Key Insights

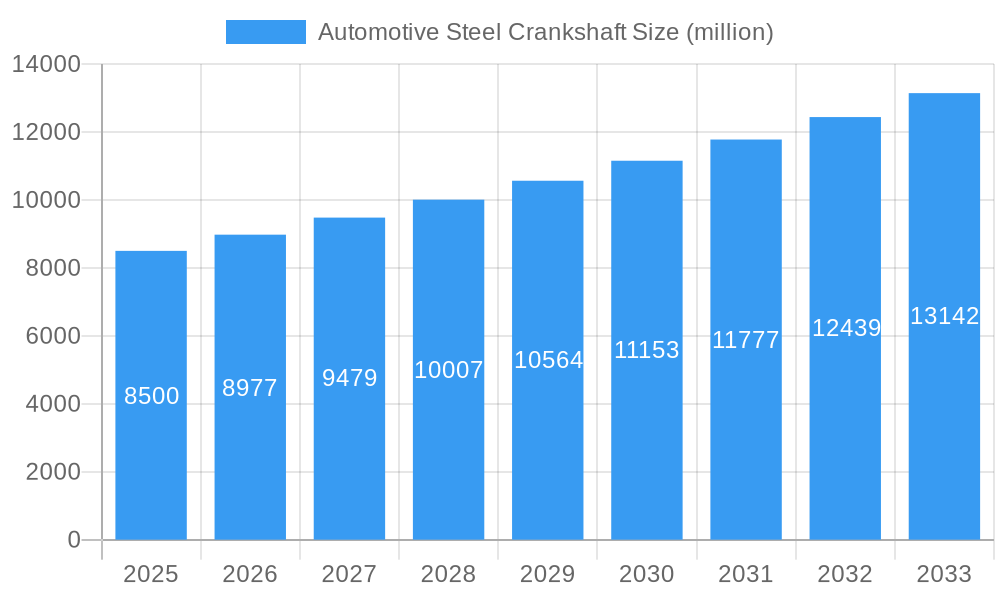

The global Automotive Steel Crankshaft market is projected for substantial growth, expected to reach a market size of $8.7 billion by 2025. The market is forecast to expand at a Compound Annual Growth Rate (CAGR) of 5% through 2033. This expansion is driven by increasing global vehicle production, particularly in emerging economies, and sustained demand for Internal Combustion Engine (ICE) vehicles. Advancements in engine technology, requiring more robust crankshafts, alongside high production volumes of passenger and commercial vehicles, are key growth factors. Additionally, the pursuit of improved fuel efficiency and performance in ICE vehicles indirectly elevates the demand for high-quality steel crankshafts capable of withstanding increased operational pressures and temperatures. Stringent automotive emission standards also necessitate optimized engine designs, ensuring consistent demand for reliable crankshaft components.

Automotive Steel Crankshaft Market Size (In Billion)

Despite the rise of the Electric Vehicle (EV) market, steel crankshafts will remain relevant. While EVs do not use crankshafts, the extensive existing fleet of ICE vehicles and ongoing production of new ICE models, especially for heavy-duty commercial transport and specific passenger car segments, will sustain demand. Potential restraints include the increasing adoption of EVs and the consequent long-term decline in ICE vehicle production. However, significant opportunities exist in developing nations and through continuous innovation in material science and manufacturing processes for steel crankshafts. Passenger cars and commercial vehicles are anticipated to be the dominant application segments, with both forged and cast steel crankshafts fulfilling diverse performance and cost requirements. Leading manufacturers are actively investing in research and development to enhance product offerings and meet evolving market demands.

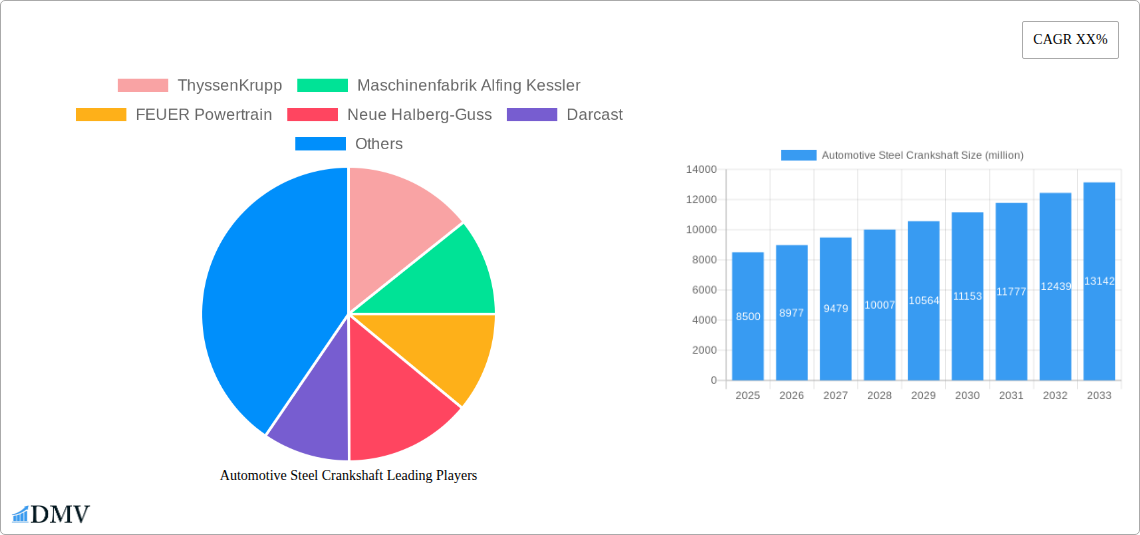

Automotive Steel Crankshaft Company Market Share

This comprehensive report offers a definitive analysis of the global Automotive Steel Crankshaft market, detailing its current state and future outlook. With a study period from 2019 to 2033, including a base year of 2025, this report is an essential resource for stakeholders seeking to understand market dynamics, identify growth avenues, and navigate competitive landscapes. We provide in-depth coverage of market composition, industry evolution, product innovations, and strategic forecasts, serving automotive manufacturers, component suppliers, investors, and industry analysts. This report delivers actionable intelligence for informed strategic decision-making in this vital automotive component sector.

Automotive Steel Crankshaft Market Composition & Trends

The global automotive steel crankshaft market exhibits a moderately consolidated structure, with key players investing heavily in technological advancements and process optimizations to maintain a competitive edge. Innovation catalysts include the increasing demand for lighter, more durable crankshafts to improve fuel efficiency and reduce emissions, driven by stringent environmental regulations worldwide. The regulatory landscape plays a pivotal role, with evolving emission standards and safety mandates influencing material choices and manufacturing processes. Substitute products, such as those made from advanced composites or different metal alloys, are being explored, but steel crankshafts continue to dominate due to their cost-effectiveness and proven reliability. End-user profiles are diverse, ranging from high-volume passenger car manufacturers to specialized commercial vehicle producers, each with specific performance and cost requirements. Mergers and acquisitions (M&A) activities are notable, with several major players engaging in strategic alliances and consolidations to expand their market reach, enhance their product portfolios, and achieve economies of scale. For instance, historical M&A deal values indicate significant investment flowing into this sector, aiming to bolster production capacities and technological capabilities.

- Market Share Distribution: The top five players are estimated to hold approximately 60% of the market share, with significant regional variations.

- Innovation Focus: Key areas of innovation include advanced forging techniques, improved material science for enhanced strength-to-weight ratios, and precision machining for tighter tolerances.

- Regulatory Impact: Stringent emission norms (e.g., Euro 7, EPA standards) are pushing for more efficient engine designs, directly impacting crankshaft performance requirements.

- M&A Activity: Recent years have witnessed strategic acquisitions by larger conglomerates seeking to integrate their supply chains and expand their product offerings in the powertrain segment. Estimated M&A deal values in the past three years collectively reached over $500 million, signaling robust consolidation efforts.

Automotive Steel Crankshaft Industry Evolution

The automotive steel crankshaft industry has undergone significant evolution, driven by transformative shifts in automotive technology, manufacturing processes, and global economic trends. Throughout the historical period of 2019–2024, the market experienced steady growth, buoyed by the increasing global vehicle production and the inherent demand for internal combustion engine (ICE) components. However, the advent and rapid adoption of electric vehicles (EVs) have introduced a dynamic element, prompting a strategic re-evaluation of market strategies. Despite the rise of EVs, the sheer volume of existing ICE vehicles and the continued production of hybrids ensure a substantial and enduring demand for steel crankshafts, particularly in emerging economies where ICE technology remains prevalent.

Technological advancements have been a cornerstone of this evolution. The development of advanced forging techniques, such as isothermal forging and precision forging, has enabled the production of lighter, stronger, and more complex crankshaft designs. These innovations are crucial for enhancing engine performance, improving fuel efficiency, and meeting increasingly stringent emission standards. Furthermore, advancements in material science, including the use of high-strength low-alloy (HSLA) steels and advanced heat treatment processes, have contributed to improved durability and performance metrics of steel crankshafts. Computational fluid dynamics (CFD) and finite element analysis (FEA) are now integral to crankshaft design, allowing engineers to optimize designs for reduced stress concentrations and improved material utilization, leading to more reliable and longer-lasting components.

Shifting consumer demands have also played a critical role. The persistent consumer preference for a wide range of vehicle types, including performance-oriented vehicles and heavy-duty commercial trucks, continues to drive the demand for robust and reliable steel crankshafts. While there is a growing emphasis on fuel economy and reduced emissions, consumers are also concerned with the longevity and performance of their vehicles. This dual demand necessitates the continuous innovation of steel crankshafts to meet these evolving expectations. The estimated growth rate for the automotive steel crankshaft market, projected to be around 3.5% from 2025 to 2033, reflects this ongoing demand, even amidst the transition towards electrification. Adoption metrics for advanced manufacturing techniques in crankshaft production have seen a steady increase, with over 70% of major manufacturers now utilizing advanced simulation tools in their design processes.

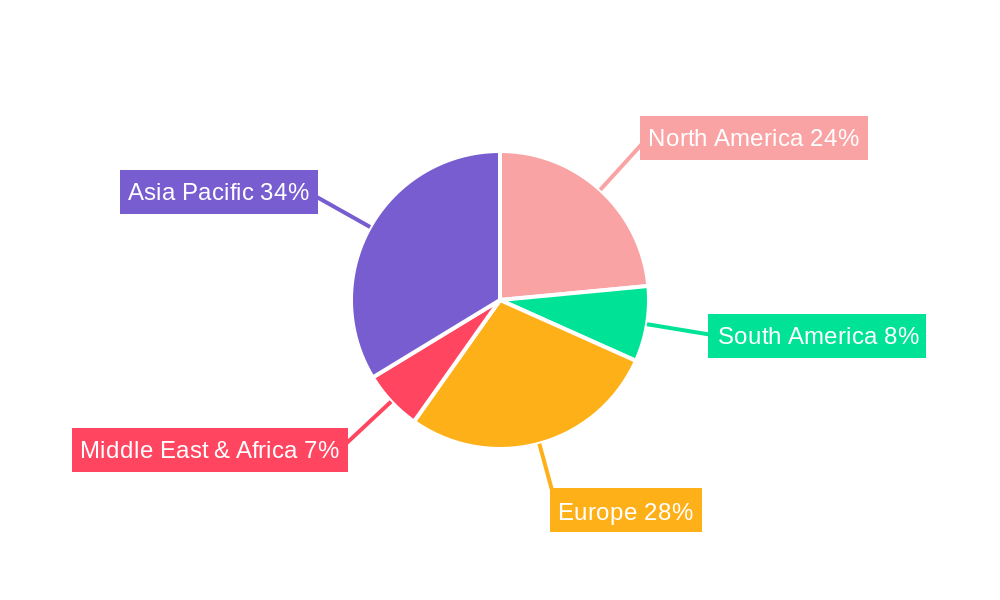

Leading Regions, Countries, or Segments in Automotive Steel Crankshaft

The automotive steel crankshaft market's dominance is intricately linked to the global automotive manufacturing landscape, with specific regions and segments exhibiting exceptional growth and influence. Asia-Pacific, spearheaded by China and India, stands out as the leading region, propelled by its massive automotive production volumes, burgeoning domestic demand for passenger cars and commercial vehicles, and favorable manufacturing cost structures. This region's dominance is further amplified by significant investments in expanding production capacities and an increasing focus on export markets.

Within the Application segment, Passenger Cars represent the largest and most influential category. The sheer volume of passenger vehicles produced globally, coupled with continuous model updates and the persistent demand for internal combustion engine (ICE) powertrains in many markets, solidifies this segment's leading position. While the transition to electric vehicles is gaining momentum, hybrid powertrains that still utilize crankshafts are also contributing to sustained demand. The technological advancements in engine efficiency and emissions reduction for passenger cars directly translate into a need for high-performance, precisely engineered steel crankshafts.

In terms of Types, Forged Steel crankshafts hold a commanding lead. This superiority stems from their inherent strength, durability, and superior fatigue resistance compared to cast iron steel crankshafts. Forged steel crankshafts are essential for high-performance engines, heavy-duty applications, and scenarios demanding extreme reliability under high stress. The precision and meticulous engineering involved in forging processes allow for optimal grain flow and material integrity, making them the preferred choice for premium and performance-oriented vehicles, as well as for critical components in commercial vehicles where longevity and robustness are paramount.

- Asia-Pacific Dominance Drivers:

- High Production Volume: Countries like China and India are global hubs for automotive manufacturing, producing millions of vehicles annually.

- Growing Domestic Demand: Rapidly expanding middle classes in these nations fuel the demand for passenger cars and commercial vehicles.

- Cost Competitiveness: Lower manufacturing and labor costs make the region an attractive base for crankshaft production and export.

- Government Initiatives: Supportive policies for the automotive sector and infrastructure development further bolster growth.

- Passenger Cars Segment Leadership:

- Global Vehicle Production Numbers: Passenger cars constitute the largest share of global automotive output.

- Hybrid Powertrain Integration: Continued development and sales of hybrid vehicles maintain demand for crankshafts.

- Performance and Efficiency Demands: Manufacturers are continually striving to improve the performance and fuel efficiency of ICEs in passenger cars, requiring advanced crankshaft designs.

- Forged Steel Crankshaft Superiority:

- Exceptional Strength and Durability: Forging creates a denser, stronger material with superior grain structure, ideal for high-stress applications.

- Performance Applications: Essential for high-RPM engines and performance vehicles requiring maximum reliability.

- Commercial Vehicle Reliability: Crucial for the demanding operational cycles of trucks, buses, and heavy machinery.

- Technological Advancements in Forging: Innovations in isothermal and precision forging are enhancing the quality and reducing the weight of forged steel crankshafts.

Automotive Steel Crankshaft Product Innovations

Automotive steel crankshaft product innovations are critically focused on enhancing performance, reducing weight, and improving manufacturing efficiency to meet evolving vehicle demands. Manufacturers are developing crankshafts with optimized designs that reduce rotational inertia, leading to improved engine responsiveness and fuel economy. Advances in material science, such as the use of high-strength steel alloys and advanced heat treatment processes, are yielding crankshafts with superior fatigue strength and wear resistance. Precision machining techniques, including multi-axis CNC machining, ensure tighter tolerances and improved surface finishes, contributing to quieter engine operation and reduced friction. Furthermore, the integration of advanced simulation tools during the design phase allows for the virtual testing of crankshaft performance under various operating conditions, accelerating product development cycles and ensuring optimal reliability.

Propelling Factors for Automotive Steel Crankshaft Growth

The automotive steel crankshaft market is propelled by a confluence of technological advancements, economic imperatives, and evolving regulatory landscapes. The continued, albeit gradually declining, global reliance on internal combustion engines (ICE) for a significant portion of passenger cars and commercial vehicles remains a primary driver. Technological innovation, particularly in engine downsizing and turbocharging, necessitates the development of stronger and lighter crankshafts to handle increased power densities, directly boosting demand for high-performance steel variants. Economic growth in emerging markets fuels vehicle sales, subsequently increasing the demand for essential engine components like crankshafts. Furthermore, stringent emission regulations worldwide, while pushing for electrification, also drive innovation in ICE efficiency, requiring more advanced and precisely engineered crankshafts to meet these targets. The sheer volume of existing ICE fleets requiring maintenance and replacement parts also provides a steady, albeit slower, growth stream.

Obstacles in the Automotive Steel Crankshaft Market

Despite robust demand, the automotive steel crankshaft market faces significant obstacles that could impede growth. The accelerating global transition towards electric vehicles (EVs) poses a substantial long-term threat, as EVs do not utilize crankshafts, thereby reducing the overall addressable market for these components. Stringent environmental regulations, while also a driver for innovation in ICE, can increase manufacturing costs due to the need for specialized materials and processes, impacting profitability. Supply chain disruptions, as witnessed in recent years, can lead to material shortages, production delays, and increased component costs, affecting the entire value chain. Intense competition among established players and emerging manufacturers, particularly from low-cost regions, can lead to price wars and reduced profit margins. Moreover, the capital-intensive nature of crankshaft manufacturing requires significant investment in advanced machinery and skilled labor, creating a barrier to entry for new players.

Future Opportunities in Automotive Steel Crankshaft

Emerging opportunities within the automotive steel crankshaft market lie in catering to the persistent demand for hybrid powertrains and optimizing crankshafts for advanced ICE technologies. As the automotive industry navigates the transition to electrification, hybrid vehicles will continue to utilize internal combustion engines, albeit with potentially different performance profiles, creating a niche for specialized crankshaft designs. The ongoing development of more fuel-efficient and lower-emission ICE technologies in emerging markets, where EV adoption may be slower, presents a significant growth avenue. Furthermore, advancements in manufacturing processes, such as additive manufacturing (3D printing) for prototyping and specialized components, or the development of novel steel alloys with improved performance characteristics, offer avenues for product differentiation and market expansion. The aftermarket service sector, catering to the vast existing fleet of ICE vehicles, also presents a stable and ongoing opportunity for crankshaft manufacturers and suppliers.

Major Players in the Automotive Steel Crankshaft Ecosystem

- ThyssenKrupp

- Maschinenfabrik Alfing Kessler

- FEUER Powertrain

- Neue Halberg-Guss

- Darcast

- Arrow Precision

- CIE Automotive

- Teksid

- Ellwood Crankshaft

- NSI Crankshaft

- Kellogg Crankshaft

- Quimmco

- TFO Corporation

- Metalart Corporation

- Guilin Fuda

- Zhejiang Sun Stock

- Jiangsu Songlin

Key Developments in Automotive Steel Crankshaft Industry

- 2023/Ongoing: Increased investment in R&D for lighter and more durable crankshaft materials to improve fuel efficiency and meet stricter emission standards.

- 2023/Ongoing: Adoption of advanced simulation and AI-driven design tools to optimize crankshaft performance and reduce development cycles.

- 2022/2023: Strategic partnerships and consolidations among key players to enhance production capabilities and expand market reach, driven by global supply chain shifts.

- 2021/2022: Focus on precision forging techniques and advanced heat treatments to produce crankshafts with superior fatigue strength and wear resistance.

- 2020/2021: Increased demand for crankshafts for hybrid vehicle powertrains, reflecting the industry's gradual shift towards electrification.

- 2019/2020: Growing emphasis on sustainable manufacturing processes and material sourcing within the crankshaft production chain.

Strategic Automotive Steel Crankshaft Market Forecast

The strategic automotive steel crankshaft market forecast indicates a period of sustained, albeit moderating, growth driven by the continued demand for hybrid powertrains and the robust presence of internal combustion engines in key global markets. While the long-term outlook is influenced by the accelerating EV transition, the immediate to medium-term future presents significant opportunities for manufacturers who can innovate and adapt. Technological advancements in materials science and manufacturing processes will be crucial for producing lighter, stronger, and more efficient crankshafts that meet evolving performance and emission standards. Investment in expanding production capacity in emerging economies and focusing on aftermarket services will be key strategic imperatives for players aiming to capitalize on future market potential. The market is expected to grow at a Compound Annual Growth Rate (CAGR) of approximately 3.5% from 2025 to 2033, with an estimated market value reaching upwards of $5,000 million by the end of the forecast period.

Automotive Steel Crankshaft Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Forged Steel

- 2.2. Cast Iron Steel

Automotive Steel Crankshaft Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Steel Crankshaft Regional Market Share

Geographic Coverage of Automotive Steel Crankshaft

Automotive Steel Crankshaft REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Forged Steel

- 5.2.2. Cast Iron Steel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Forged Steel

- 6.2.2. Cast Iron Steel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Forged Steel

- 7.2.2. Cast Iron Steel

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Forged Steel

- 8.2.2. Cast Iron Steel

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Forged Steel

- 9.2.2. Cast Iron Steel

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Steel Crankshaft Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Forged Steel

- 10.2.2. Cast Iron Steel

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ThyssenKrupp

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Maschinenfabrik Alfing Kessler

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 FEUER Powertrain

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Neue Halberg-Guss

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Darcast

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Arrow Precision

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 CIE Automotive

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Teksid

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ellwood Crankshaft

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 NSI Crankshaft

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Kellogg Crankshaft

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Quimmco

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 TFO Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Metalart Corporation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Guilin Fuda

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Zhejiang Sun Stock

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Jiangsu Songlin

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 ThyssenKrupp

List of Figures

- Figure 1: Global Automotive Steel Crankshaft Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Steel Crankshaft Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Steel Crankshaft Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Steel Crankshaft Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive Steel Crankshaft Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Steel Crankshaft Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Steel Crankshaft Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Steel Crankshaft Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Steel Crankshaft Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Steel Crankshaft Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive Steel Crankshaft Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Steel Crankshaft Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Steel Crankshaft Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Steel Crankshaft Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Steel Crankshaft Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Steel Crankshaft Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive Steel Crankshaft Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Steel Crankshaft Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Steel Crankshaft Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Steel Crankshaft Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Steel Crankshaft Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Steel Crankshaft Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Steel Crankshaft Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Steel Crankshaft Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Steel Crankshaft Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Steel Crankshaft Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Steel Crankshaft Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Steel Crankshaft Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Steel Crankshaft Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Steel Crankshaft Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Steel Crankshaft Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Steel Crankshaft Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Steel Crankshaft Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Steel Crankshaft Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Steel Crankshaft Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Steel Crankshaft Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Steel Crankshaft Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Steel Crankshaft Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Steel Crankshaft Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Steel Crankshaft Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Steel Crankshaft?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Automotive Steel Crankshaft?

Key companies in the market include ThyssenKrupp, Maschinenfabrik Alfing Kessler, FEUER Powertrain, Neue Halberg-Guss, Darcast, Arrow Precision, CIE Automotive, Teksid, Ellwood Crankshaft, NSI Crankshaft, Kellogg Crankshaft, Quimmco, TFO Corporation, Metalart Corporation, Guilin Fuda, Zhejiang Sun Stock, Jiangsu Songlin.

3. What are the main segments of the Automotive Steel Crankshaft?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Steel Crankshaft," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Steel Crankshaft report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Steel Crankshaft?

To stay informed about further developments, trends, and reports in the Automotive Steel Crankshaft, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence