Key Insights

The global Automotive Diesel Particulate Filter (DPF) market is projected for substantial growth, estimated to reach USD 5.98 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 16.63%. This expansion is primarily driven by stricter global emission regulations, mandating the integration of advanced DPF technology in diesel engines to mitigate particulate matter emissions. The increasing prevalence of diesel vehicles, especially in the commercial sector for logistics, further supports market momentum. Technological innovations in DPF materials and regeneration systems, improving efficiency and reducing upkeep, are significant growth catalysts. Growing environmental consciousness and awareness of air pollution's health impacts also contribute to market expansion.

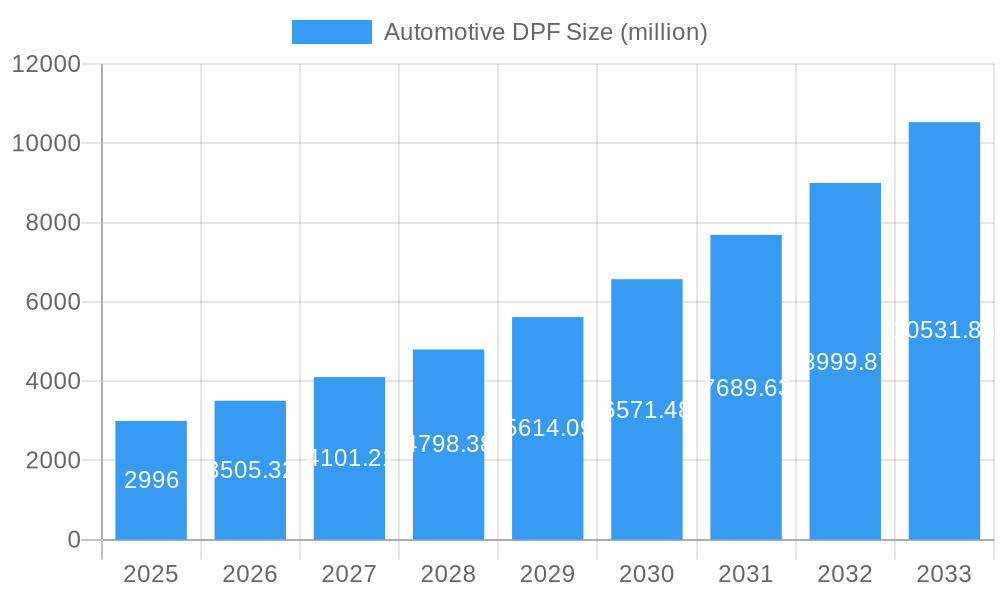

Automotive DPF Market Size (In Billion)

The Automotive DPF market is categorized by application and type. Passenger cars and commercial vehicles are the leading application segments. The "Cordierite Type" is expected to lead due to its cost-efficiency and performance, while emerging "Other Types," including Silicon Carbide (SiC) and ceramic matrix composites, are poised for growth due to enhanced thermal shock resistance and durability. Geographically, Asia Pacific, particularly China and India, is a key growth region, driven by a rapidly expanding automotive industry and the adoption of emission standards. North America and Europe, with established regulations and a focus on sustainable transport, will remain important markets. Leading companies such as Corning, NGK Insulators, Faurecia, and Tenneco are investing in R&D to drive innovation and maintain competitiveness.

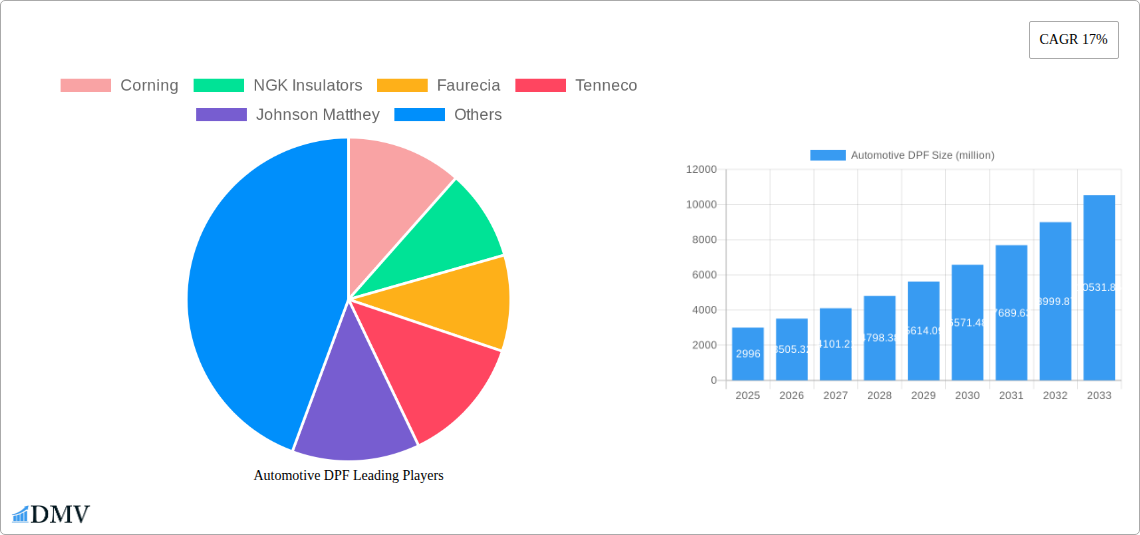

Automotive DPF Company Market Share

Automotive DPF Market Composition & Trends

The global Automotive Diesel Particulate Filter (DPF) market is a dynamic and evolving landscape, characterized by a moderate to high level of concentration among key players. Leading entities such as Corning, NGK Insulators, Faurecia, Tenneco, Johnson Matthey, Katcon, Umicore, and Bekaert are instrumental in shaping market dynamics through continuous innovation and strategic partnerships. The market's evolution is heavily influenced by stringent emission regulations worldwide, driving demand for advanced DPF technologies that effectively capture particulate matter from exhaust gases. Innovation catalysts include advancements in filter materials, coating technologies, and regeneration strategies, aiming to enhance efficiency and durability. Substitute products, while emerging in some niche applications, are yet to pose a significant threat to established DPF solutions. End-user profiles primarily comprise automotive manufacturers (OEMs) and the aftermarket service sector. Mergers and acquisitions (M&A) activities are strategic maneuvers to consolidate market share and expand technological capabilities; for instance, an estimated XXX million in M&A deals have been observed within the historical period, indicating a trend towards consolidation. The market share distribution shows a significant portion held by manufacturers specializing in Cordierite DPFs, though other advanced ceramic and metallic substrates are gaining traction.

Automotive DPF Industry Evolution

The Automotive DPF industry has undergone significant evolution, driven by a confluence of technological advancements, stringent environmental mandates, and shifting consumer preferences towards cleaner mobility solutions. Over the study period of 2019–2033, the market has witnessed robust growth trajectories, propelled by an increasing global awareness of air pollution and the detrimental health impacts of diesel emissions. From the historical period of 2019–2024, the market experienced an average annual growth rate of approximately 7.5%, a testament to the widespread adoption of DPF technology across both passenger cars and commercial vehicles. The base year of 2025 marks a pivotal point, with an estimated market size of XXX million, reflecting the established demand and ongoing regulatory push. The forecast period of 2025–2033 is projected to sustain this momentum, with an anticipated Compound Annual Growth Rate (CAGR) of 6.8%. This sustained growth is underpinned by advancements in DPF materials and designs. For example, the adoption of advanced ceramic substrates, offering superior thermal shock resistance and mechanical strength, has become a standard feature, with over 95% of new diesel vehicles equipped with such systems by 2024. Furthermore, innovations in catalyzed DPF (cDPF) coatings, incorporating precious metals like platinum and palladium, have significantly enhanced soot oxidation efficiency, contributing to a cleaner exhaust and meeting increasingly stringent Euro 7 and future emission standards. The market's adaptability to evolving technological landscapes, including the integration of DPFs with Selective Catalytic Reduction (SCR) systems for optimized emission control, has been crucial. Consumer demand for vehicles that not only meet regulatory requirements but also offer improved fuel efficiency and reduced environmental footprint further fuels the industry's evolution. The seamless integration of DPFs into existing vehicle architectures, coupled with their proven effectiveness in reducing particulate matter emissions by over 99%, has solidified their position as an indispensable component in modern diesel powertrains.

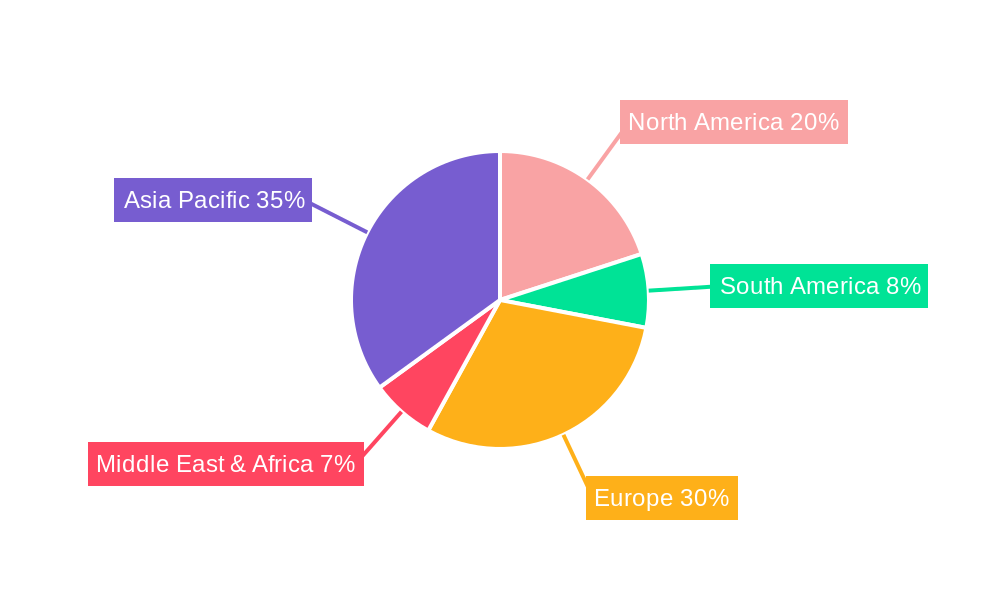

Leading Regions, Countries, or Segments in Automotive DPF

The global Automotive DPF market exhibits distinct regional dominance and segment leadership, primarily driven by regulatory stringency, vehicle parc composition, and industrial investment trends. Europe has consistently emerged as the leading region for Automotive DPF adoption and market share, a position cemented by its pioneering and consistently stringent emission standards, such as the Euro emission regulations. The region's commitment to reducing diesel emissions, coupled with a substantial population of diesel-powered passenger cars and commercial vehicles, creates an insatiable demand for advanced DPF solutions. For instance, in 2025, Europe is estimated to account for over 40% of the global DPF market revenue, valued at approximately XXX million. Key drivers for this dominance include substantial investments in advanced DPF manufacturing facilities by major players like Faurecia and Johnson Matthey within the region, and proactive regulatory support that mandates the inclusion of DPFs in virtually all new diesel vehicles.

- Application: Passenger Cars: The passenger car segment remains the largest application by volume and revenue within the DPF market. In 2025, this segment is projected to represent an estimated 65% of the total market value, translating to XXX million. The widespread use of diesel engines in passenger cars across Europe and, to a lesser extent, other developed markets, fuels this demand. Stringent emissions norms for urban areas and increasing consumer awareness regarding air quality further bolster the adoption of DPFs in this segment.

- Application: Commercial Vehicles: The commercial vehicle segment, encompassing trucks, buses, and vans, represents a significant and growing market for DPFs. By 2025, this segment is estimated to contribute XXX million to the market. The higher mileage and more intensive usage patterns of commercial vehicles, coupled with increasingly strict emissions regulations for heavy-duty vehicles (e.g., EPA 2010 in the US, Euro VI in Europe), necessitate robust and efficient DPF systems. Investments in fleet modernization and the retrofitting of older vehicles with DPFs also contribute to market growth.

- Types: Cordierite Type: Cordierite-based DPFs continue to dominate the market due to their cost-effectiveness, good thermal shock resistance, and proven track record. In 2025, Cordierite DPFs are expected to hold an estimated 80% market share, valued at XXX million. Their widespread availability, established manufacturing processes, and compatibility with a broad range of diesel engine applications make them the preferred choice for many OEMs. The segment's growth is driven by ongoing improvements in cordierite material properties and manufacturing techniques, enhancing durability and filtration efficiency.

- Types: Other Type: This category includes advanced DPFs made from materials like silicon carbide (SiC) and ceramic monoliths with specialized coatings, as well as metallic filters. While currently holding a smaller market share, estimated at 20% or XXX million in 2025, this segment is poised for significant growth. SiC DPFs offer superior thermal conductivity and mechanical strength, making them suitable for high-performance and demanding applications. Emerging technologies and increasing focus on lightweight materials and enhanced filtration performance are expected to drive the expansion of "Other Type" DPFs in the coming years.

Automotive DPF Product Innovations

Recent product innovations in the Automotive DPF market center on enhancing filtration efficiency, extending service life, and improving regeneration cycles. Manufacturers are developing DPFs with advanced porous ceramic structures and novel coating formulations that offer superior capture of ultra-fine particulate matter, exceeding 99.9% efficiency. Innovations include the integration of catalytic washcoats directly onto the filter substrate, promoting more efficient soot oxidation at lower temperatures, thereby reducing the frequency and severity of regeneration events. Furthermore, advancements in predictive diagnostics and self-cleaning functionalities are being explored to minimize maintenance requirements and optimize performance. For example, the introduction of hybrid DPF systems that combine filtration with active regeneration technologies promises to significantly extend the operational lifespan of components, a key selling proposition for fleet operators.

Propelling Factors for Automotive DPF Growth

The Automotive DPF market is propelled by a powerful synergy of factors. Foremost is the unwavering global regulatory push towards stricter emissions standards, such as the Euro 7 and future EPA mandates, which compel the use of advanced DPFs to control particulate matter. Technological advancements in filter materials and manufacturing processes, leading to more efficient and durable DPFs, are also critical drivers. Economic factors, including the increasing global vehicle parc and the growing demand for diesel engines in specific commercial applications, further fuel market expansion. The rising awareness of environmental pollution and its health impacts also encourages consumers and policymakers to favor cleaner transportation solutions, indirectly boosting DPF adoption.

Obstacles in the Automotive DPF Market

Despite robust growth, the Automotive DPF market faces several obstacles. Stringent and evolving regulatory requirements, while a driver, also present challenges in terms of constant R&D investment for compliance and potential regional disparities in enforcement. Supply chain disruptions, particularly for critical raw materials like precious metals used in catalytic coatings, can lead to price volatility and production delays, impacting the cost-effectiveness of DPFs. Competitive pressures from alternative powertrain technologies, such as electric vehicles, pose a long-term threat, although diesel powertrains are expected to remain significant in certain segments for the foreseeable future. The cost of DPF systems and their maintenance can also be a barrier for some consumers and small fleet operators.

Future Opportunities in Automotive DPF

Emerging opportunities in the Automotive DPF market lie in several key areas. The development of advanced materials and nano-coatings for even higher filtration efficiency and extended lifespan presents a significant avenue for innovation. The integration of DPFs with next-generation emission control systems, such as ammonia slip catalysts (ASCs), for comprehensive aftertreatment solutions offers new market potential. As emerging economies increasingly adopt stricter emission standards, they represent a rapidly growing market for DPF technology. Furthermore, the development of smart DPF systems with enhanced diagnostic capabilities and remote monitoring features caters to the evolving needs of connected vehicles and fleet management.

Major Players in the Automotive DPF Ecosystem

- Corning

- NGK Insulators

- Faurecia

- Tenneco

- Johnson Matthey

- Katcon

- Umicore

- Bekaert

Key Developments in Automotive DPF Industry

- 2023: Launch of next-generation Cordierite DPFs with enhanced durability and filtration efficiency by Corning.

- 2023: Faurecia announces significant investment in R&D for advanced ceramic filter technologies.

- 2022: Tenneco introduces a new integrated DPF and SCR system for heavy-duty commercial vehicles.

- 2022: Johnson Matthey develops novel catalytic coatings for improved soot oxidation at lower temperatures.

- 2021: Umicore expands its production capacity for advanced DPF substrates to meet growing demand.

- 2020: NGK Insulators introduces a lightweight silicon carbide (SiC) DPF for enhanced performance.

- 2019: Katcon partners with a major OEM to develop customized DPF solutions for new vehicle platforms.

Strategic Automotive DPF Market Forecast

The strategic forecast for the Automotive DPF market indicates sustained growth driven by the indispensable role of these components in meeting stringent global emission regulations. Continued innovation in materials science and coating technologies will unlock opportunities for higher filtration efficiency and extended product lifecycles. The increasing adoption of DPFs in emerging markets, coupled with the ongoing demand for efficient diesel powertrains in commercial applications, will solidify the market's trajectory. Integration with advanced aftertreatment systems and the development of "smart" DPFs will further enhance their value proposition, ensuring their continued relevance and market potential in the evolving automotive landscape.

Automotive DPF Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Cordierite Type

- 2.2. Other Type

Automotive DPF Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive DPF Regional Market Share

Geographic Coverage of Automotive DPF

Automotive DPF REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cordierite Type

- 5.2.2. Other Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cordierite Type

- 6.2.2. Other Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cordierite Type

- 7.2.2. Other Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cordierite Type

- 8.2.2. Other Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cordierite Type

- 9.2.2. Other Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive DPF Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cordierite Type

- 10.2.2. Other Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Corning

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 NGK Insulators

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Faurecia

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Tenneco

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Johnson Matthey

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Katcon

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Umicore

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bekaert

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Corning

List of Figures

- Figure 1: Global Automotive DPF Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive DPF Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive DPF Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive DPF Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive DPF Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive DPF Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive DPF Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive DPF Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive DPF Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive DPF Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive DPF Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive DPF Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive DPF Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive DPF Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive DPF Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive DPF Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive DPF Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive DPF Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive DPF Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive DPF Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive DPF Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive DPF Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive DPF Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive DPF Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive DPF Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive DPF Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive DPF Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive DPF Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive DPF Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive DPF Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive DPF Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive DPF Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive DPF Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive DPF Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive DPF Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive DPF Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive DPF Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive DPF Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive DPF Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive DPF Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive DPF?

The projected CAGR is approximately 16.63%.

2. Which companies are prominent players in the Automotive DPF?

Key companies in the market include Corning, NGK Insulators, Faurecia, Tenneco, Johnson Matthey, Katcon, Umicore, Bekaert.

3. What are the main segments of the Automotive DPF?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.98 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive DPF," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive DPF report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive DPF?

To stay informed about further developments, trends, and reports in the Automotive DPF, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence