Key Insights

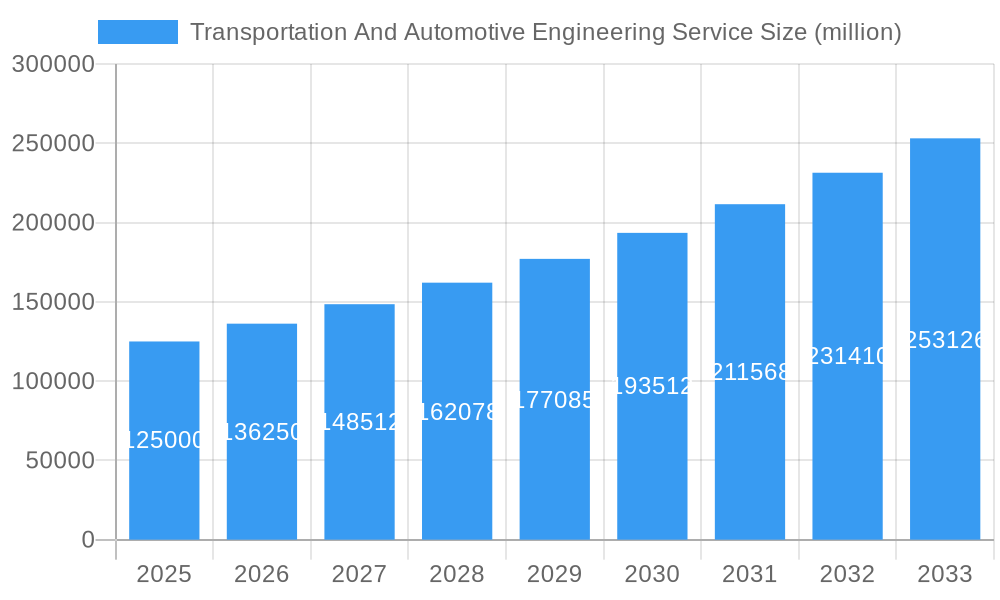

The Transportation and Automotive Engineering Service market is poised for significant expansion, projected to reach an estimated market size of approximately $125 billion in 2025. This growth is fueled by an anticipated Compound Annual Growth Rate (CAGR) of around 9% during the forecast period of 2025-2033, indicating robust and sustained development. The primary drivers behind this surge are the accelerating adoption of electric vehicles (EVs), the increasing complexity of automotive electronics and software, and the growing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies. Furthermore, the integration of connectivity services, the constant need for powertrain and exhaust system optimization for regulatory compliance and efficiency, and the ongoing digital transformation within the automotive industry are all contributing to this upward trajectory. The market is segmented across various applications, including passenger cars and commercial vehicles, and further categorized by types of services such as electrical and body controls, chassis engineering, connectivity services, powertrain and exhaust solutions, simulation, and others.

Transportation And Automotive Engineering Service Market Size (In Billion)

This dynamic market landscape is characterized by several key trends, including the pervasive influence of Industry 4.0 in automotive manufacturing, the rise of software-defined vehicles, and the critical need for cybersecurity solutions within connected automotive ecosystems. Moreover, the focus on sustainable mobility and the development of intelligent transportation systems are creating new avenues for growth and innovation. However, the market also faces certain restraints, such as the high cost of advanced technologies, the evolving regulatory landscape that can create compliance challenges, and the ongoing global semiconductor shortage, which can impact production timelines and the availability of critical components. Companies like Capgemini, Tech Mahindra, HCLTech, HARMAN International, AVL, and FEV are at the forefront, offering a wide array of specialized engineering services to cater to the diverse needs of this rapidly evolving sector. Geographically, North America and Europe are expected to maintain their strong market presence, driven by significant investments in automotive R&D and the adoption of new technologies, while Asia Pacific, particularly China and India, is anticipated to witness the fastest growth due to its expanding automotive production base and increasing consumer demand for advanced features.

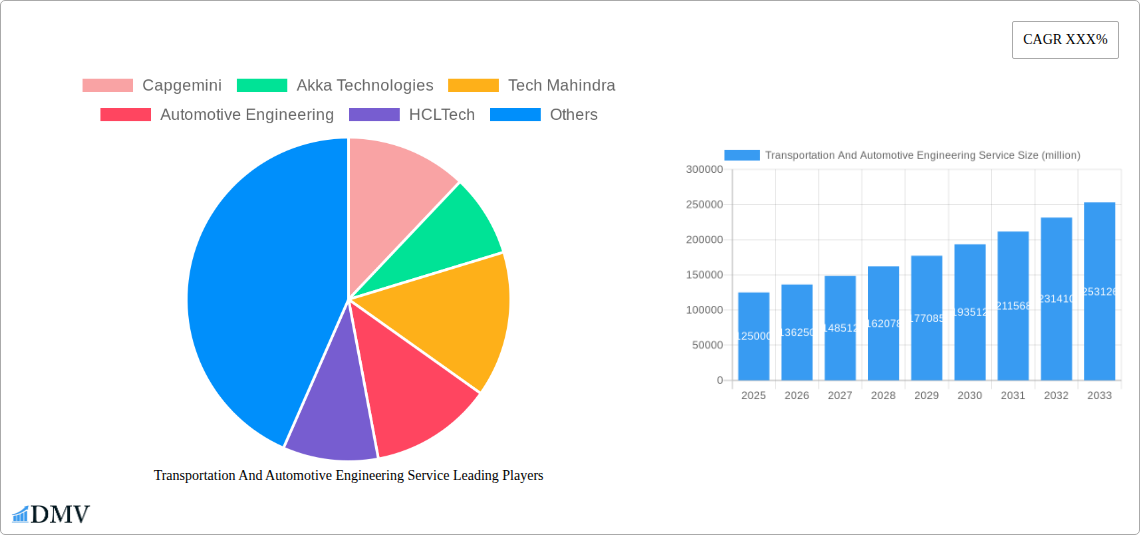

Transportation And Automotive Engineering Service Company Market Share

Transportation and Automotive Engineering Service: Comprehensive Market Analysis and Strategic Forecast (2019–2033)

This in-depth report, "Transportation and Automotive Engineering Service," provides a meticulously researched analysis of the global automotive engineering services market. Covering the study period from 2019 to 2033, with a base year of 2025 and a detailed forecast for 2025–2033, this report equips stakeholders with actionable intelligence to navigate the evolving landscape of automotive design, development, and manufacturing. We delve into critical market segments, technological advancements, regulatory shifts, and the competitive ecosystem, offering a panoramic view of this dynamic industry.

This report is essential for automotive manufacturers, Tier 1 suppliers, engineering service providers, technology developers, investors, and policymakers seeking to understand market trends, identify growth opportunities, and mitigate potential risks within the automotive engineering services sector. With a focus on passenger cars and commercial vehicles, and dissecting key service types including Electrical and Body Controls, Chassis, Connectivity Services, Powertrain and Exhaust, and Simulation, this analysis is comprehensive.

Transportation And Automotive Engineering Service Market Composition & Trends

The global transportation and automotive engineering service market exhibits a moderate to high level of concentration, driven by a select group of major players and a growing number of specialized engineering service providers. Innovation catalysts are predominantly found in the rapid advancements in electric vehicle (EV) technology, autonomous driving systems, and connected car functionalities, which necessitate complex engineering solutions. Regulatory landscapes, particularly concerning emissions standards and safety mandates, continue to shape development priorities. Substitute products are emerging in the form of in-house engineering capabilities by large OEMs and the increasing adoption of software-defined vehicles, potentially reducing reliance on external engineering services for certain aspects. End-user profiles are diverse, ranging from established automotive giants to agile EV startups, all seeking specialized expertise in areas such as automotive software development, ADAS engineering, and vehicle electrification. Mergers and acquisitions (M&A) activity is a significant trend, with deal values in the hundreds of millions of dollars as companies aim to consolidate expertise, expand service portfolios, and gain market share. For instance, acquisitions in the domain of AI-powered simulation and advanced driver-assistance systems (ADAS) are common.

- Market Share Distribution: Dominated by key players like Capgemini, Akka Technologies, and Tech Mahindra, with a substantial portion held by other specialized firms.

- M&A Deal Values: Averaging in the range of $100 million to $500 million, indicating strategic consolidation and talent acquisition.

- Key Innovation Catalysts: EV integration, ADAS development, cybersecurity for connected vehicles, and lightweight materials.

- Regulatory Impact: Stringent emissions targets and evolving safety standards driving demand for compliant engineering solutions.

Transportation And Automotive Engineering Service Industry Evolution

The transportation and automotive engineering service industry has undergone a dramatic transformation over the historical period (2019–2024) and is poised for significant expansion throughout the forecast period (2025–2033). The industry's growth trajectory has been significantly influenced by the accelerating adoption of electric vehicles (EVs), the increasing sophistication of autonomous driving technologies, and the pervasive integration of connectivity solutions within vehicles. In the historical period, the market witnessed a steady demand for traditional engineering services related to internal combustion engines and chassis development. However, the latter part of this period saw a pronounced shift towards electrification, with a surge in demand for battery management systems, electric powertrain design, and EV charging infrastructure integration.

Technological advancements have been a primary engine of this evolution. The widespread adoption of advanced simulation tools, including computational fluid dynamics (CFD) and finite element analysis (FEA), has drastically reduced development cycles and prototyping costs. Furthermore, the burgeoning field of artificial intelligence (AI) and machine learning (ML) is revolutionizing vehicle development, particularly in areas like predictive maintenance, driver monitoring systems, and the optimization of autonomous driving algorithms. The shift towards software-defined vehicles has also elevated the importance of automotive software engineering and embedded systems development, transforming traditional hardware-centric engineering services.

Consumer demands have also played a crucial role. Consumers are increasingly prioritizing safety, fuel efficiency, in-car infotainment, and seamless connectivity. This has translated into higher demand for engineering services related to ADAS features, infotainment system integration, and over-the-air (OTA) software updates. The rise of shared mobility and ride-sharing platforms has further influenced vehicle design, emphasizing durability, passenger comfort, and sophisticated fleet management capabilities, all of which rely on advanced engineering support.

The base year of 2025 marks a pivotal point where the industry has largely embraced the foundational shifts towards electrification and digitalization. Looking ahead to the forecast period (2025–2033), we anticipate continued high growth rates, with a projected Compound Annual Growth Rate (CAGR) of approximately 7% to 9%. This sustained growth will be fueled by the maturation of EV technology, the increasing deployment of Level 3 and Level 4 autonomous driving systems, and the widespread adoption of 5G connectivity for enhanced vehicle-to-everything (V2X) communication. The market for automotive cybersecurity services is also expected to skyrocket as connected vehicles become more prevalent and vulnerable to cyber threats. Furthermore, the increasing complexity of vehicle architectures, with a greater reliance on centralized computing platforms and sophisticated sensor suites, will drive demand for highly specialized engineering expertise in areas such as sensor fusion, AI model deployment, and integrated system validation. Companies like HCLTech, HARMAN International, and RICARDO are well-positioned to capitalize on these evolving demands.

Leading Regions, Countries, or Segments in Transportation And Automotive Engineering Service

The Passenger Cars segment continues to be the dominant force within the transportation and automotive engineering service market, accounting for an estimated 65% to 70% of the global market share. This dominance is driven by several converging factors, including persistent consumer demand, ongoing innovation in passenger vehicle technology, and substantial investment trends. Within the application segment, Electrical and Body Controls represents a particularly strong area of growth, fueled by the rapid expansion of EV technology and the increasing complexity of in-car electronic systems. This segment, along with Connectivity Services, is projected to witness the highest CAGRs due to the automotive industry's relentless push towards smarter, more connected, and software-defined vehicles.

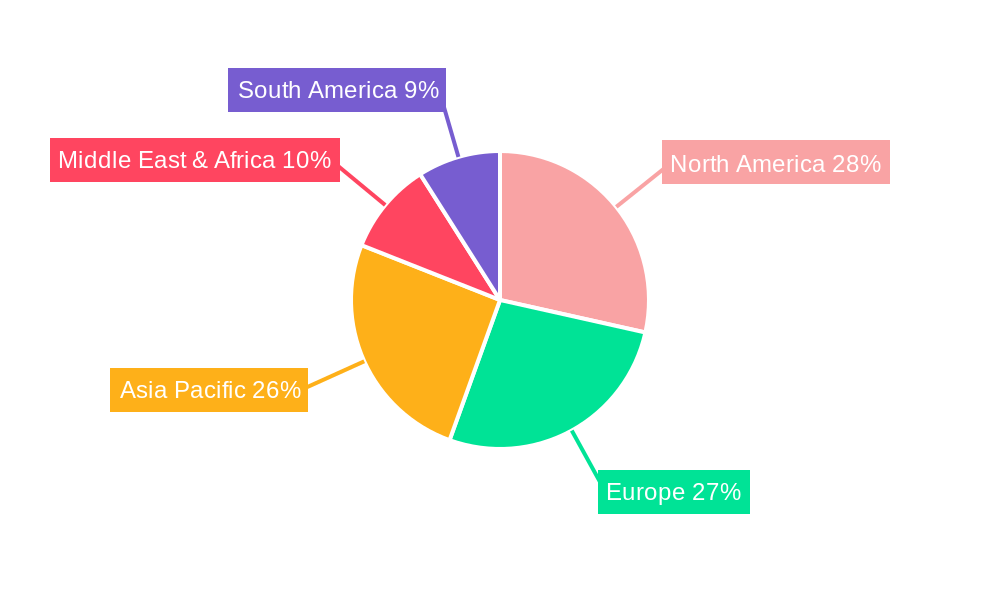

Geographically, North America and Europe have historically led the market, and this trend is expected to persist through the forecast period. These regions benefit from established automotive manufacturing bases, strong OEM presence, and a proactive regulatory environment that encourages technological adoption. For instance, stringent emissions regulations in Europe and supportive EV incentives in North America act as significant drivers for engineering service demand in areas like Powertrain and Exhaust optimization for emissions compliance and battery technology development.

The Asia-Pacific region is emerging as a significant growth powerhouse, driven by the massive automotive markets in China, India, and South Korea, coupled with substantial government investments in advanced manufacturing and R&D. The sheer volume of vehicle production in this region, coupled with the rapid adoption of new technologies, makes it a critical market for engineering services.

Key drivers for the dominance of Passenger Cars include:

- Technological Advancements: Continuous innovation in areas like advanced driver-assistance systems (ADAS), infotainment, and powertrain efficiency.

- Consumer Demand: Growing preference for feature-rich, safe, and eco-friendly vehicles.

- Electrification Push: Significant investments by OEMs and governments in EV development and deployment.

- Regulatory Support: Favorable policies and mandates promoting cleaner vehicles and advanced safety features.

The Electrical and Body Controls segment is experiencing exponential growth due to:

- EV Integration: The critical need for sophisticated battery management systems, motor controllers, and onboard charging solutions.

- Smart Cabin Features: Demand for advanced user interfaces, ambient lighting, and personalized in-car experiences.

- ADAS Hardware: Increasing integration of sensors, cameras, and ECUs for autonomous driving functionalities.

Connectivity Services are also a major growth driver, propelled by:

- V2X Communication: Development and implementation of vehicle-to-everything communication for enhanced safety and traffic management.

- Infotainment and Telematics: Demand for seamless integration of navigation, streaming services, and remote vehicle diagnostics.

- Over-the-Air (OTA) Updates: The need for robust engineering support to enable seamless software updates for enhanced functionality and security.

Companies such as AVL, Bertrandt, ALTEN Group, and L&T Technology Services are actively engaged in these leading segments and regions, offering a wide spectrum of specialized engineering solutions. The Simulation segment, while smaller in absolute terms, is crucial as it underpins development across all other segments, enabling faster prototyping and validation.

Transportation And Automotive Engineering Service Product Innovations

The transportation and automotive engineering service sector is witnessing a wave of groundbreaking product innovations driven by the convergence of software, hardware, and advanced analytics. Key advancements include the development of sophisticated AI-powered predictive maintenance platforms that analyze vehicle sensor data to anticipate component failures, thereby reducing downtime and operational costs. Furthermore, innovative solutions for advanced driver-assistance systems (ADAS) are emerging, offering enhanced safety features such as advanced lane-keeping assist, adaptive cruise control, and automatic emergency braking, often powered by novel sensor fusion techniques and real-time processing. The electrification trend has spurred innovations in battery management systems (BMS) that optimize charging cycles, extend battery life, and improve thermal performance. Additionally, engineering services are now deeply integrated with the development of software-defined vehicles, enabling modular architectures that allow for frequent over-the-air (OTA) updates, enhancing vehicle functionality and security post-purchase. This focus on agile software development and robust cybersecurity is a unique selling proposition for leading providers like Capgemini and Tech Mahindra.

Propelling Factors for Transportation And Automotive Engineering Service Growth

The transportation and automotive engineering service market is propelled by a confluence of powerful factors. Foremost among these is the global mandate for vehicle electrification, driving unprecedented demand for expertise in battery technology, electric powertrains, and charging infrastructure. The relentless pursuit of autonomous driving technologies necessitates complex software and hardware engineering solutions for sensor integration, AI algorithm development, and validation. Increasingly stringent regulatory compliance, particularly concerning emissions reduction and safety standards, compels automakers to invest heavily in advanced engineering services. Furthermore, the pervasive integration of connectivity services and the shift towards software-defined vehicles create a continuous need for sophisticated automotive software development and cybersecurity expertise. Finally, the growing trend of outsourcing non-core engineering activities by Original Equipment Manufacturers (OEMs) to specialized service providers further fuels market expansion.

Obstacles in the Transportation And Automotive Engineering Service Market

Despite robust growth, the transportation and automotive engineering service market faces several significant obstacles. Regulatory complexities and evolving standards across different regions can create fragmented development requirements and increase compliance costs. Supply chain disruptions, as witnessed in recent years, can severely impact the availability of critical components, leading to project delays and increased expenditure for engineering services tied to hardware development. Intense competitive pressures from a growing number of service providers, both large and specialized, can lead to price erosion and margin compression. Moreover, the rapid pace of technological change, especially in areas like AI and electrification, requires continuous investment in talent acquisition and upskilling, posing a talent gap challenge. The high upfront cost of implementing advanced testing and simulation infrastructure can also be a barrier for smaller engineering firms.

Future Opportunities in Transportation And Automotive Engineering Service

Emerging opportunities in the transportation and automotive engineering service market are abundant and diverse. The continued growth of the Electric Vehicle (EV) market presents significant opportunities in areas such as advanced battery thermal management, lightweight materials for EV platforms, and the development of smart charging solutions. The maturation of autonomous driving technologies, particularly Level 4 and Level 5, will open up vast markets for validation, simulation, and AI-driven decision-making systems. The increasing demand for connected vehicle services, including V2X communication, over-the-air updates, and in-car infotainment, offers a fertile ground for software and cybersecurity engineering expertise. Furthermore, the development of sustainable mobility solutions, including hydrogen fuel cell technology and advanced recycling processes for automotive components, will create new avenues for specialized engineering services. The expansion into emerging markets and the development of engineering solutions for new mobility concepts like micro-mobility also represent significant future growth potential.

Major Players in the Transportation And Automotive Engineering Service Ecosystem

- Capgemini

- Akka Technologies

- Tech Mahindra

- HCLTech

- HARMAN International

- RICARDO

- AVL

- Bertrandt

- ALTEN Group

- L&T Technology Services

- FEV

- Onward Technologies

- Kistler

- EDAG Group

- ESI Group

- Segula Technologies

- GlobalLogic

- EPAM

- Belcan

- T-NET JAPAN

- HORIBA

- Intertek

- Altair

Key Developments in Transportation And Automotive Engineering Service Industry

- 2023 Q4: HARMAN International announced a significant partnership with a major automotive OEM to develop next-generation in-car infotainment systems, integrating advanced AI capabilities.

- 2024 Q1: AVL launched a new suite of simulation tools for rapid development and validation of electric vehicle powertrains, significantly reducing testing timelines.

- 2024 Q2: Tech Mahindra acquired a specialized automotive software company, further strengthening its capabilities in connected car solutions and cybersecurity.

- 2024 Q3: Capgemini expanded its global R&D center focused on autonomous driving technologies, investing heavily in AI and machine learning talent.

- 2024 Q4: Ricardo unveiled a new modular platform for high-performance electric vehicle transmissions, addressing the growing demand for scalable EV architectures.

- 2025 Q1 (Projected): Akka Technologies is expected to announce a new strategic alliance focused on developing advanced ADAS sensor fusion technologies for commercial vehicles.

- 2025 Q2 (Projected): L&T Technology Services is anticipated to launch new services for battery lifecycle management and sustainable automotive manufacturing processes.

Strategic Transportation And Automotive Engineering Service Market Forecast

The strategic forecast for the transportation and automotive engineering service market is exceptionally positive, driven by the irreversible megatrends of electrification, autonomy, and connectivity. The increasing complexity of vehicles, coupled with stricter environmental regulations and evolving consumer expectations, ensures a sustained demand for specialized engineering expertise. Growth catalysts include the widespread adoption of electric vehicles, the advancement of semi-autonomous and fully autonomous driving systems, and the proliferation of connected car features enabling seamless data exchange and enhanced user experiences. Furthermore, the growing emphasis on cybersecurity for automotive applications and the development of sustainable mobility solutions will open new market segments. The market's potential is further amplified by ongoing consolidation through mergers and acquisitions, which will lead to stronger, more integrated service offerings and increased market penetration, promising significant returns for stakeholders invested in this dynamic sector.

Transportation And Automotive Engineering Service Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Type

- 2.1. Electrical and Body Controls

- 2.2. Chassis

- 2.3. Connectivity Services

- 2.4. Powertrain and Exhaust

- 2.5. Simulation

- 2.6. Others

Transportation And Automotive Engineering Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Transportation And Automotive Engineering Service Regional Market Share

Geographic Coverage of Transportation And Automotive Engineering Service

Transportation And Automotive Engineering Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Electrical and Body Controls

- 5.2.2. Chassis

- 5.2.3. Connectivity Services

- 5.2.4. Powertrain and Exhaust

- 5.2.5. Simulation

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Electrical and Body Controls

- 6.2.2. Chassis

- 6.2.3. Connectivity Services

- 6.2.4. Powertrain and Exhaust

- 6.2.5. Simulation

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Electrical and Body Controls

- 7.2.2. Chassis

- 7.2.3. Connectivity Services

- 7.2.4. Powertrain and Exhaust

- 7.2.5. Simulation

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Electrical and Body Controls

- 8.2.2. Chassis

- 8.2.3. Connectivity Services

- 8.2.4. Powertrain and Exhaust

- 8.2.5. Simulation

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Electrical and Body Controls

- 9.2.2. Chassis

- 9.2.3. Connectivity Services

- 9.2.4. Powertrain and Exhaust

- 9.2.5. Simulation

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Transportation And Automotive Engineering Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Electrical and Body Controls

- 10.2.2. Chassis

- 10.2.3. Connectivity Services

- 10.2.4. Powertrain and Exhaust

- 10.2.5. Simulation

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Capgemini

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Akka Technologies

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Tech Mahindra

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Automotive Engineering

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 HCLTech

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HARMAN International

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 RICARDO

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AVL

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Bertrandt

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ALTEN Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 L&T Technology Services

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 FEV

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Onward Technologies

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Kistler

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 EDAG Group

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ESI Group

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Segula Technologies

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 GlobalLogic

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 EPAM

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Belcan

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 T-NET JAPAN

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 HORIBA

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Intertek

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Altair

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.1 Capgemini

List of Figures

- Figure 1: Global Transportation And Automotive Engineering Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Transportation And Automotive Engineering Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Transportation And Automotive Engineering Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Transportation And Automotive Engineering Service Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Transportation And Automotive Engineering Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Transportation And Automotive Engineering Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Transportation And Automotive Engineering Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Transportation And Automotive Engineering Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Transportation And Automotive Engineering Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Transportation And Automotive Engineering Service Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Transportation And Automotive Engineering Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Transportation And Automotive Engineering Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Transportation And Automotive Engineering Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Transportation And Automotive Engineering Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Transportation And Automotive Engineering Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Transportation And Automotive Engineering Service Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Transportation And Automotive Engineering Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Transportation And Automotive Engineering Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Transportation And Automotive Engineering Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Transportation And Automotive Engineering Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Transportation And Automotive Engineering Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Transportation And Automotive Engineering Service Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Transportation And Automotive Engineering Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Transportation And Automotive Engineering Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Transportation And Automotive Engineering Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Transportation And Automotive Engineering Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Transportation And Automotive Engineering Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Transportation And Automotive Engineering Service Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Transportation And Automotive Engineering Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Transportation And Automotive Engineering Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Transportation And Automotive Engineering Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Transportation And Automotive Engineering Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Transportation And Automotive Engineering Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Transportation And Automotive Engineering Service?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the Transportation And Automotive Engineering Service?

Key companies in the market include Capgemini, Akka Technologies, Tech Mahindra, Automotive Engineering, HCLTech, HARMAN International, RICARDO, AVL, Bertrandt, ALTEN Group, L&T Technology Services, FEV, Onward Technologies, Kistler, EDAG Group, ESI Group, Segula Technologies, GlobalLogic, EPAM, Belcan, T-NET JAPAN, HORIBA, Intertek, Altair.

3. What are the main segments of the Transportation And Automotive Engineering Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Transportation And Automotive Engineering Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Transportation And Automotive Engineering Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Transportation And Automotive Engineering Service?

To stay informed about further developments, trends, and reports in the Transportation And Automotive Engineering Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence