Key Insights

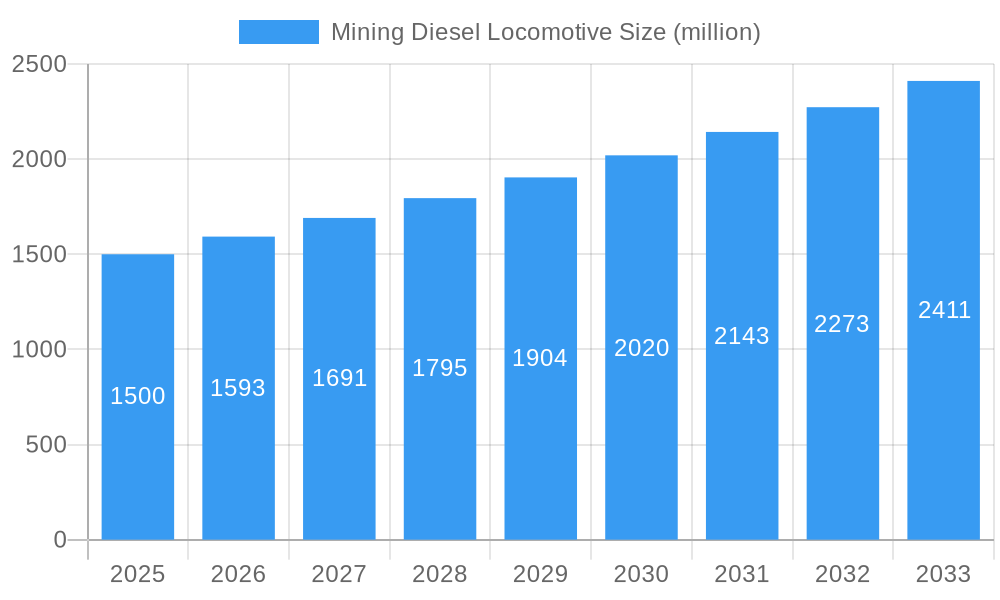

The global mining diesel locomotive market is poised for substantial growth, with an estimated market size of USD 23.52 billion by 2025, driven by a projected Compound Annual Growth Rate (CAGR) of 8.4% from 2025 to 2033. This expansion is underpinned by the increasing global demand for essential minerals and metals, necessitating efficient and robust material handling solutions in both underground and open-cast mining operations. Technological advancements, including enhanced fuel efficiency, reduced emissions, and improved safety features, are further propelling market adoption as mining companies seek to optimize operational costs and environmental compliance. Investments in mining infrastructure, particularly in emerging economies, are also a key growth catalyst.

Mining Diesel Locomotive Market Size (In Billion)

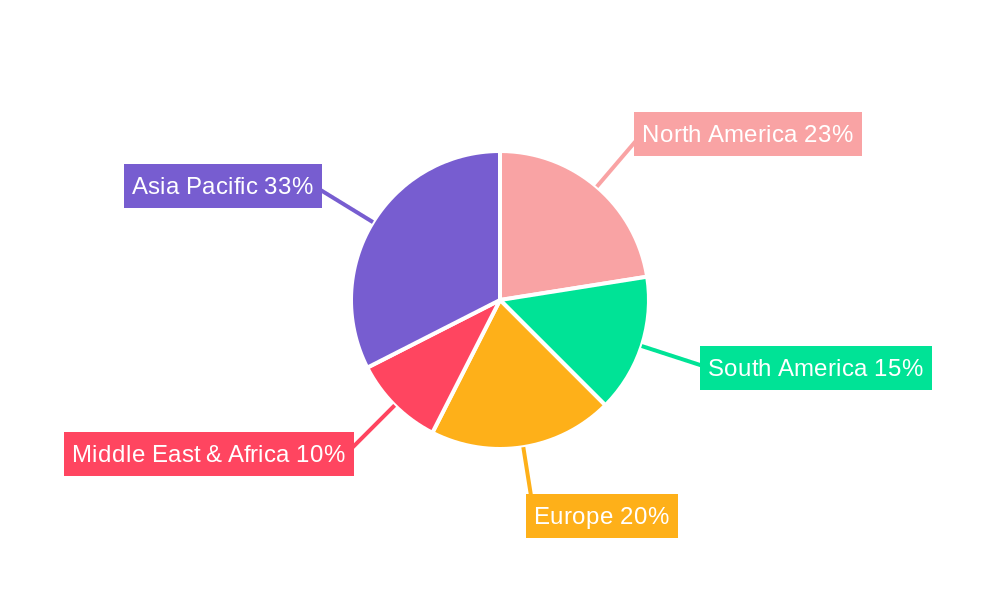

The market segmentation indicates a dominance of locomotives exceeding 40 tons, reflecting the trend towards larger-scale mining operations. Both Underground Mining and Open-Cast Mining applications are significant, each requiring specialized locomotive designs. Geographically, the Asia Pacific region is expected to lead in both market size and growth, fueled by extensive mining activities and technological advancements. North America and Europe represent mature markets focused on fleet modernization and sustainable solutions. Key market challenges include stringent environmental regulations and the considerable initial investment required for these specialized vehicles.

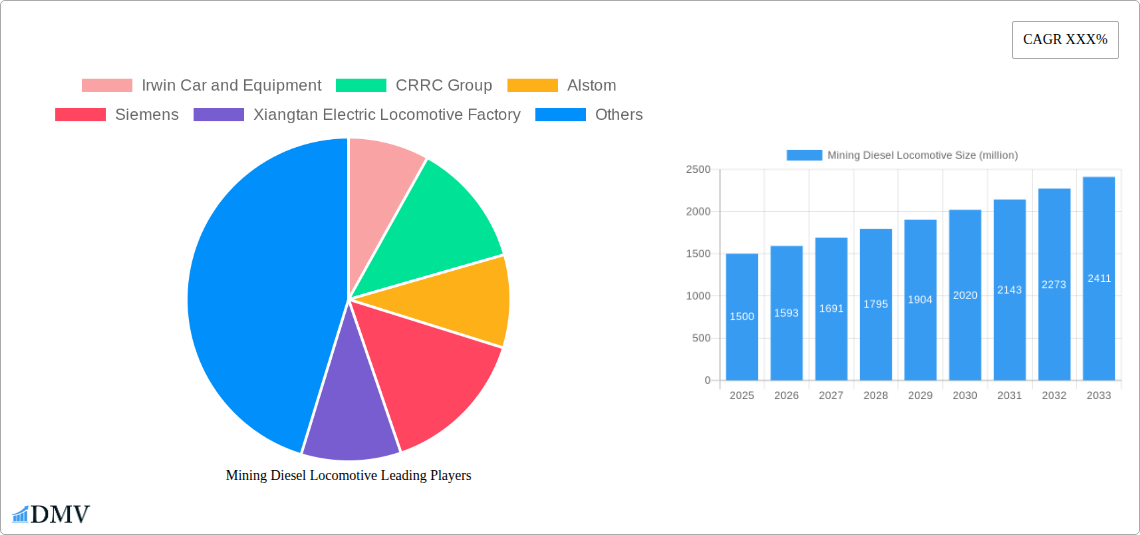

Mining Diesel Locomotive Company Market Share

This analysis provides a comprehensive overview of the mining diesel locomotive market, forecasting its development from 2025 to 2033, with 2025 as the base year. It covers market share, key growth drivers, and the regulatory environment, offering critical insights for stakeholders involved in underground mining and open-cast mining sectors. The report details locomotive types from less than 20 tons to more than 40 tons and examines the strategies of leading manufacturers in the heavy-duty mining equipment sector.

Mining Diesel Locomotive Market Composition & Trends

The global mining diesel locomotive market is characterized by a moderate to high concentration, with a few dominant players holding significant market shares. Innovation is primarily driven by the demand for increased efficiency, reduced emissions, and enhanced safety features in harsh mining environments. Regulatory landscapes are evolving, with a growing emphasis on environmental compliance and the adoption of cleaner technologies, though diesel remains a prevalent power source in many remote mining operations. Substitute products, such as battery-powered locomotives and conveyor systems, are gaining traction, particularly in underground applications where ventilation is a concern. End-user profiles span large-scale mining corporations, mid-sized mining operations, and specialized contractors, all seeking reliable and robust hauling solutions. Mergers and acquisitions (M&A) activities, with estimated deal values in the hundreds of million, are strategically reshaping the competitive landscape, consolidating expertise and expanding market reach. The market also observes continuous efforts towards optimizing operational costs and improving the lifespan of existing fleets, contributing to a stable demand for maintenance and upgrade services.

- Market Concentration: Dominated by a few key global manufacturers.

- Innovation Catalysts: Focus on fuel efficiency, emission reduction, and operational safety.

- Regulatory Landscapes: Increasing environmental scrutiny, driving demand for cleaner technologies.

- Substitute Products: Battery-electric locomotives and conveyor systems are emerging alternatives.

- End-User Profiles: Large mining corporations, mid-sized operations, and contractors.

- M&A Activities: Strategic consolidation to enhance market position and technological capabilities, with significant million dollar valuations.

Mining Diesel Locomotive Industry Evolution

The mining diesel locomotive industry has undergone a significant evolution, driven by both technological advancements and the changing demands of the global mining sector. Historically, diesel locomotives were the undisputed workhorses due to their ruggedness, range, and relative ease of operation in remote locations. The study period, 2019–2024, witnessed a steady demand, with an estimated market value of hundreds of million in the base year of 2025. Technological advancements have focused on improving engine performance, reducing fuel consumption, and minimizing particulate matter emissions to comply with stricter environmental regulations. Innovations in power train technology, including hydrostatic transmissions and more efficient turbocharging systems, have played a crucial role. The adoption rate of more advanced and fuel-efficient diesel models has been gradually increasing, with an estimated adoption rate of xx% for new generation locomotives in the last few years of the historical period. Shifting consumer demands are increasingly prioritizing not only performance and reliability but also the total cost of ownership, including maintenance, fuel, and environmental impact. This has led to a greater emphasis on durability, modular design for easier repairs, and longer service intervals. The market has also seen a rise in specialized locomotive designs tailored for specific mining conditions, such as those with enhanced braking systems for steep inclines or improved dust suppression for arid environments. Furthermore, the integration of telematics and diagnostic tools has become more prevalent, enabling predictive maintenance and optimizing fleet management, a trend that has seen a xx% increase in adoption over the past two years of the historical period. The industry is continuously adapting to the cyclical nature of mining commodity prices, balancing investment in new equipment with the operational efficiency of existing fleets. The forecast period, 2025–2033, is anticipated to see a continued, albeit moderated, growth trajectory, with an estimated annual growth rate of xx% to millions. This evolution is a testament to the industry's resilience and its capacity to innovate in response to global economic and environmental shifts.

Leading Regions, Countries, or Segments in Mining Diesel Locomotive

The mining diesel locomotive market exhibits distinct regional dominance and segment preferences, driven by the prevalence of mining activities, regulatory frameworks, and technological adoption rates. Underground mining applications consistently represent a significant portion of the market share, estimated at xx% of total market revenue, due to the essential role of locomotives in hauling ore and materials through complex tunnel systems. Within this segment, the 20 tons to 40 tons weight category is particularly dominant, accounting for an estimated xx% of underground mining locomotive sales, offering a balance of power and maneuverability required for confined spaces. Conversely, open-cast mining operations often necessitate larger and more powerful locomotives, with the more than 40 tons category seeing substantial demand, representing an estimated xx% of the open-cast segment.

Geographically, regions with substantial mining industries, such as Australia, North America (Canada and the United States), and certain parts of South America (e.g., Chile, Peru), are leading consumers. The investment trends in these regions are heavily influenced by commodity prices and new project developments. For instance, substantial investments in new mines and expansions in Australia are projected to drive demand for more than 40 tons locomotives in open-cast operations, contributing an estimated hundreds of million to regional market growth. In contrast, countries like China, with extensive underground mining operations and significant domestic manufacturing capabilities, represent a substantial market for less than 20 tons and 20 tons to 40 tons locomotives, particularly within the underground mining segment. Regulatory support for technological upgrades and emissions reduction also plays a pivotal role. Countries with stringent environmental regulations are seeing a growing preference for fuel-efficient and lower-emission diesel locomotives, or are actively exploring alternative power sources, though diesel remains a reliable option for many established operations. The sheer scale of mining operations in these leading regions, coupled with ongoing technological adoption and the need for efficient material transport, solidifies their position as key drivers of the global mining diesel locomotive market, with an overall market share estimated at over xx% for the top three regions combined.

- Dominant Application: Underground Mining, accounting for an estimated xx% of market revenue.

- Key Weight Segment (Underground): 20 tons to 40 Tons, representing an estimated xx% of underground applications.

- Key Weight Segment (Open-Cast): More than 40 Tons, significant within open-cast mining.

- Leading Regions: Australia, North America, and South America, driven by extensive mining activities.

- Significant Market: China, with strong domestic manufacturing and underground mining focus.

- Investment Trends: Commodity prices and new mining project development are key drivers.

- Regulatory Impact: Stringent environmental laws are influencing technology adoption.

Mining Diesel Locomotive Product Innovations

Product innovations in the mining diesel locomotive sector are primarily focused on enhancing operational efficiency, improving safety, and reducing environmental impact. Manufacturers are developing locomotives with advanced fuel injection systems and engine management technologies to achieve significant improvements in fuel economy, leading to estimated fuel cost reductions of up to xx% for operators. Enhanced braking systems, utilizing dynamic braking and fail-safe mechanisms, are being integrated to ensure safe operation on steep gradients, a critical factor in many mining environments. Furthermore, the incorporation of robust, dust-resistant components and improved cabin ergonomics contribute to the longevity of the equipment and the well-being of operators. Unique selling propositions now include telematics integration for real-time performance monitoring and predictive maintenance, allowing for reduced downtime and optimized operational schedules.

Propelling Factors for Mining Diesel Locomotive Growth

The growth of the mining diesel locomotive market is propelled by several interconnected factors. Firstly, the sustained global demand for essential minerals and metals, driven by industrialization and infrastructure development, necessitates efficient and reliable material transport solutions, directly boosting demand for these locomotives. Secondly, technological advancements in engine design are yielding more fuel-efficient and lower-emission diesel engines, addressing environmental concerns while reducing operational costs for mining companies. For example, the adoption of modern diesel particulate filters (DPFs) has significantly reduced particulate emissions by an estimated xx%. Thirdly, the vast number of existing mining operations, particularly in developing economies, rely on robust and proven diesel technology, creating a consistent demand for new units and replacement parts. The significant investment in new mining projects, estimated in the billions of million globally, further fuels the need for essential hauling equipment. Finally, the inherent advantages of diesel locomotives in terms of range, refueling infrastructure availability (especially in remote locations), and initial cost-effectiveness continue to make them a preferred choice for many mining applications.

Obstacles in the Mining Diesel Locomotive Market

Despite robust growth drivers, the mining diesel locomotive market faces several obstacles. Stringent environmental regulations, particularly concerning emissions standards, pose a significant challenge, necessitating costly upgrades or driving a shift towards alternative technologies. Supply chain disruptions, as witnessed in recent global events, can impact the availability of critical components and raw materials, leading to production delays and increased costs. Competitive pressure from emerging technologies like battery-electric locomotives, which offer zero tailpipe emissions and potentially lower running costs in certain environments, presents a growing restraint. Moreover, the volatile nature of commodity prices can lead to fluctuations in mining investment, directly affecting the demand for new locomotives. The initial capital investment required for new diesel locomotives, though often lower than alternatives, can still be a barrier for smaller mining operations.

Future Opportunities in Mining Diesel Locomotive

The mining diesel locomotive market presents several promising future opportunities. The increasing focus on hybrid diesel-electric powertrains offers a pathway to reduce fuel consumption and emissions while retaining the operational flexibility of diesel. Furthermore, the growing demand for specialized locomotives designed for extreme conditions, such as those in Arctic regions or high-altitude mines, opens up niche market segments. The expansion of mining operations in developing economies, with less stringent initial environmental regulations but a growing awareness of sustainability, presents a significant growth avenue. The retrofitting and upgrading of existing fleets with modern, more efficient engines and emission control systems also represent a substantial aftermarket opportunity. Finally, the integration of advanced automation and remote operation capabilities into diesel locomotives can enhance safety and efficiency, creating a competitive advantage for manufacturers who invest in these technologies.

Major Players in the Mining Diesel Locomotive Ecosystem

- Irwin Car and Equipment

- CRRC Group

- Alstom

- Siemens

- Xiangtan Electric Locomotive Factory

- China Railway Baoji Machinery

- TridentGroup

- AEG Power Solutions

- Hitachi

- Bombardier Transportation

- Jining Enwei Intelligent Technology

Key Developments in Mining Diesel Locomotive Industry

- 2023: Increased focus on hybrid diesel-electric locomotive development by major manufacturers to meet evolving emission standards.

- 2022: Several mining companies in Australia and Canada announced significant investments in new mine expansions, boosting demand for heavy-duty locomotives.

- 2021: Launch of advanced emission control systems for diesel locomotives, achieving xx% reduction in particulate matter.

- 2020: Strategic partnerships formed between locomotive manufacturers and battery technology providers to explore hybrid solutions.

- 2019: Introduction of telematics and IoT integration in new diesel locomotive models for enhanced fleet management and predictive maintenance.

Strategic Mining Diesel Locomotive Market Forecast

The strategic mining diesel locomotive market forecast anticipates continued growth driven by the indispensable role of these machines in global resource extraction. The market's future is intrinsically linked to ongoing technological advancements, particularly in hybrid powertrains and emission reduction technologies, which will allow diesel locomotives to remain competitive. Emerging markets and the continuous need for efficient hauling in both established and new mining ventures will provide a stable demand base. Investment in upgraded locomotives, offering improved fuel efficiency and lower operational costs, alongside the aftermarket for maintenance and parts, will represent significant growth catalysts. The industry's ability to adapt to evolving environmental regulations while maintaining cost-effectiveness will be key to its sustained success, with an estimated market expansion reaching several millions by 2033.

Mining Diesel Locomotive Segmentation

-

1. Application

- 1.1. Underground Mining

- 1.2. Open-Cast Mining

-

2. Type

- 2.1. Less than 20 Tons

- 2.2. 20 tons to 40 Tons

- 2.3. More than 40 Tons

Mining Diesel Locomotive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mining Diesel Locomotive Regional Market Share

Geographic Coverage of Mining Diesel Locomotive

Mining Diesel Locomotive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Underground Mining

- 5.1.2. Open-Cast Mining

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Less than 20 Tons

- 5.2.2. 20 tons to 40 Tons

- 5.2.3. More than 40 Tons

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Underground Mining

- 6.1.2. Open-Cast Mining

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Less than 20 Tons

- 6.2.2. 20 tons to 40 Tons

- 6.2.3. More than 40 Tons

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Underground Mining

- 7.1.2. Open-Cast Mining

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Less than 20 Tons

- 7.2.2. 20 tons to 40 Tons

- 7.2.3. More than 40 Tons

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Underground Mining

- 8.1.2. Open-Cast Mining

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Less than 20 Tons

- 8.2.2. 20 tons to 40 Tons

- 8.2.3. More than 40 Tons

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Underground Mining

- 9.1.2. Open-Cast Mining

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Less than 20 Tons

- 9.2.2. 20 tons to 40 Tons

- 9.2.3. More than 40 Tons

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Mining Diesel Locomotive Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Underground Mining

- 10.1.2. Open-Cast Mining

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Less than 20 Tons

- 10.2.2. 20 tons to 40 Tons

- 10.2.3. More than 40 Tons

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Irwin Car and Equipment

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 CRRC Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Alstom

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Siemens

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Xiangtan Electric Locomotive Factory

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 China Railway Baoji Machinery

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 TridentGroup

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AEG Power Solutions

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Hitachi

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Bombardier Transportation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jining Enwei Intelligent Technology

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Irwin Car and Equipment

List of Figures

- Figure 1: Global Mining Diesel Locomotive Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Mining Diesel Locomotive Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Mining Diesel Locomotive Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Mining Diesel Locomotive Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Mining Diesel Locomotive Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Mining Diesel Locomotive Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Mining Diesel Locomotive Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Mining Diesel Locomotive Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Mining Diesel Locomotive Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Mining Diesel Locomotive Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Mining Diesel Locomotive Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Mining Diesel Locomotive Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Mining Diesel Locomotive Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Mining Diesel Locomotive Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Mining Diesel Locomotive Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Mining Diesel Locomotive Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Mining Diesel Locomotive Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Mining Diesel Locomotive Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Mining Diesel Locomotive Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Mining Diesel Locomotive Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Mining Diesel Locomotive Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Mining Diesel Locomotive Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Mining Diesel Locomotive Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Mining Diesel Locomotive Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Mining Diesel Locomotive Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Mining Diesel Locomotive Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Mining Diesel Locomotive Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Mining Diesel Locomotive Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Mining Diesel Locomotive Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Mining Diesel Locomotive Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Mining Diesel Locomotive Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Mining Diesel Locomotive Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Mining Diesel Locomotive Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Mining Diesel Locomotive Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Mining Diesel Locomotive Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Mining Diesel Locomotive Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Mining Diesel Locomotive Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Mining Diesel Locomotive Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Mining Diesel Locomotive Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Mining Diesel Locomotive Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mining Diesel Locomotive?

The projected CAGR is approximately 8.4%.

2. Which companies are prominent players in the Mining Diesel Locomotive?

Key companies in the market include Irwin Car and Equipment, CRRC Group, Alstom, Siemens, Xiangtan Electric Locomotive Factory, China Railway Baoji Machinery, TridentGroup, AEG Power Solutions, Hitachi, Bombardier Transportation, Jining Enwei Intelligent Technology.

3. What are the main segments of the Mining Diesel Locomotive?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 23.52 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mining Diesel Locomotive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mining Diesel Locomotive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mining Diesel Locomotive?

To stay informed about further developments, trends, and reports in the Mining Diesel Locomotive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence