Key Insights

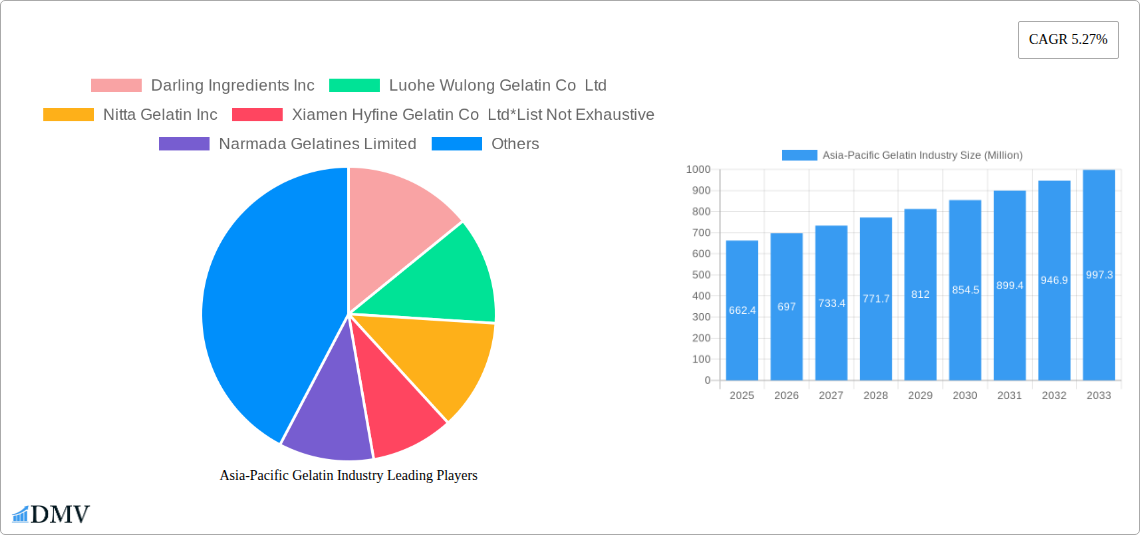

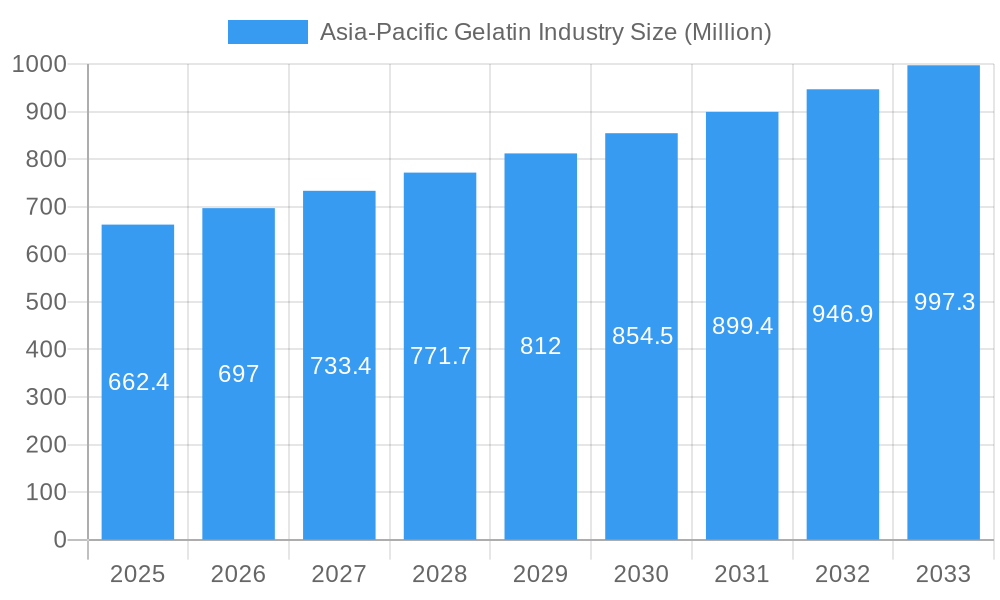

The Asia-Pacific Gelatin Industry is poised for significant growth, projected to reach a substantial market size of $662.4 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 5.27% through 2033. This robust expansion is fueled by a confluence of powerful market drivers, including the escalating demand for natural and functional ingredients across diverse end-use sectors. The personal care and cosmetics industry, in particular, is a key beneficiary, leveraging gelatin's emulsifying, stabilizing, and skin-conditioning properties in a wide array of premium products. Simultaneously, the food and beverage sector, encompassing bakery, confectionery, sauces, beverages, dairy products, snacks, and ready-to-eat/ready-to-cook items, is increasingly incorporating gelatin for its gelling, thickening, and nutritional benefits. This broad applicability, coupled with a growing consumer preference for clean-label products and naturally derived ingredients, is significantly propelling market penetration. Emerging trends such as the development of specialized gelatin derivatives for pharmaceutical applications and advancements in sustainable sourcing and production techniques are further shaping the industry's trajectory, ensuring continued innovation and market expansion.

Asia-Pacific Gelatin Industry Market Size (In Million)

The competitive landscape is characterized by the presence of both established global players and emerging regional manufacturers, all vying for market share. Companies like Darling Ingredients Inc., Nitta Gelatin Inc., and GELITA AG are at the forefront, supported by strategic expansions and product innovations. However, the market also faces certain restraints, including fluctuating raw material prices, stringent regulatory requirements for food and pharmaceutical grade gelatin, and the availability of viable alternatives. Nevertheless, the Asia-Pacific region, driven by burgeoning economies like China and India with their rapidly growing middle class and increasing disposable incomes, presents immense opportunities. China, in particular, is a dominant force due to its extensive manufacturing capabilities and substantial domestic consumption, while India's expanding food processing industry and growing health consciousness contribute significantly to market dynamics. The strategic focus on product differentiation, quality assurance, and exploring new applications will be crucial for stakeholders aiming to capitalize on the sustained growth of this dynamic market.

Asia-Pacific Gelatin Industry Company Market Share

Dive deep into the dynamic Asia-Pacific gelatin market with this in-depth report, meticulously analyzing its current landscape and forecasting future trajectories. Covering the extensive study period of 2019–2033, with a base year and estimated year of 2025, this report provides unparalleled insights for stakeholders. Explore the burgeoning demand for animal-based gelatin and the emerging potential of marine-based gelatin, alongside its critical role in sectors like Personal Care and Cosmetics and the vast Food and Beverage industry, encompassing Bakery, Confectionery, Condiments/Sauces, Beverages, Dairy and Dairy Alternative Products, Snacks, and RTE/RTC Food Products. Uncover the competitive strategies and market penetration across key geographies including China, India, Australia, Japan, and the Rest of Asia Pacific. This report is your indispensable guide to understanding market composition, key trends, industry evolution, leading segments, groundbreaking innovations, growth drivers, market obstacles, future opportunities, major players, pivotal developments, and a strategic market forecast.

Asia-Pacific Gelatin Industry Market Composition & Trends

The Asia-Pacific gelatin market, a critical component of the global nutraceutical and food ingredient supply chain, is characterized by a moderate to high concentration, with a few dominant players holding significant market share. Innovation remains a key catalyst, driven by advancements in processing technologies and the development of specialized gelatin grades for diverse applications. The regulatory landscape is evolving, with increasing emphasis on food safety standards, traceability, and sustainability, particularly concerning animal-derived products. While animal-based gelatin continues to dominate, the exploration of marine-based gelatin as a sustainable alternative is gaining traction, though it faces technological hurdles and consumer perception challenges. End-user profiles are becoming more sophisticated, demanding customized solutions with specific functionalities, such as enhanced gelling, emulsification, and texturization properties. Mergers and acquisitions (M&A) activity, while not currently at a fever pitch, is expected to increase as larger companies seek to consolidate their market positions and acquire innovative technologies or expand their geographic reach. For instance, M&A deals in the broader food ingredients sector have averaged values of $XX Million over the historical period, indicating potential investment avenues. Key market share distribution reveals China as a leading producer and consumer, followed closely by India, showcasing their significant contributions to the animal-based gelatin segment within the Food and Beverage sector.

Asia-Pacific Gelatin Industry Industry Evolution

The Asia-Pacific gelatin industry has undergone a significant transformation over the historical period of 2019–2024, marked by consistent growth trajectories and an increasing reliance on technological advancements. The market has witnessed an average annual growth rate of approximately 6.5%, driven by a confluence of factors including rising disposable incomes, evolving dietary preferences, and expanding applications across diverse sectors. Early in the historical period, the industry was primarily focused on providing standard gelatin for traditional uses in confectionery and pharmaceuticals. However, consumer demand has shifted dramatically, pushing manufacturers towards higher-value, specialized gelatin products. This evolution is evident in the adoption of advanced processing techniques that enable the production of gelatin with tailored functionalities, such as controlled gelling times, improved clarity, and enhanced nutritional profiles.

Technological advancements have been instrumental in this evolutionary path. The implementation of sophisticated extraction and purification processes has not only improved product quality but also enhanced production efficiency, contributing to cost-effectiveness. Furthermore, the integration of smart manufacturing practices, including automation and data analytics, has allowed for greater precision in production and better quality control, meeting stringent international standards. The Food and Beverage segment, in particular, has been a major driver of this evolution. Within this, confectionery and bakery applications have historically dominated, but the demand for gelatin in dairy and dairy alternative products, beverages, and RTE/RTC food products has surged. This surge is fueled by the growing trend towards convenience foods and the desire for texture and mouthfeel enhancement in these products.

Consumer demand for healthier and more functional food ingredients has also played a pivotal role. Manufacturers have responded by developing gelatin products with improved amino acid profiles and by exploring alternative sources like marine life, though animal-based gelatin derived from bovine and porcine sources remains the market's mainstay. The Personal Care and Cosmetics sector has also contributed to this evolution, with a growing demand for collagen peptides and gelatin derivatives for skincare and anti-aging products. Regulatory bodies have also influenced this evolution by tightening safety and quality standards, prompting manufacturers to invest in research and development to ensure compliance and product superiority. The industry's evolution is thus a testament to its adaptability, driven by technological prowess, changing consumer needs, and a proactive response to the dynamic global market environment.

Leading Regions, Countries, or Segments in Asia-Pacific Gelatin Industry

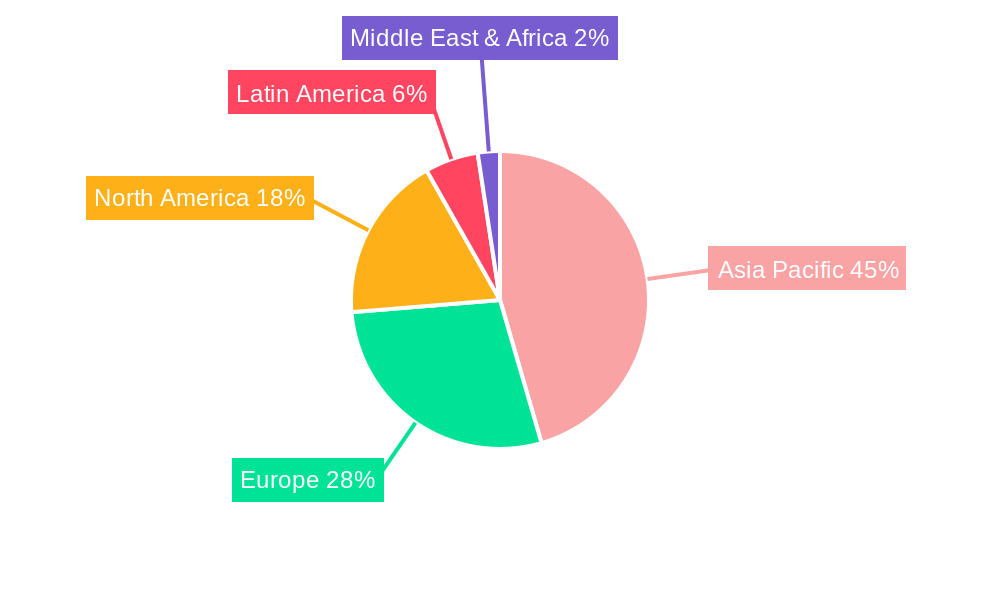

The Asia Pacific region stands as the undisputed leader in the global gelatin market, driven by the immense manufacturing capabilities and burgeoning consumer base within its key economies. Within this vast region, China has emerged as the dominant force, accounting for an estimated 45% of the regional market share. This dominance is attributed to several key drivers:

- Industrial Scale Production: China possesses a vast network of large-scale animal processing facilities, providing a readily available and cost-effective supply of raw materials for gelatin extraction. The presence of numerous gelatin manufacturers, ranging from small to large enterprises, fuels competitive pricing and ample supply.

- Robust Food and Beverage Sector: The sheer size of China's Food and Beverage industry is a colossal consumption engine. The thriving confectionery sector, a traditional stronghold for gelatin, coupled with the rapidly growing demand for gelatin in bakery goods, dairy and dairy alternative products, and functional beverages, solidifies China's leading position. The increasing adoption of RTE/RTC food products further amplifies gelatin's utility.

- Growing Pharmaceutical and Nutraceutical Demand: Beyond food, China's expanding pharmaceutical and nutraceutical industries represent a significant demand for high-purity gelatin, primarily for capsules and supplements. This segment, while smaller than food, is a high-value contributor.

- Government Support and Infrastructure: While direct subsidies for gelatin production might be limited, the Chinese government's overarching support for its manufacturing sector, coupled with advanced logistics and infrastructure, facilitates efficient production and distribution.

Following closely behind China, India has established itself as another pivotal market, securing approximately 25% of the regional share. India's strength lies in:

- Abundant Raw Material Availability: Similar to China, India has a substantial livestock population, providing a rich source for animal-based gelatin. The country's traditional meat processing industry is a cornerstone of this supply.

- Expanding Food Processing Industry: India's food processing sector is witnessing exponential growth. The increasing disposable incomes and changing lifestyles have boosted demand for processed foods, with gelatin playing a crucial role in confectionery, bakery, and dairy products.

- Untapped Pharmaceutical Potential: The pharmaceutical industry in India, a global hub for generic drug manufacturing, presents a significant and growing demand for pharmaceutical-grade gelatin.

- Skilled Workforce and Cost-Effectiveness: India benefits from a large, skilled workforce and a comparatively lower production cost, making its gelatin offerings competitive.

The Food and Beverage segment as a whole is the undisputed leader across the Asia-Pacific region, driven by its widespread application and immense consumption volumes. Within this segment, Confectionery applications consistently hold the largest market share, estimated at around 30%, due to gelatin's essential role in creating desirable textures, chewiness, and clarity in candies, gummies, and chocolates. Bakery applications follow, contributing roughly 20%, where gelatin is used for gelling, stabilization, and improving the texture of cakes, pastries, and bread fillings. The Dairy and Dairy Alternative Products segment is experiencing rapid growth, projected to capture 15% of the market share, driven by the use of gelatin in yogurts, desserts, and plant-based dairy alternatives for texture and stability. Beverages contribute approximately 10%, with gelatin used in clarity enhancement and as a clarifying agent. Snacks and RTE/RTC Food Products collectively account for the remaining 25%, with gelatin utilized for texture modification, binding, and as a functional ingredient in various convenient food items. The Personal Care and Cosmetics segment, while smaller in volume, is a significant contributor in terms of value, particularly with the rising popularity of collagen-based skincare products.

Asia-Pacific Gelatin Industry Product Innovations

The Asia-Pacific gelatin industry is witnessing a surge in product innovations, focusing on enhanced functionality and sustainability. Manufacturers are developing specialized gelatin grades with precise gelling temperatures, bloom strengths, and viscosity profiles to cater to niche applications in food, pharmaceuticals, and cosmetics. A key innovation is the development of low-molecular-weight collagen peptides and hydrolyzed gelatin, offering improved bioavailability and absorption for nutraceutical products and skincare formulations. Furthermore, advancements in extraction and purification techniques are leading to gelatin with reduced odor and improved clarity, enhancing its appeal in high-end food products. The introduction of texturizing gelatin solutions, like PB Leiner's TEXTURA Tempo Ready, exemplifies innovation aimed at improving culinary experiences with intense flavor and exceptional stability.

Propelling Factors for Asia-Pacific Gelatin Industry Growth

Several key factors are propelling the growth of the Asia-Pacific gelatin industry. Firstly, the burgeoning middle class across the region, particularly in China and India, has led to increased disposable incomes, fueling demand for processed foods, confectionery, and health supplements, all significant consumers of gelatin. Secondly, the expanding pharmaceutical and nutraceutical sectors are driving demand for high-purity gelatin for capsules, tablets, and dietary supplements. Technological advancements in production processes are improving efficiency and enabling the creation of specialized gelatin grades, thereby expanding application possibilities. Finally, favorable government initiatives promoting food processing and healthcare infrastructure development in several Asia-Pacific countries further bolster the market's expansion.

Obstacles in the Asia-Pacific Gelatin Industry Market

Despite its robust growth, the Asia-Pacific gelatin industry faces several obstacles. Stringent regulatory requirements and evolving food safety standards across different countries can pose compliance challenges for manufacturers, particularly for smaller players. Fluctuations in the prices and availability of raw materials, primarily collagen-rich animal by-products, due to factors like disease outbreaks or shifts in agricultural practices, can impact production costs and supply chain stability. Furthermore, the growing consumer preference for vegetarian and vegan alternatives in food and cosmetics presents a competitive threat, necessitating innovation in non-animal-derived gelling agents. Intense competition among numerous regional and international players can also lead to price pressures and affect profit margins.

Future Opportunities in Asia-Pacific Gelatin Industry

Emerging opportunities in the Asia-Pacific gelatin industry are diverse and promising. The escalating demand for clean-label and natural ingredients presents a significant opportunity for gelatin producers who can emphasize its natural origin and minimal processing. The expanding health and wellness trend is driving growth in the nutraceutical sector, creating demand for specialized collagen peptides and gelatin for sports nutrition, anti-aging, and joint health products. Furthermore, the growing interest in sustainable and ethically sourced ingredients opens avenues for gelatin derived from more sustainable sources or produced through environmentally conscious processes. The increasing adoption of gelatin in non-traditional applications, such as edible films and biodegradable packaging, also signifies untapped market potential.

Major Players in the Asia-Pacific Gelatin Industry Ecosystem

- Darling Ingredients Inc.

- Luohe Wulong Gelatin Co Ltd

- Nitta Gelatin Inc.

- Xiamen Hyfine Gelatin Co Ltd

- Narmada Gelatines Limited

- Asahi Gelatine Industrial Co Ltd

- GELITA AG

- Foodchem International Corporation

- Jellice Group

- India Gelatine & Chemicals Ltd

- Italgelatine SpA

Key Developments in Asia-Pacific Gelatin Industry Industry

- November 2022: PB Leiner, a subsidiary of Tessenderlo Group, unveiled TEXTURA Tempo Ready, a cutting-edge texturizing gelatin solution for the food service industry, packaged for culinary professionals and promising enhanced flavor, mouthfeel, and stability.

- May 2021: Darling Ingredients Inc. expanded its Rousselot brand portfolio with the launch of X-Pure® GelDAT, a meticulously purified, pharmaceutical-grade, and modified gelatin, reinforcing its commitment to high-quality products.

- January 2021: Nitta Gelatin India introduced a superior-grade gelatin for the Hotel/Restaurant/Catering (HoReCa) sector, manufactured using advanced Japanese technology and adhering to stringent GMP, HACCP, and European hygiene standards.

Strategic Asia-Pacific Gelatin Industry Market Forecast

The strategic forecast for the Asia-Pacific gelatin market anticipates sustained robust growth, driven by the confluence of evolving consumer lifestyles and continuous technological innovation. The increasing demand for convenient and healthy food products will continue to fuel the Food and Beverage sector's reliance on gelatin for texture, stabilization, and gelling properties, particularly in confectionery, bakery, and dairy alternatives. The expanding pharmaceutical and nutraceutical industries, driven by an aging population and a growing emphasis on preventive healthcare, will significantly boost the demand for high-purity, specialized gelatin. Furthermore, the push towards sustainable and clean-label ingredients presents a substantial opportunity for manufacturers to differentiate their offerings and capture market share. Emerging markets within the Rest of Asia Pacific are also poised for significant growth, presenting new frontiers for market penetration and strategic expansion.

Asia-Pacific Gelatin Industry Segmentation

-

1. Form

- 1.1. Animal Based

- 1.2. Marine Based

-

2. End -ser

- 2.1. Personal Care and Cosmetics

-

2.2. Food and Beverage

- 2.2.1. Bakery

- 2.2.2. Confectionery

- 2.2.3. Condiments/Sauces

- 2.2.4. Beverages

- 2.2.5. Dairy and Dairy Alternative Products

- 2.2.6. Snacks

- 2.2.7. RTE/RTC Food Products

-

3. Geography

-

3.1. Asia Pacific

- 3.1.1. China

- 3.1.2. India

- 3.1.3. Australia

- 3.1.4. Japan

- 3.1.5. Rest of Asia Pacific

-

3.1. Asia Pacific

Asia-Pacific Gelatin Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Australia

- 1.4. Japan

- 1.5. Rest of Asia Pacific

Asia-Pacific Gelatin Industry Regional Market Share

Geographic Coverage of Asia-Pacific Gelatin Industry

Asia-Pacific Gelatin Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.27% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Low-Fat and Fat-Free Food Products; Expanding Cosmetic and Personal Care Industries Utilize Gelatin for Various Purposes

- 3.3. Market Restrains

- 3.3.1. Fluctuations in Raw Material Proces Affecting Production Costs

- 3.4. Market Trends

- 3.4.1. Increasing Demand for Low-Fat and Fat-Free Food Products

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia-Pacific Gelatin Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Form

- 5.1.1. Animal Based

- 5.1.2. Marine Based

- 5.2. Market Analysis, Insights and Forecast - by End -ser

- 5.2.1. Personal Care and Cosmetics

- 5.2.2. Food and Beverage

- 5.2.2.1. Bakery

- 5.2.2.2. Confectionery

- 5.2.2.3. Condiments/Sauces

- 5.2.2.4. Beverages

- 5.2.2.5. Dairy and Dairy Alternative Products

- 5.2.2.6. Snacks

- 5.2.2.7. RTE/RTC Food Products

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Asia Pacific

- 5.3.1.1. China

- 5.3.1.2. India

- 5.3.1.3. Australia

- 5.3.1.4. Japan

- 5.3.1.5. Rest of Asia Pacific

- 5.3.1. Asia Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Form

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Darling Ingredients Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Luohe Wulong Gelatin Co Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Nitta Gelatin Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Xiamen Hyfine Gelatin Co Ltd*List Not Exhaustive

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Narmada Gelatines Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Asahi Gelatine Industrial Co Ltd

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 GELITA AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Foodchem International Corporation

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Jellice Group

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 India Gelatine & Chemicals Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Italgelatine SpA

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Darling Ingredients Inc

List of Figures

- Figure 1: Asia-Pacific Gelatin Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Gelatin Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 2: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Form 2020 & 2033

- Table 3: Asia-Pacific Gelatin Industry Revenue Million Forecast, by End -ser 2020 & 2033

- Table 4: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by End -ser 2020 & 2033

- Table 5: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 6: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 7: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 10: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Form 2020 & 2033

- Table 11: Asia-Pacific Gelatin Industry Revenue Million Forecast, by End -ser 2020 & 2033

- Table 12: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by End -ser 2020 & 2033

- Table 13: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 14: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 15: Asia-Pacific Gelatin Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia-Pacific Gelatin Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: China Asia-Pacific Gelatin Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia-Pacific Gelatin Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 19: India Asia-Pacific Gelatin Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: India Asia-Pacific Gelatin Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 21: Australia Asia-Pacific Gelatin Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Australia Asia-Pacific Gelatin Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 23: Japan Asia-Pacific Gelatin Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Japan Asia-Pacific Gelatin Industry Volume (K Tons) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacific Asia-Pacific Gelatin Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Rest of Asia Pacific Asia-Pacific Gelatin Industry Volume (K Tons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Gelatin Industry?

The projected CAGR is approximately 5.27%.

2. Which companies are prominent players in the Asia-Pacific Gelatin Industry?

Key companies in the market include Darling Ingredients Inc, Luohe Wulong Gelatin Co Ltd, Nitta Gelatin Inc, Xiamen Hyfine Gelatin Co Ltd*List Not Exhaustive, Narmada Gelatines Limited, Asahi Gelatine Industrial Co Ltd, GELITA AG, Foodchem International Corporation, Jellice Group, India Gelatine & Chemicals Ltd, Italgelatine SpA.

3. What are the main segments of the Asia-Pacific Gelatin Industry?

The market segments include Form, End -ser, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 662.4 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Low-Fat and Fat-Free Food Products; Expanding Cosmetic and Personal Care Industries Utilize Gelatin for Various Purposes.

6. What are the notable trends driving market growth?

Increasing Demand for Low-Fat and Fat-Free Food Products.

7. Are there any restraints impacting market growth?

Fluctuations in Raw Material Proces Affecting Production Costs.

8. Can you provide examples of recent developments in the market?

November 2022: PB Leiner, a subsidiary of Tessenderlo Group, made a significant stride in the food service industry by unveiling TEXTURA Tempo Ready-a cutting-edge texturizing gelatin solution. This innovative product comes conveniently packaged in small pouches and is exclusively distributed to culinary professionals through carefully selected wholesalers. TEXTURA Tempo Ready promises to elevate gastronomic experiences with its remarkable attributes, including intense flavor, exquisite mouthfeel, and exceptional stability over time.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Gelatin Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Gelatin Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Gelatin Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Gelatin Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence