Key Insights

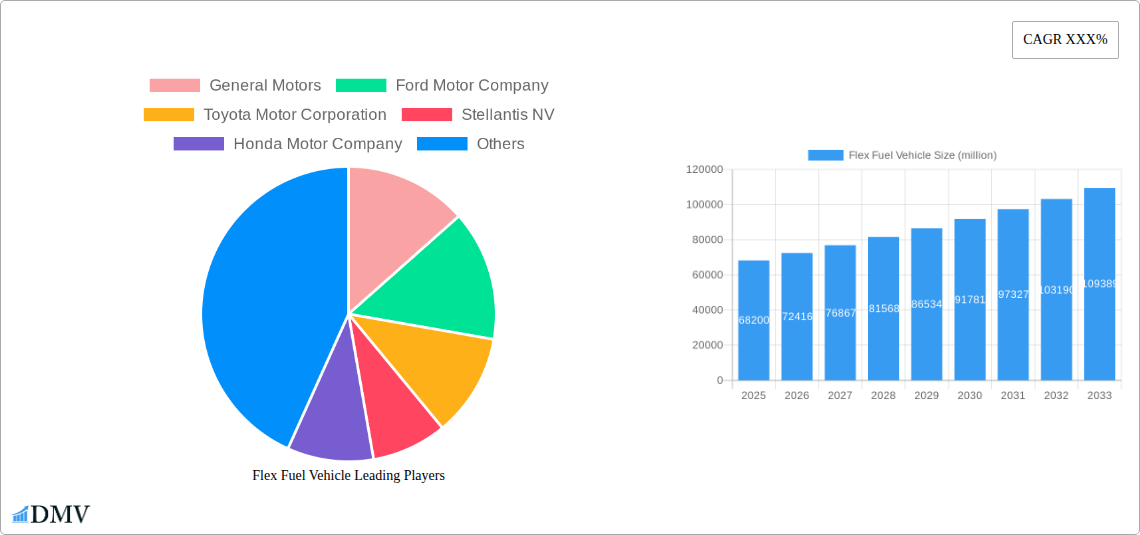

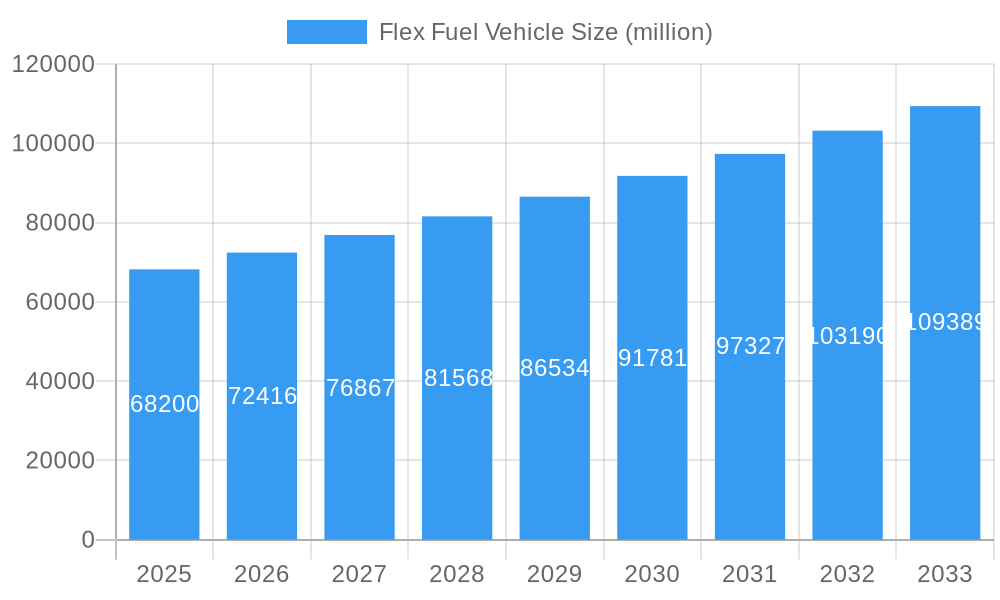

The global Flex Fuel Vehicle market is poised for significant expansion, projected to reach an estimated $68.2 billion in 2025. This growth is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 6.1% throughout the forecast period of 2025-2033. A primary driver for this burgeoning market is the increasing global demand for sustainable and renewable fuel alternatives to traditional gasoline. Governments worldwide are implementing policies and incentives to encourage the adoption of flex-fuel vehicles, recognizing their role in reducing carbon emissions and enhancing energy independence. Furthermore, advancements in engine technology have made flex-fuel vehicles more efficient and appealing to consumers, offering greater fuel flexibility and potentially lower operating costs. The Passenger Car segment is expected to lead the market, driven by consumer preference for versatile and environmentally conscious transportation options.

Flex Fuel Vehicle Market Size (In Billion)

The market's trajectory is further shaped by evolving consumer preferences and a growing awareness of environmental impact. The transition towards lower carbon footprints is a global imperative, and flex-fuel vehicles, capable of running on a blend of gasoline and ethanol, present a practical and accessible solution for many drivers. The market is segmented by ethanol blend capabilities, with E10 to E25 and E25 to E85 representing key categories, indicating a demand for vehicles that can accommodate varying levels of renewable fuel. Despite the positive outlook, challenges such as the availability and infrastructure for higher ethanol blends and consumer education regarding the benefits and operation of flex-fuel vehicles will need to be addressed to fully unlock the market's potential. However, with major automotive players like General Motors, Ford, and Toyota actively investing in flex-fuel technology, the future of this segment appears robust and dynamic.

Flex Fuel Vehicle Company Market Share

Flex Fuel Vehicle Market Composition & Trends

The global flex fuel vehicle (FFV) market is experiencing dynamic shifts, characterized by increasing adoption driven by environmental consciousness and evolving regulatory frameworks. Market concentration is moderately fragmented, with key players like General Motors, Ford Motor Company, Toyota Motor Corporation, Stellantis NV, and Volkswagen AG vying for significant market share. These flexible fuel cars and flexible fuel trucks represent a growing segment within the automotive industry, offering consumers the choice to run on gasoline or ethanol blends up to E85 and above. Innovation catalysts include advancements in engine technology for improved fuel efficiency and reduced emissions, alongside government incentives promoting the use of renewable fuels. The regulatory landscape is a critical driver, with policies supporting biofuel mandates and emissions standards directly impacting FFV sales. Substitute products, primarily electric vehicles (EVs) and traditional internal combustion engine (ICE) vehicles, present competition, but FFVs offer a bridge technology, leveraging existing refueling infrastructure. End-user profiles are diverse, encompassing environmentally conscious consumers, fleet operators seeking cost savings through cheaper ethanol blends, and regions with strong biofuel production. Mergers and acquisitions (M&A) activity, while not yet at peak billion-dollar valuations for FFV-specific deals, are present within the broader automotive and biofuel sectors, with deal values in the hundreds of billions influencing technological integration and market expansion. The market share distribution of FFVs within the total vehicle market is steadily increasing, projected to reach billions in value by the forecast period.

- Market Concentration: Moderately fragmented with key global automakers.

- Innovation Catalysts: Advanced engine technology, biofuel efficiency, emission reduction.

- Regulatory Landscape: Crucial driver via biofuel mandates and emission standards.

- Substitute Products: EVs and traditional ICE vehicles.

- End-User Profiles: Environmentally conscious consumers, fleet operators, biofuel-producing regions.

- M&A Activity: Impactful in the broader automotive and biofuel sectors, with deal values in the hundreds of billions.

- Projected FFV Market Value: Billions by the forecast period.

Flex Fuel Vehicle Industry Evolution

The flex fuel vehicle (FFV) industry has witnessed significant evolution from its historical roots to its current position as a key player in the transition towards sustainable mobility. The study period, spanning from 2019 to 2033, with a base year of 2025, highlights a consistent upward trajectory in market growth. The historical period (2019–2024) saw steady, albeit sometimes modest, growth in FFV adoption, particularly in regions with established biofuel production and supportive government policies. As we enter the estimated year of 2025 and look towards the forecast period (2025–2033), the industry is poised for accelerated expansion. This growth is underpinned by a confluence of factors, including increasingly stringent emission regulations worldwide, a growing consumer preference for environmentally friendly transportation options, and advancements in ethanol fuel and engine technologies that enhance the performance and efficiency of FFVs.

Technological advancements have been pivotal in this evolution. Early FFVs primarily focused on accommodating E10 to E25 blends. However, innovations have enabled the widespread adoption of vehicles capable of utilizing higher ethanol concentrations, such as E25 to E85, and even E85 and above blends. This increased flexibility provides consumers with greater choice and allows for deeper integration with renewable energy sources. The development of sophisticated engine control units (ECUs), advanced fuel injection systems, and materials resistant to higher ethanol concentrations have been crucial. Furthermore, research and development efforts are continually focused on optimizing combustion processes to maximize the benefits of ethanol's higher octane rating, leading to improved power output and fuel economy when using higher blends.

Shifting consumer demands are also a major propellant. As awareness of climate change intensifies, consumers are actively seeking greener alternatives. FFVs, with their ability to run on renewable ethanol, are perceived as a more sustainable option compared to traditional gasoline-powered vehicles, especially in regions where ethanol is sourced from sustainable agricultural practices. This demand is further amplified by the economic advantages that can be realized through the use of lower-cost ethanol blends, making them an attractive choice for both individual car owners and large fleet operators in sectors like commercial vehicles. The inherent versatility of FFVs, allowing them to run on gasoline when ethanol is unavailable, also addresses range anxiety and infrastructure concerns, a key differentiator against some purely alternative fuel vehicles. The industry's ability to adapt to these evolving demands, coupled with ongoing technological innovation, has cemented the flex fuel car market and flex fuel truck market as integral components of the automotive future, contributing billions in market value and driving innovation across the entire automotive supply chain. The projected growth rates are expected to be in the low double digits annually throughout the forecast period, translating into billions in market expansion. Adoption metrics, currently in the millions of vehicles, are anticipated to see substantial increases.

Leading Regions, Countries, or Segments in Flex Fuel Vehicle

The global flex fuel vehicle (FFV) market exhibits distinct leadership across various geographical regions and vehicle segments, driven by a complex interplay of policy, infrastructure, and consumer preference. While global adoption is on the rise, certain areas and vehicle types stand out prominently.

The Passenger Car segment consistently dominates the FFV landscape. This is primarily due to the broad appeal of FFV technology to individual consumers seeking flexibility, environmental benefits, and potential cost savings. Automakers like General Motors, Ford Motor Company, and Toyota Motor Corporation have historically invested heavily in developing a wide range of passenger car models capable of utilizing various ethanol blends, from E10 to E25 and extending to E85 and above. This widespread availability and diverse model offerings within the passenger car category directly contribute to higher sales volumes and market penetration. Consumer awareness regarding the environmental advantages of ethanol blends, such as reduced greenhouse gas emissions, further fuels demand in this segment. Moreover, the established refueling infrastructure for gasoline also supports the adoption of FFVs, as they can seamlessly revert to gasoline if ethanol is not readily available. The market value generated by FFV passenger cars is expected to account for billions by the forecast period.

Conversely, the Commercial Vehicle segment, encompassing trucks and vans, presents a significant and growing opportunity. While historically lagging behind passenger cars in FFV adoption, the economic incentives associated with higher ethanol blends are increasingly attractive to commercial fleet operators. The potential for substantial cost savings on fuel, especially in regions with abundant and affordable ethanol production, can significantly impact operational budgets. Companies like Stellantis NV and Volkswagen AG are expanding their offerings in this space, recognizing the immense potential for volume sales and long-term fuel cost reduction. Regulatory pressures to reduce fleet emissions are also a key driver for commercial vehicle adoption of FFVs. Investment trends in this segment are shifting, with a growing focus on developing robust FFV powertrains capable of handling the demands of heavy-duty applications. Regulatory support, through fleet emission mandates and tax incentives for alternative fuel vehicles, is also crucial in accelerating the adoption of FFVs within the commercial sector, contributing billions in potential market value.

Regarding fuel type, the E25 to E85 blend range currently represents the most significant market share. This is due to a balance of factors: a substantial and growing supply of ethanol capable of supporting these blends in major production regions, coupled with vehicle technologies that reliably and efficiently utilize these concentrations. Automakers have optimized their engines to leverage the benefits of E85, including its higher octane rating, which can lead to improved performance. The widespread availability of E85 at select fueling stations in key markets like the United States further bolsters its popularity. While E85 and Above offers the greatest environmental and potential economic benefits, its adoption is somewhat constrained by the need for more widespread infrastructure and ongoing advancements in engine durability for extremely high ethanol concentrations. However, with continued innovation and investment, this segment is projected to see substantial growth throughout the forecast period, moving from hundreds of millions in current market value to billions. E10 to E25 remains a foundational segment, offering a readily accessible entry point for consumers and a stepping stone to higher blends.

- Dominant Application Segment: Passenger Car.

- Key Drivers: Broad consumer appeal, diverse model availability, environmental consciousness, existing refueling infrastructure.

- Market Value Contribution: Billions by the forecast period.

- Growing Application Segment: Commercial Vehicle.

- Key Drivers: Economic incentives for fleet operators, significant fuel cost savings potential, increasing fleet emission mandates.

- Investment Trends: Shifting towards robust FFV powertrains for heavy-duty applications.

- Regulatory Support: Fleet emission mandates, tax incentives.

- Dominant Fuel Type Segment: E25 to E85.

- Key Drivers: Balanced ethanol supply and demand, optimized engine technologies, widespread E85 availability in key markets.

- Emerging Fuel Type Segment: E85 and Above.

- Key Drivers: Greatest environmental and economic potential, ongoing infrastructure development and engine advancements.

- Projected Growth: Substantial throughout the forecast period.

- Foundational Fuel Type Segment: E10 to E25.

- Key Drivers: Readily accessible entry point, widespread compatibility.

Flex Fuel Vehicle Product Innovations

Recent product innovations in the flex fuel vehicle (FFV) market are significantly enhancing performance, efficiency, and consumer convenience. Automakers are introducing advanced engine management systems that intelligently adapt to varying ethanol blends, ensuring optimal combustion and emissions control. For instance, new FFV models from Hyundai Motor Company and Nissan Motor Company feature sophisticated sensor arrays that precisely detect ethanol content, allowing the engine control unit (ECU) to adjust ignition timing and fuel injection for maximum power and fuel economy. Subaru Corporation is also pushing boundaries with enhanced material science in its fuel systems, ensuring greater durability and compatibility with higher ethanol concentrations. These advancements not only improve the driving experience but also contribute to a reduction in the carbon footprint of these vehicles, aligning with growing consumer and regulatory demands for sustainable transportation solutions. The unique selling proposition lies in the unparalleled flexibility offered to consumers, bridging the gap between traditional internal combustion engines and the burgeoning electric vehicle market.

Propelling Factors for Flex Fuel Vehicle Growth

Several key factors are propelling the flex fuel vehicle (FFV) market forward. Technologically, advancements in engine management systems and material science are enabling greater compatibility and efficiency with higher ethanol blends. Economically, the fluctuating prices of gasoline and the often lower cost of ethanol, especially in major producing regions, make FFVs an attractive option for cost-conscious consumers and fleet operators. Regulatory influences are also paramount, with governments worldwide implementing stricter emission standards and promoting biofuel usage through mandates and incentives, thereby creating a favorable environment for FFV adoption. The existing fueling infrastructure for gasoline also provides a significant advantage, reducing the perceived risk for consumers compared to vehicles reliant on entirely new infrastructure.

Obstacles in the Flex Fuel Vehicle Market

Despite positive momentum, the flex fuel vehicle (FFV) market faces several obstacles. Regulatory challenges can arise from inconsistent or unpredictable biofuel mandates across different regions, creating uncertainty for manufacturers and consumers. Supply chain disruptions, particularly concerning the availability and pricing of ethanol, can impact the economic viability of FFVs. Competitive pressures from the rapidly advancing electric vehicle (EV) sector, which often receives significant government support and public attention, pose a substantial threat. Furthermore, consumer awareness and education regarding the benefits and operational nuances of FFVs remain a barrier, with some consumers still apprehensive about using higher ethanol blends. The perceived complexity of operating an FFV can also deter potential buyers, even with technological advancements.

Future Opportunities in Flex Fuel Vehicle

The future holds numerous opportunities for the flex fuel vehicle (FFV) market. Emerging opportunities include the development of FFVs specifically tailored for niche commercial applications, such as last-mile delivery vehicles, where fuel cost savings can be maximized. Technological advancements in biofuel production, such as cellulosic ethanol derived from agricultural waste, promise more sustainable and abundant fuel sources, further strengthening the FFV value proposition. The expansion of FFV availability into new geographical markets with growing biofuel production capabilities presents a significant growth avenue. Moreover, the integration of FFV technology with hybrid powertrains could offer a compelling blend of efficiency, performance, and reduced emissions, appealing to a broader consumer base.

Major Players in the Flex Fuel Vehicle Ecosystem

- General Motors

- Ford Motor Company

- Toyota Motor Corporation

- Stellantis NV

- Honda Motor Company

- Hyundai Motor Company

- Nissan Motor Company

- Subaru Corporation

- Volkswagen AG

- BMW AG

- Volvo Car Corporation

Key Developments in Flex Fuel Vehicle Industry

- 2023/08: Toyota Motor Corporation announces enhanced FFV technology for its upcoming SUV lineup, improving E85 compatibility and fuel efficiency.

- 2023/11: Ford Motor Company expands its E85-compatible vehicle offerings, targeting fleet customers with cost-saving initiatives.

- 2024/01: Stellantis NV outlines its strategy to increase FFV production in North America, focusing on popular truck and van models.

- 2024/03: Volkswagen AG introduces new engine technologies for its European market FFVs, enabling smoother transitions between gasoline and ethanol blends.

- 2024/05: Honda Motor Company invests in advanced biofuel research to support the future development of its FFV powertrains.

- 2024/07: Hyundai Motor Company showcases a concept FFV with a focus on advanced driver-assistance systems and sustainable interior materials.

- 2024/09: Nissan Motor Company announces partnerships with biofuel producers to secure stable ethanol supply for its FFV range.

- 2024/11: Subaru Corporation highlights its commitment to durable fuel systems for higher ethanol blends in its latest FFV models.

- 2025/01: BMW AG explores the integration of FFV technology into its premium segment vehicles, emphasizing performance and environmental responsibility.

- 2025/03: Volvo Car Corporation announces its intention to offer select FFV models in key emerging markets with strong biofuel production.

Strategic Flex Fuel Vehicle Market Forecast

The strategic forecast for the flex fuel vehicle (FFV) market is overwhelmingly positive, driven by a convergence of technological innovation, supportive government policies, and evolving consumer preferences for sustainable transportation. The continuous development of more efficient and robust ethanol-powered vehicles is set to unlock new market segments and further penetrate existing ones. With governments worldwide prioritizing emissions reduction and energy independence, the demand for vehicles capable of utilizing renewable fuels like ethanol will continue to surge, creating a multi-billion dollar market opportunity. The inherent flexibility of FFVs, coupled with their ability to leverage existing gasoline infrastructure, positions them as a crucial transitional technology, bridging the gap towards a fully decarbonized future and promising significant market growth and potential for stakeholders across the automotive and energy sectors.

Flex Fuel Vehicle Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. E10 to E25

- 2.2. E25 to E85

- 2.3. E85 and Above

Flex Fuel Vehicle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Flex Fuel Vehicle Regional Market Share

Geographic Coverage of Flex Fuel Vehicle

Flex Fuel Vehicle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. E10 to E25

- 5.2.2. E25 to E85

- 5.2.3. E85 and Above

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. E10 to E25

- 6.2.2. E25 to E85

- 6.2.3. E85 and Above

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. E10 to E25

- 7.2.2. E25 to E85

- 7.2.3. E85 and Above

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. E10 to E25

- 8.2.2. E25 to E85

- 8.2.3. E85 and Above

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. E10 to E25

- 9.2.2. E25 to E85

- 9.2.3. E85 and Above

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Flex Fuel Vehicle Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. E10 to E25

- 10.2.2. E25 to E85

- 10.2.3. E85 and Above

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 General Motors

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ford Motor Company

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Toyota Motor Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Stellantis NV

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Honda Motor Company

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hyundai Motor Company

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nissan Motor Company

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Subaru Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Volkswagen AG

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 BMW AG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Volvo Car Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 General Motors

List of Figures

- Figure 1: Global Flex Fuel Vehicle Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Flex Fuel Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Flex Fuel Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Flex Fuel Vehicle Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Flex Fuel Vehicle Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Flex Fuel Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Flex Fuel Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Flex Fuel Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Flex Fuel Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Flex Fuel Vehicle Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Flex Fuel Vehicle Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Flex Fuel Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Flex Fuel Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Flex Fuel Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Flex Fuel Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Flex Fuel Vehicle Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Flex Fuel Vehicle Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Flex Fuel Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Flex Fuel Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Flex Fuel Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Flex Fuel Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Flex Fuel Vehicle Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Flex Fuel Vehicle Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Flex Fuel Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Flex Fuel Vehicle Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Flex Fuel Vehicle Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Flex Fuel Vehicle Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Flex Fuel Vehicle Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Flex Fuel Vehicle Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Flex Fuel Vehicle Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Flex Fuel Vehicle Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Flex Fuel Vehicle Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Flex Fuel Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Flex Fuel Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Flex Fuel Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Flex Fuel Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Flex Fuel Vehicle Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Flex Fuel Vehicle Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Flex Fuel Vehicle Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Flex Fuel Vehicle Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flex Fuel Vehicle?

The projected CAGR is approximately 6.1%.

2. Which companies are prominent players in the Flex Fuel Vehicle?

Key companies in the market include General Motors, Ford Motor Company, Toyota Motor Corporation, Stellantis NV, Honda Motor Company, Hyundai Motor Company, Nissan Motor Company, Subaru Corporation, Volkswagen AG, BMW AG, Volvo Car Corporation.

3. What are the main segments of the Flex Fuel Vehicle?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flex Fuel Vehicle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flex Fuel Vehicle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flex Fuel Vehicle?

To stay informed about further developments, trends, and reports in the Flex Fuel Vehicle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence