Key Insights

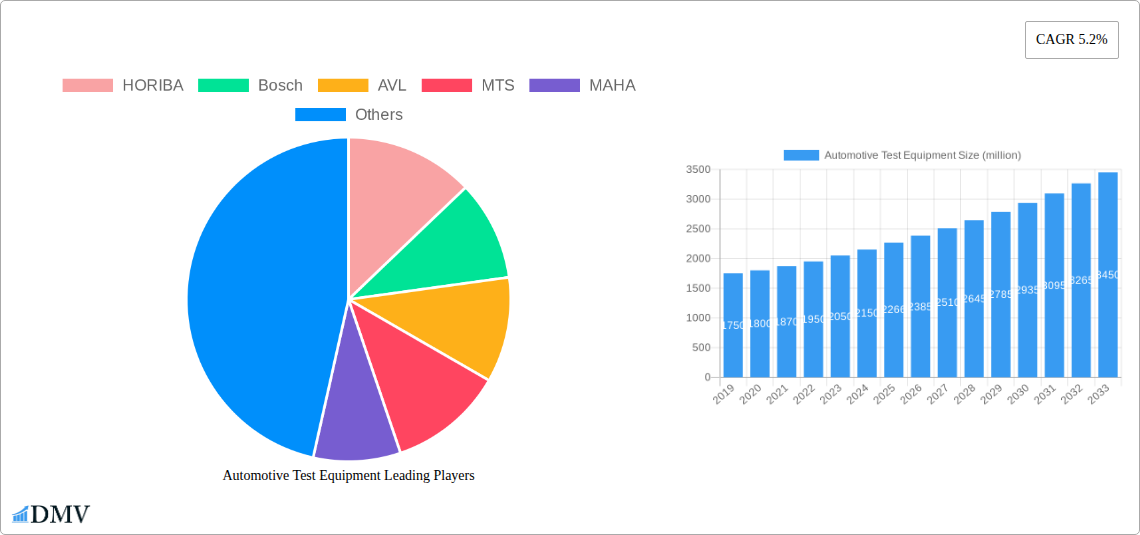

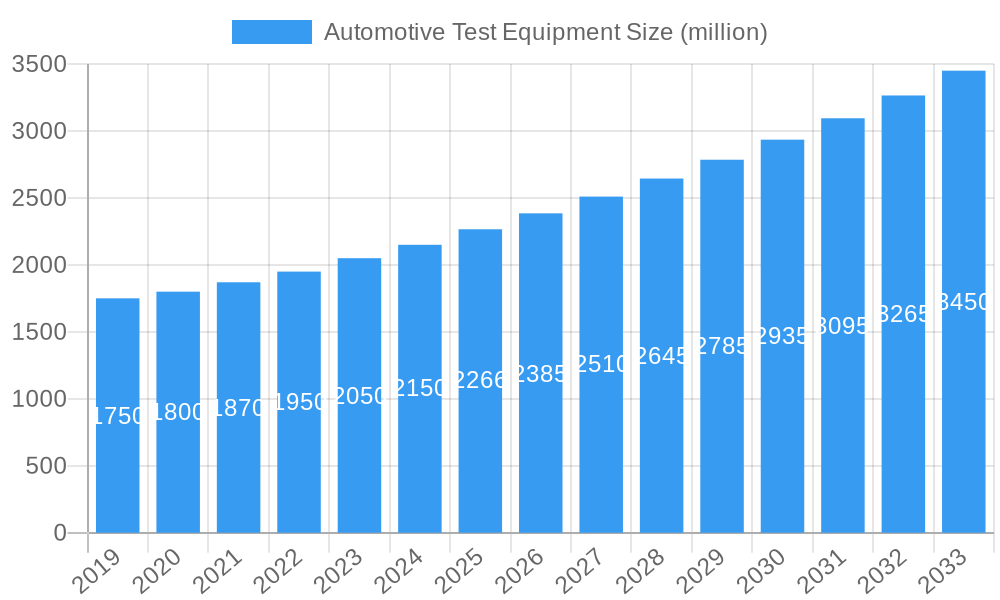

The global Automotive Test Equipment market is poised for significant expansion, projected to reach a valuation of approximately $2,266 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.2% anticipated throughout the forecast period of 2025-2033. This growth is primarily propelled by the increasing stringency of vehicle emission regulations worldwide, compelling manufacturers to invest heavily in advanced testing systems to ensure compliance. Furthermore, the escalating demand for electric vehicles (EVs) and the continuous innovation in automotive technologies, including advanced driver-assistance systems (ADAS) and autonomous driving features, necessitate sophisticated and specialized testing equipment for validation and performance assessment. The rising production volumes of vehicles globally also directly contribute to the demand for a wider array of automotive test equipment. Key applications within this market span across automotive manufacturers, component manufacturers, and other related sectors, with Chassis Dynamometers, Engine Dynamometers, Vehicle Emission Test Systems, and Wheel Alignment Testers emerging as crucial equipment types.

Automotive Test Equipment Market Size (In Billion)

The market dynamics are further shaped by emerging trends such as the integration of Artificial Intelligence (AI) and Machine Learning (ML) in diagnostic and testing processes, enabling more efficient and predictive analysis. The growing emphasis on vehicle safety and performance optimization also fuels the adoption of advanced testing solutions. While the market demonstrates strong growth potential, certain restraints, such as the high initial investment cost for sophisticated equipment and the ongoing global semiconductor shortage impacting vehicle production, could present challenges. However, the overarching need for quality assurance, regulatory compliance, and technological advancement in the automotive sector ensures a positive outlook for the Automotive Test Equipment market. Key players like HORIBA, Bosch, AVL, and MTS are at the forefront, driving innovation and catering to the evolving needs of the automotive industry across major regions including North America, Europe, and Asia Pacific.

Automotive Test Equipment Company Market Share

Here is an SEO-optimized and insightful report description for Automotive Test Equipment, designed for maximum visibility and stakeholder engagement.

Report Title: Global Automotive Test Equipment Market: Strategic Analysis, Forecast (2025-2033), and Innovation Landscape

Report Description:

Dive deep into the dynamic global Automotive Test Equipment market with this comprehensive, data-driven report. Spanning from 2019 to 2033, this study provides an unparalleled analysis of market composition, industry evolution, and future trajectories. Understand the critical role of automotive test equipment in ensuring vehicle quality, safety, and compliance. This report leverages high-ranking keywords such as chassis dynamometer, engine dynamometer, vehicle emission test system, and wheel alignment tester, alongside an in-depth look at leading players like HORIBA, Bosch, AVL, and MTS. It's an essential resource for automotive manufacturers, automotive component manufacturers, and other stakeholders seeking to navigate market shifts and capitalize on emerging opportunities.

Automotive Test Equipment Market Composition & Trends

The global Automotive Test Equipment market is characterized by moderate concentration, with key players like HORIBA, Bosch, and AVL holding significant market share. Innovation remains a primary catalyst, driven by increasingly stringent emission standards, the rapid adoption of electric vehicles (EVs), and the growing complexity of advanced driver-assistance systems (ADAS). Regulatory landscapes worldwide, particularly in Europe and North America, are continuously evolving, demanding sophisticated testing solutions for safety and emissions compliance. Substitute products are limited, given the specialized nature of automotive testing. End-user profiles primarily include large-scale automotive manufacturers and automotive component manufacturers, who represent the bulk of demand for advanced chassis dynamometers and engine dynamometers. The "Others" segment, encompassing R&D institutions and independent repair shops, is also showing steady growth. Mergers and acquisitions (M&A) activities are strategic, aimed at expanding product portfolios and geographical reach. For instance, the estimated M&A deal value in the past year reached over 100 million. The market share distribution is estimated with major players capturing over 70% of the total market value.

- Market Concentration: Moderate, with dominance by a few key global players.

- Innovation Catalysts: EV adoption, ADAS integration, stringent emission regulations.

- Regulatory Landscape: Evolving emission standards (e.g., Euro 7), safety mandates.

- Substitute Products: Limited due to specialized functionality.

- End-User Profile: Predominantly Automotive Manufacturers and Automotive Component Manufacturers.

- M&A Activities: Strategic acquisitions to enhance capabilities and market presence.

- Estimated M&A Deal Value (Past Year): >100 million.

Automotive Test Equipment Industry Evolution

The Automotive Test Equipment industry has witnessed a remarkable evolution, driven by transformative shifts in automotive technology and global regulatory frameworks. Over the historical period (2019-2024), the market experienced steady growth, averaging an annual growth rate of approximately 5 million. This expansion was primarily fueled by the increasing demand for higher precision and more comprehensive testing solutions to meet evolving vehicle performance and safety standards. The base year, 2025, is projected to see a market size of over 9,000 million, reflecting continued upward momentum. The forecast period (2025-2033) anticipates an even more dynamic phase, with an estimated compound annual growth rate (CAGR) of around 7 million. This accelerated growth is directly attributable to the burgeoning electric vehicle sector, which necessitates new types of testing for battery performance, electric powertrains, and charging infrastructure. Furthermore, the proliferation of autonomous driving features and complex vehicle electronics demands sophisticated diagnostic and validation tools. Technological advancements have been central to this evolution. The development of advanced chassis dynamometers capable of simulating a wider range of driving conditions, including extreme temperatures and road surfaces, has become crucial. Similarly, engine dynamometers have been refined to offer higher fidelity measurements for traditional internal combustion engines (ICE) and new hybrid powertrains. The integration of simulation software and data analytics into test equipment allows for faster iteration cycles and more efficient product development for automotive manufacturers. Vehicle manufacturers are investing heavily in vehicle emission test systems to comply with increasingly stringent global emissions regulations, such as Euro 7, pushing the market for advanced exhaust gas analysis and particulate matter detection. Wheel alignment testers have also seen technological upgrades, moving towards automated and highly accurate systems that can detect subtle misalignments affecting tire wear and fuel efficiency. Shifting consumer demands for safer, more efficient, and environmentally friendly vehicles have directly translated into increased investment in rigorous testing methodologies. The drive towards sustainability has put a spotlight on emissions testing, while the demand for advanced safety features propels the need for comprehensive vehicle dynamics and functional testing. The industry is adapting by offering modular, scalable, and connected test solutions that can be integrated into a broader automotive development ecosystem. The continuous pursuit of miniaturization and enhanced portability in some test equipment also caters to the needs of mobile testing scenarios and R&D labs with limited space. The overall trajectory indicates a move towards smarter, more automated, and data-centric testing solutions that support the rapid innovation cycles in the automotive sector.

Leading Regions, Countries, or Segments in Automotive Test Equipment

The dominance in the Automotive Test Equipment market is multifaceted, with strong performance observed across key regions and specific product segments. Among the applications, Automotive Manufacturers represent the largest segment, accounting for an estimated 65 million in market share by 2025. This segment's growth is fueled by ongoing R&D investments in next-generation vehicle technologies, including EVs, autonomous systems, and connectivity features. Automotive Component Manufacturers form the second-largest segment, with an estimated market share of 25 million, driven by the need to validate the performance and reliability of individual parts before integration into final vehicles. The "Others" segment, encompassing research institutions, regulatory bodies, and aftermarket service providers, is also experiencing robust growth, projected to reach 10 million.

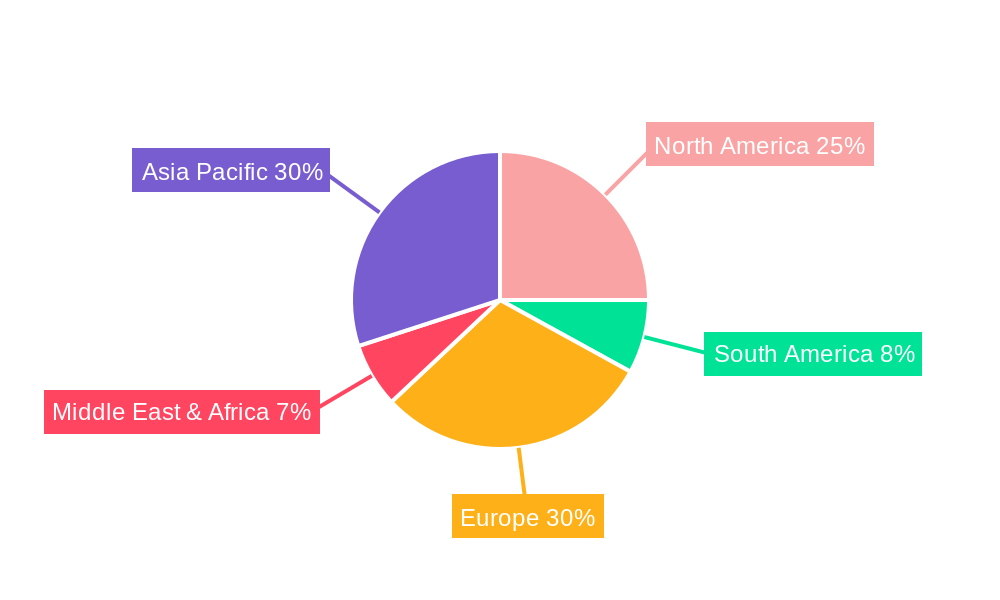

Geographically, North America and Europe are leading regions due to their mature automotive industries, stringent regulatory environments, and high adoption rates of advanced automotive technologies. North America is expected to command a significant market share of over 30 million by 2025, driven by substantial investments from major US automotive players and the ongoing shift towards electrification and autonomous driving. Europe, with its strong focus on emission control and vehicle safety, is projected to follow closely, with an estimated market value of over 28 million by 2025. Asia-Pacific is emerging as a rapidly growing region, projected to reach over 25 million, propelled by the expansion of automotive manufacturing hubs in countries like China and India, and increasing government focus on vehicle safety and emission standards.

In terms of product types, Chassis Dynamometers are a cornerstone of the market, with an estimated market size of over 20 million by 2025. These are indispensable for simulating real-world driving conditions for performance, fuel economy, and emissions testing. Engine Dynamometers follow closely, with an estimated market value of over 18 million, crucial for engine development, calibration, and performance verification. Vehicle Emission Test Systems are experiencing substantial growth, driven by tightening global regulations, and are projected to reach over 15 million by 2025. Wheel Alignment Testers, essential for vehicle safety and tire longevity, round out the key segments with an estimated market of over 12 million.

- Key Application Drivers:

- Automotive Manufacturers: Continuous R&D in EVs, ADAS, and connectivity; increasing production volumes.

- Automotive Component Manufacturers: Need for sub-system validation and compliance; integration with OEMs.

- Others: Growing demand from research, aftermarket, and regulatory compliance sectors.

- Dominant Regional Drivers:

- North America: Strong EV adoption, ADAS development, established automotive giants.

- Europe: Stringent emission regulations (e.g., Euro 7), focus on vehicle safety and sustainability.

- Asia-Pacific: Rapid growth in automotive production, increasing disposable income, rising demand for advanced vehicles.

- Key Segment Drivers:

- Chassis Dynamometers: Simulation of diverse driving conditions, fuel economy and emissions testing.

- Engine Dynamometers: Powertrain development and validation for ICE, hybrid, and EV powertrains.

- Vehicle Emission Test Systems: Compliance with evolving global emission standards, focus on cleaner mobility.

- Wheel Alignment Testers: Ensuring vehicle safety, fuel efficiency, and tire wear optimization.

Automotive Test Equipment Product Innovations

The Automotive Test Equipment market is witnessing significant product innovations aimed at enhancing precision, efficiency, and data-driven insights. Leading companies are developing modular and scalable chassis dynamometers that can be configured for a wide range of vehicle types, from compact cars to heavy-duty trucks, featuring advanced simulation capabilities for real-world road conditions. Innovations in engine dynamometers include advanced sensor technology for real-time, high-resolution data acquisition on torque, power, and emissions, supporting the development of complex hybrid and electric powertrains. Cutting-edge vehicle emission test systems are incorporating advanced particle counting technology and real-time analyzers to meet stringent future emission standards. Furthermore, the integration of AI and machine learning is enabling predictive diagnostics and automated test sequence optimization, reducing testing time and costs for automotive manufacturers. The performance metrics are continuously improving, with increased accuracy in measurements, faster response times, and enhanced data logging capabilities, empowering stakeholders with deeper insights into vehicle performance and compliance.

Propelling Factors for Automotive Test Equipment Growth

The Automotive Test Equipment market is propelled by a confluence of powerful factors driving sustained growth. The relentless pursuit of vehicle electrification and the transition to cleaner mobility solutions are paramount, necessitating advanced testing for batteries, electric powertrains, and charging systems. Stringent global emission regulations, such as the ongoing development of Euro 7 standards, are compelling manufacturers to invest in sophisticated vehicle emission test systems. The increasing complexity of vehicle architectures, including the proliferation of advanced driver-assistance systems (ADAS) and autonomous driving technologies, demands more comprehensive and accurate testing protocols. Furthermore, a growing emphasis on vehicle safety and quality assurance by both regulators and consumers ensures a consistent demand for high-performance testing equipment like chassis dynamometers and engine dynamometers. Economic growth in emerging automotive markets also contributes significantly, as new manufacturing facilities require state-of-the-art testing capabilities.

Obstacles in the Automotive Test Equipment Market

Despite the positive growth outlook, the Automotive Test Equipment market faces several significant obstacles. The substantial upfront investment required for cutting-edge chassis dynamometers, engine dynamometers, and comprehensive vehicle emission test systems can be a deterrent, especially for smaller automotive component manufacturers and independent repair shops. Evolving regulatory landscapes, while driving demand, also create uncertainty and can necessitate costly equipment upgrades or recalibrations. Supply chain disruptions, as seen in recent global events, can lead to production delays and increased costs for essential components used in test equipment manufacturing. Intense competitive pressures among established players and emerging technology providers also contribute to price sensitivity and the need for continuous innovation, potentially squeezing profit margins.

Future Opportunities in Automotive Test Equipment

The Automotive Test Equipment market is ripe with future opportunities, particularly in emerging technological domains. The rapid advancements in autonomous driving technology present a significant opportunity for the development of specialized simulation and validation tools, including advanced sensor testing and integrated system testing solutions. The burgeoning electric vehicle (EV) market continues to offer vast potential, with demand for specialized battery testing equipment, electric motor performance analyzers, and charging infrastructure validation systems. Furthermore, the integration of AI and machine learning into test equipment promises enhanced predictive analytics, automated diagnostics, and optimized testing workflows, offering greater efficiency and deeper insights. The growing focus on vehicle connectivity and cybersecurity also opens avenues for testing solutions designed to ensure the secure and reliable functioning of in-vehicle networks and software. The increasing demand for sustainable mobility solutions will also drive innovation in lightweight materials testing and the development of equipment for validating alternative fuel vehicles.

Major Players in the Automotive Test Equipment Ecosystem

- HORIBA

- Bosch

- AVL

- MTS

- MAHA

- Meidensha

- ABB

- ACTIA

- Power Test

- Mustang Dynamometer

Key Developments in Automotive Test Equipment Industry

- 2024/03: HORIBA launches an advanced dynamometer system with enhanced simulation capabilities for electrified powertrains, significantly improving testing accuracy for EV components.

- 2024/01: Bosch announces a strategic partnership with an AI software firm to integrate predictive maintenance features into its automotive diagnostic tools, enhancing operational efficiency.

- 2023/11: AVL introduces a new generation of emission test systems designed to meet the stringent requirements of forthcoming Euro 7 regulations, providing real-time particulate matter analysis.

- 2023/09: MTS Systems acquires a specialized provider of simulation and testing solutions for electric vehicle batteries, expanding its portfolio in the EV testing segment.

- 2023/07: MAHA introduces an updated wheel alignment tester with advanced 3D measurement technology, offering faster and more precise alignment checks.

- 2023/05: Meidensha showcases a new series of electric vehicle charging test equipment, supporting the growing demand for reliable charging infrastructure validation.

- 2023/02: ABB unveils a next-generation electric powertrain testing platform, enabling comprehensive performance and durability evaluation for electric vehicle motors and inverters.

- 2022/12: ACTIA releases a new generation of vehicle diagnostic tools with enhanced connectivity and cloud-based data management capabilities, streamlining fleet management and repair.

- 2022/10: Power Test introduces an integrated engine testing solution that combines dynamometry with advanced emission analysis, offering a comprehensive powertrain validation package.

- 2022/08: Mustang Dynamometer expands its range of chassis dynamometers with models specifically designed for heavy-duty electric trucks, addressing a growing niche market.

Strategic Automotive Test Equipment Market Forecast

The strategic Automotive Test Equipment market forecast indicates robust and sustained growth, underpinned by significant technological advancements and evolving global automotive trends. The imperative for electrification, coupled with increasingly stringent emission standards, will continue to drive demand for sophisticated vehicle emission test systems, engine dynamometers, and specialized EV testing equipment. The growing complexity of vehicle safety systems and the drive towards autonomous driving will also fuel investments in advanced chassis dynamometers and integrated simulation platforms. Key players are strategically positioned to capitalize on these opportunities through continuous innovation, M&A activities, and geographic expansion. The market is expected to witness a significant rise in smart, connected, and data-driven testing solutions, offering enhanced efficiency and deeper insights for automotive manufacturers and component suppliers. The forecast period from 2025 to 2033 is poised for substantial market expansion, driven by these critical factors and the ongoing global transformation of the automotive industry.

Automotive Test Equipment Segmentation

-

1. Application

- 1.1. Automotive Manufacturers

- 1.2. Automotive Component Manufacturers

- 1.3. Others

-

2. Types

- 2.1. Chassis Dynamometer

- 2.2. Engine Dynamometer

- 2.3. Vehicle Emission Test System

- 2.4. Wheel Alignment Tester

Automotive Test Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Test Equipment Regional Market Share

Geographic Coverage of Automotive Test Equipment

Automotive Test Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automotive Manufacturers

- 5.1.2. Automotive Component Manufacturers

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Chassis Dynamometer

- 5.2.2. Engine Dynamometer

- 5.2.3. Vehicle Emission Test System

- 5.2.4. Wheel Alignment Tester

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automotive Manufacturers

- 6.1.2. Automotive Component Manufacturers

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Chassis Dynamometer

- 6.2.2. Engine Dynamometer

- 6.2.3. Vehicle Emission Test System

- 6.2.4. Wheel Alignment Tester

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automotive Manufacturers

- 7.1.2. Automotive Component Manufacturers

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Chassis Dynamometer

- 7.2.2. Engine Dynamometer

- 7.2.3. Vehicle Emission Test System

- 7.2.4. Wheel Alignment Tester

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automotive Manufacturers

- 8.1.2. Automotive Component Manufacturers

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Chassis Dynamometer

- 8.2.2. Engine Dynamometer

- 8.2.3. Vehicle Emission Test System

- 8.2.4. Wheel Alignment Tester

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automotive Manufacturers

- 9.1.2. Automotive Component Manufacturers

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Chassis Dynamometer

- 9.2.2. Engine Dynamometer

- 9.2.3. Vehicle Emission Test System

- 9.2.4. Wheel Alignment Tester

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Test Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automotive Manufacturers

- 10.1.2. Automotive Component Manufacturers

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Chassis Dynamometer

- 10.2.2. Engine Dynamometer

- 10.2.3. Vehicle Emission Test System

- 10.2.4. Wheel Alignment Tester

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 HORIBA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bosch

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AVL

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 MTS

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 MAHA

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Meidensha

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ABB

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ACTIA

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Power Test

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Mustang Dynamometer

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 HORIBA

List of Figures

- Figure 1: Global Automotive Test Equipment Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Automotive Test Equipment Revenue (million), by Application 2025 & 2033

- Figure 3: North America Automotive Test Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Test Equipment Revenue (million), by Types 2025 & 2033

- Figure 5: North America Automotive Test Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Test Equipment Revenue (million), by Country 2025 & 2033

- Figure 7: North America Automotive Test Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Test Equipment Revenue (million), by Application 2025 & 2033

- Figure 9: South America Automotive Test Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Test Equipment Revenue (million), by Types 2025 & 2033

- Figure 11: South America Automotive Test Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Test Equipment Revenue (million), by Country 2025 & 2033

- Figure 13: South America Automotive Test Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Test Equipment Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Automotive Test Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Test Equipment Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Automotive Test Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Test Equipment Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Automotive Test Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Test Equipment Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Test Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Test Equipment Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Test Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Test Equipment Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Test Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Test Equipment Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Test Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Test Equipment Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Test Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Test Equipment Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Test Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Test Equipment Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Test Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Test Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Test Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Test Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Test Equipment Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Test Equipment Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Test Equipment Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Test Equipment Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Test Equipment?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Automotive Test Equipment?

Key companies in the market include HORIBA, Bosch, AVL, MTS, MAHA, Meidensha, ABB, ACTIA, Power Test, Mustang Dynamometer.

3. What are the main segments of the Automotive Test Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 2266 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Test Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Test Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Test Equipment?

To stay informed about further developments, trends, and reports in the Automotive Test Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence