Key Insights

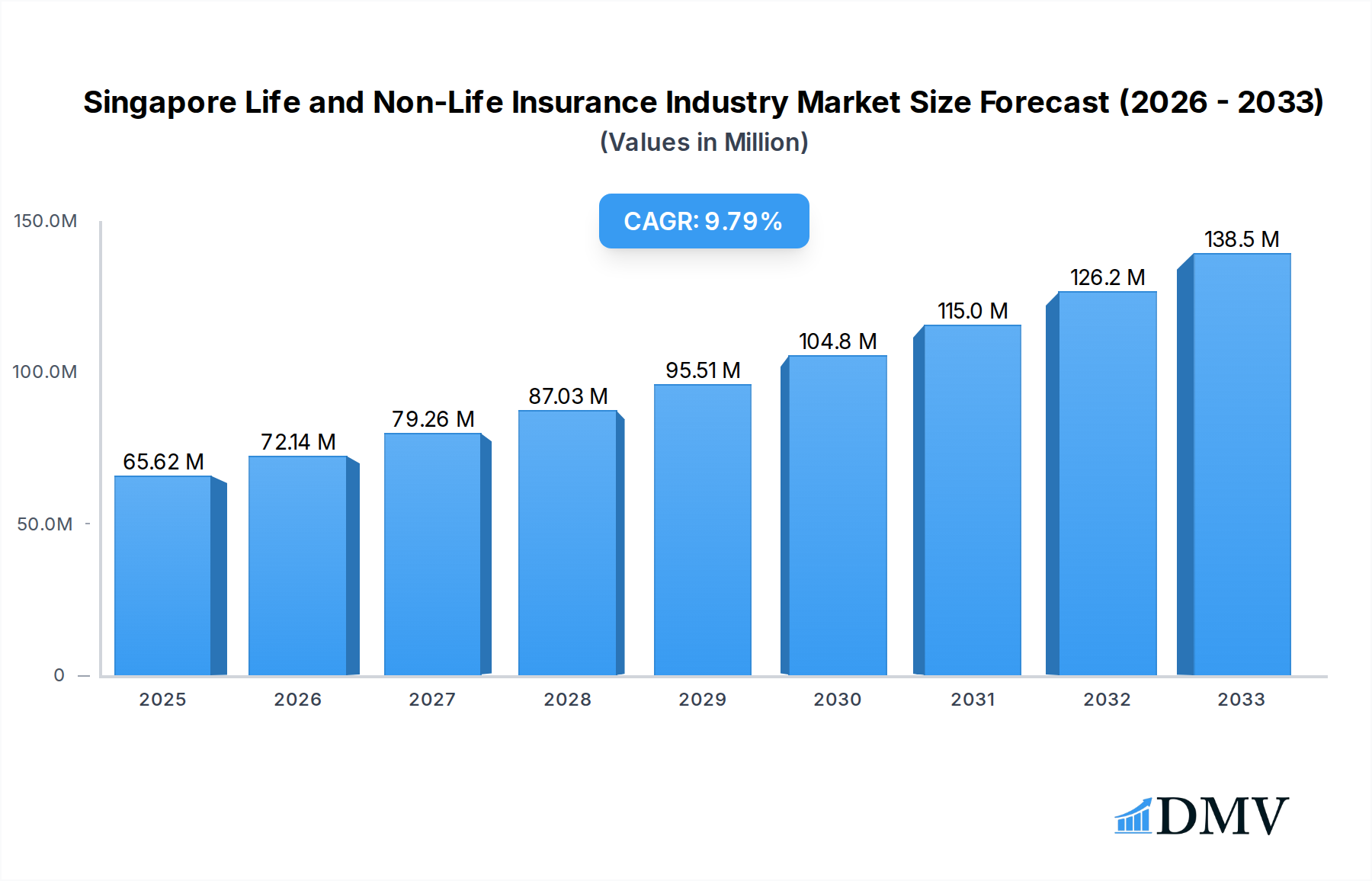

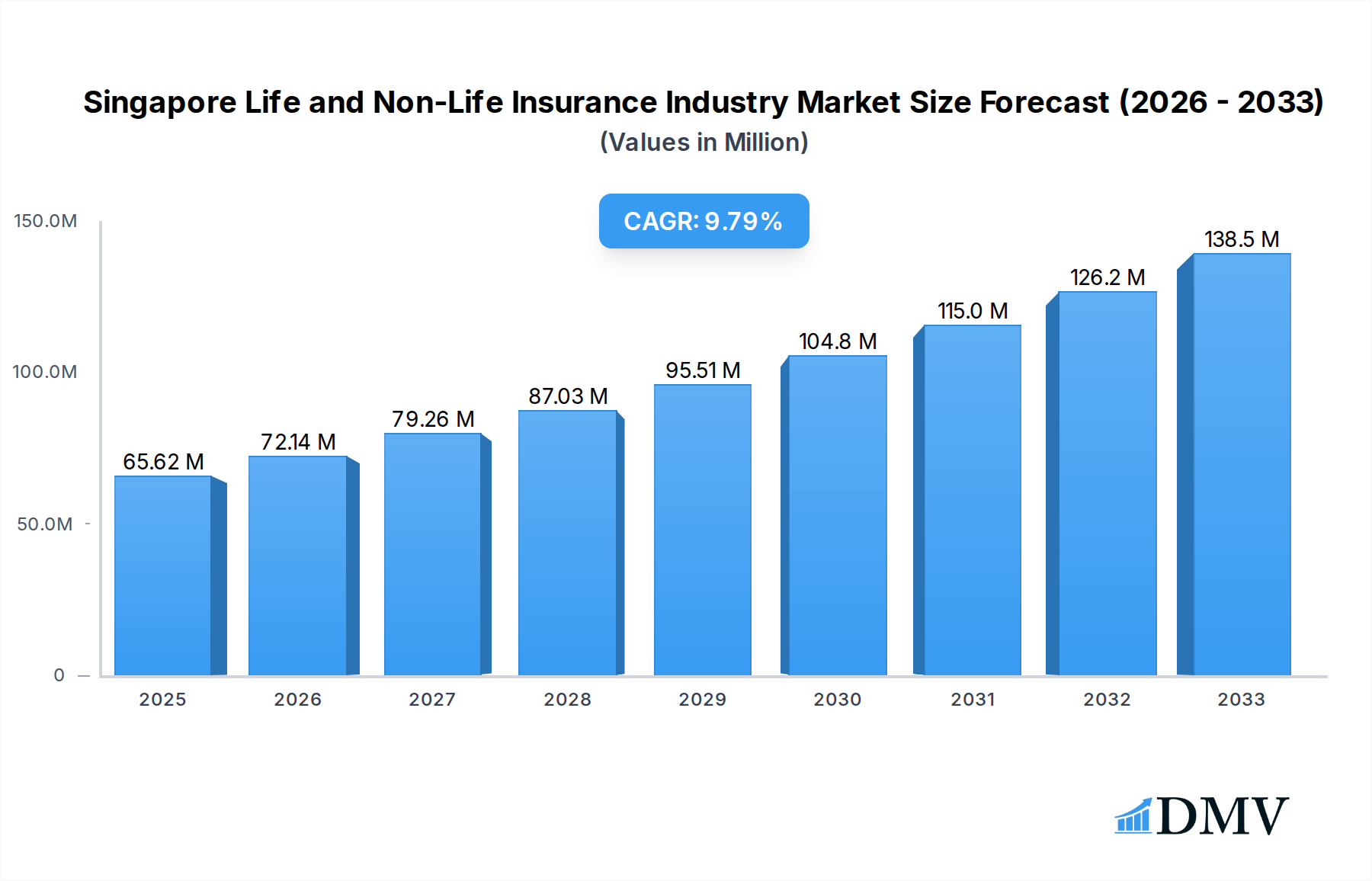

The Singapore Life and Non-Life Insurance Industry is poised for robust expansion, with a current estimated market size of 65.62 million and a projected Compound Annual Growth Rate (CAGR) of 9.95% over the forecast period. This growth is underpinned by several key drivers, including increasing disposable incomes, a growing awareness of financial planning and risk management, and a supportive regulatory environment that fosters innovation and consumer confidence. The life insurance segment, encompassing both individual and group policies, is expected to see sustained demand driven by a maturing population and an increased focus on long-term savings and protection. Similarly, the non-life insurance sector, covering essential areas like motor and home insurance, will benefit from mandatory regulations and a rising standard of living that necessitates greater asset protection. Digitalization and the adoption of InsurTech solutions are also playing a pivotal role, enhancing customer experience and streamlining distribution channels.

Singapore Life and Non-Life Insurance Industry Market Size (In Million)

The distribution landscape is undergoing a significant transformation, with direct channels and online platforms gaining prominence alongside traditional agency and banking partnerships. This evolution allows for greater accessibility and personalized product offerings. While the market is characterized by strong growth, potential restraints include intense competition among established players and emerging InsurTech startups, as well as evolving consumer preferences that demand more flexible and value-added products. Nevertheless, the industry's ability to adapt to these dynamics, coupled with a continued emphasis on personalized solutions and integrated financial services, will be crucial in sustaining its upward trajectory. Key companies like SCOR Services Asia-Pacific Pte Ltd, Swiss Re Asia Pte Ltd, and The Great Eastern Life Assurance Company Limited are at the forefront of this dynamic market, driving innovation and catering to the diverse needs of the Singaporean population.

Singapore Life and Non-Life Insurance Industry Company Market Share

Singapore Life and Non-Life Insurance Industry Market Composition & Trends

The Singapore Life and Non-Life Insurance Industry presents a dynamic and evolving landscape, characterized by significant market concentration among key players and a robust drive towards innovation. Major entities like The Great Eastern Life Assurance Company Limited, AIA Singapore Private Limited, and MSIG Insurance (Singapore) Pte Ltd hold substantial market share, influencing competitive strategies and product development. The industry is propelled by catalysts such as increasing digital adoption, a growing awareness of financial planning, and a sophisticated regulatory framework designed to foster stability and consumer protection. Substitute products, ranging from direct investments to alternative savings schemes, pose a constant challenge, necessitating insurers to continuously enhance their value propositions. End-user profiles are diversifying, with a rise in demand for personalized and flexible insurance solutions catering to different life stages and risk appetites. Mergers and acquisitions (M&A) remain a significant trend, with deal values often reaching hundreds of millions, reshaping the competitive arena. For instance, the acquisition of AXA Singapore by HSBC Insurance in February 2022 exemplifies this consolidation. The market share distribution reveals a robust presence of both life and non-life segments, with ongoing M&A activities impacting overall market concentration.

- Market Concentration: Dominated by a few large, established insurers, but with growing space for specialized and digital players.

- Innovation Catalysts: Digitalization, Insurtech advancements, evolving customer expectations, and a focus on preventative health.

- Regulatory Landscape: Proactive and supportive, emphasizing financial stability, consumer protection, and innovation enablement.

- Substitute Products: Wealth management products, direct investments, and alternative savings vehicles.

- End-User Profiles: Diverse, encompassing millennials seeking digital solutions, families requiring comprehensive protection, and seniors focusing on retirement planning.

- M&A Activities: Active, with substantial deal values driving consolidation and market expansion.

Singapore Life and Non-Life Insurance Industry Industry Evolution

The Singapore Life and Non-Life Insurance Industry has undergone a remarkable transformation throughout the historical period of 2019-2024, with projections indicating continued robust growth through 2033. Market growth trajectories are being significantly shaped by technological advancements and a palpable shift in consumer demands, moving from traditional, product-centric offerings to more personalized, needs-based solutions. The base year of 2025 serves as a pivotal point, reflecting the accumulated impact of digital acceleration and evolving consumer preferences. During the historical period, the industry witnessed an average annual growth rate of approximately 5-7% in premium income. This expansion was fueled by increasing disposable incomes, a growing middle class, and a heightened awareness of financial security, particularly in the wake of global uncertainties.

Technological advancements have been a primary driver of this evolution. The adoption of artificial intelligence (AI) and machine learning (ML) in underwriting, claims processing, and customer service has led to greater efficiency and improved customer experiences. Insurtech startups have injected innovation into the market, challenging incumbents with agile digital platforms and novel product offerings. This has pressured established players to accelerate their digital transformation strategies, invest in data analytics, and enhance their online customer engagement capabilities.

Consumer demands have also evolved dramatically. There is a discernible shift towards greater transparency, simpler policy structures, and more convenient access to insurance products and services. The rise of the digital native generation has amplified the demand for seamless online purchase journeys, self-service portals, and personalized advice delivered through digital channels. Furthermore, an increasing focus on health and wellness has spurred demand for innovative health insurance products that offer preventative care benefits, wellness programs, and integrated digital health solutions. The COVID-19 pandemic further accelerated this trend, highlighting the importance of comprehensive health coverage and the convenience of digital access.

Looking ahead to the forecast period of 2025-2033, the industry is poised for sustained growth, albeit with potential shifts in segment dominance. The estimated year of 2025 is expected to see a mature market embracing digital-first strategies. Growth rates are projected to remain in the healthy range of 4-6% annually, driven by ongoing economic development, an aging population requiring retirement and healthcare solutions, and the continued integration of technology. The industry's ability to adapt to emerging risks, such as climate change and cyber threats, through innovative product design and risk management will also be crucial. The emphasis will increasingly be on value-added services beyond traditional insurance coverage, such as financial advisory, health management platforms, and personalized risk mitigation solutions, ensuring the industry remains relevant and indispensable in the lives of Singaporean consumers.

Leading Regions, Countries, or Segments in Singapore Life and Non-Life Insurance Industry

Within the Singapore Life and Non-Life Insurance Industry, a granular analysis reveals distinct areas of dominance and growth drivers across various insurance types and distribution channels. The Life Insurance segment, particularly Individual Life Insurance, consistently exhibits strong performance, driven by a deep-seated societal emphasis on long-term financial security, retirement planning, and wealth accumulation. Singapore's well-educated populace and high disposable incomes create a fertile ground for sophisticated life insurance products, including whole life, term life, and investment-linked policies. The demand for legacy planning and protection against premature death further solidifies the dominance of this sub-segment.

- Individual Life Insurance: Leads due to strong demand for retirement planning, wealth accumulation, and protection against life's uncertainties. High disposable incomes and a focus on long-term financial security are key drivers.

- Group Life Insurance: Exhibits steady growth, driven by employer-provided benefits and a commitment to employee welfare.

- Non-Life Insurance - Motor: Remains a significant segment, though its growth is influenced by vehicle ownership trends and economic conditions.

- Non-Life Insurance - Home: Shows consistent demand, driven by property ownership and the need for asset protection.

- Non-Life Insurance - Other Non-life Insurance: A broad category encompassing travel, personal accident, and specialized commercial lines, experiencing diverse growth patterns based on economic activity and emerging risks.

When examining distribution channels, Agency channels, traditionally strong, are evolving to incorporate digital tools and hybrid models. However, Banks as a distribution channel for insurance products (bancassurance) play a crucial role, leveraging their extensive customer base and trusted relationships to offer life and non-life solutions. The Direct channel, powered by digital platforms and online comparison sites, is rapidly gaining traction, appealing to a segment of consumers seeking convenience and competitive pricing. "Other Distribution Channels," which can include brokers and affinity groups, also contribute to market penetration.

- Distribution Channel - Agency: Remains influential, adapting to digital tools and hybrid approaches to engage customers.

- Distribution Channel - Banks (Bancassurance): A dominant force, leveraging established customer relationships and broad product offerings.

- Distribution Channel - Direct: Experiencing rapid growth due to digital accessibility, convenience, and competitive pricing appeals.

- Distribution Channel - Other Distribution Channels: Includes brokers and affinity groups, contributing to niche market penetration.

Investment trends within these segments are leaning towards personalized products, digital-first experiences, and value-added services. Regulatory support for financial planning and insurance penetration continues to bolster the life insurance sector, while a focus on consumer protection influences product design across all non-life categories. The dominance of these segments is further underpinned by continuous product innovation and effective marketing strategies tailored to specific consumer needs.

Singapore Life and Non-Life Insurance Industry Product Innovations

The Singapore Life and Non-Life Insurance Industry is witnessing a wave of product innovations designed to meet evolving consumer needs and leverage technological advancements. Insurers are actively developing and launching parametric insurance products, which trigger payouts based on predefined events like natural disasters or flight delays, offering faster and more transparent claims processing. The integration of wearable technology and IoT devices is enabling personalized health and wellness insurance policies that reward healthy lifestyles with premium discounts or benefits. Furthermore, there's a growing trend towards modular and customizable insurance solutions, allowing policyholders to tailor coverage to their specific life stages and financial circumstances. These innovations are not just about coverage but also about proactive risk management and enhanced customer engagement, leading to improved policyholder satisfaction and retention.

Propelling Factors for Singapore Life and Non-Life Insurance Industry Growth

Several key factors are propelling the growth of the Singapore Life and Non-Life Insurance Industry. Technologically, the pervasive adoption of digital platforms and Insurtech solutions is enhancing customer experience, streamlining operations, and enabling personalized product offerings. Economically, Singapore's robust financial sector, high per capita income, and a strong emphasis on savings and investment create a favorable environment for insurance penetration. Regulatory support from authorities like the Monetary Authority of Singapore (MAS) in fostering innovation, promoting fair competition, and ensuring financial stability further bolsters confidence and encourages investment. An aging population, coupled with increasing awareness of the importance of financial planning and healthcare, also acts as a significant growth driver.

Obstacles in the Singapore Life and Non-Life Insurance Industry Market

Despite its growth, the Singapore Life and Non-Life Insurance Industry faces several obstacles. Regulatory challenges, while aimed at consumer protection, can sometimes lead to increased compliance costs and slower product development cycles for insurers. Supply chain disruptions, though less direct for insurance, can indirectly impact economic stability and consumer spending power, thereby affecting premium growth. Intense competitive pressures from both established players and agile Insurtech startups necessitate continuous innovation and cost management, potentially squeezing profit margins. Evolving customer expectations for seamless digital experiences and transparent pricing also present a challenge for legacy systems and traditional business models.

Future Opportunities in Singapore Life and Non-Life Insurance Industry

Emerging opportunities in the Singapore Life and Non-Life Insurance Industry are abundant. The burgeoning Insurtech sector presents a significant avenue for partnerships and the development of innovative digital-first products and services. The growing demand for cyber insurance, driven by increased digitalization and the prevalence of cyber threats, offers a substantial growth market. Furthermore, the development of sustainable and ESG-focused insurance products aligns with global trends and appeals to a growing segment of socially conscious consumers. The expansion of microinsurance solutions targeting underserved segments of the population also represents a promising opportunity for increased financial inclusion.

Major Players in the Singapore Life and Non-Life Insurance Industry Ecosystem

- SCOR Services Asia-Pacific Pte Ltd

- Swiss Re Asia Pte Ltd

- The Great Eastern Life Assurance Company Limited

- Aon Singapore Pte Ltd

- Tokio Marine Life Insurance Singapore Ltd

- MSIG Insurance (Singapore) Pte Ltd

- Liberty Insurance Pte Ltd

- Aviva Ltd

- AIA Singapore Private Limited

- Swiss Life (Singapore) Pte Ltd

Key Developments in Singapore Life and Non-Life Insurance Industry Industry

- Oct 2022: The Singapore-based digital health insurance platform DocDoc partnered with QBE Singapore to launch a new group health insurance product in the country. QBE is a leading provider of professional insurance and special expert services.

- Feb 2022: HSBC Insurance (Asia Pacific) Holdings Limited, an indirect wholly-owned subsidiary of HSBC Holdings PLC (HSBC), completed the acquisition of 100% of the issued share capital of AXA Insurance Pte Limited (AXA Singapore).

Strategic Singapore Life and Non-Life Insurance Industry Market Forecast

The strategic forecast for the Singapore Life and Non-Life Insurance Industry indicates a sustained period of growth driven by a confluence of compelling factors. The increasing embrace of Insurtech and digital transformation will continue to enhance operational efficiencies and customer engagement, paving the way for more personalized and accessible insurance solutions. An aging demographic, coupled with heightened awareness of financial planning and health management, will fuel demand for both life and non-life insurance products, particularly in the retirement and healthcare segments. Regulatory initiatives aimed at fostering innovation and protecting consumers will create a stable and trustworthy market environment. Emerging opportunities in areas such as cyber insurance, sustainable finance, and microinsurance will further diversify the market and cater to evolving consumer needs, ensuring the industry's continued relevance and robust expansion through the forecast period.

Singapore Life and Non-Life Insurance Industry Segmentation

-

1. Insurance Type

-

1.1. Life Insurance

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-life Insurance

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Other Non-life Insurance

-

1.1. Life Insurance

-

2. Distribution channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Other Distribution Channels

Singapore Life and Non-Life Insurance Industry Segmentation By Geography

- 1. Singapore

Singapore Life and Non-Life Insurance Industry Regional Market Share

Geographic Coverage of Singapore Life and Non-Life Insurance Industry

Singapore Life and Non-Life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.95% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Life Insurance

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-life Insurance

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Other Non-life Insurance

- 5.1.1. Life Insurance

- 5.2. Market Analysis, Insights and Forecast - by Distribution channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Singapore

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Singapore Life and Non-Life Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6.1.1. Life Insurance

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non-life Insurance

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Other Non-life Insurance

- 6.1.1. Life Insurance

- 6.2. Market Analysis, Insights and Forecast - by Distribution channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Insurance Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SCOR Services Asia-Pacific Pte Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Swiss Re Asia Pte Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Great Eastern Life Assurance Company Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Aon Singapore Pte Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Tokio Marine Life Insurance Singapore Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MSIG Insurance (Singapore) Pte Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Liberty Insurance Pte Ltd**List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Aviva Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AIA Singapore Private Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Swiss Life (Singapore) Pte Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 SCOR Services Asia-Pacific Pte Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Singapore Life and Non-Life Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Singapore Life and Non-Life Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 2: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Distribution channel 2020 & 2033

- Table 3: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Insurance Type 2020 & 2033

- Table 5: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Distribution channel 2020 & 2033

- Table 6: Singapore Life and Non-Life Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Singapore Life and Non-Life Insurance Industry?

The projected CAGR is approximately 9.95%.

2. Which companies are prominent players in the Singapore Life and Non-Life Insurance Industry?

Key companies in the market include SCOR Services Asia-Pacific Pte Ltd, Swiss Re Asia Pte Ltd, The Great Eastern Life Assurance Company Limited, Aon Singapore Pte Ltd, Tokio Marine Life Insurance Singapore Ltd, MSIG Insurance (Singapore) Pte Ltd, Liberty Insurance Pte Ltd**List Not Exhaustive, Aviva Ltd, AIA Singapore Private Limited, Swiss Life (Singapore) Pte Ltd.

3. What are the main segments of the Singapore Life and Non-Life Insurance Industry?

The market segments include Insurance Type, Distribution channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 65.62 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Life Insurance is Driving the Market; Increasing Digital Adoption in the Insurance Industry is Driving the Market.

6. What are the notable trends driving market growth?

Increase in GDP Per Capita of the Finance and Insurance Industry is Anticipated to Drive the Market.

7. Are there any restraints impacting market growth?

Increasing Cost Acts as a Restraint to the Market.

8. Can you provide examples of recent developments in the market?

Oct 2022: The Singapore-based digital health insurance platform DocDoc partnered with QBE Singapore to launch a new group health insurance product in the country. QBE is a leading provider of professional insurance and special expert services.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Singapore Life and Non-Life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Singapore Life and Non-Life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Singapore Life and Non-Life Insurance Industry?

To stay informed about further developments, trends, and reports in the Singapore Life and Non-Life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence