Key Insights

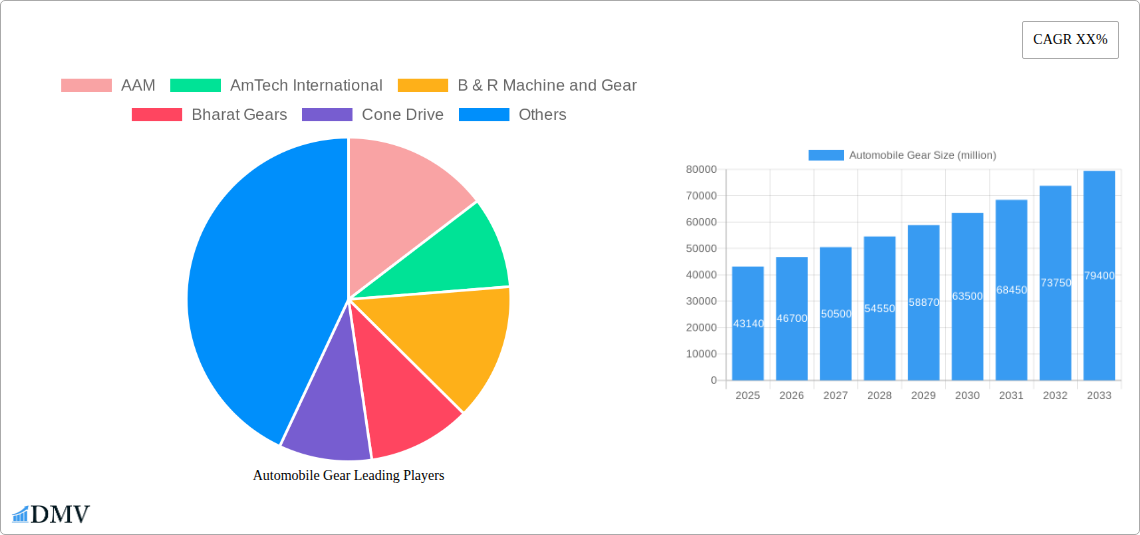

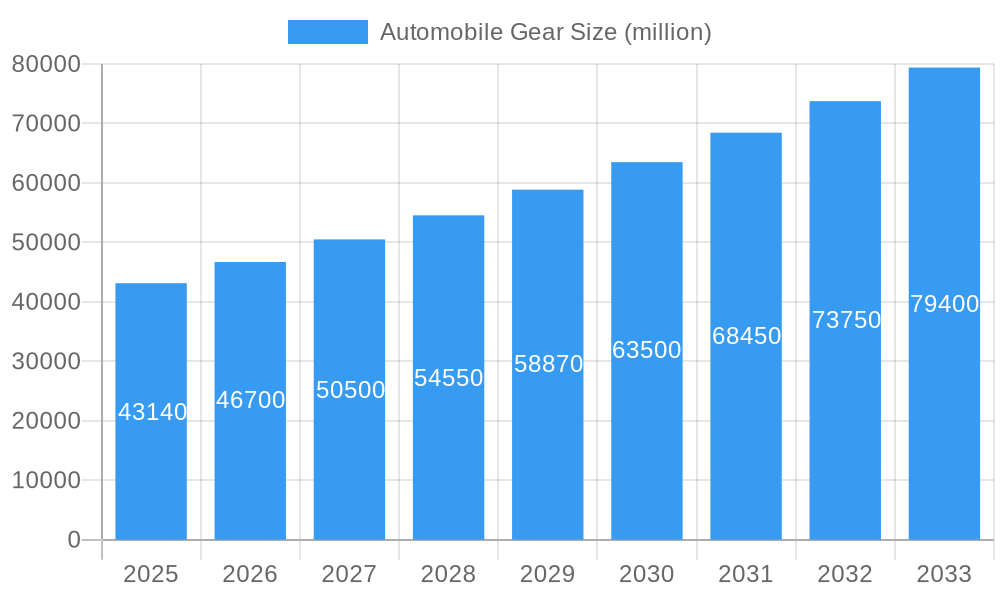

The global Automobile Gear market is poised for substantial growth, projected to reach USD 43.14 billion by 2025, with an impressive CAGR of 57.44% during the forecast period of 2019-2033. This rapid expansion is primarily fueled by the burgeoning automotive industry, driven by increasing vehicle production worldwide, particularly in emerging economies. The escalating demand for passenger cars and commercial vehicles, coupled with advancements in automotive technology such as electric and hybrid powertrains, necessitates the development of more sophisticated and durable gear systems. The increasing complexity of vehicle transmissions, including the growing adoption of automatic and continuously variable transmissions (CVTs), further stimulates the demand for specialized gears. Furthermore, the constant push for improved fuel efficiency and reduced emissions is compelling manufacturers to invest in lightweight and high-performance gear materials and designs, contributing significantly to market growth.

Automobile Gear Market Size (In Billion)

The market segmentation highlights the diverse applications and types of gears influencing this dynamic landscape. The dominant application segments include Passenger Cars and Commercial Vehicles, reflecting the sheer volume of production in these areas. Within types, Skew Shaft Gears, Intersecting Shaft Gears, and Parallel Shaft Gears all play crucial roles in various drivetrain configurations. Key players like AAM, Bosch, ZF TRW, and GKN are at the forefront of innovation, developing advanced gear solutions that enhance performance, durability, and efficiency. The market's trajectory is also shaped by the ongoing trends towards electrification, autonomous driving, and smart manufacturing, all of which require specialized gear components. While the market is robust, potential restraints such as raw material price volatility and the high cost of advanced manufacturing technologies could present challenges, but the overarching growth drivers are expected to outweigh these concerns, ensuring a prosperous future for the automobile gear industry.

Automobile Gear Company Market Share

Automobile Gear Market Composition & Trends

The global automobile gear market, valued at over 1.5 billion in the base year 2025, is characterized by a dynamic blend of established players and emerging innovators. Market concentration is moderately high, with key companies like ZF TRW, Bosch, and AAM holding significant market share, estimated to be over 60% combined. Innovation is primarily driven by the relentless pursuit of higher fuel efficiency, reduced emissions, and enhanced vehicle performance. Regulatory landscapes, particularly stricter emission standards and safety mandates, are powerful catalysts for gear technology advancements. Substitute products, such as continuously variable transmissions (CVTs) and electric vehicle (EV) powertrains, pose a growing challenge, compelling traditional gear manufacturers to adapt. End-user profiles are diversifying, encompassing the burgeoning demand for electric and hybrid vehicles alongside the continued strength of the passenger car and commercial vehicle segments. Mergers and acquisitions are a significant feature, with recent deals valued at over 2.2 billion, aimed at consolidating market presence, acquiring new technologies, and expanding geographical reach.

- Market Share Distribution (2025):

- ZF TRW: 22.5%

- Bosch: 21.0%

- AAM: 18.0%

- GKN: 10.5%

- Others: 28.0%

- M&A Deal Values (Historical 2019-2024):

- Average Annual Deal Value: 350 million

- Total Deal Value (2019-2024): 2.1 billion

- Key Innovation Catalysts:

- Stricter emission standards (Euro 7, CAFE)

- Electrification of powertrains

- Demand for lightweight and durable gear solutions

- Advancements in materials science and manufacturing processes

Automobile Gear Industry Evolution

The automobile gear industry has undergone a profound transformation, driven by technological evolution and shifting market demands. Over the historical period from 2019 to 2024, the market witnessed a steady growth trajectory, with an average annual growth rate of 4.8%. This growth was primarily fueled by the robust performance of the global automotive sector, particularly in emerging economies. Technological advancements have been at the forefront of this evolution. Manufacturers have shifted from traditional steel gears to more advanced materials like forged alloys and composites, enhancing strength-to-weight ratios and reducing wear. The introduction of precision manufacturing techniques, such as hobbing, grinding, and lapping, has led to improved gear accuracy, reduced noise, and increased efficiency. The increasing complexity of transmissions, including the move towards multi-speed automatic transmissions and the integration of hybrid powertrains, has necessitated the development of highly specialized and durable gears.

The base year 2025 is projected to see the market value reaching 1.5 billion, with a projected compound annual growth rate (CAGR) of 5.2% during the forecast period of 2025–2033. This sustained growth is underpinned by several key trends. The electrification of vehicles, while initially perceived as a threat, is now a significant growth driver. Electric vehicles still require reduction gears to transmit power from the electric motor to the wheels, and these gears often demand higher precision and torque density. Consequently, there's a growing demand for specialized EV gears, including those with optimized tooth profiles and materials for silent operation and extended lifespan. Furthermore, advancements in digital manufacturing and Industry 4.0 principles are revolutionizing production processes. The adoption of AI-driven design, simulation, and automated quality control is leading to faster development cycles, reduced production costs, and higher product reliability. Consumer demand for smoother, quieter, and more fuel-efficient vehicles continues to push the boundaries of gear technology, encouraging the development of innovative gear designs and manufacturing processes that minimize friction and power loss. The integration of smart technologies, such as sensors within gearboxes for predictive maintenance, is also an emerging trend that will shape the future of the industry.

- Historical Market Growth (2019-2024):

- Average Annual Growth Rate: 4.8%

- Total Market Value (2019): ~1.2 billion

- Total Market Value (2024): ~1.48 billion

- Projected Market Growth (2025-2033):

- Projected CAGR: 5.2%

- Projected Market Value (2033): ~2.2 billion

- Key Technological Advancements:

- Advanced materials: Forged alloys, composites, high-strength steels.

- Precision manufacturing: Hobbing, grinding, lapping, shot peening.

- Gear design: Optimized tooth profiles, helical gears, hypoid gears.

- EV-specific gears: High torque density, low noise, lightweight designs.

Leading Regions, Countries, or Segments in Automobile Gear

The automobile gear market's dominance is intricately linked to the global automotive production landscape. In the Application segment, Passenger Car remains the leading segment, driven by the sheer volume of vehicles produced worldwide. However, the Commercial Vehicle segment is exhibiting a robust growth rate, fueled by increasing logistics demands and the growing adoption of advanced powertrains in heavy-duty applications. Analyzing by Type, Parallel Shaft Gears are the most prevalent, forming the backbone of most traditional transmissions. Skew Shaft Gears, particularly hypoid gears, are crucial for rear-wheel-drive and all-wheel-drive systems.

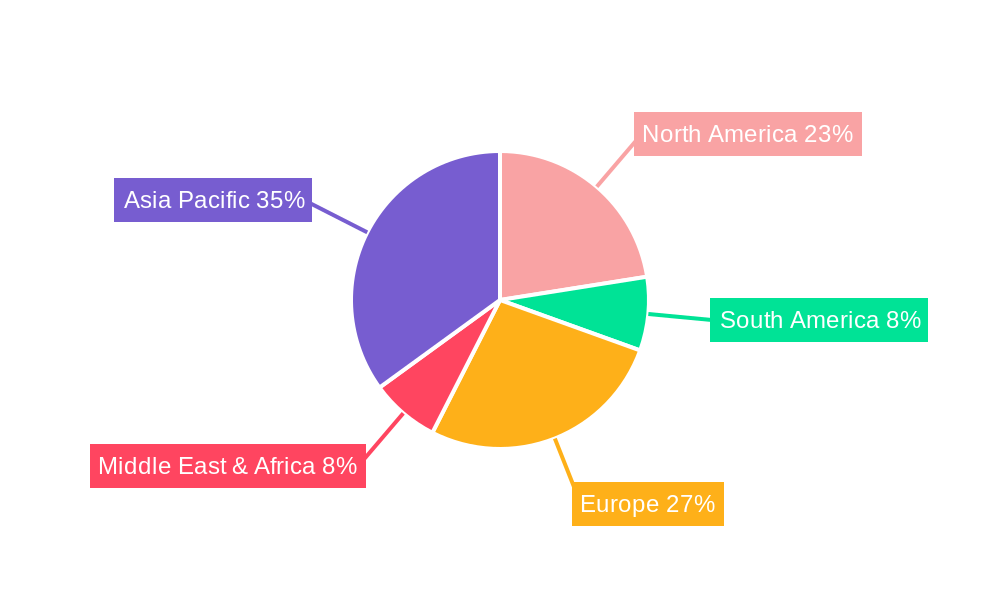

Geographically, Asia Pacific stands out as the dominant region, accounting for over 45% of the global automobile gear market share in the base year 2025. This dominance is primarily attributed to the massive automotive manufacturing hubs in China, India, Japan, and South Korea. The region benefits from a strong manufacturing ecosystem, growing domestic demand for vehicles, and significant investments in automotive R&D. China, in particular, is a powerhouse, not only in production volume but also in the adoption of advanced gear technologies, especially for EVs.

Within Asia Pacific, countries like China and India are significant growth engines. China's vast passenger car and electric vehicle market, coupled with its strong manufacturing capabilities, positions it as a leader. India's rapidly expanding automotive sector, with a growing middle class and increasing demand for both passenger and commercial vehicles, further bolsters the region's position.

Key drivers for this dominance include:

- Massive Production Volumes: Asia Pacific is home to the world's largest automotive manufacturers, leading to a sustained demand for automobile gears.

- Growing EV Adoption: The region is at the forefront of electric vehicle adoption, creating a surge in demand for specialized EV gears.

- Cost-Effective Manufacturing: Favorable manufacturing costs and a skilled labor force contribute to the region's competitive advantage.

- Government Support and Incentives: Many governments in Asia Pacific actively promote the automotive industry through favorable policies and incentives, further stimulating the demand for automobile gears.

- Technological Advancements: Leading companies in the region are investing heavily in R&D to develop next-generation gear technologies, including those for advanced driver-assistance systems (ADAS) and autonomous vehicles.

The Passenger Car application segment is expected to continue its stronghold, projected to account for 60% of the market share in 2025. However, the Commercial Vehicle segment's CAGR is estimated at 5.5%, driven by global trade and infrastructure development. Parallel Shaft Gears will remain dominant with a market share of 55%, while Skew Shaft Gears will see steady growth due to their application in performance vehicles and SUVs.

Automobile Gear Product Innovations

The automobile gear industry is abuzz with innovative product developments focused on enhancing efficiency, durability, and performance. Manufacturers are increasingly leveraging advanced materials like high-strength steels and composite alloys to create lighter yet stronger gears, contributing to improved fuel economy. Precision engineering techniques, including digital simulation and advanced manufacturing processes, are yielding gears with optimized tooth profiles and surface treatments that significantly reduce friction and noise. Innovations in gear design for electric vehicles are paramount, with a focus on high-torque density and silent operation, often employing helical and spur gear configurations tailored for electric powertrains. Performance metrics such as increased load-carrying capacity, extended lifespan (over 150,000 miles), and reduced rotational losses are key indicators of these advancements, ensuring these gears meet the demanding requirements of modern automotive applications.

Propelling Factors for Automobile Gear Growth

The automobile gear market's growth is propelled by a confluence of technological, economic, and regulatory factors. The accelerating transition towards electric vehicles (EVs) is a monumental driver, as EVs still necessitate sophisticated reduction gears to manage motor torque. Stricter global emission standards (e.g., Euro 7, CAFE) compel manufacturers to develop more fuel-efficient powertrains, which in turn demands more efficient and lighter gears. Economic growth in emerging markets, leading to increased vehicle sales, directly translates to higher demand for automotive gears. Furthermore, technological advancements in manufacturing processes, such as additive manufacturing and advanced surface treatments, are enabling the production of higher-performance, more cost-effective gears.

- Key Growth Drivers:

- Electrification of Vehicles: Demand for EV reduction gears is surging.

- Stringent Emission Regulations: Driving the need for fuel-efficient transmission components.

- Economic Development in Emerging Markets: Increasing vehicle ownership and production.

- Technological Advancements: Improved manufacturing and material science.

Obstacles in the Automobile Gear Market

Despite robust growth, the automobile gear market faces several significant obstacles. The escalating cost of raw materials, particularly specialty steels and rare earth elements used in advanced alloys, presents a considerable challenge, impacting profit margins and potentially increasing end-product prices. Supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can lead to production delays and increased lead times for critical components. The intense competition within the market, especially from lower-cost manufacturers in developing regions, puts pressure on pricing and forces continuous innovation to maintain market share. Furthermore, the evolving landscape of automotive powertrains, with the long-term potential for even more radical shifts away from traditional transmissions, creates an element of uncertainty for long-term investment strategies.

- Key Restraints:

- Volatile Raw Material Prices: Fluctuations in steel and alloy costs.

- Global Supply Chain Disruptions: Leading to production delays and increased lead times.

- Intense Market Competition: Price pressures and the need for differentiation.

- Technological Obsolescence Risk: Potential for rapid shifts in powertrain technology.

Future Opportunities in Automobile Gear

The future of the automobile gear market is ripe with opportunities. The exponential growth of the electric vehicle sector presents a significant avenue, with a rising demand for highly specialized EV reduction gears, including those for dual-motor and tri-motor configurations. The development of advanced driver-assistance systems (ADAS) and autonomous driving technologies will necessitate new types of gears for actuator systems and precision steering mechanisms. Furthermore, the growing trend towards mobility-as-a-service (MaaS) and shared mobility solutions could lead to new requirements for highly durable and low-maintenance gear systems. Exploring new markets in regions with rapidly expanding automotive industries and investing in research for next-generation gear materials and manufacturing techniques will be crucial for capturing future growth.

- Emerging Opportunities:

- Growth in EV Gear Market: Specialized reduction gears for electric powertrains.

- ADAS and Autonomous Driving: Gears for control systems and actuators.

- Mobility-as-a-Service (MaaS): Demand for durable and low-maintenance gears.

- New Geographic Markets: Expansion into rapidly developing automotive regions.

Major Players in the Automobile Gear Ecosystem

- AAM

- AmTech International

- B & R Machine and Gear

- Bharat Gears

- Bosch

- Cone Drive

- Dynamatic Technologies

- Franz Morat

- GKN

- Gleason Plastic Gears

- IMS Gear

- RSB

- Showa

- Taiwan United Gear

- Universal Auto Gears

- ZF TRW

Key Developments in Automobile Gear Industry

- 2023 October: ZF TRW launched a new generation of lightweight gears for hybrid and electric powertrains, offering improved efficiency and reduced NVH (Noise, Vibration, and Harshness).

- 2023 September: AAM announced a strategic partnership with an EV startup to develop specialized gear sets for next-generation electric vehicles, projecting a market value of over 500 million in new contracts.

- 2023 July: Bosch showcased its advanced gear manufacturing capabilities at an industry exhibition, highlighting its investment of over 750 million in R&D for precision gears.

- 2023 April: GKN acquired a smaller, specialized gear manufacturer, expanding its portfolio in performance and high-precision automotive gears, with a deal value estimated at 300 million.

- 2023 February: Gleason Plastic Gears introduced a new high-performance polymer gear material designed for extreme temperature applications in EVs, aiming to capture 15% of the plastic gear market.

- 2022 November: Cone Drive expanded its manufacturing facility in the US, investing 200 million to boost production capacity for industrial and automotive gears.

- 2022 July: Dynamatic Technologies secured a significant order from a major European automaker for transmission gears, valued at approximately 400 million over five years.

Strategic Automobile Gear Market Forecast

The strategic automobile gear market forecast indicates sustained and robust growth, driven by the unstoppable momentum of vehicle electrification and increasingly stringent environmental regulations. The ongoing demand for enhanced fuel efficiency and reduced emissions in internal combustion engine vehicles will continue to fuel innovation in traditional gear technologies. Emerging markets are poised to become significant contributors to growth, owing to increasing disposable incomes and a burgeoning middle class driving vehicle ownership. Investments in advanced manufacturing techniques, including Industry 4.0 principles and AI-driven design, will be critical for manufacturers to maintain a competitive edge and capitalize on the expanding opportunities in the global automobile gear landscape, projected to reach over 2.2 billion by 2033.

Automobile Gear Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Skew Shaft Gears

- 2.2. Intersecting Shaft Gear

- 2.3. Parallel Shaft Gears

Automobile Gear Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automobile Gear Regional Market Share

Geographic Coverage of Automobile Gear

Automobile Gear REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Skew Shaft Gears

- 5.2.2. Intersecting Shaft Gear

- 5.2.3. Parallel Shaft Gears

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Skew Shaft Gears

- 6.2.2. Intersecting Shaft Gear

- 6.2.3. Parallel Shaft Gears

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Skew Shaft Gears

- 7.2.2. Intersecting Shaft Gear

- 7.2.3. Parallel Shaft Gears

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Skew Shaft Gears

- 8.2.2. Intersecting Shaft Gear

- 8.2.3. Parallel Shaft Gears

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Skew Shaft Gears

- 9.2.2. Intersecting Shaft Gear

- 9.2.3. Parallel Shaft Gears

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automobile Gear Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Skew Shaft Gears

- 10.2.2. Intersecting Shaft Gear

- 10.2.3. Parallel Shaft Gears

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 AAM

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 AmTech International

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 B & R Machine and Gear

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bharat Gears

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Cone Drive

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Dynamatic Technologies

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Franz Morat

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 GKN

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Gleason Plastic Gears

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 IMS Gear

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bosch

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 RSB

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Showa

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Taiwan United Gear

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Universal Auto Gears

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 ZF TRW

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 AAM

List of Figures

- Figure 1: Global Automobile Gear Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automobile Gear Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automobile Gear Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automobile Gear Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Automobile Gear Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automobile Gear Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automobile Gear Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automobile Gear Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automobile Gear Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automobile Gear Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Automobile Gear Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automobile Gear Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automobile Gear Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automobile Gear Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automobile Gear Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automobile Gear Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Automobile Gear Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automobile Gear Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automobile Gear Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automobile Gear Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automobile Gear Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automobile Gear Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automobile Gear Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automobile Gear Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automobile Gear Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automobile Gear Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automobile Gear Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automobile Gear Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Automobile Gear Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automobile Gear Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automobile Gear Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Automobile Gear Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Automobile Gear Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Automobile Gear Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Automobile Gear Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Automobile Gear Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automobile Gear Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automobile Gear Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Automobile Gear Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automobile Gear Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automobile Gear?

The projected CAGR is approximately 5.58%.

2. Which companies are prominent players in the Automobile Gear?

Key companies in the market include AAM, AmTech International, B & R Machine and Gear, Bharat Gears, Cone Drive, Dynamatic Technologies, Franz Morat, GKN, Gleason Plastic Gears, IMS Gear, Bosch, RSB, Showa, Taiwan United Gear, Universal Auto Gears, ZF TRW.

3. What are the main segments of the Automobile Gear?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automobile Gear," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automobile Gear report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automobile Gear?

To stay informed about further developments, trends, and reports in the Automobile Gear, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence