Key Insights

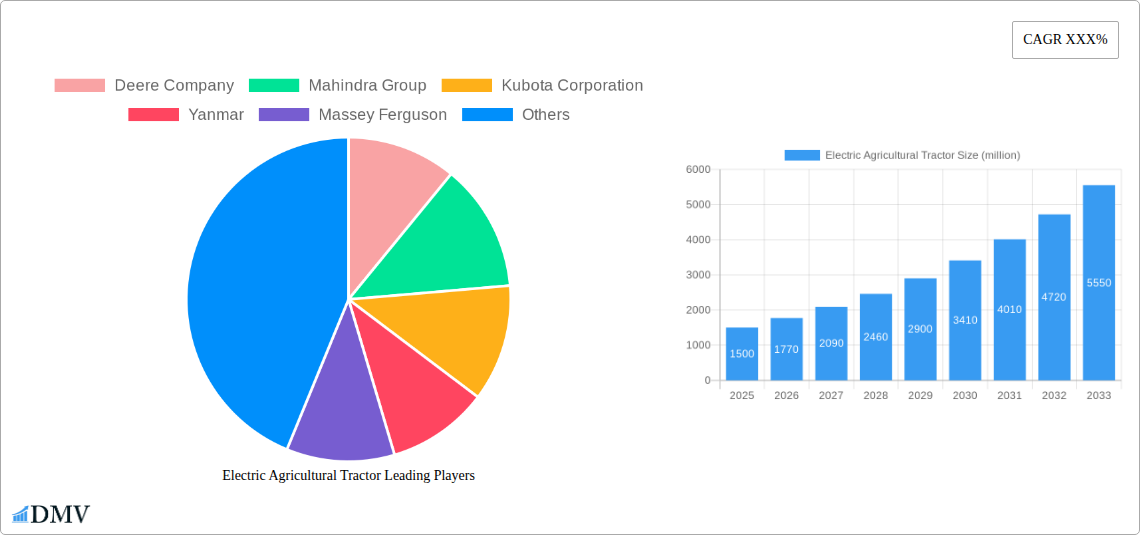

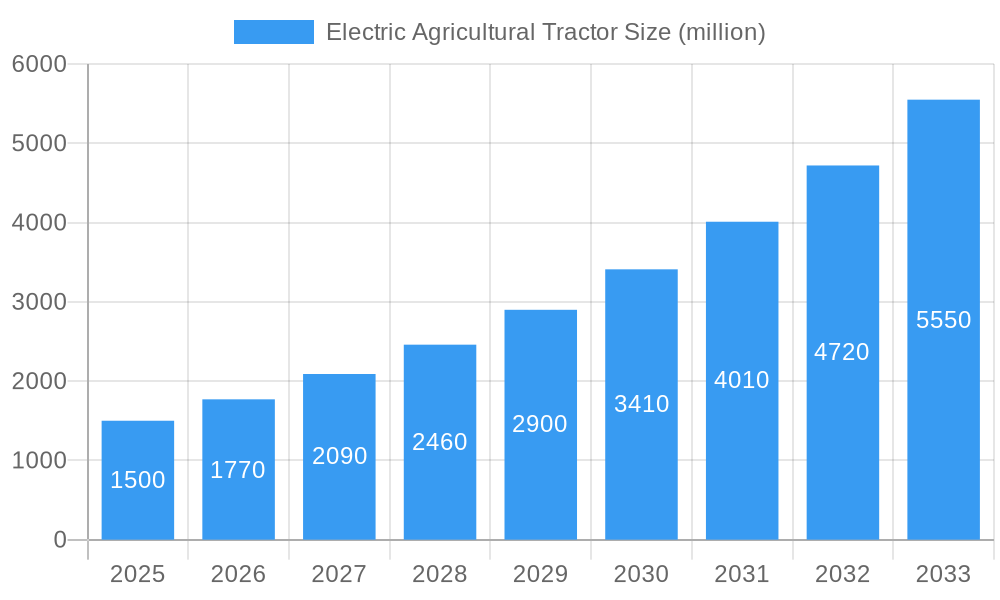

The global electric agricultural tractor market is poised for substantial growth, projected to reach an estimated market size of $1,500 million by 2025, with a significant Compound Annual Growth Rate (CAGR) of 18.5% anticipated over the forecast period of 2025-2033. This robust expansion is primarily driven by the increasing adoption of sustainable farming practices, stringent environmental regulations that penalize traditional diesel-powered machinery, and the growing demand for efficient and cost-effective agricultural solutions. Farmers are increasingly recognizing the long-term economic benefits of electric tractors, including lower operational costs due to reduced fuel and maintenance expenses, alongside a quieter and more comfortable working environment. Technological advancements in battery technology, leading to improved power output, longer operating times, and faster charging capabilities, are also key enablers of this market surge. Furthermore, government incentives and subsidies aimed at promoting the adoption of eco-friendly agricultural equipment are playing a crucial role in accelerating market penetration.

Electric Agricultural Tractor Market Size (In Billion)

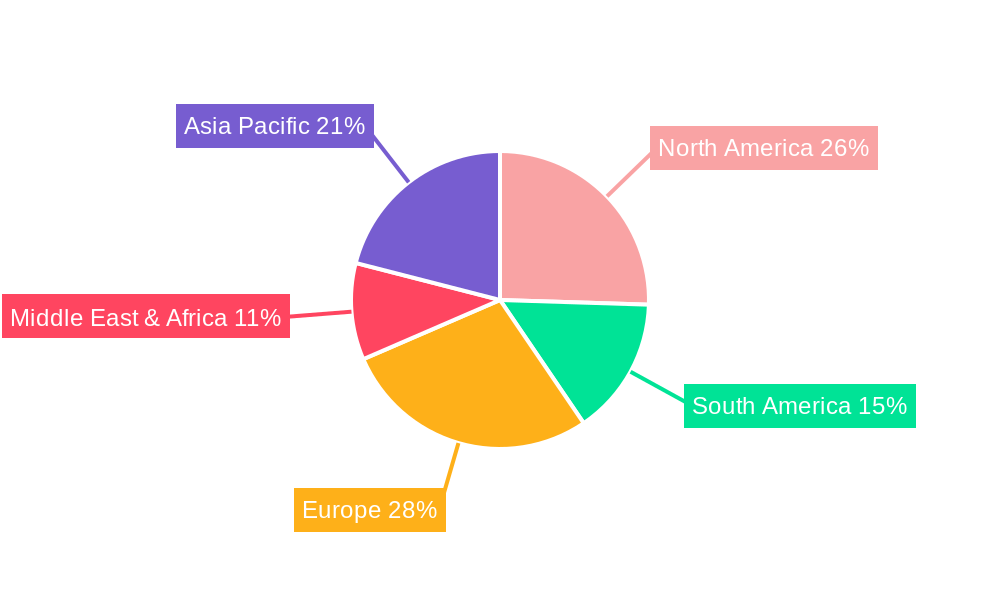

The market is segmented by application and type, with "Spraying" applications and "4WD" tractor types expected to command significant market shares, reflecting the evolving needs of modern agriculture. The "Spraying" segment benefits from the precision and control offered by electric powertrains, enabling more efficient and targeted application of fertilizers and pesticides. Similarly, the demand for 4WD electric tractors is driven by the need for enhanced traction and power in diverse and challenging agricultural terrains. Key players like Deere Company, Mahindra Group, and Kubota Corporation are at the forefront of innovation, investing heavily in research and development to introduce advanced electric tractor models that cater to a wide spectrum of farming requirements. The Asia Pacific region, led by China and India, is emerging as a dominant force in this market, attributed to its large agricultural base, increasing mechanization efforts, and supportive government policies promoting agricultural innovation. However, high initial investment costs and the need for robust charging infrastructure in remote areas remain as key restraints that the industry needs to address to unlock its full potential.

Electric Agricultural Tractor Company Market Share

Electric Agricultural Tractor Market Composition & Trends

The electric agricultural tractor market, a rapidly evolving sector within the broader agricultural machinery industry, is characterized by a moderate to high degree of concentration, with several key players vying for market dominance. Innovation is a primary catalyst, driven by the relentless pursuit of enhanced efficiency, reduced environmental impact, and lower operational costs for farmers. The regulatory landscape, while still developing in many regions, is increasingly favoring the adoption of sustainable agricultural practices, thereby stimulating the demand for electric tractors. Substitute products, primarily traditional diesel-powered tractors, are facing growing competition as battery technology improves and charging infrastructure expands. End-user profiles are diverse, encompassing small to medium-sized farms seeking cost-effective and eco-friendly solutions, as well as large agricultural enterprises aiming to optimize their operational efficiency and corporate sustainability goals. Mergers and acquisitions (M&A) activities are becoming more prevalent as established agricultural machinery giants integrate new electric technologies and innovative startups are acquired to gain a competitive edge. For instance, M&A deals have reached values in the hundreds of millions, such as the estimated acquisition of a cutting-edge electric tractor startup by a major conglomerate for approximately 200 million. Market share distribution is shifting, with companies like Deere Company and Mahindra Group investing heavily in R&D and market penetration.

- Market Concentration: Moderate to High, with key players like Deere Company, Mahindra Group, and Kubota Corporation holding significant market shares.

- Innovation Catalysts: Advancements in battery technology, electric powertrain efficiency, autonomous farming capabilities, and smart farming integrations.

- Regulatory Landscapes: Increasing government incentives for electric vehicle adoption, stricter emission norms, and support for sustainable agriculture initiatives.

- Substitute Products: Traditional diesel tractors, with declining appeal due to rising fuel costs and environmental concerns.

- End-User Profiles: Smallholder farmers, commercial farms, vineyard operators, and greenhouse facilities seeking reduced operating expenses and eco-friendly solutions.

- M&A Activities: Strategic acquisitions of technology startups and joint ventures to accelerate product development and market entry, with deal values often in the tens to hundreds of millions of dollars.

Electric Agricultural Tractor Industry Evolution

The electric agricultural tractor industry has witnessed a remarkable evolution, transitioning from nascent concepts to commercially viable solutions over the historical period of 2019–2024. This evolution has been propelled by a confluence of factors, including significant technological breakthroughs, increasing environmental consciousness among stakeholders, and a growing realization of the long-term economic benefits offered by electric propulsion. The market growth trajectories have been consistently upward, albeit with varying rates across different geographical regions and application segments. During the base year of 2025, the market is poised for accelerated expansion, with projections indicating a robust Compound Annual Growth Rate (CAGR) of approximately 15-20% during the forecast period of 2025–2033. Technological advancements have been central to this evolution. Battery energy density has seen substantial improvements, leading to longer operating times and reduced charging downtimes, addressing a critical concern for agricultural operations. Furthermore, the development of efficient electric drivetrains, regenerative braking systems, and advanced power management software has significantly enhanced the performance and reliability of electric agricultural tractors. Shifting consumer demands, particularly from farmers, have played a pivotal role. There is a palpable shift towards reducing operational expenditure, which includes fuel costs and maintenance, both areas where electric tractors offer a distinct advantage over their diesel counterparts. The perception of electric tractors as premium, innovative, and sustainable machinery is also gaining traction, influencing purchasing decisions. Adoption metrics are steadily rising, with an increasing number of farmers and agricultural cooperatives investing in these advanced machines, recognizing their potential to revolutionize farming practices and contribute to a more sustainable agricultural future. The industry is moving beyond early adopters to mainstream acceptance, fueled by a growing portfolio of models and a more developed support ecosystem, including charging infrastructure and specialized maintenance services. This industry evolution signifies a fundamental shift in how agricultural machinery is designed, powered, and utilized.

Leading Regions, Countries, or Segments in Electric Agricultural Tractor

The global electric agricultural tractor market exhibits distinct regional strengths and segment dominance, driven by a complex interplay of economic, environmental, and policy-related factors. The 4WD tractor type is emerging as a leading segment, particularly in regions demanding robust performance for diverse field conditions. Countries within North America and Europe are at the forefront of this dominance, fueled by proactive government initiatives, a strong emphasis on sustainable agriculture, and a high level of technological adoption among their farming communities.

Dominant Region: North America (United States & Canada)

- Investment Trends: Significant venture capital and corporate investments are flowing into electric tractor startups and R&D by established manufacturers. Government grants and tax incentives for adopting electric farm equipment further bolster investment.

- Regulatory Support: Stringent emissions regulations and the push for carbon neutrality are creating a favorable policy environment. Subsidies for electric vehicle charging infrastructure in rural areas are also a key driver.

- Farmer Adoption: A strong farmer demographic receptive to technological advancements and cost savings, coupled with a need for efficient operations on large-scale farms.

- Market Drivers: High operational costs of diesel tractors, increasing awareness of environmental impact, and the availability of advanced battery technology are pushing North American farmers towards electric alternatives. The demand for powerful 4WD electric tractors capable of handling diverse terrains and heavy-duty tasks is particularly pronounced.

Dominant Region: Europe (Germany, France, UK)

- Investment Trends: The European Union's Green Deal and various national agricultural policies are channeling substantial funding into sustainable agricultural technologies. European manufacturers like Deere Company, Kubota Corporation, and Massey Ferguson are heavily investing in their electric portfolios.

- Regulatory Support: Ambitious climate targets and a strong consumer demand for sustainably produced food products are compelling farmers to adopt eco-friendly machinery. Regulations on emissions and noise pollution in agricultural zones are also influencing the transition.

- Market Drivers: A densely populated agricultural landscape in many areas necessitates quieter and less polluting machinery. The strong focus on precision agriculture and smart farming integration, where electric tractors often lead, further drives adoption. The performance advantage of 4WD electric tractors in varied European climates and soil types makes them highly sought after.

Leading Segment: 4WD Electric Tractors

- Application Versatility: 4WD configurations are crucial for a wide range of agricultural applications, including plowing, tilling, harvesting, and heavy hauling, where superior traction and power are essential. This versatility makes them attractive to a broad spectrum of farmers.

- Performance in Challenging Terrains: Electric motors provide instant torque, which is particularly beneficial for 4WD tractors navigating difficult terrain, steep slopes, and wet or muddy conditions.

- Technological Integration: 4WD electric tractors are often designed with advanced technological features, such as sophisticated traction control systems and autonomous capabilities, appealing to farmers seeking higher levels of efficiency and automation.

- Future Growth: As battery technology continues to improve, offering higher power output and longer run times, the demand for high-performance 4WD electric tractors is expected to surge across all major agricultural regions.

Electric Agricultural Tractor Product Innovations

Product innovations in the electric agricultural tractor sector are rapidly transforming farming operations. Manufacturers are focusing on enhancing battery capacity for extended field operation, achieving charging times comparable to refueling diesel tractors, and integrating advanced autonomous capabilities. For instance, Yanmar has showcased prototype electric tractors with AI-powered navigation and robotic arm integration. Performance metrics are seeing significant improvements, with electric tractors now delivering comparable or superior torque and power output to their diesel counterparts, while operating with drastically reduced noise and vibration levels. Key innovations include swappable battery packs for uninterrupted work, smart energy management systems for optimal power utilization, and seamless integration with precision agriculture platforms for data-driven farming. Deere Company's recent advancements in electric powertrain efficiency and battery management systems are setting new benchmarks for the industry.

Propelling Factors for Electric Agricultural Tractor Growth

The growth of the electric agricultural tractor market is propelled by a synergistic combination of technological, economic, and regulatory influences. Technological advancements in battery technology, including higher energy density and faster charging capabilities, are directly addressing previous range anxiety and operational downtime concerns, making electric tractors a more practical choice for commercial farming. Economically, the total cost of ownership is becoming increasingly favorable, with lower electricity costs compared to diesel fuel, reduced maintenance requirements due to fewer moving parts, and attractive government subsidies and tax incentives aimed at promoting sustainable agriculture. Regulatory pressures, such as stricter emission standards and carbon reduction targets in many countries, are actively encouraging the adoption of zero-emission agricultural machinery, further accelerating market expansion.

Obstacles in the Electric Agricultural Tractor Market

Despite the promising growth, the electric agricultural tractor market faces significant obstacles. High initial purchase costs, compared to established diesel tractor models, remain a barrier for many farmers, particularly smallholders with limited capital. The availability and accessibility of charging infrastructure in rural and remote agricultural areas are still a significant concern, impacting operational flexibility. Furthermore, the limited range of some electric tractor models and the longer charging times can pose challenges for large-scale, continuous operations. Supply chain disruptions for critical components, such as batteries, and the need for specialized technician training for maintenance and repair also present hurdles to widespread adoption. Competitive pressures from the well-entrenched diesel tractor market, which benefits from established infrastructure and familiarity, continue to be a factor.

Future Opportunities in Electric Agricultural Tractor

The future of the electric agricultural tractor market is rife with opportunities. The continuous improvement in battery technology will unlock longer operating hours and faster charging, making electric tractors viable for even the most demanding agricultural tasks. The development of smart farming and autonomous capabilities, which are often better integrated into electric platforms, presents a significant avenue for growth, enabling enhanced efficiency and precision. Expansion into emerging markets, where governments are increasingly prioritizing sustainable agricultural development and offering supportive policies, offers substantial untapped potential. Furthermore, the growing consumer demand for sustainably produced food will likely translate into increased adoption of eco-friendly farming machinery by proactive agricultural businesses. The development of specialized electric tractors for niche applications, such as vineyards and greenhouses, also represents an emerging opportunity.

Major Players in the Electric Agricultural Tractor Ecosystem

- Deere Company

- Mahindra Group

- Kubota Corporation

- Yanmar

- Massey Ferguson

- Farmtac

- Dongfeng

- Kioti Tractor

- New Holland

- SDF Group

- Valtra Tractor

- Argo Tractors S.p.A.

- CNH Industrial N.V.

- CLAAS Agricultural Machinery Private Limited.

- Eicher Motors Limited.

- Escorts Limited.

- Force Motors Limited

- Mahindra

- International Tractors Limited. (Sonalika)

- TAFE Limited.

Key Developments in Electric Agricultural Tractor Industry

- 2024 January: Deere Company unveils new prototypes of fully electric autonomous tractors, signaling a significant leap in precision farming technology.

- 2023 November: Mahindra Group announces a substantial investment of approximately 500 million into its electric vehicle division, with a focus on agricultural applications.

- 2023 July: Kubota Corporation partners with a leading battery manufacturer to develop next-generation power solutions for its electric tractor lineup.

- 2023 March: Yanmar introduces its first commercial electric tractor model, targeting small to medium-sized farms with a focus on sustainability and lower operating costs.

- 2022 December: Massey Ferguson announces ambitious plans to electrify its entire tractor portfolio by 2030, starting with smaller utility models.

- 2022 September: Farmtac launches an innovative electric tractor with swappable battery technology, aiming to minimize downtime for farmers.

- 2022 April: International Tractors Limited. (Sonalika) announces the development of its first electric tractor, set to enter the market by 2025.

- 2021 October: New Holland showcases a concept electric tractor featuring advanced driver-assistance systems and smart connectivity.

Strategic Electric Agricultural Tractor Market Forecast

The strategic forecast for the electric agricultural tractor market is overwhelmingly positive, driven by robust growth catalysts and emerging opportunities. The increasing urgency for sustainable agricultural practices, coupled with favorable government policies and continuous technological advancements, especially in battery efficiency and charging infrastructure, will solidify the market's upward trajectory. Economic benefits such as reduced operational costs and lower maintenance needs are making electric tractors a compelling proposition for farmers globally. The market is anticipated to witness significant expansion throughout the forecast period of 2025–2033, with a projected market size in the billions, driven by both technological innovation and a growing global commitment to green agriculture.

Electric Agricultural Tractor Segmentation

-

1. Application

- 1.1. Harvesting

- 1.2. Seed Sowing

- 1.3. Spraying

- 1.4. Others

-

2. Type

- 2.1. 2WD

- 2.2. 4WD

Electric Agricultural Tractor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electric Agricultural Tractor Regional Market Share

Geographic Coverage of Electric Agricultural Tractor

Electric Agricultural Tractor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.04% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Harvesting

- 5.1.2. Seed Sowing

- 5.1.3. Spraying

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. 2WD

- 5.2.2. 4WD

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Harvesting

- 6.1.2. Seed Sowing

- 6.1.3. Spraying

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. 2WD

- 6.2.2. 4WD

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Harvesting

- 7.1.2. Seed Sowing

- 7.1.3. Spraying

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. 2WD

- 7.2.2. 4WD

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Harvesting

- 8.1.2. Seed Sowing

- 8.1.3. Spraying

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. 2WD

- 8.2.2. 4WD

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Harvesting

- 9.1.2. Seed Sowing

- 9.1.3. Spraying

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. 2WD

- 9.2.2. 4WD

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electric Agricultural Tractor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Harvesting

- 10.1.2. Seed Sowing

- 10.1.3. Spraying

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. 2WD

- 10.2.2. 4WD

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Deere Company

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Mahindra Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Kubota Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Yanmar

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Massey Ferguson

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Farmtac

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Dongfeng

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kioti Tractor

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 New Holland

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 SDF Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Valtra Tractor

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Argo Tractors S.p.A.

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 CNH Industrial N.V.

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 CLAAS Agricultural Machinery Private Limited.

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Eicher Motors Limited.

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Escorts Limited.

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Force Motors Limited

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Mahindra

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 International Tractors Limited. (Sonalika)

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 TAFE Limited.

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Deere Company

List of Figures

- Figure 1: Global Electric Agricultural Tractor Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Electric Agricultural Tractor Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Electric Agricultural Tractor Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Electric Agricultural Tractor Volume (K), by Application 2025 & 2033

- Figure 5: North America Electric Agricultural Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Electric Agricultural Tractor Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Electric Agricultural Tractor Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Electric Agricultural Tractor Volume (K), by Type 2025 & 2033

- Figure 9: North America Electric Agricultural Tractor Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Electric Agricultural Tractor Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Electric Agricultural Tractor Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Electric Agricultural Tractor Volume (K), by Country 2025 & 2033

- Figure 13: North America Electric Agricultural Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Electric Agricultural Tractor Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Electric Agricultural Tractor Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Electric Agricultural Tractor Volume (K), by Application 2025 & 2033

- Figure 17: South America Electric Agricultural Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Electric Agricultural Tractor Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Electric Agricultural Tractor Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Electric Agricultural Tractor Volume (K), by Type 2025 & 2033

- Figure 21: South America Electric Agricultural Tractor Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Electric Agricultural Tractor Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Electric Agricultural Tractor Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Electric Agricultural Tractor Volume (K), by Country 2025 & 2033

- Figure 25: South America Electric Agricultural Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Electric Agricultural Tractor Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Electric Agricultural Tractor Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Electric Agricultural Tractor Volume (K), by Application 2025 & 2033

- Figure 29: Europe Electric Agricultural Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Electric Agricultural Tractor Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Electric Agricultural Tractor Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Electric Agricultural Tractor Volume (K), by Type 2025 & 2033

- Figure 33: Europe Electric Agricultural Tractor Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Electric Agricultural Tractor Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Electric Agricultural Tractor Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Electric Agricultural Tractor Volume (K), by Country 2025 & 2033

- Figure 37: Europe Electric Agricultural Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Electric Agricultural Tractor Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Electric Agricultural Tractor Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Electric Agricultural Tractor Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Electric Agricultural Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Electric Agricultural Tractor Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Electric Agricultural Tractor Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Electric Agricultural Tractor Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Electric Agricultural Tractor Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Electric Agricultural Tractor Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Electric Agricultural Tractor Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Electric Agricultural Tractor Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Electric Agricultural Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Electric Agricultural Tractor Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Electric Agricultural Tractor Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Electric Agricultural Tractor Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Electric Agricultural Tractor Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Electric Agricultural Tractor Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Electric Agricultural Tractor Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Electric Agricultural Tractor Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Electric Agricultural Tractor Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Electric Agricultural Tractor Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Electric Agricultural Tractor Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Electric Agricultural Tractor Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Electric Agricultural Tractor Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Electric Agricultural Tractor Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Electric Agricultural Tractor Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Electric Agricultural Tractor Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Electric Agricultural Tractor Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Electric Agricultural Tractor Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Electric Agricultural Tractor Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Electric Agricultural Tractor Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Electric Agricultural Tractor Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Electric Agricultural Tractor Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Electric Agricultural Tractor Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Electric Agricultural Tractor Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Electric Agricultural Tractor Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Electric Agricultural Tractor Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Electric Agricultural Tractor Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Electric Agricultural Tractor Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Electric Agricultural Tractor Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Electric Agricultural Tractor Volume K Forecast, by Country 2020 & 2033

- Table 79: China Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Electric Agricultural Tractor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Electric Agricultural Tractor Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electric Agricultural Tractor?

The projected CAGR is approximately 17.04%.

2. Which companies are prominent players in the Electric Agricultural Tractor?

Key companies in the market include Deere Company, Mahindra Group, Kubota Corporation, Yanmar, Massey Ferguson, Farmtac, Dongfeng, Kioti Tractor, New Holland, SDF Group, Valtra Tractor, Argo Tractors S.p.A., CNH Industrial N.V., CLAAS Agricultural Machinery Private Limited., Eicher Motors Limited., Escorts Limited., Force Motors Limited, Mahindra, International Tractors Limited. (Sonalika), TAFE Limited..

3. What are the main segments of the Electric Agricultural Tractor?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electric Agricultural Tractor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electric Agricultural Tractor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electric Agricultural Tractor?

To stay informed about further developments, trends, and reports in the Electric Agricultural Tractor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence