Key Insights

The global commercial aircraft aerostructure market is poised for significant expansion, projected to reach approximately $65 billion by 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of around 7.5% through 2033. This impressive trajectory is primarily fueled by the burgeoning demand for air travel, especially in emerging economies, leading to increased aircraft production and replacement cycles. The "Passenger Transport" segment, by far the largest, will continue to dominate, driven by airlines investing in larger and more fuel-efficient fleets to cater to growing passenger volumes. Furthermore, the expanding global logistics and e-commerce sectors are also contributing to the growth of the "Freight" segment, necessitating the development and production of specialized cargo aircraft and aerostructures. Advancements in materials science, particularly the increasing adoption of lightweight and high-strength composites alongside traditional metals and alloys, are enabling manufacturers to produce more fuel-efficient, durable, and cost-effective aerostructures, further propelling market growth.

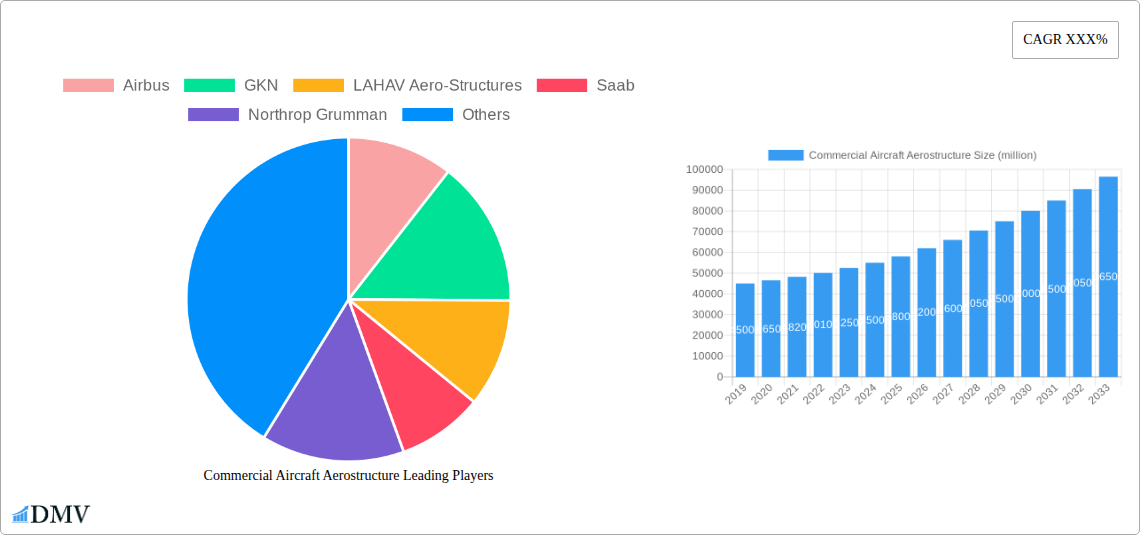

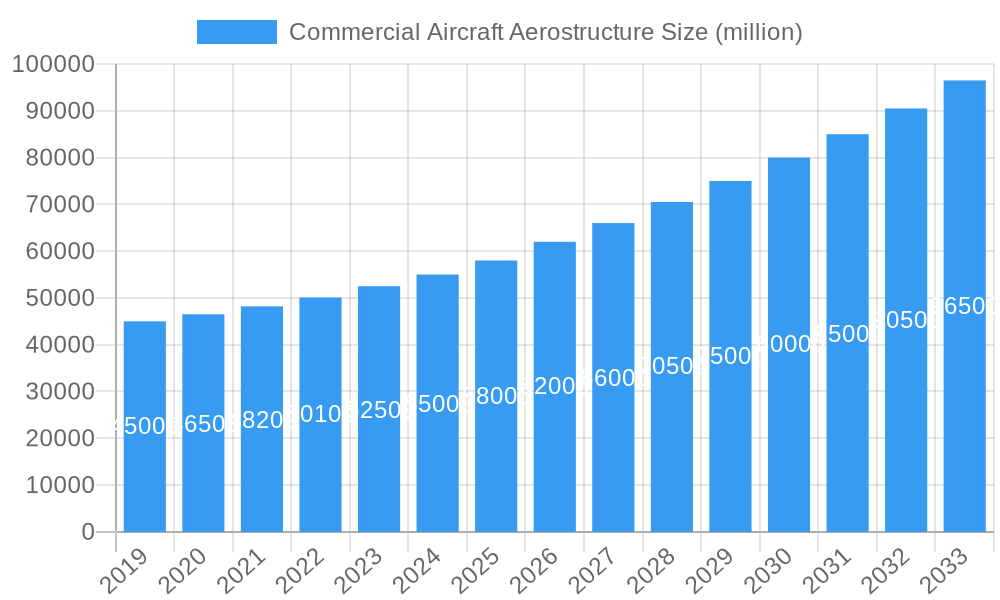

Commercial Aircraft Aerostructure Market Size (In Billion)

The market's expansion is strategically underpinned by key drivers such as the continuous innovation in aircraft design, the need for enhanced fuel efficiency to meet stringent environmental regulations, and the ongoing modernization of aging aircraft fleets worldwide. However, the industry also faces certain restraints, including the high capital investment required for manufacturing advanced aerostructures, potential supply chain disruptions, and geopolitical uncertainties that can impact global aviation demand. Despite these challenges, the market is characterized by intense competition among leading players like Airbus, Boeing, Spirit AeroSystems, and GKN, who are actively engaged in research and development to gain a competitive edge. Strategic collaborations, mergers, and acquisitions are also shaping the competitive landscape, as companies aim to consolidate their market position and expand their technological capabilities across diverse regions, with Asia Pacific and North America expected to be the leading growth regions.

Commercial Aircraft Aerostructure Company Market Share

This in-depth report provides a critical analysis of the global Commercial Aircraft Aerostructure Market, spanning from the historical period of 2019–2024, with a base year of 2025 and an extensive forecast period extending to 2033. Delve into the intricate composition, evolving trends, and strategic landscape of this vital sector. We examine market concentration, innovation catalysts, and the impact of regulatory frameworks on key players such as Airbus, Boeing, Spirit AeroSystems, GKN, and Northrop Grumman. Discover how advancements in composite aerostructures and novel metal alloys are reshaping aircraft design, driving efficiency, and catering to the burgeoning demand in passenger transport and freight applications. This report quantifies market share distribution, identifies key M&A activities with deal values reaching hundreds of millions, and assesses the influence of substitute products and end-user profiles. Understanding these dynamics is crucial for stakeholders navigating the competitive and technologically driven commercial aerospace industry.

Commercial Aircraft Aerostructure Market Composition & Trends

The Commercial Aircraft Aerostructure Market exhibits a moderately concentrated landscape, with key players like Boeing, Airbus, and Spirit AeroSystems holding significant market share, estimated at over 60% combined. Innovation is primarily driven by the pursuit of lightweight materials and enhanced aerodynamic efficiency. Advancements in carbon fiber composites and advanced aluminum alloys are paramount, leading to substantial fuel savings and reduced environmental impact. Regulatory landscapes, particularly those enforced by EASA and the FAA, are increasingly focused on safety, sustainability, and emissions reduction, directly influencing material choices and manufacturing processes. Substitute products, though limited in this highly specialized field, include advancements in engine technology and airframe modifications that can marginally offset the need for entirely new aerostructure designs. End-user profiles are predominantly comprised of major airlines and cargo operators, whose fleet expansion and modernization plans are direct indicators of market demand. Mergers and acquisitions are a consistent feature, with deals often valued in the hundreds of millions, aimed at consolidating expertise, expanding manufacturing capabilities, and securing supply chains. For instance, GKN's acquisition of Fokker Technologies for approximately $800 million significantly bolstered its composite aerostructure offerings. Strategic partnerships and joint ventures also play a crucial role in distributing R&D burdens and accessing specialized technologies, particularly within the metals and alloys segment. The continuous drive for fuel efficiency and passenger comfort fuels investment in next-generation aerostructures, positioning companies like Leonardo and Aernnova at the forefront of material science and structural integrity. The market is characterized by a persistent demand for cost-effectiveness and performance, driving a delicate balance between material innovation and manufacturing scalability.

Commercial Aircraft Aerostructure Industry Evolution

The Commercial Aircraft Aerostructure Industry has witnessed remarkable evolution, driven by a confluence of technological innovation, shifting market demands, and the ever-present imperative for enhanced aviation efficiency and sustainability. Over the study period (2019–2033), the market has experienced robust growth trajectories, with an average annual growth rate (AAGR) projected at 5.2% during the forecast period. This growth is intrinsically linked to the increasing global demand for air travel and cargo transport, necessitating the expansion and modernization of airline fleets. Key technological advancements, particularly in the realm of advanced composites and lightweight metals, have been transformative. The adoption of carbon fiber reinforced polymers (CFRPs) has surged, now comprising an estimated 50% of modern aircraft primary structures, significantly reducing aircraft weight and, consequently, fuel consumption by up to 20%. This shift from traditional aluminum alloys to composites is a defining characteristic of the industry's evolution. Furthermore, advancements in additive manufacturing (3D printing) are beginning to revolutionize the production of complex aerostructure components, offering greater design freedom and reducing material waste.

Shifting consumer demands, primarily driven by environmental concerns and the desire for improved passenger experience, also play a pivotal role. Airlines are increasingly prioritizing fuel-efficient aircraft, which directly translates into a demand for lighter and more aerodynamically optimized aerostructures. This has spurred significant investment in research and development for next-generation materials and manufacturing techniques. The focus on sustainability extends to the entire lifecycle of aerostructures, from material sourcing and manufacturing processes to end-of-life recycling. The Passenger Transport segment, historically the largest, continues to be a primary driver, fueled by a growing middle class in emerging economies and a resurgence in global tourism. The Freight segment is also experiencing substantial growth, propelled by the boom in e-commerce and global supply chain optimization. The development of larger and more efficient cargo aircraft, such as Boeing's Dreamlifter and Airbus' BelugaXL, highlights the evolving needs of the logistics industry and the critical role of aerostructures in enabling these capabilities.

The industry's evolution is also marked by increased collaboration and strategic alliances between aerostructure manufacturers and aircraft OEMs. Companies like Spirit AeroSystems, a major supplier to Boeing, and Latécoère, a key partner for Airbus, exemplify the intricate supply chain dynamics. The constant drive for cost reduction, without compromising safety or performance, has led to the adoption of advanced manufacturing processes, automation, and lean manufacturing principles. The metals segment, while still significant, is seeing a gradual shift towards higher-strength alloys and innovative forming techniques to maintain competitiveness against composites. The integration of smart materials and sensors within aerostructures for real-time structural health monitoring is another emerging trend, promising enhanced safety and predictive maintenance capabilities, further underscoring the industry's dynamic and forward-looking nature. The commercial aircraft aerostructure market size is projected to reach approximately $120 billion by 2025, with a sustained upward trend driven by these multifaceted evolutionary forces.

Leading Regions, Countries, or Segments in Commercial Aircraft Aerostructure

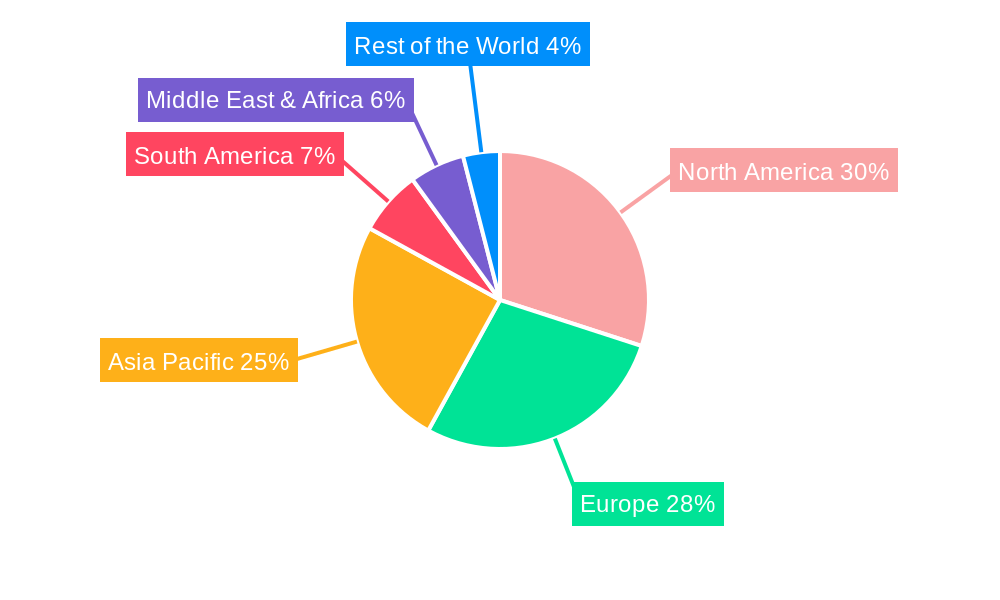

The Commercial Aircraft Aerostructure Market is characterized by a clear dominance in specific regions and segments, driven by a complex interplay of factors including established aerospace manufacturing infrastructure, government support, and the presence of major aircraft manufacturers.

Dominant Region: North America

North America, particularly the United States, stands as the leading region in the global commercial aircraft aerostructure market. This dominance is underpinned by several key drivers:

- Presence of Major OEMs: The United States is home to two of the world's largest commercial aircraft manufacturers, Boeing, with significant aerostructure production facilities in regions like Washington and South Carolina. This proximity naturally fuels a vast demand for aerostructures.

- Advanced Manufacturing Capabilities: The region boasts highly sophisticated manufacturing capabilities, with a strong emphasis on advanced materials, automation, and stringent quality control processes. Companies like Northrop Grumman and Spirit AeroSystems are at the forefront of this technological prowess.

- Robust R&D Investment: Significant investment in research and development for next-generation aerostructures, particularly in composites and high-performance alloys, further solidifies North America's leadership. This includes ongoing exploration into novel applications of metals for critical structural components.

- Skilled Workforce: The presence of a highly skilled and experienced aerospace workforce is crucial for designing, manufacturing, and testing complex aerostructures.

Dominant Segment: Passenger Transport Application

Within the application segments, Passenger Transport continues to be the largest and most influential driver of the commercial aircraft aerostructure market.

- Fleet Expansion and Modernization: The consistent global demand for air travel, driven by economic growth and rising disposable incomes, necessitates continuous fleet expansion and the replacement of older, less fuel-efficient aircraft. This directly translates into a sustained demand for new aerostructures.

- Demand for Fuel Efficiency: Airlines are under immense pressure to reduce operational costs, with fuel being a significant expenditure. This drives a strong preference for aircraft utilizing lightweight aerostructures, predominantly made from advanced composites and high-strength metals.

- New Aircraft Programs: The introduction of new aircraft models, such as Boeing's 737 MAX and Airbus' A320neo family, which feature significant proportions of composite aerostructures, further amplifies demand in this segment.

- Passenger Comfort and Experience: Modern aircraft designs, incorporating advanced aerostructures, also contribute to enhanced passenger comfort through quieter cabins and more spacious interiors.

Key Drivers within Segments:

- Application: Passenger Transport: Investment trends in new aircraft orders from major airlines, such as United Airlines and Delta Air Lines, are direct indicators of market growth. Regulatory support for cleaner aviation technologies incentivizes the adoption of fuel-efficient aerostructures.

- Type: Composites: Technological advancements in resin systems and fiber manufacturing are enabling the creation of stronger, lighter, and more cost-effective composite aerostructures. The adoption rate of composite materials in new aircraft designs is a critical performance metric.

- Type: Alloys: The continuous development of advanced aluminum-lithium alloys and titanium alloys offers improved strength-to-weight ratios and corrosion resistance, maintaining their relevance for specific aerostructure components. Investment in novel forging and casting techniques for these alloys is a key trend.

- Type: Metals: While composites are gaining traction, specialized metals continue to be vital for high-stress areas and specific components. Innovations in metal processing and joining techniques are crucial for maintaining competitiveness.

The freight segment is also experiencing significant growth, driven by e-commerce and global logistics demands. The development of dedicated cargo aircraft and freighter conversions of passenger jets contribute to the increasing demand for aerostructures in this sector. However, the sheer volume of passenger aircraft production and demand ensures that Passenger Transport remains the dominant application segment for the foreseeable future.

Commercial Aircraft Aerostructure Product Innovations

The Commercial Aircraft Aerostructure Market is a hotbed of innovation, with a relentless focus on material science and design optimization. Significant advancements in carbon fiber composites, particularly through nanotechnology integration and advanced resin systems, have led to aerostructures that are up to 30% lighter and significantly stronger than traditional aluminum counterparts. These innovations, seen in components like wing skins and fuselage sections, offer improved fuel efficiency, reduced maintenance, and enhanced aerodynamic performance. The development of self-healing composites and smart aerostructures embedded with sensors for real-time structural health monitoring represents a paradigm shift, promising unprecedented safety and operational efficiency. Furthermore, advancements in advanced metal alloys, including novel aluminum-lithium variants and high-strength titanium, are enabling the creation of more durable and heat-resistant components for critical areas. The unique selling proposition of these innovations lies in their ability to directly translate into substantial operational cost savings for airlines and a reduced environmental footprint for the aviation industry.

Propelling Factors for Commercial Aircraft Aerostructure Growth

The Commercial Aircraft Aerostructure Market is propelled by several critical factors. Firstly, the escalating global demand for air travel and cargo, driven by economic growth and e-commerce, necessitates the expansion and modernization of aircraft fleets. Secondly, a paramount focus on fuel efficiency and emission reduction, mandated by increasingly stringent environmental regulations, drives the adoption of lightweight materials like advanced composites and high-strength alloys. Technological advancements in material science and manufacturing processes, such as additive manufacturing, are enabling the creation of more efficient and cost-effective aerostructures. Finally, substantial investments in research and development by major aerospace players like Airbus and Boeing are continuously pushing the boundaries of what is possible in aerostructure design and functionality.

Obstacles in the Commercial Aircraft Aerostructure Market

Despite robust growth, the Commercial Aircraft Aerostructure Market faces significant obstacles. Regulatory hurdles and lengthy certification processes for new materials and designs can impede innovation speed. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, pose a constant threat to production timelines and cost-effectiveness. Intense competition among established players like Spirit AeroSystems and emerging manufacturers, coupled with the high capital investment required for advanced manufacturing facilities, creates significant pricing pressures. Furthermore, the skilled labor shortage in specialized manufacturing fields can impact production capacity. The reliance on a limited number of key suppliers for critical raw materials, such as specialized carbon fibers and titanium, also presents a vulnerability, with potential impacts on production schedules and material costs reaching hundreds of millions in disruption.

Future Opportunities in Commercial Aircraft Aerostructure

Emerging opportunities in the Commercial Aircraft Aerostructure Market are vast and transformative. The growing demand for sustainable aviation fuels (SAFs) and the push towards electric and hybrid-electric aircraft will spur innovation in lightweight, durable aerostructures capable of accommodating new propulsion systems. The expansion of the freight segment, driven by e-commerce, presents a significant opportunity for the development of specialized cargo aerostructures. Advancements in digital manufacturing, including AI-driven design optimization and advanced robotics, will unlock new levels of efficiency and customization. Furthermore, the increasing focus on urban air mobility (UAM) and regional jet development will create new markets for smaller, highly efficient aerostructures. The development of bio-composites and advanced recycling techniques for aerostructures also presents a significant sustainability-focused opportunity, with potential for circular economy integration.

Major Players in the Commercial Aircraft Aerostructure Ecosystem

- Airbus

- GKN

- LAHAV Aero-Structures

- Saab

- Northrop Grumman

- ST Engineering

- Daher

- Aernnova

- Leonardo

- Boeing

- Latécoère

- AKKA

- MITSUBISHI HEAVY INDUSTRIES

- Spirit AeroSystems

Key Developments in Commercial Aircraft Aerostructure Industry

- 2023: Airbus and Boeing announce significant investments in advanced composite research, aiming to increase the proportion of composites in future aircraft to over 70%.

- 2023: Spirit AeroSystems expands its additive manufacturing capabilities, securing contracts for 3D-printed metallic components worth approximately $50 million.

- 2022: GKN Aerospace demonstrates a new generation of lightweight composite wing structures with integrated sensors, enhancing structural health monitoring capabilities.

- 2022: Leonardo invests $150 million in a new facility dedicated to the production of advanced aerostructures for next-generation regional jets.

- 2021: Northrop Grumman secures a multi-year contract valued at over $500 million for the supply of advanced aerostructures to a leading commercial aircraft OEM.

- 2020: Aernnova inaugurates a new R&D center focused on sustainable aerostructure materials and manufacturing processes.

- 2019: Latécoère announces a strategic partnership with a battery technology firm to explore aerostructure designs for electric aircraft.

Strategic Commercial Aircraft Aerostructure Market Forecast

The Commercial Aircraft Aerostructure Market is poised for sustained growth, driven by innovation in composites and advanced alloys, coupled with an insatiable global demand for air travel and efficient cargo transport. Strategic investments in R&D for lightweight materials, sustainable manufacturing, and digital technologies will be paramount. The increasing emphasis on environmental regulations will continue to fuel the adoption of fuel-efficient aerostructures, particularly in the Passenger Transport segment. Opportunities in emerging markets and the burgeoning freight sector, alongside advancements in urban air mobility, will further diversify and expand the market's potential. The successful navigation of supply chain complexities and the cultivation of a skilled workforce will be critical for capitalizing on the projected market expansion.

Commercial Aircraft Aerostructure Segmentation

-

1. Application

- 1.1. Passenger Transport

- 1.2. Freight

-

2. Type

- 2.1. Alloys

- 2.2. Composites

- 2.3. Metals

Commercial Aircraft Aerostructure Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Commercial Aircraft Aerostructure Regional Market Share

Geographic Coverage of Commercial Aircraft Aerostructure

Commercial Aircraft Aerostructure REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Transport

- 5.1.2. Freight

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Alloys

- 5.2.2. Composites

- 5.2.3. Metals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Transport

- 6.1.2. Freight

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Alloys

- 6.2.2. Composites

- 6.2.3. Metals

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Transport

- 7.1.2. Freight

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Alloys

- 7.2.2. Composites

- 7.2.3. Metals

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Transport

- 8.1.2. Freight

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Alloys

- 8.2.2. Composites

- 8.2.3. Metals

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Transport

- 9.1.2. Freight

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Alloys

- 9.2.2. Composites

- 9.2.3. Metals

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Commercial Aircraft Aerostructure Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Transport

- 10.1.2. Freight

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Alloys

- 10.2.2. Composites

- 10.2.3. Metals

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Airbus

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GKN

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 LAHAV Aero-Structures

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Saab

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Northrop Grumman

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ST Engineering

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Daher

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aernnova

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Leonardo

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Boeing

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Latécoère

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 AKKA

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 MITSUBISHI HEAVY INDUSTRIES

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Spirit AeroSystems

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Airbus

List of Figures

- Figure 1: Global Commercial Aircraft Aerostructure Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Commercial Aircraft Aerostructure Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Commercial Aircraft Aerostructure Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Commercial Aircraft Aerostructure Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Commercial Aircraft Aerostructure Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Commercial Aircraft Aerostructure Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Commercial Aircraft Aerostructure Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Commercial Aircraft Aerostructure Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Commercial Aircraft Aerostructure Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Commercial Aircraft Aerostructure Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Commercial Aircraft Aerostructure Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Commercial Aircraft Aerostructure Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Commercial Aircraft Aerostructure Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Commercial Aircraft Aerostructure Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Commercial Aircraft Aerostructure Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Commercial Aircraft Aerostructure Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Commercial Aircraft Aerostructure Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Commercial Aircraft Aerostructure Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Commercial Aircraft Aerostructure Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Commercial Aircraft Aerostructure Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Commercial Aircraft Aerostructure Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Commercial Aircraft Aerostructure Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Commercial Aircraft Aerostructure Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Commercial Aircraft Aerostructure Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Commercial Aircraft Aerostructure Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Commercial Aircraft Aerostructure Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Commercial Aircraft Aerostructure Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Commercial Aircraft Aerostructure Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Commercial Aircraft Aerostructure Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Commercial Aircraft Aerostructure Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Commercial Aircraft Aerostructure Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Commercial Aircraft Aerostructure Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Commercial Aircraft Aerostructure Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Commercial Aircraft Aerostructure?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Commercial Aircraft Aerostructure?

Key companies in the market include Airbus, GKN, LAHAV Aero-Structures, Saab, Northrop Grumman, ST Engineering, Daher, Aernnova, Leonardo, Boeing, Latécoère, AKKA, MITSUBISHI HEAVY INDUSTRIES, Spirit AeroSystems.

3. What are the main segments of the Commercial Aircraft Aerostructure?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Commercial Aircraft Aerostructure," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Commercial Aircraft Aerostructure report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Commercial Aircraft Aerostructure?

To stay informed about further developments, trends, and reports in the Commercial Aircraft Aerostructure, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence