Key Insights

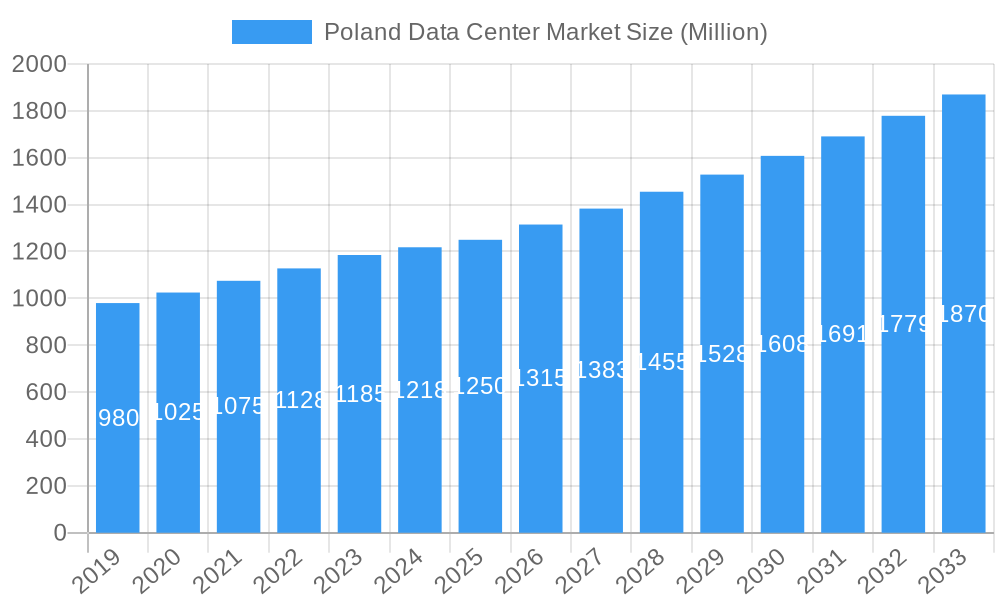

The Poland Data Center Market is projected for substantial growth, expected to reach a market size of $1.16 billion by 2024, exhibiting a robust Compound Annual Growth Rate (CAGR) of 15.68% through the forecast period of 2025-2033. This expansion is driven by increasing digital transformation across sectors, widespread cloud adoption, and a growing demand for hyperscale and colocation facilities. Key factors include significant digital infrastructure investments and Poland's strategic European location, positioning it as a prime hub for data operations and disaster recovery. The market is experiencing heightened demand for large and massive data centers to support hyperscalers and enterprise needs, alongside a strong preference for Tier 3 and Tier 4 facilities driven by security and reliability requirements.

Poland Data Center Market Market Size (In Billion)

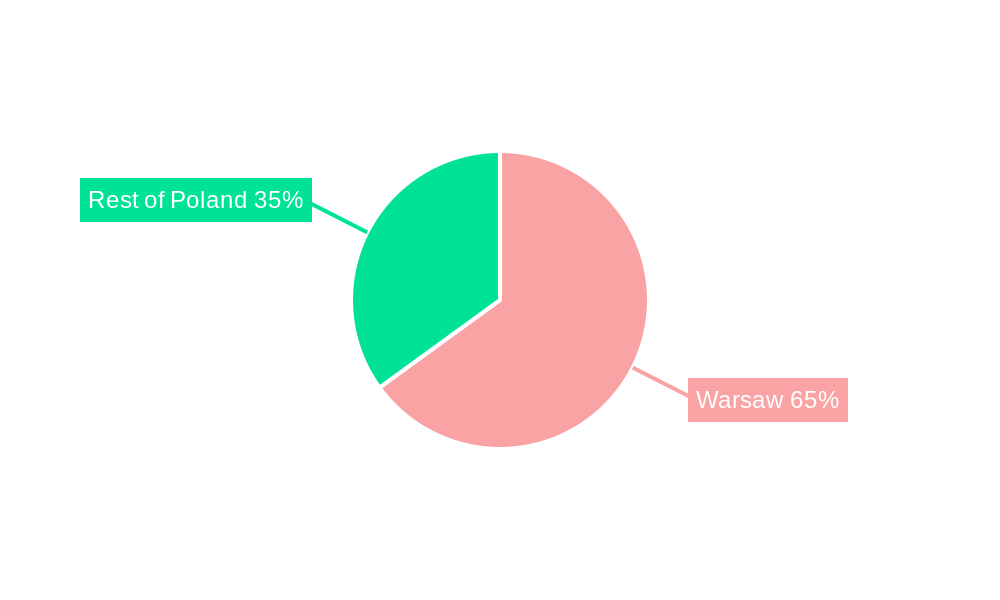

Market segmentation highlights Warsaw as a primary investment and operational center, with 'Rest of Poland' also showing significant growth due to improved connectivity. The BFSI, Cloud, and Telecom sectors lead end-user demand, fueled by data-intensive operations and network expansion. E-commerce and Media & Entertainment sectors are also key contributors. Challenges include high initial capital investment, escalating operational costs, and the need for skilled IT talent. Despite these hurdles, continuous digital evolution and data generation will foster sustained growth and innovation in the Poland Data Center Market.

Poland Data Center Market Company Market Share

Gain comprehensive insights into the Poland data center market with this in-depth, SEO-optimized report. Covering the period from 2019 to 2033, with a base year of 2024 and projections for 2024, this analysis is essential for stakeholders capitalizing on Central Europe's digital transformation. Explore the Poland colocation market, Poland cloud infrastructure, Warsaw data center expansion, and hyperscale data centers in Poland for a granular understanding of market dynamics and future opportunities.

Poland Data Center Market Market Composition & Trends

The Poland data center market is characterized by increasing concentration driven by significant investments from global players and robust domestic growth. Innovation is being catalyzed by the burgeoning demand for cloud services and AI, pushing for advanced infrastructure solutions. The regulatory landscape, while evolving, generally supports foreign investment and technological development. Substitute products, such as on-premise solutions, are gradually losing ground to the scalability and cost-efficiency of colocation and cloud services. End-user profiles are diverse, with BFSI, Cloud, E-Commerce, and Telecom sectors leading adoption. Mergers and Acquisitions (M&A) activities are on the rise, consolidating market share and expanding service offerings. Projected M&A deal values are estimated to reach XX Million within the forecast period. Market share distribution is dynamically shifting, with hyperscale providers capturing a significant portion of new capacity.

- Market Concentration: Growing consolidation due to strategic acquisitions and new entrant investments.

- Innovation Catalysts: Demand for AI, IoT, Big Data, and cloud services driving technological advancements.

- Regulatory Landscape: Favorable policies supporting digital infrastructure development and foreign investment.

- End-User Profiles: BFSI, Cloud, E-Commerce, and Telecom are key drivers of data center utilization.

- M&A Activities: Increasing consolidation for market expansion and service diversification, with projected deal values of XX Million.

Poland Data Center Market Industry Evolution

The Poland data center industry has witnessed remarkable growth and evolution throughout the historical period of 2019-2024, with projected sustained expansion through 2033. This trajectory is fueled by a confluence of factors, including increasing digitalization across all sectors, a surge in data generation, and the strategic positioning of Poland as a digital hub in Eastern Europe. Technological advancements have been swift, with a significant push towards higher density computing, advanced cooling solutions, and enhanced energy efficiency to meet the growing demands of hyperscale clients and enterprise users alike.

The adoption of cloud services has seen exponential growth, transforming how businesses operate and consume IT resources. This shift necessitates robust and scalable data center infrastructure in Poland. The market has moved from basic colocation to sophisticated wholesale and hyperscale solutions, accommodating the needs of major cloud providers and large enterprises. Consumer demand has also evolved, with expectations for faster, more reliable, and secure digital services driving the need for localized data processing and reduced latency. This has directly translated into increased demand for carrier-neutral facilities and edge computing capabilities. The overall growth rate of the Poland data center market has been consistently high, estimated at over XX% CAGR during the historical period, and is projected to continue at a strong pace. Adoption metrics for advanced colocation services are surpassing XX% of enterprise IT budgets.

Leading Regions, Countries, or Segments in Poland Data Center Market

The Poland data center market is dominated by Warsaw as the primary hotspot for data center development and operations. This region's strategic location, robust connectivity, and established digital ecosystem make it the epicenter of colocation and hyperscale investments. The Rest of Poland is also experiencing gradual growth, with emerging hubs developing to serve regional demand and diversify the national data center footprint.

In terms of Data Center Size, Massive and Mega data centers are becoming increasingly prevalent, catering to the needs of hyperscale cloud providers and large enterprises. Large and Medium facilities also play a crucial role, serving a broader range of retail and wholesale colocation customers. The Tier Type landscape is evolving, with a strong focus on Tier 3 and Tier 4 facilities, emphasizing high availability, redundancy, and resilience. While Tier 1 and 2 facilities still exist, the trend is towards more robust and reliable infrastructure.

The Absorption of data center space, particularly Non-Utilized capacity, remains a key indicator of market health, with ongoing development ensuring sufficient space for future demand. Hyperscale colocation is a significant segment, driven by global cloud giants establishing their presence. Wholesale colocation is also a dominant force, serving enterprises requiring significant dedicated space and power. Retail colocation caters to smaller businesses and specific needs.

By End User, Cloud providers are the leading adopters, followed closely by BFSI and E-Commerce sectors, which require high performance and reliability. The Telecom sector also contributes significantly through its demand for network infrastructure and interconnection services. Government and Manufacturing are also growing segments, leveraging data center capabilities for digital transformation and operational efficiency.

- Dominant Region: Warsaw (Hotspot) – Benefitting from connectivity, talent pool, and established digital infrastructure.

- Emerging Segments: Mega and Massive Data Centers – Driven by hyperscale demand.

- Tier Focus: Tier 3 and Tier 4 – Essential for high availability and resilience.

- Absorption Dynamics: Healthy non-utilized capacity to meet future growth.

- Key Colocation Types: Hyperscale and Wholesale – Leading the market in terms of capacity and investment.

- Primary End Users: Cloud, BFSI, E-Commerce, and Telecom – Driving significant demand.

Poland Data Center Market Product Innovations

The Poland data center market is experiencing a wave of product innovations focused on enhancing efficiency, sustainability, and performance. Advancements in cooling technologies, such as liquid cooling solutions for high-density computing, are gaining traction. Innovations in power management, including renewable energy integration and advanced UPS systems, are crucial for meeting sustainability goals and ensuring operational continuity. Furthermore, the development of modular and prefabricated data center designs is accelerating deployment times and offering greater scalability. These innovations are not only improving performance metrics like PUE (Power Usage Effectiveness) to below 1.x, but also offering unique selling propositions for providers to attract environmentally conscious and performance-driven clients.

Propelling Factors for Poland Data Center Market Growth

Several key factors are propelling the Poland data center market forward. The robust growth of the digital economy, driven by increasing internet penetration and mobile device usage, is a primary catalyst. Growing adoption of cloud computing services across industries, including BFSI, e-commerce, and manufacturing, necessitates greater data center capacity. Government initiatives and favorable foreign investment policies are encouraging the development of advanced digital infrastructure. Furthermore, Poland's strategic geographical location, serving as a gateway to Eastern Europe, makes it an attractive hub for data localization and disaster recovery solutions. Technological advancements in areas like AI and IoT are also fueling demand for high-performance computing power, further stimulating market expansion.

- Digital Economy Growth: Increasing internet and mobile penetration.

- Cloud Adoption: Widespread use of cloud services by enterprises.

- Favorable Investment Policies: Government support for digital infrastructure.

- Geographical Advantage: Strategic location for regional connectivity.

- Technological Advancements: Demand for AI and IoT infrastructure.

Obstacles in the Poland Data Center Market Market

Despite the robust growth, the Poland data center market faces certain obstacles. Securing adequate and reliable power supply, especially with the increasing energy demands of large-scale facilities, remains a challenge. Regulatory complexities and the evolving environmental standards can also pose hurdles for new developments and expansions. Competition from established international players and the need for skilled IT professionals to manage advanced infrastructure contribute to operational challenges. Supply chain disruptions for specialized equipment and rising construction costs can impact project timelines and budgets. Furthermore, cybersecurity threats require continuous investment in advanced security measures, adding to operational expenses.

- Power Supply: Ensuring consistent and sufficient energy for expanding facilities.

- Regulatory Hurdles: Navigating evolving environmental and construction regulations.

- Talent Acquisition: Finding and retaining skilled IT professionals.

- Supply Chain Issues: Potential disruptions in equipment delivery.

- Cybersecurity Demands: Ongoing investment in advanced security measures.

Future Opportunities in Poland Data Center Market

The Poland data center market presents significant future opportunities. The continued growth of hyperscale cloud providers expanding their presence in the region offers substantial demand for large-scale facilities. The increasing adoption of edge computing, driven by the need for low-latency applications in sectors like autonomous driving and smart manufacturing, opens new avenues for smaller, distributed data centers. The focus on sustainability and renewable energy sources presents opportunities for developing green data centers, attracting environmentally conscious clients. Furthermore, the ongoing digital transformation of traditional industries like manufacturing and healthcare will create sustained demand for robust and secure data processing and storage solutions. The expansion into nearby markets from a Polish base also represents a strategic growth opportunity.

- Hyperscale Expansion: Continued investment by major cloud providers.

- Edge Computing Growth: Demand for low-latency, distributed infrastructure.

- Green Data Centers: Opportunities in sustainable and renewable energy-powered facilities.

- Industry Digitalization: Sustained demand from traditional sectors.

- Regional Market Expansion: Leveraging Poland as a hub for neighboring countries.

Major Players in the Poland Data Center Market Ecosystem

- Exea p z o o

- Atman Sp z o o

- Sinersio Polska Sp z o o

- Deutsche Telekom AG (T-Mobile Poska SA)

- Equinix Inc

- Comarch SA

- 3S Data Center SA (P4 Sp z o o)

- LIMDC

- Beyond pl Sp z o o

- Vantage Data Centers LLC

- S-NET Sp z o o (TOYA Group)

- Polcom SA

Key Developments in Poland Data Center Market Industry

- December 2022: Atman purchased land, the 5.5-hectare site in Duchnice near Ożarów Mazowiecki, to build another data center. The Atman Data Center Warsaw-3 campus was scheduled to open in Q4 2024 with a target IT capacity of 43 MW.

- August 2022: A new colocation facility would expand Atman Data Center Warsaw-1. The F7 building would have a dedicated power capacity of 7.2 MW for customers’ IT equipment. The new server rooms of 2,916 sq. m were planned to be commissioned in February 2024.

- June 2022: Vantage completed the first facility on its 12-acre (five-hectare) Warsaw campus. Once fully developed, the two-data center campus would offer 48MW of critical IT capacity across 390,000 square feet (36,000 square meters).

Strategic Poland Data Center Market Market Forecast

The strategic outlook for the Poland data center market is exceptionally strong. The market is poised for sustained growth driven by increasing digitalization across all sectors, a burgeoning demand for cloud services, and significant foreign investment. The expansion of hyperscale capabilities and the emerging trend of edge computing will create new avenues for development and innovation. Furthermore, Poland's strategic location within Europe positions it as a critical hub for data localization and regional connectivity, further solidifying its importance in the global data center landscape. The ongoing investments in advanced infrastructure and the commitment to sustainability will ensure Poland remains a competitive and attractive market for data center operations in the coming years, with an estimated market value projected to reach XX Billion by 2033.

Poland Data Center Market Segmentation

-

1. Hotspot

- 1.1. Warsaw

- 1.2. Rest of Poland

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

4.2. By Colocation Type

- 4.2.1. Hyperscale

- 4.2.2. Retail

- 4.2.3. Wholesale

-

4.3. By End User

- 4.3.1. BFSI

- 4.3.2. Cloud

- 4.3.3. E-Commerce

- 4.3.4. Government

- 4.3.5. Manufacturing

- 4.3.6. Media & Entertainment

- 4.3.7. Telecom

- 4.3.8. Other End User

Poland Data Center Market Segmentation By Geography

- 1. Poland

Poland Data Center Market Regional Market Share

Geographic Coverage of Poland Data Center Market

Poland Data Center Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Automation in the Security Screening Industry

- 3.2.2 Especially to Detect Advanced Threats

- 3.2.3 etc.; Upsurge in Terror Activities Across the Region; Increasing Government Initiatives on Security Inspection in Schools and Colleges; Increasing Government Initiatives for Smart Cities

- 3.3. Market Restrains

- 3.3.1 Supply Chain Issues Caused By Geopolitical Scenario and the COVID-19 Pandemic

- 3.3.2 etc.; High Installation and Maintenance Costs

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Data Center Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Warsaw

- 5.1.2. Rest of Poland

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.4.2. By Colocation Type

- 5.4.2.1. Hyperscale

- 5.4.2.2. Retail

- 5.4.2.3. Wholesale

- 5.4.3. By End User

- 5.4.3.1. BFSI

- 5.4.3.2. Cloud

- 5.4.3.3. E-Commerce

- 5.4.3.4. Government

- 5.4.3.5. Manufacturing

- 5.4.3.6. Media & Entertainment

- 5.4.3.7. Telecom

- 5.4.3.8. Other End User

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Exea p z o o

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Atman Sp z o o

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Sinersio Polska Sp z o o

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Deutsche Telekom AG (T-Mobile Poska SA)

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Equinix Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Comarch SA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 3S Data Center SA (P4 Sp z o o)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 LIMDC

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Beyond pl Sp z o o

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Vantage Data Centers LLC5 4 LIST OF COMPANIES STUDIE

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 S-NET Sp z o o (TOYA Group)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Polcom SA

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.1 Exea p z o o

List of Figures

- Figure 1: Poland Data Center Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Data Center Market Share (%) by Company 2025

List of Tables

- Table 1: Poland Data Center Market Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 2: Poland Data Center Market Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 3: Poland Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 4: Poland Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 5: Poland Data Center Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Poland Data Center Market Revenue billion Forecast, by Hotspot 2020 & 2033

- Table 7: Poland Data Center Market Revenue billion Forecast, by Data Center Size 2020 & 2033

- Table 8: Poland Data Center Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 9: Poland Data Center Market Revenue billion Forecast, by Absorption 2020 & 2033

- Table 10: Poland Data Center Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Data Center Market?

The projected CAGR is approximately 15.68%.

2. Which companies are prominent players in the Poland Data Center Market?

Key companies in the market include Exea p z o o, Atman Sp z o o, Sinersio Polska Sp z o o, Deutsche Telekom AG (T-Mobile Poska SA), Equinix Inc, Comarch SA, 3S Data Center SA (P4 Sp z o o), LIMDC, Beyond pl Sp z o o, Vantage Data Centers LLC5 4 LIST OF COMPANIES STUDIE, S-NET Sp z o o (TOYA Group), Polcom SA.

3. What are the main segments of the Poland Data Center Market?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Automation in the Security Screening Industry. Especially to Detect Advanced Threats. etc.; Upsurge in Terror Activities Across the Region; Increasing Government Initiatives on Security Inspection in Schools and Colleges; Increasing Government Initiatives for Smart Cities.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Supply Chain Issues Caused By Geopolitical Scenario and the COVID-19 Pandemic. etc.; High Installation and Maintenance Costs.

8. Can you provide examples of recent developments in the market?

December 2022: Atman purchased land, the 5.5-hectare site in Duchnice near Ożarów Mazowiecki, to build another data center. The Atman Data Center Warsaw-3 campus was scheduled to open in Q4 2024 with a target IT capacity of 43 MW.August 2022: A new colocation facility would expand Atman Data Center Warsaw-1. The F7 building would have a dedicated power capacity of 7.2 MW for customers’ IT equipment. The new server rooms of 2,916 sq. m were planned to be commissioned in February 2024.June 2022: Vantage completed the first facility on its 12-acre (five-hectare) Warsaw campus. Once fully developed, the two-data center campus would offer 48MW of critical IT capacity across 390,000 square feet (36,000 square meters).

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Data Center Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Data Center Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Data Center Market?

To stay informed about further developments, trends, and reports in the Poland Data Center Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence