Key Insights

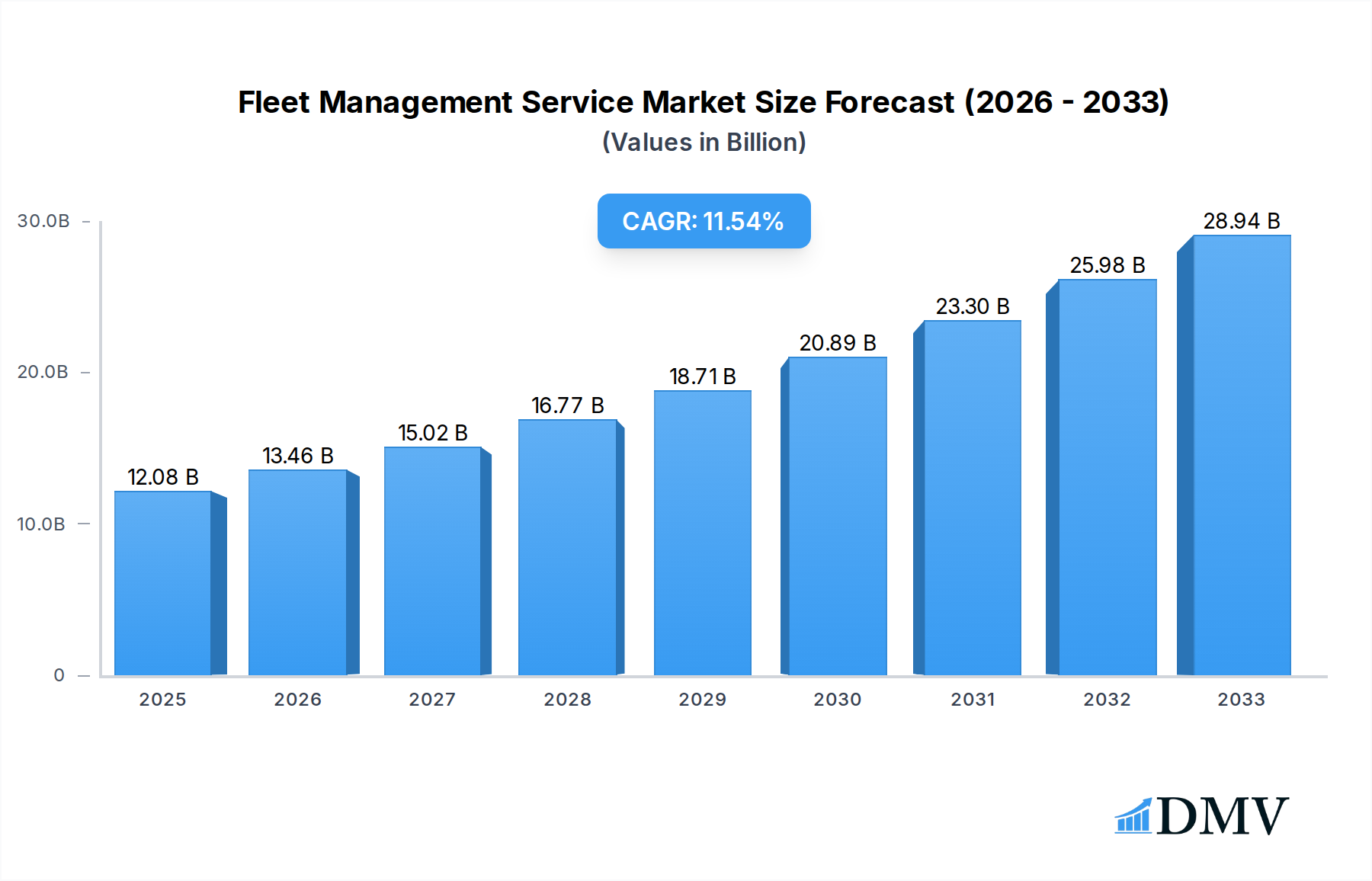

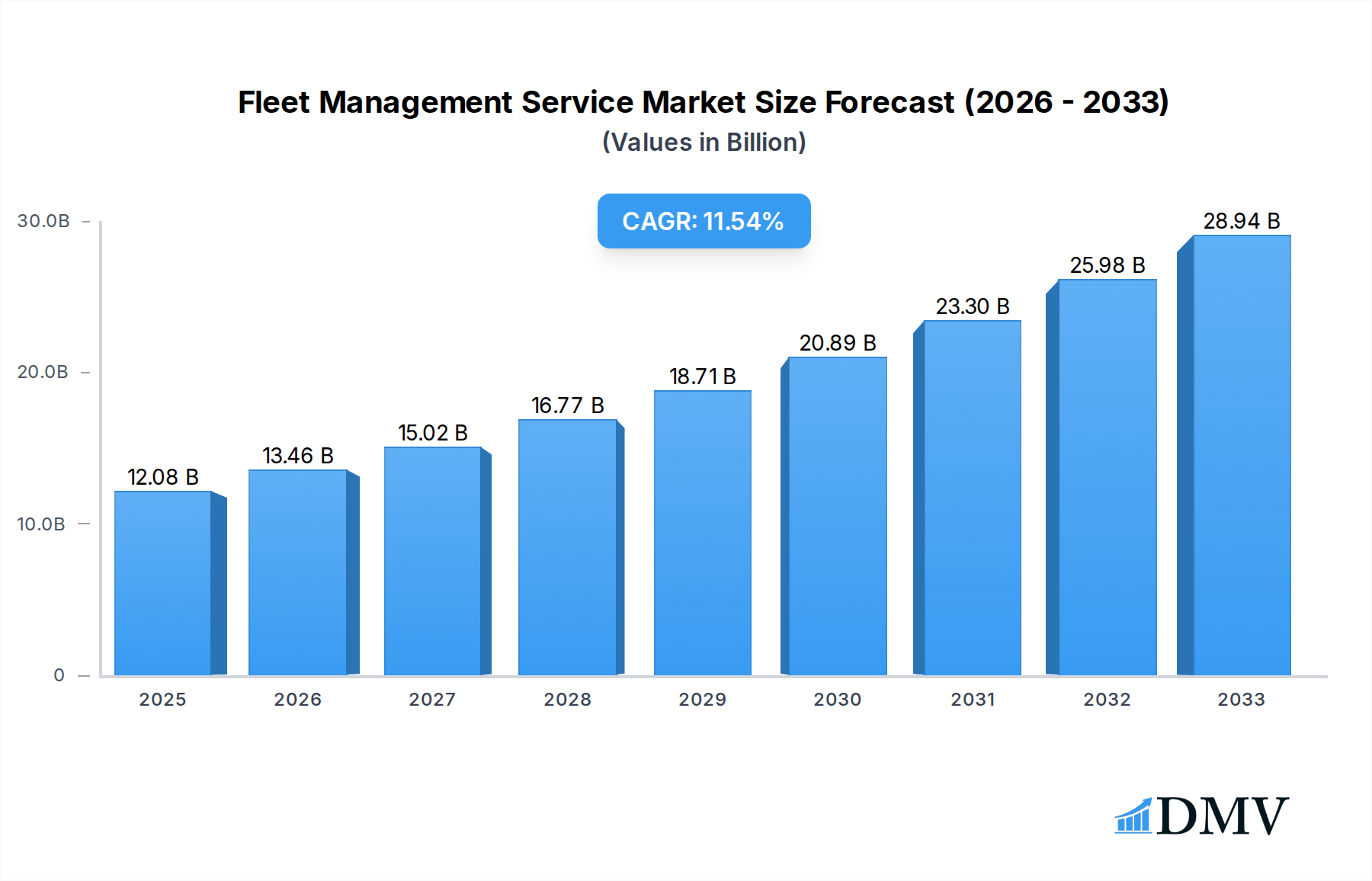

The global Fleet Management Service market is poised for significant expansion, projected to reach an estimated USD 12.08 billion in 2025, with a robust compound annual growth rate (CAGR) of 11.7% during the forecast period of 2025-2033. This upward trajectory is primarily driven by the increasing adoption of advanced technologies such as telematics, GPS tracking, and AI-powered analytics, which enhance operational efficiency, reduce costs, and improve safety for fleet operators. The growing demand for optimized logistics, particularly in the booming e-commerce sector, is a key catalyst. Furthermore, stringent government regulations concerning emissions and vehicle safety are pushing businesses towards more sustainable and compliant fleet management solutions. The market's growth is further fueled by the need for proactive maintenance, reducing downtime and extending the lifespan of vehicles, thereby contributing to lower operational expenditures.

Fleet Management Service Market Size (In Billion)

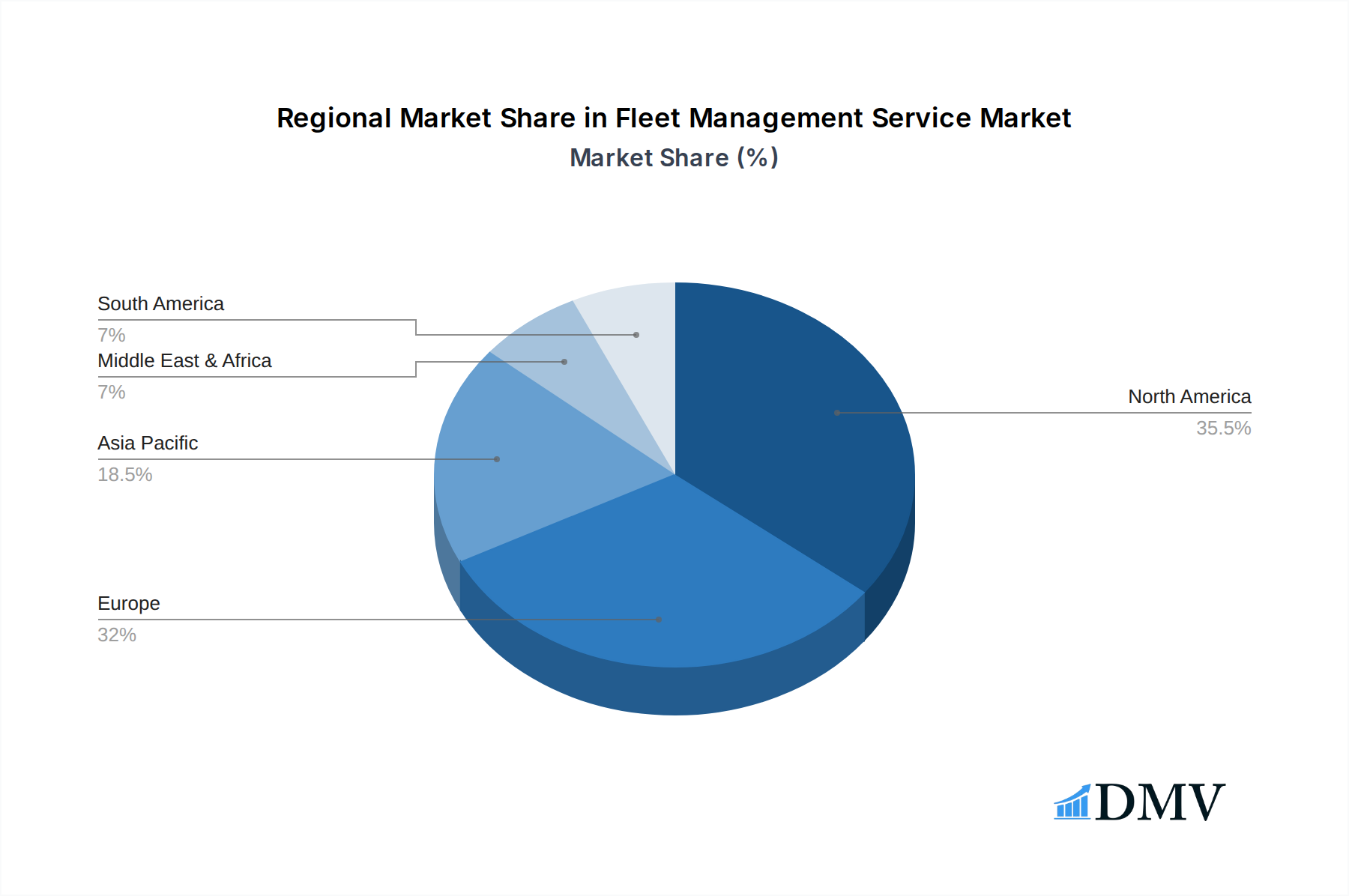

The market segmentation reveals a strong emphasis on the 'Transport and Logistics' application segment, reflecting its critical role in supply chains. The 'Maintenance and Repair' and 'Inspection and MOT Preparation' service types are also expected to witness substantial growth as fleet operators prioritize vehicle upkeep to ensure optimal performance and regulatory adherence. Major players like Cox Automotive, Ford, Zenith, and Ayvens (LeasePlan) are actively investing in R&D and strategic partnerships to offer comprehensive, integrated fleet management solutions. Geographically, North America and Europe currently dominate the market due to well-established infrastructure and early adoption of fleet management technologies. However, the Asia Pacific region is anticipated to emerge as a high-growth market, driven by rapid industrialization, increasing fleet sizes, and a growing awareness of the benefits of professional fleet management. The increasing trend towards electric vehicles (EVs) in fleets also presents a significant opportunity for service providers to offer specialized charging and maintenance solutions.

Fleet Management Service Company Market Share

This comprehensive report, "Fleet Management Service Market Analysis & Future Outlook: 2019–2033," delivers an in-depth examination of the global fleet management industry. Leveraging data from the historical period (2019–2024), base year (2025), and an extensive forecast period through 2033, this report equips stakeholders with actionable intelligence. The study meticulously dissects market composition, industry evolution, regional dominance, product innovations, growth drivers, inherent challenges, and promising future opportunities. Featuring insights from industry titans like Cox Automotive, Ford, Zenith, and Ayvens (LeasePlan), this analysis provides a panoramic view of the market's trajectory and strategic imperatives for sustained success.

Fleet Management Service Market Composition & Trends

The global fleet management service market is characterized by a dynamic interplay of established players and emerging innovators, fostering a competitive yet collaborative ecosystem. Market concentration, while significant among top-tier providers such as Holman (formerly ARI Fleet), Element, and Enterprise Fleet Management, also presents opportunities for niche players offering specialized solutions. Innovation catalysts are primarily driven by the relentless pursuit of operational efficiency, cost reduction, and enhanced sustainability across diverse fleet applications. Regulatory landscapes, particularly those pertaining to emissions standards and data privacy, are increasingly shaping service offerings and operational mandates. Substitute products, though limited, include in-house fleet management capabilities and less integrated technological solutions. End-user profiles span the Transport and Logistics, Public Sector, and Commercial segments, each with distinct operational requirements and adoption rates for advanced fleet management technologies. Mergers and acquisitions (M&A) activities are a significant trend, with deal values in the billions of dollars, as larger entities consolidate market share and expand their service portfolios. For instance, recent M&A activities have seen transaction values exceeding XXX billion, reflecting the strategic importance of this sector. The market share distribution indicates a healthy competitive environment with significant potential for disruption by innovative startups.

- Market Share Distribution: Dominated by a few key players, but with substantial room for specialized service providers.

- M&A Deal Values: Consistently exceeding XXX billion annually, signaling robust consolidation and investment.

- Regulatory Impact: Increasing stringency in emissions and data security regulations driving technology adoption.

- End-User Segmentation: Strong demand from Transport & Logistics and Commercial sectors, with growing interest from Public Sector.

Fleet Management Service Industry Evolution

The fleet management service industry has undergone a profound evolution, transforming from basic vehicle maintenance to sophisticated, data-driven operational platforms. Over the study period from 2019 to 2033, the market has witnessed consistent growth trajectories fueled by technological advancements and shifting consumer demands. The historical period (2019–2024) saw an initial surge in the adoption of telematics and GPS tracking, leading to improved visibility and basic route optimization. The base year (2025) represents a pivotal point where the integration of AI, IoT, and predictive analytics is becoming standard, moving beyond reactive to proactive fleet management.

Technological advancements have been the primary engine of this evolution. The proliferation of connected vehicles, equipped with sensors that generate vast amounts of data, has enabled sophisticated analysis of driver behavior, vehicle health, and fuel efficiency. This data, processed through advanced algorithms, allows for predictive maintenance, thereby reducing downtime and operational costs. The estimated market growth rate for fleet management services is projected to be XX% annually during the forecast period (2025–2033). Adoption metrics for telematics solutions have surpassed XX% across major commercial fleets, with a significant increase in the adoption of AI-powered dispatch and route planning software.

Consumer demand has also played a crucial role. Businesses are increasingly prioritizing sustainability, demanding solutions that reduce carbon footprints and improve fuel efficiency. This has led to a greater emphasis on electric vehicle (EV) integration into fleet management strategies, including charging infrastructure optimization and battery health monitoring. Furthermore, the rise of the on-demand economy and e-commerce has amplified the need for agile, efficient, and responsive logistics, placing greater demands on fleet managers to optimize delivery routes and schedules in real-time. The integration of fleet management services with broader supply chain management software is becoming a critical differentiator, offering end-to-end visibility and control. The industry's evolution is marked by a transition from a transactional service model to a strategic partnership, where fleet management providers become integral to a company's operational success. The market value is expected to reach XXX billion by 2033, a significant increase from XXX billion in 2025.

Leading Regions, Countries, or Segments in Fleet Management Service

The global fleet management service market exhibits strong regional variations and segment dominance, with North America and Europe emerging as leading regions due to mature economies and advanced technological adoption. Within these regions, the Transport and Logistics segment consistently leads in terms of market share and growth, driven by the ever-increasing demand for efficient movement of goods and services. This dominance is further amplified by the critical role of robust fleet management in optimizing supply chains, reducing delivery times, and managing the operational costs of large vehicle fleets. Companies like Enterprise Fleet Management and Marshall Fleet Solutions are prominent players in this segment.

In terms of countries, the United States and Germany are at the forefront, owing to supportive government policies, high vehicle penetration, and a strong presence of major fleet operators. The Public Sector, while representing a smaller share, is a significant growth area, particularly in areas like waste management and public transportation, where operational efficiency and cost control are paramount. The Commercial segment, encompassing businesses of all sizes across various industries, also contributes substantially to market demand.

Analyzing the types of services, Maintenance and Repair remains a cornerstone, driven by the inherent need to keep vehicles operational and safe. However, Financing and Acquisition services are gaining increasing prominence as companies leverage specialized financing solutions to manage capital expenditure and acquire new fleets, often with a focus on sustainable vehicle options. The integration of advanced telematics and data analytics into these services allows for predictive maintenance scheduling and optimized vehicle lifecycle management. For instance, Ayvens (LeasePlan) and Wheels are key players offering comprehensive financing and acquisition solutions. The market's growth in these leading segments is underpinned by:

- Investment Trends: Significant capital inflow into fleet modernization and technology adoption, particularly in North America and Europe.

- Regulatory Support: Favorable government initiatives promoting fuel efficiency, emissions reduction, and the adoption of electric fleets.

- Technological Integration: Widespread adoption of telematics, IoT, and AI for real-time data analysis and optimization across all fleet types.

- Economic Factors: Growing emphasis on operational cost reduction and supply chain resilience driving demand for integrated fleet management solutions.

- Industry-Specific Needs: Tailored solutions addressing the unique operational challenges of the Transport and Logistics, Public Sector, and Commercial segments.

Fleet Management Service Product Innovations

Product innovation in fleet management services is primarily focused on enhancing data utilization, automation, and sustainability. Key advancements include the integration of AI-powered predictive analytics for proactive maintenance, reducing unexpected downtime and associated costs. Real-time route optimization algorithms are becoming more sophisticated, factoring in traffic, weather, and delivery windows for unparalleled efficiency. The growing emphasis on electric vehicles (EVs) has spurred innovations in battery management systems, charging infrastructure optimization, and total cost of ownership (TCO) calculators specifically for EV fleets. Unique selling propositions often lie in the seamless integration of these disparate data streams into user-friendly platforms, offering a single pane of glass for comprehensive fleet oversight. Performance metrics are demonstrably improving, with reported reductions in fuel consumption by up to XX% and decreases in maintenance costs by XX% through proactive measures.

Propelling Factors for Fleet Management Service Growth

The global fleet management service market is propelled by a confluence of technological, economic, and regulatory factors. The rapid advancement and declining costs of telematics and IoT devices have made sophisticated fleet tracking and data analysis more accessible than ever. Economically, businesses are under increasing pressure to optimize operational expenditures, and fleet management services offer a direct pathway to reduce fuel consumption, maintenance costs, and labor inefficiencies. Regulatory pressures, such as stricter emissions standards and corporate sustainability mandates, are compelling companies to adopt greener fleets and more efficient operational practices. For example, government incentives for EV adoption and the introduction of low-emission zones in urban areas are directly driving the demand for specialized fleet management solutions.

Obstacles in the Fleet Management Service Market

Despite its robust growth, the fleet management service market faces several obstacles. Regulatory challenges, particularly in navigating diverse international compliance requirements, can be complex and costly. Supply chain disruptions, such as the global semiconductor shortage, have impacted vehicle availability and the deployment of new fleet technologies, leading to extended lead times and increased costs. Competitive pressures are intense, with a crowded market requiring continuous innovation and value-added services to retain customers. Furthermore, the initial investment in advanced fleet management systems can be a barrier for smaller businesses, and the lack of standardized data protocols across different vehicle manufacturers and telematics providers can hinder seamless integration. The cost of acquiring and integrating new technologies can amount to XXX million for larger fleets.

Future Opportunities in Fleet Management Service

Emerging opportunities in the fleet management service market are abundant, driven by technological advancements and evolving business needs. The expansion of autonomous vehicle technology presents a significant long-term opportunity for specialized management and monitoring solutions. The growing demand for sustainable logistics is creating new markets for comprehensive EV fleet management, including charging optimization and battery lifecycle services. Furthermore, the integration of fleet data with broader enterprise resource planning (ERP) and supply chain management systems offers a pathway to provide more holistic business intelligence and operational control. The development of predictive analytics for a wider range of operational aspects, beyond just maintenance, such as predicting delivery times with greater accuracy, will also drive adoption.

Major Players in the Fleet Management Service Ecosystem

- Cox Automotive

- Ford

- Zenith

- Go Plant Fleet Services

- Vector Fleet Management

- Big Brand

- Epika Fleet Services

- Bona Bros

- CLM

- Ayvens (LeasePlan)

- Wheels

- Holman (formerly ARI Fleet)

- Element

- EQSTRA

- Marshall Fleet Solutions

- Premier Logistics

- Enterprise Fleet Management

Key Developments in Fleet Management Service Industry

- 2023: Increased investment in AI for predictive maintenance, leading to a XX% reduction in unplanned downtime for early adopters.

- 2024: Launch of advanced telematics platforms integrating real-time carbon emission tracking and reporting, aligning with growing ESG demands.

- 2024: Significant M&A activity with XXX billion in disclosed deals, focusing on consolidating market share and expanding service portfolios.

- 2025: Greater integration of Electric Vehicle (EV) management solutions, including smart charging and battery health monitoring, becoming a standard offering.

- 2025: Enhanced focus on cybersecurity for fleet data, with providers implementing robust security protocols to protect sensitive operational information.

- 2026: Expected widespread adoption of advanced route optimization software incorporating real-time traffic and weather data, further improving delivery efficiency.

- 2027: Emergence of more comprehensive financing and acquisition models tailored for mixed fleets (ICE and EV).

- 2028: Growing adoption of integrated fleet management systems that seamlessly connect with supply chain and logistics platforms.

- 2029: Continued development of autonomous fleet management solutions and the integration of AI for their operational oversight.

- 2030: Increased regulatory pressure on emissions and sustainability leading to further innovation in green fleet management technologies.

- 2031: Expansion of the market into emerging economies with tailored solutions addressing local infrastructure and operational needs.

- 2032: Greater emphasis on data analytics for driver behavior coaching and safety improvement programs.

- 2033: Forecasted market size of XXX billion, reflecting sustained growth and technological integration.

Strategic Fleet Management Service Market Forecast

The strategic fleet management service market forecast is overwhelmingly positive, driven by ongoing technological innovation and an unwavering business imperative for operational efficiency and sustainability. The continued integration of AI, IoT, and advanced data analytics will empower fleet operators with unprecedented levels of insight and control. The accelerating transition towards electric and alternative fuel vehicles will create substantial demand for specialized management solutions, further expanding the market. Economic pressures will continue to push businesses towards cost optimization, making sophisticated fleet management services indispensable. Emerging markets and the increasing complexity of global supply chains also present significant opportunities for growth. The market is poised for sustained expansion, with strategic investments in technology and service diversification being key to capitalizing on future potential, with an estimated market value reaching XXX billion by the end of the forecast period.

Fleet Management Service Segmentation

-

1. Application

- 1.1. Transport and Logistics

- 1.2. Public Sector

- 1.3. Commercial

- 1.4. Other

-

2. Types

- 2.1. Maintenance and Repair

- 2.2. Inspection and MOT Preparation

- 2.3. Financing and Acquisition

- 2.4. Other Service

Fleet Management Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fleet Management Service Regional Market Share

Geographic Coverage of Fleet Management Service

Fleet Management Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Transport and Logistics

- 5.1.2. Public Sector

- 5.1.3. Commercial

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Maintenance and Repair

- 5.2.2. Inspection and MOT Preparation

- 5.2.3. Financing and Acquisition

- 5.2.4. Other Service

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Transport and Logistics

- 6.1.2. Public Sector

- 6.1.3. Commercial

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Maintenance and Repair

- 6.2.2. Inspection and MOT Preparation

- 6.2.3. Financing and Acquisition

- 6.2.4. Other Service

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Transport and Logistics

- 7.1.2. Public Sector

- 7.1.3. Commercial

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Maintenance and Repair

- 7.2.2. Inspection and MOT Preparation

- 7.2.3. Financing and Acquisition

- 7.2.4. Other Service

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Transport and Logistics

- 8.1.2. Public Sector

- 8.1.3. Commercial

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Maintenance and Repair

- 8.2.2. Inspection and MOT Preparation

- 8.2.3. Financing and Acquisition

- 8.2.4. Other Service

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Transport and Logistics

- 9.1.2. Public Sector

- 9.1.3. Commercial

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Maintenance and Repair

- 9.2.2. Inspection and MOT Preparation

- 9.2.3. Financing and Acquisition

- 9.2.4. Other Service

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fleet Management Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Transport and Logistics

- 10.1.2. Public Sector

- 10.1.3. Commercial

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Maintenance and Repair

- 10.2.2. Inspection and MOT Preparation

- 10.2.3. Financing and Acquisition

- 10.2.4. Other Service

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Cox Automotive

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ford

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Zenith

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Go Plant Fleet Services

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Vector Fleet Management

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Big Brand

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Epika Fleet Services

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bona Bros

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CLM

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ayvens (LeasePlan)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Wheels

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Holman (formerly ARI Fleet)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Element

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 EQSTRA

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Marshall Fleet Solutions

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Premier Logistics

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Enterprise Fleet Management

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Cox Automotive

List of Figures

- Figure 1: Global Fleet Management Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fleet Management Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Fleet Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fleet Management Service Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Fleet Management Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fleet Management Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fleet Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fleet Management Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Fleet Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fleet Management Service Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Fleet Management Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fleet Management Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Fleet Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fleet Management Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Fleet Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fleet Management Service Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Fleet Management Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fleet Management Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Fleet Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fleet Management Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fleet Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fleet Management Service Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fleet Management Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fleet Management Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fleet Management Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fleet Management Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Fleet Management Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fleet Management Service Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Fleet Management Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fleet Management Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Fleet Management Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Fleet Management Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Fleet Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Fleet Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Fleet Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Fleet Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Fleet Management Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Fleet Management Service Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Fleet Management Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fleet Management Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fleet Management Service?

The projected CAGR is approximately 11.7%.

2. Which companies are prominent players in the Fleet Management Service?

Key companies in the market include Cox Automotive, Ford, Zenith, Go Plant Fleet Services, Vector Fleet Management, Big Brand, Epika Fleet Services, Bona Bros, CLM, Ayvens (LeasePlan), Wheels, Holman (formerly ARI Fleet), Element, EQSTRA, Marshall Fleet Solutions, Premier Logistics, Enterprise Fleet Management.

3. What are the main segments of the Fleet Management Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.08 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fleet Management Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fleet Management Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fleet Management Service?

To stay informed about further developments, trends, and reports in the Fleet Management Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence