and increased costs. The high cost of advanced ADC solutions can also be a barrier for smaller enterprises, limiting their access to cutting-edge capabilities. Furthermore, the rapid pace of technological change requires continuous investment in training and skill development for IT staff to effectively manage and leverage ADC functionalities. Supply chain disruptions, though less prevalent now, can still impact the availability of hardware-based ADC appliances. Finally, the increasing competition from cloud-native load balancing services offered by major cloud providers poses a competitive challenge to traditional ADC vendors.

Future Opportunities in Application Delivery Controllers Market

The Application Delivery Controllers (ADC) market is ripe with future opportunities. The burgeoning adoption of edge computing presents a significant avenue for ADCs to optimize application delivery closer to the end-user, reducing latency and improving performance. The growing demand for AI-driven insights and automated application performance management will drive innovation in intelligent ADC capabilities. The continued expansion of IoT devices will create new traffic management challenges and opportunities for ADCs to secure and optimize data flow. Furthermore, the increasing focus on cybersecurity and data privacy regulations will fuel the demand for ADCs with advanced security features and compliance capabilities. The evolution of 5G networks will also unlock new possibilities for high-performance, low-latency application delivery, where ADCs will play a crucial role.

Major Players in the Application Delivery Controllers Market Ecosystem

- Radware Corporation

- Loadbalancer.org Inc

- Barracuda Networks Inc

- Akamai Technologies Inc

- Fortinet Inc

- F5 Networks Inc

- Piolink Inc

- Juniper Networks Inc

- Kemp Technologies Inc

- A10 Networks Inc

- Array Networks Inc

- Sangfor Technologies Inc

- Citrix Systems Inc

- HAProxy Technologies LLC

Key Developments in Application Delivery Controllers Market Industry

- June 2023: Fortinet, a global cybersecurity leader, announced that 11 new managed security service providers (MSSPs) have adopted Fortinet Secure SD-WAN to enhance business outcomes and customer experiences. These MSSPs include Kyndryl; 11:11 Systems; Claro Empresas; Globe Business; InfiniVAN, Inc.; KT Corporation; Neurosoft S.A.; Sify Technologies; SPTel; solutions by STC; and Tata Teleservices, leveraging Fortinet Secure SD-WAN for differentiated connectivity services.

- February 2023: Juniper Networks, a leader in AI-driven networks, announced plans to expand its collaboration with IBM to integrate IBM's network automation capabilities with Juniper's Radio Access Network (RAN) optimization and Open Radio Access Network (O-RAN) technology. This collaboration aims to deliver a unified RAN management platform using intelligent automation to enable Communications Service Providers (CSPs) to monetize, optimize, and scale their next-generation network investments and improve mobile user experiences.

Strategic Application Delivery Controllers Market Market Forecast

The Application Delivery Controllers (ADC) market is poised for substantial growth in the coming years, driven by the relentless digital transformation across industries. The increasing adoption of cloud-native architectures and the proliferation of microservices will necessitate more agile and scalable ADC solutions. The growing threat landscape will continue to propel demand for ADCs with integrated, advanced security features, including WAF, DDoS protection, and bot mitigation. Furthermore, the expansion of edge computing and the rollout of 5G networks will create new opportunities for optimizing application delivery at the network edge. AI and machine learning integration will be a key differentiator, enabling predictive traffic management and automated issue resolution. Businesses will increasingly rely on ADCs to ensure application availability, performance, and security, making them an indispensable component of modern IT infrastructure.

Application Delivery Controllers Market Segmentation

-

1. Deployment

- 1.1. Cloud

- 1.2. On-premise

-

2. Enterprise Size

- 2.1. Small and Medium Enterprises (SMEs)

- 2.2. Large Enterprises

-

3. End-user Vertical

- 3.1. BFSI

- 3.2. Retail

- 3.3. IT and Telecom

- 3.4. Healthcare

- 3.5. Other End-user Verticals

Application Delivery Controllers Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Application Delivery Controllers Market Regional Market Share

Geographic Coverage of Application Delivery Controllers Market

Application Delivery Controllers Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Reliable Application Performance; Increasing Cyberattacks

- 3.3. Market Restrains

- 3.3.1. Increasing Network Complexity; Management Challenges and Higher Costs of ADCs

- 3.4. Market Trends

- 3.4.1. BFSI By End-user Vertical Segment is Expected to Hold Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Application Delivery Controllers Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. Cloud

- 5.1.2. On-premise

- 5.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.2.1. Small and Medium Enterprises (SMEs)

- 5.2.2. Large Enterprises

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. BFSI

- 5.3.2. Retail

- 5.3.3. IT and Telecom

- 5.3.4. Healthcare

- 5.3.5. Other End-user Verticals

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. North America Application Delivery Controllers Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 6.1.1. Cloud

- 6.1.2. On-premise

- 6.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 6.2.1. Small and Medium Enterprises (SMEs)

- 6.2.2. Large Enterprises

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. BFSI

- 6.3.2. Retail

- 6.3.3. IT and Telecom

- 6.3.4. Healthcare

- 6.3.5. Other End-user Verticals

- 6.1. Market Analysis, Insights and Forecast - by Deployment

- 7. Europe Application Delivery Controllers Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 7.1.1. Cloud

- 7.1.2. On-premise

- 7.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 7.2.1. Small and Medium Enterprises (SMEs)

- 7.2.2. Large Enterprises

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. BFSI

- 7.3.2. Retail

- 7.3.3. IT and Telecom

- 7.3.4. Healthcare

- 7.3.5. Other End-user Verticals

- 7.1. Market Analysis, Insights and Forecast - by Deployment

- 8. Asia Pacific Application Delivery Controllers Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 8.1.1. Cloud

- 8.1.2. On-premise

- 8.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 8.2.1. Small and Medium Enterprises (SMEs)

- 8.2.2. Large Enterprises

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. BFSI

- 8.3.2. Retail

- 8.3.3. IT and Telecom

- 8.3.4. Healthcare

- 8.3.5. Other End-user Verticals

- 8.1. Market Analysis, Insights and Forecast - by Deployment

- 9. Rest of the World Application Delivery Controllers Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 9.1.1. Cloud

- 9.1.2. On-premise

- 9.2. Market Analysis, Insights and Forecast - by Enterprise Size

- 9.2.1. Small and Medium Enterprises (SMEs)

- 9.2.2. Large Enterprises

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. BFSI

- 9.3.2. Retail

- 9.3.3. IT and Telecom

- 9.3.4. Healthcare

- 9.3.5. Other End-user Verticals

- 9.1. Market Analysis, Insights and Forecast - by Deployment

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Radware Corporation

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Loadbalancer org Inc

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Barracuda Networks Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Akamai Technologies Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Fortinet Inc

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 F5 Networks Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Piolink Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Juniper Networks Inc

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Kemp Technologies Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 A10 Networks Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Array Networks Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Sangfor Technologies Inc

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 Citrix Systems Inc

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 HAProxy Technologies LLC

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.1 Radware Corporation

List of Figures

- Figure 1: Global Application Delivery Controllers Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Application Delivery Controllers Market Revenue (billion), by Deployment 2025 & 2033

- Figure 3: North America Application Delivery Controllers Market Revenue Share (%), by Deployment 2025 & 2033

- Figure 4: North America Application Delivery Controllers Market Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 5: North America Application Delivery Controllers Market Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 6: North America Application Delivery Controllers Market Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 7: North America Application Delivery Controllers Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Application Delivery Controllers Market Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Application Delivery Controllers Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Application Delivery Controllers Market Revenue (billion), by Deployment 2025 & 2033

- Figure 11: Europe Application Delivery Controllers Market Revenue Share (%), by Deployment 2025 & 2033

- Figure 12: Europe Application Delivery Controllers Market Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 13: Europe Application Delivery Controllers Market Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 14: Europe Application Delivery Controllers Market Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 15: Europe Application Delivery Controllers Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Application Delivery Controllers Market Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Application Delivery Controllers Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Application Delivery Controllers Market Revenue (billion), by Deployment 2025 & 2033

- Figure 19: Asia Pacific Application Delivery Controllers Market Revenue Share (%), by Deployment 2025 & 2033

- Figure 20: Asia Pacific Application Delivery Controllers Market Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 21: Asia Pacific Application Delivery Controllers Market Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 22: Asia Pacific Application Delivery Controllers Market Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 23: Asia Pacific Application Delivery Controllers Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Pacific Application Delivery Controllers Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Application Delivery Controllers Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Application Delivery Controllers Market Revenue (billion), by Deployment 2025 & 2033

- Figure 27: Rest of the World Application Delivery Controllers Market Revenue Share (%), by Deployment 2025 & 2033

- Figure 28: Rest of the World Application Delivery Controllers Market Revenue (billion), by Enterprise Size 2025 & 2033

- Figure 29: Rest of the World Application Delivery Controllers Market Revenue Share (%), by Enterprise Size 2025 & 2033

- Figure 30: Rest of the World Application Delivery Controllers Market Revenue (billion), by End-user Vertical 2025 & 2033

- Figure 31: Rest of the World Application Delivery Controllers Market Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: Rest of the World Application Delivery Controllers Market Revenue (billion), by Country 2025 & 2033

- Figure 33: Rest of the World Application Delivery Controllers Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Application Delivery Controllers Market Revenue billion Forecast, by Deployment 2020 & 2033

- Table 2: Global Application Delivery Controllers Market Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 3: Global Application Delivery Controllers Market Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Application Delivery Controllers Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Application Delivery Controllers Market Revenue billion Forecast, by Deployment 2020 & 2033

- Table 6: Global Application Delivery Controllers Market Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 7: Global Application Delivery Controllers Market Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Application Delivery Controllers Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Application Delivery Controllers Market Revenue billion Forecast, by Deployment 2020 & 2033

- Table 10: Global Application Delivery Controllers Market Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 11: Global Application Delivery Controllers Market Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Application Delivery Controllers Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Application Delivery Controllers Market Revenue billion Forecast, by Deployment 2020 & 2033

- Table 14: Global Application Delivery Controllers Market Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 15: Global Application Delivery Controllers Market Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 16: Global Application Delivery Controllers Market Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Global Application Delivery Controllers Market Revenue billion Forecast, by Deployment 2020 & 2033

- Table 18: Global Application Delivery Controllers Market Revenue billion Forecast, by Enterprise Size 2020 & 2033

- Table 19: Global Application Delivery Controllers Market Revenue billion Forecast, by End-user Vertical 2020 & 2033

- Table 20: Global Application Delivery Controllers Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Application Delivery Controllers Market?

The projected CAGR is approximately 7.3%.

2. Which companies are prominent players in the Application Delivery Controllers Market?

Key companies in the market include Radware Corporation, Loadbalancer org Inc, Barracuda Networks Inc, Akamai Technologies Inc, Fortinet Inc, F5 Networks Inc, Piolink Inc, Juniper Networks Inc, Kemp Technologies Inc, A10 Networks Inc, Array Networks Inc, Sangfor Technologies Inc, Citrix Systems Inc, HAProxy Technologies LLC.

3. What are the main segments of the Application Delivery Controllers Market?

The market segments include Deployment, Enterprise Size, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Reliable Application Performance; Increasing Cyberattacks.

6. What are the notable trends driving market growth?

BFSI By End-user Vertical Segment is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

Increasing Network Complexity; Management Challenges and Higher Costs of ADCs.

8. Can you provide examples of recent developments in the market?

June 2023: Fortinet, one of the global cybersecurity leaders driving the convergence of networking and security, announced that 11 new managed security service providers (MSSPs) have adopted Fortinet Secure SD-WAN to assist business outcomes and customer experiences. Kyndryl; 11:11 Systems; Claro Empresas; Globe Business; InfiniVAN, Inc.; KT Corporation; Neurosoft S.A.; Sify Technologies; SPTel; solutions by STC; and Tata Teleservices join a growing list of service providers across the globe utilizing Fortinet Secure SD-WAN as the foundation for new and differentiated connectivity services without compromising on security.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Application Delivery Controllers Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Application Delivery Controllers Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Application Delivery Controllers Market?

To stay informed about further developments, trends, and reports in the Application Delivery Controllers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence