Key Insights

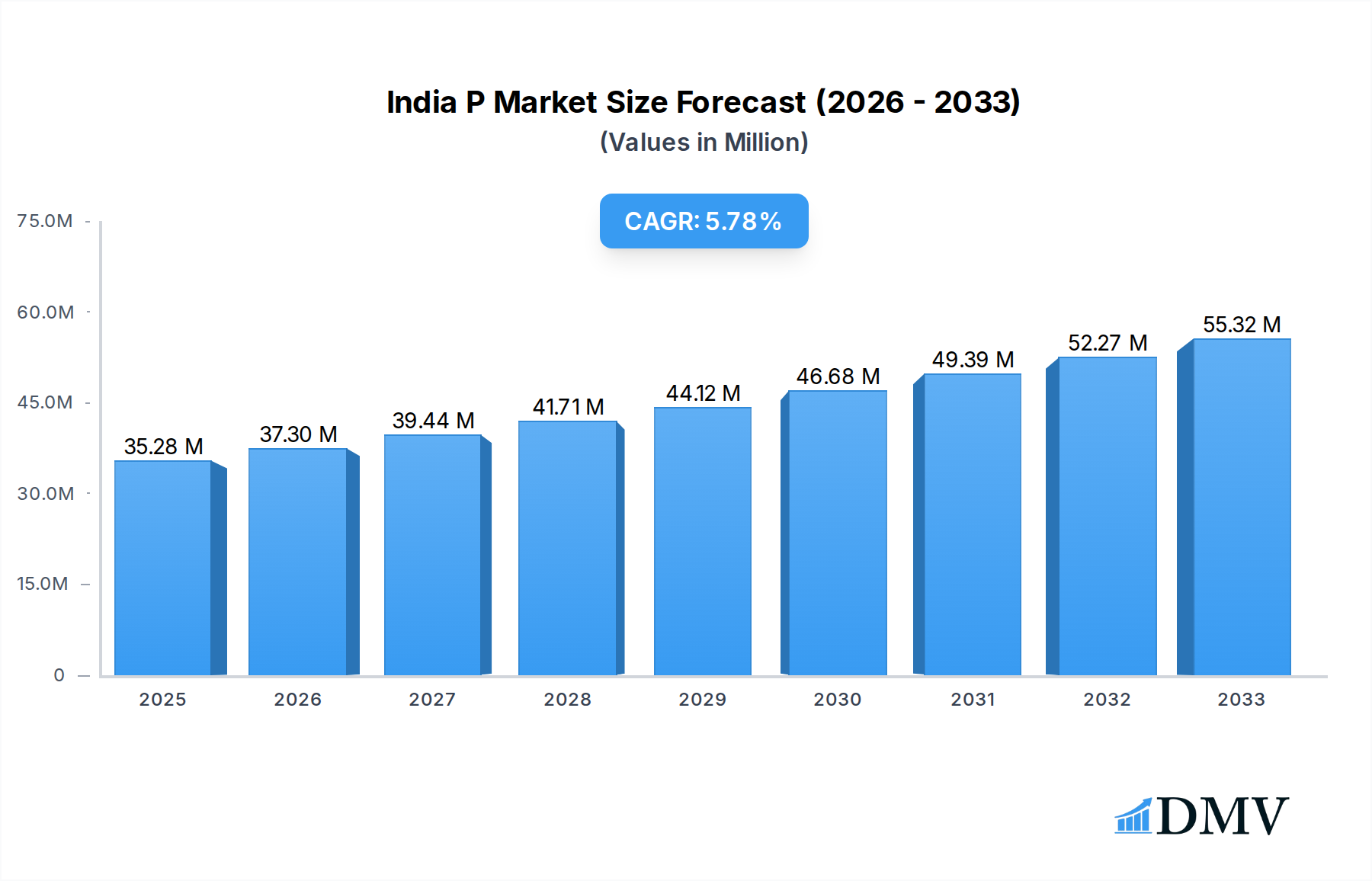

The Indian Property and Casualty (P&C) Insurance industry is poised for significant expansion, with the market size estimated at 35.28 Million in 2025. This growth is fueled by a robust CAGR of 5.78%, projecting a sustained upward trajectory through 2033. Several key drivers are propelling this expansion. A growing awareness of financial protection against unforeseen events, coupled with increasing disposable incomes, is leading to higher adoption rates for various insurance products. The government's focus on financial inclusion and digital initiatives is also making insurance more accessible to a broader population, particularly in semi-urban and rural areas. Furthermore, the evolving risk landscape, encompassing climate-related events and technological advancements, necessitates comprehensive P&C coverage. Industries like manufacturing, construction, and transportation, which are burgeoning in India, also represent substantial demand for specialized insurance solutions such as engineering and motor insurance. The widespread adoption of technology in underwriting and claims processing is further streamlining operations and enhancing customer experience, acting as a positive catalyst for market growth.

India P&C Insurance Industry Market Size (In Million)

The Indian P&C Insurance market is characterized by a diverse range of product types, including fire insurance, marine insurance, aviation insurance, engineering insurance, motor insurance, and liability insurance, catering to a wide spectrum of individual and corporate needs. Distribution channels are also multifaceted, with direct businesses, agents, banks, brokers, and micro-insurance agents playing crucial roles in market penetration. Leading companies like The New India Assurance Co Ltd, United India Insurance Company Ltd, HDFC Ergo General Insurance, and ICICI Lombard General Insurance are actively competing and innovating to capture market share. Emerging trends indicate a growing demand for parametric insurance solutions, customized policies, and integrated risk management services. While the market demonstrates strong growth potential, certain restraints such as low insurance penetration in some segments and the need for enhanced regulatory frameworks in emerging risk areas require continuous attention. The ongoing digital transformation and a focus on customer-centricity will be critical for sustained success in this dynamic market.

India P&C Insurance Industry Company Market Share

India P&C Insurance Industry Market Composition & Trends

The Indian Property and Casualty (P&C) insurance market is experiencing robust growth, driven by increasing awareness, a burgeoning middle class, and supportive regulatory reforms. Market concentration remains significant, with a few key players holding substantial market share. Innovation is a critical catalyst, with insurers increasingly leveraging technology for product development and customer engagement. The regulatory landscape, guided by IRDAI, continues to evolve, fostering a more competitive and consumer-centric environment. Substitute products, while present in some niche areas, are largely overshadowed by the comprehensive protection offered by traditional P&C insurance. End-user profiles are diversifying, encompassing individuals, MSMEs, and large corporations, each with unique risk exposures and protection needs. Mergers and Acquisitions (M&A) activities, though currently moderate, are expected to accelerate as companies seek scale and strategic advantages. For instance, recent strategic investments highlight consolidation potential and market expansion ambitions. The market capitalization of the leading P&C insurers is estimated to be in the tens of billions of US dollars, with M&A deal values projected to rise significantly in the coming years as consolidation intensifies.

- Market Share Distribution: Dominated by a few large public and private sector insurers.

- Innovation Catalysts: Digitalization, InsurTech adoption, personalized product offerings.

- Regulatory Landscape: IRDAI's proactive approach to solvency, consumer protection, and market development.

- Substitute Products: Limited direct substitutes for comprehensive P&C coverage.

- End-User Profiles: Diversified, from individual homeowners to large industrial enterprises.

- M&A Activities: Emerging trend for strategic consolidation and market expansion.

India P&C Insurance Industry Industry Evolution

The evolution of the Indian P&C insurance industry has been a dynamic journey, transitioning from a state-controlled monopoly to a liberalized, competitive, and increasingly sophisticated market. The historical period from 2019-2024 witnessed steady growth, fueled by rising disposable incomes, increased urbanization, and a greater understanding of the importance of risk mitigation. The base year of 2025 serves as a crucial inflection point, with the market poised for accelerated expansion throughout the forecast period of 2025-2033. Technological advancements have been pivotal in this evolution. The adoption of digital platforms, AI-driven underwriting, and data analytics has not only streamlined operations but also enabled the creation of innovative, customer-centric products. Shifting consumer demands, driven by greater awareness of evolving risks such as cyber threats and climate change, have pushed insurers to broaden their product portfolios and enhance their service delivery mechanisms. For example, the growth in motor insurance has been directly correlated with the rising number of vehicles on the road, while the demand for fire and engineering insurance has seen an upward trajectory with increased industrial and infrastructure development. The penetration rate of P&C insurance, while still lower than global averages, is on a consistent upward trend, projected to reach significant milestones by 2033. Specific data points indicate a Compound Annual Growth Rate (CAGR) of approximately 10-12% over the historical period, with projections suggesting a similar or even higher growth rate in the forecast period. The adoption of InsurTech solutions has seen a dramatic increase, with over 70% of insurers reporting increased investment in digital transformation initiatives. This evolution is fundamentally reshaping how insurance is perceived, purchased, and utilized in India.

Leading Regions, Countries, or Segments in India P&C Insurance Industry

The Indian P&C Insurance Industry exhibits strong dominance in certain segments and distribution channels, reflecting the country's economic landscape and consumer behavior.

Dominant Product Types:

- Motor Insurance: This segment consistently holds the largest share in the Indian P&C insurance market. The ever-increasing number of vehicles on Indian roads, coupled with mandatory third-party liability coverage, fuels this dominance. Factors like rising per capita income, easy financing options for vehicles, and stringent traffic regulations contribute to its sustained growth. The market for motor insurance is projected to continue its upward trajectory, driven by new vehicle registrations and an increasing awareness of comprehensive coverage needs.

- Fire Insurance: With a rapidly industrializing economy and significant investments in manufacturing and infrastructure, fire insurance is another crucial segment. Protection against fire and allied perils is essential for businesses and homeowners alike. Government initiatives promoting industrial growth and smart city projects further bolster the demand for fire insurance.

Dominant Distribution Channels:

- Agents: Traditionally, agents have been the backbone of insurance distribution in India. Their deep reach into semi-urban and rural areas, coupled with their ability to build personal relationships with customers, makes them indispensable. The personal touch and advisory role offered by agents are highly valued by a significant portion of the Indian population, particularly for complex P&C products.

- Banks (Bancassurance): Bancassurance has emerged as a potent distribution channel, leveraging the vast customer base of banks. This channel offers convenience to customers, allowing them to purchase insurance alongside other financial products. The widespread presence of banks across the country makes them a highly effective conduit for reaching a large audience.

Key Drivers of Dominance:

- Regulatory Support: Favorable regulations by IRDAI encourage market penetration and product innovation across all segments.

- Economic Growth: India's robust economic growth fuels demand across various insurance products, particularly motor and fire insurance, as industrial and individual asset ownership increases.

- Consumer Awareness: Growing awareness about the importance of financial protection against unforeseen events is a significant driver across all segments and distribution channels.

- Technological Integration: While agents and banks remain dominant, the increasing adoption of digital platforms and online sales is also gaining traction, especially for simpler P&C products.

India P&C Insurance Industry Product Innovations

The Indian P&C insurance sector is witnessing a surge in innovative product development, driven by InsurTech advancements and a deeper understanding of evolving consumer needs. Insurers are now offering personalized policies tailored to specific risk profiles, moving beyond traditional one-size-fits-all approaches. Cyber insurance is gaining prominence, addressing the increasing threat of cyberattacks on businesses and individuals. Furthermore, parametric insurance solutions, which trigger payouts based on pre-defined events rather than traditional claims assessment, are being explored for agriculture and natural disaster coverage, promising faster claims settlement. These innovations are enhancing customer value proposition and driving market growth by addressing previously unmet needs with advanced technological integrations and data analytics.

Propelling Factors for India P&C Insurance Industry Growth

The Indian P&C Insurance industry's growth is propelled by several synergistic factors. Technological adoption, particularly InsurTech and AI, is revolutionizing underwriting, claims processing, and customer service, leading to increased efficiency and personalized offerings. A robust economic growth trajectory, characterized by rising disposable incomes and a burgeoning middle class, is expanding the addressable market for insurance products. Supportive regulatory reforms by IRDAI continue to foster a conducive environment for competition, innovation, and consumer protection, encouraging market expansion. Furthermore, a growing awareness of risk management and the need for financial security, amplified by increasing incidents of natural calamities and cyber threats, is driving demand across all P&C segments.

Obstacles in the India P&C Insurance Industry Market

Despite its promising outlook, the Indian P&C Insurance market faces several obstacles. A significant challenge remains the low insurance penetration rate, particularly in rural and semi-urban areas, stemming from a lack of awareness and affordability concerns for a segment of the population. The complex regulatory environment, while evolving, can sometimes pose challenges for agile product development and market entry. Intense competition among a growing number of insurers can lead to price wars, impacting profitability. Furthermore, the susceptibility to natural disasters and climate-related events introduces significant underwriting risks and can lead to substantial claims payouts, impacting the solvency of insurers. Supply chain disruptions, though less directly impacting insurance products themselves, can affect the broader economic environment that underpins insurance demand.

Future Opportunities in India P&C Insurance Industry

The future of the Indian P&C Insurance industry is brimming with opportunities. The burgeoning digital economy presents a vast untapped market for cyber insurance and other technology-dependent risk covers. The growing focus on sustainable development and climate resilience opens avenues for innovative products in areas like renewable energy project insurance and crop insurance against climate change impacts. The government's push for infrastructure development will drive demand for engineering and construction-related insurance. Furthermore, the increasing adoption of electric vehicles (EVs) and autonomous driving technologies will necessitate the development of specialized motor insurance products. Collaborations between insurers and InsurTech startups will continue to unlock new business models and enhance customer experience.

Major Players in the India P&C Insurance Industry Ecosystem

- The New India Assurance Co Ltd

- United India Insurance Company Ltd

- HDFC Ergo General Insurance

- National Insurance Company Ltd

- ICICI Lombard General Insurance

- Bajaj Allianz General Insurance

- The Oriental Insurance Co Ltd

- Cholamandalam MS General Insurance Co Ltd

- IFFCO Tokio General Insurance Co Ltd

- Reliance General Insurance Co Ltd

- SBI General Insurance Co Ltd

Key Developments in India P&C Insurance Industry Industry

- March 2024: ICICI Lombard General Insurance acquired a 0.7% stake in Kotak Mahindra Bank for USD 2.92 billion, signalling strategic investment and potential for enhanced bancassurance partnerships. Concurrently, the company issued equity shares under its ICICI Lombard Employees Stock Option Scheme-2005, demonstrating confidence in its future growth prospects and employee retention strategies.

- August 2023: HDFC ERGO partnered with Duck Creek Technologies to significantly enhance its presence and operational capabilities within the Indian insurance market. This collaboration involves the implementation of advanced cloud-based SaaS solutions and the establishment of a local workforce of approximately 1,000 people, underscoring a commitment to localized service and technological advancement. This initiative aligns with Duck Creek's broader global market strategy, specifically targeting India's insurance industry, which is projected to reach USD 200 billion by 2027. Duck Creek also established a new data center in India to robustly support this expansion and its associated technological demands.

Strategic India P&C Insurance Industry Market Forecast

The strategic forecast for the Indian P&C Insurance market points towards sustained and accelerated growth, driven by a confluence of favorable factors. The increasing adoption of digital technologies and InsurTech solutions will continue to enhance operational efficiency, personalize customer offerings, and expand market reach into previously underserved segments. Economic expansion, coupled with a rising middle class, will fuel demand for a wider array of P&C products. Supportive regulatory frameworks are expected to encourage further competition and innovation, leading to a more robust and customer-centric market. Emerging opportunities in areas like cyber insurance, parametric solutions for climate risks, and specialized coverage for new-age industries present significant avenues for market development and revenue generation, promising a dynamic and prosperous future for the sector.

India P&C Insurance Industry Segmentation

-

1. Product Type

- 1.1. Fire Insurance

- 1.2. Marine Insurance

- 1.3. Aviation Insurance

- 1.4. Engineering Insurance

- 1.5. Motor Insurance

- 1.6. Liability Insurance

- 1.7. Other Product Types

-

2. Distribution Channel

- 2.1. Direct Businesses

- 2.2. Agents

- 2.3. Banks

- 2.4. Brokers

- 2.5. Micro-Insurance Agents

- 2.6. Other Distribution Channel

India P&C Insurance Industry Segmentation By Geography

- 1. India

India P&C Insurance Industry Regional Market Share

Geographic Coverage of India P&C Insurance Industry

India P&C Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Fire Insurance

- 5.1.2. Marine Insurance

- 5.1.3. Aviation Insurance

- 5.1.4. Engineering Insurance

- 5.1.5. Motor Insurance

- 5.1.6. Liability Insurance

- 5.1.7. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct Businesses

- 5.2.2. Agents

- 5.2.3. Banks

- 5.2.4. Brokers

- 5.2.5. Micro-Insurance Agents

- 5.2.6. Other Distribution Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. India P&C Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Fire Insurance

- 6.1.2. Marine Insurance

- 6.1.3. Aviation Insurance

- 6.1.4. Engineering Insurance

- 6.1.5. Motor Insurance

- 6.1.6. Liability Insurance

- 6.1.7. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct Businesses

- 6.2.2. Agents

- 6.2.3. Banks

- 6.2.4. Brokers

- 6.2.5. Micro-Insurance Agents

- 6.2.6. Other Distribution Channel

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 The New India Assurance Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 United India Insurance Company Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 HDFC Ergo General Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 National Insurance Company Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 ICICI Lombard General Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Bajaj Allianz General Insurance

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 The Oriental Insurance Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cholamandalam MS General Insurance Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 IFFCO Tokio General Insurance Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Reliance General Insurance Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SBI General Insurance Co Ltd**List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 The New India Assurance Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India P&C Insurance Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India P&C Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: India P&C Insurance Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: India P&C Insurance Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 3: India P&C Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: India P&C Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: India P&C Insurance Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: India P&C Insurance Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: India P&C Insurance Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: India P&C Insurance Industry Volume Billion Forecast, by Product Type 2020 & 2033

- Table 9: India P&C Insurance Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: India P&C Insurance Industry Volume Billion Forecast, by Distribution Channel 2020 & 2033

- Table 11: India P&C Insurance Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: India P&C Insurance Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India P&C Insurance Industry?

The projected CAGR is approximately 5.78%.

2. Which companies are prominent players in the India P&C Insurance Industry?

Key companies in the market include The New India Assurance Co Ltd, United India Insurance Company Ltd, HDFC Ergo General Insurance, National Insurance Company Ltd, ICICI Lombard General Insurance, Bajaj Allianz General Insurance, The Oriental Insurance Co Ltd, Cholamandalam MS General Insurance Co Ltd, IFFCO Tokio General Insurance Co Ltd, Reliance General Insurance Co Ltd, SBI General Insurance Co Ltd**List Not Exhaustive.

3. What are the main segments of the India P&C Insurance Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.28 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Awareness of Insurance Benefits; Increased Asset Ownership is Expected to Drive Market Growth.

6. What are the notable trends driving market growth?

Growing Awareness of Insurance Products and Services is Driving the Market.

7. Are there any restraints impacting market growth?

Rising Awareness of Insurance Benefits; Increased Asset Ownership is Expected to Drive Market Growth.

8. Can you provide examples of recent developments in the market?

March 2024: ICICI Lombard General Insurance acquired a 0.7% stake in Kotak Mahindra Bank for USD 2.92 billion. Concurrently, the company issued equity shares under its ICICI Lombard Employees Stock Option Scheme-2005, indicating confidence in its growth prospects.August 2023: HDFC ERGO partnered with Duck Creek Technologies to enhance its presence in the Indian insurance market. The collaboration involves implementing cloud-based SaaS solutions and employing a local workforce of approximately 1,000 people. This initiative aligns with Duck Creek's global market strategy and targets India's insurance industry, which is projected to reach USD 200 billion by 2027. Duck Creek established a new data center in India to support this expansion.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India P&C Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India P&C Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India P&C Insurance Industry?

To stay informed about further developments, trends, and reports in the India P&C Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence