Key Insights

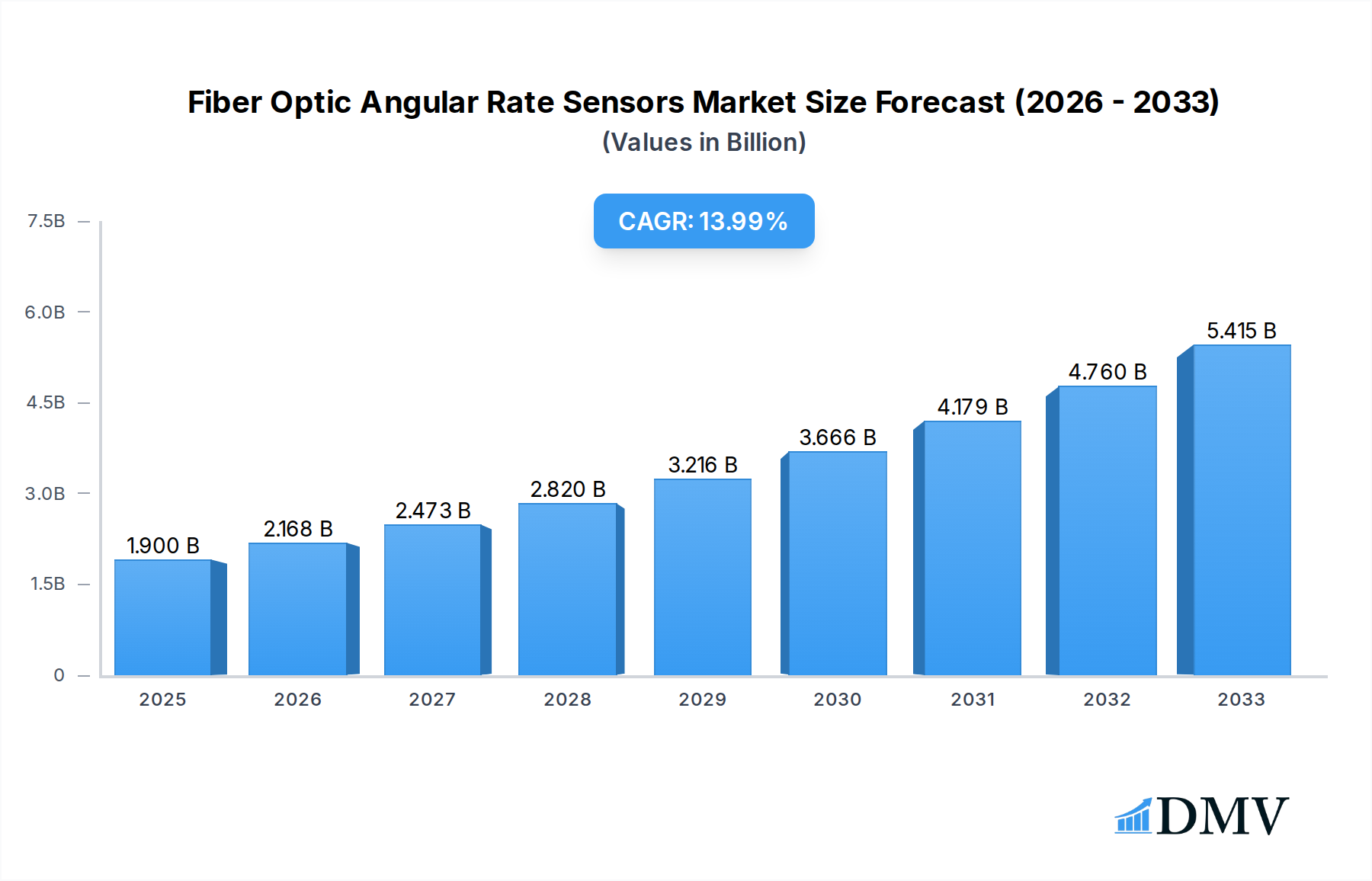

The global Fiber Optic Angular Rate Sensors market is poised for substantial expansion, projected to reach USD 1.9 billion in 2025. This impressive growth trajectory is underscored by a compelling Compound Annual Growth Rate (CAGR) of 14.2% anticipated over the forecast period of 2025-2033. The primary impetus for this surge stems from the escalating demand for high-precision navigation and guidance systems across critical sectors like aviation and space, and naval applications. The inherent advantages of fiber optic sensors, including their immunity to electromagnetic interference, compact size, and robust performance in extreme environments, make them indispensable for advanced aerospace and defense platforms. The increasing sophistication of unmanned aerial vehicles (UAVs), satellite navigation systems, and modern submarine technology further fuels the adoption of these advanced sensors, driving market value and technological innovation.

Fiber Optic Angular Rate Sensors Market Size (In Billion)

Emerging trends and a dynamic competitive landscape are shaping the future of the Fiber Optic Angular Rate Sensors market. While the aviation and space segment is expected to dominate, the ship and submarine sector is also witnessing significant growth due to the modernization of naval fleets and the development of autonomous underwater vehicles. Technological advancements, particularly in miniaturization and enhanced accuracy, are key trends that will likely drive market expansion. However, the market faces certain restraints, including the high initial cost of sophisticated fiber optic sensor systems and the need for specialized expertise in their installation and maintenance. Despite these challenges, the relentless pursuit of improved performance and reliability in critical applications ensures a robust and expanding market for fiber optic angular rate sensors, with key players like Northrop Grumman, Honeywell, and Safran actively investing in research and development to maintain their competitive edge.

Fiber Optic Angular Rate Sensors Company Market Share

This comprehensive report, spanning the Study Period 2019–2033, with a Base Year of 2025 and Forecast Period 2025–2033, offers an in-depth analysis of the global Fiber Optic Angular Rate Sensor (FOARS) market. With the Estimated Year 2025 market size projected to reach $xx billion, this report provides critical insights for stakeholders seeking to understand market dynamics, technological advancements, and future growth trajectories. The FOARS market, driven by the relentless demand for high-precision navigation and stabilization across defense, aerospace, and maritime sectors, is set for substantial expansion, fueled by innovation and strategic investments. Our analysis delves into the intricacies of this billion-dollar industry, identifying key players, disruptive technologies, and emerging opportunities.

Fiber Optic Angular Rate Sensors Market Composition & Trends

The global Fiber Optic Angular Rate Sensors market is characterized by a dynamic landscape shaped by intense innovation and strategic consolidation. Market concentration is moderate, with a few major players holding significant shares, but a growing number of specialized companies are contributing to innovation. The Historical Period 2019–2024 has witnessed significant R&D investments, particularly in enhancing sensor performance, miniaturization, and cost-effectiveness, acting as key innovation catalysts. Regulatory landscapes, particularly stringent aerospace and defense standards, are driving the adoption of advanced FOARS for enhanced safety and performance. While established technologies like MEMS gyroscopes exist as substitute products, the superior performance of FOARS in terms of accuracy, bandwidth, and resistance to harsh environments ensures their continued dominance in critical applications. End-user profiles are increasingly diverse, ranging from major defense contractors to emerging players in autonomous systems and offshore energy exploration. Mergers & Acquisitions (M&A) activities are a crucial trend, with deal values in the past five years estimated to be in the $xx billion range, as larger entities seek to acquire specialized FOARS technologies and expand their market reach.

- Market Share Distribution: Leading companies like Northrop Grumman and KVH Industries are estimated to hold approximately xx% and xx% of the market share respectively.

- M&A Deal Values (Historical Period 2019-2024): Estimated cumulative deal value of $xx billion, indicating significant industry consolidation and strategic investments.

- Innovation Catalysts: Focus on Fiber Bragg Grating (FBG) technology, Ring Laser Gyro (RLG) alternatives, and digital signal processing advancements.

- Regulatory Landscapes: Strict adherence to MIL-STD and DO-160 standards for aerospace and defense applications.

- Substitute Product Landscape: Competition from high-end MEMS gyroscopes, though FOARS maintain a performance edge in demanding applications.

Fiber Optic Angular Rate Sensors Industry Evolution

The Fiber Optic Angular Rate Sensors industry has undergone a remarkable evolution, transforming from niche technologies to indispensable components in high-precision navigation and stabilization systems. Over the Study Period 2019–2033, the market has experienced a compound annual growth rate (CAGR) of approximately xx%, a testament to its increasing strategic importance. This growth trajectory has been propelled by relentless technological advancements, with early research focusing on basic principles of optical gyroscopes evolving into sophisticated interferometric and resonant fiber optic gyroscopes (IFOGs and RFOGs). The Historical Period 2019–2024 saw significant breakthroughs in miniaturization, power efficiency, and improved resistance to shock and vibration, making FOARS suitable for an ever-wider range of platforms.

Shifting consumer demands, particularly from the defense and aerospace sectors, have played a pivotal role. The increasing complexity of modern warfare, the rise of unmanned aerial vehicles (UAVs) and autonomous systems, and the stringent requirements for satellite navigation have amplified the need for highly accurate and reliable angular rate sensing. This has led to a surge in the adoption of FOARS for applications such as INS (Inertial Navigation Systems), attitude and heading reference systems (AHRS), and stabilization platforms.

Furthermore, advancements in materials science and manufacturing techniques have reduced production costs, making FOARS more accessible to a broader market. The development of compact, high-performance FOARS has enabled their integration into smaller platforms, including tactical missiles, drones, and even advanced robotics. The market is also witnessing a growing demand for digital output FOARS, simplifying integration with modern electronic systems. Looking ahead, the Forecast Period 2025–2033 is projected to see continued innovation, with a focus on further improving accuracy (down to xx µdeg/s), reducing drift rates, and enhancing operational lifespan, ensuring FOARS remain at the forefront of precision navigation technology. The estimated market value for 2025 alone is projected to be $xx billion, with strong growth anticipated in the subsequent years.

Leading Regions, Countries, or Segments in Fiber Optic Angular Rate Sensors

The global Fiber Optic Angular Rate Sensors market demonstrates clear leadership within specific segments and geographical regions, driven by robust defense spending, advanced technological infrastructure, and government support for innovation. The Application segment of Aviation and Space emerges as the dominant force, accounting for an estimated xx% of the total market share. This is directly attributable to the critical need for highly accurate navigation and stabilization in commercial aircraft, military jets, satellites, and spacecraft. The inherent advantages of FOARS, such as high accuracy, wide dynamic range, and immunity to electromagnetic interference, make them indispensable for flight control systems, missile guidance, and satellite attitude control.

Within the Types segment, Multi-Axis sensors (typically 2-axis and 3-axis configurations) are the most sought-after, driven by their ability to provide comprehensive angular rate data for complete spatial orientation. This segment commands an estimated xx% of the market. The Ship and Submarine application segment also represents a significant market share, approximately xx%, owing to the demanding operational environments and the requirement for precise navigation and stabilization in naval vessels and submarines. The Others application segment, encompassing areas like robotics, industrial automation, and seismic monitoring, is a rapidly growing but currently smaller contributor, estimated at xx%.

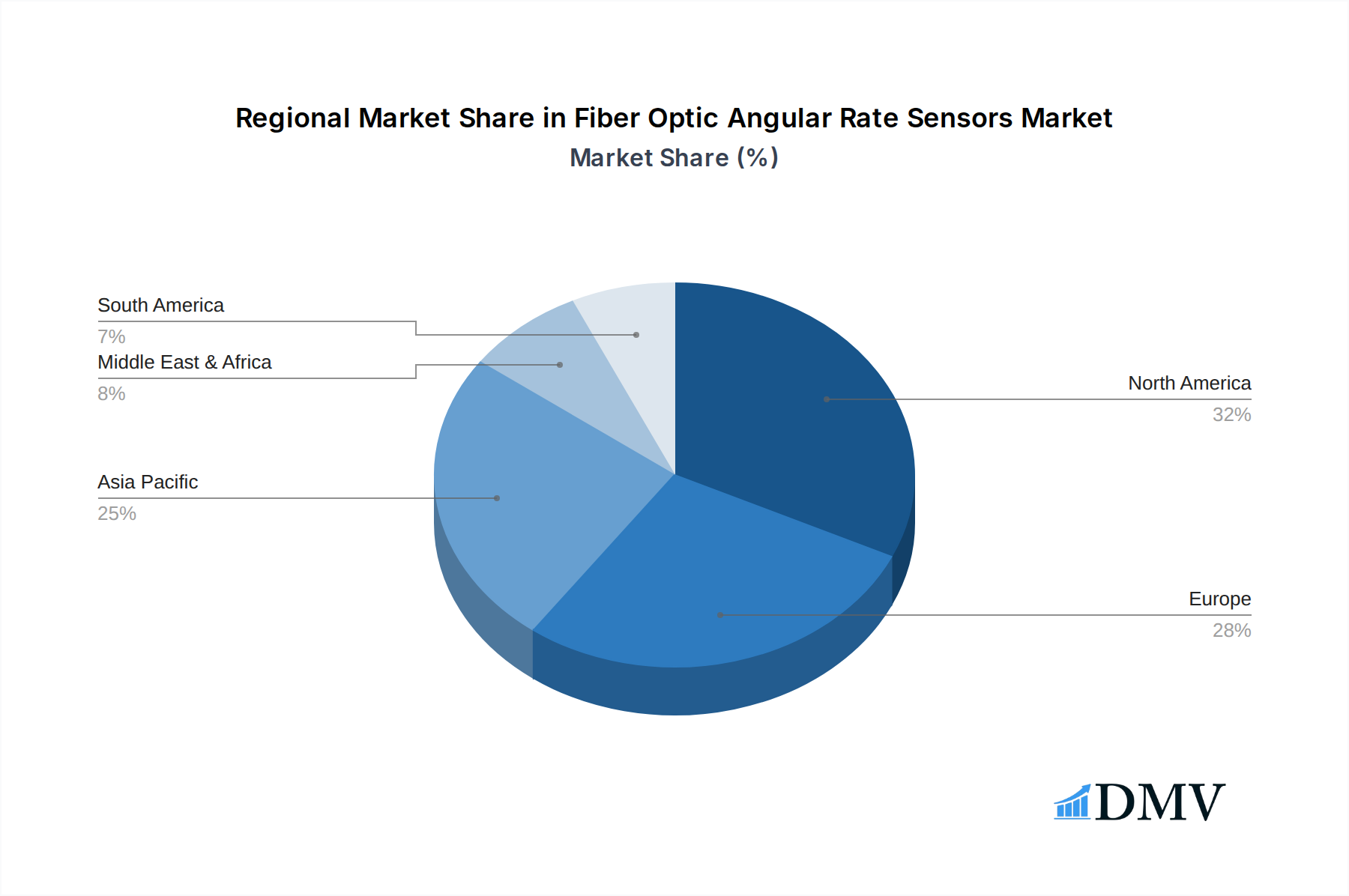

Geographically, North America leads the market, representing an estimated xx% of global revenue. This dominance is fueled by substantial investments in defense modernization, a thriving aerospace industry, and a strong presence of leading FOARS manufacturers and research institutions. The United States, in particular, drives this demand through its extensive military procurement programs and its leadership in space exploration initiatives. Europe follows as the second-largest market, with countries like France and the United Kingdom heavily investing in advanced defense and aerospace technologies. Asia-Pacific is a rapidly expanding region, driven by increasing defense budgets and growing indigenous aerospace capabilities in countries like China and India.

- Dominant Application Segment: Aviation and Space (estimated xx% market share), driven by critical navigation needs in commercial and defense aviation, as well as space missions.

- Dominant Sensor Type: Multi-Axis FOARS (estimated xx% market share), essential for comprehensive spatial orientation and control.

- Leading Geographical Region: North America (estimated xx% market share), due to significant defense spending, advanced aerospace sector, and R&D infrastructure.

- Key Drivers in Aviation and Space: Requirement for high accuracy in INS/AHRS, missile guidance systems, and satellite attitude control.

- Growth Factors in Ship and Submarine: Need for robust and reliable navigation in challenging maritime environments, especially for naval vessels and submarines.

Fiber Optic Angular Rate Sensors Product Innovations

Product innovation in Fiber Optic Angular Rate Sensors is relentlessly focused on pushing the boundaries of performance and miniaturization. Recent advancements include the development of ultra-high-accuracy IFOGs capable of achieving drift rates as low as xx nrad/s, crucial for demanding space-based applications and high-precision inertial navigation. Simultaneously, manufacturers are achieving significant reductions in size and weight, with new generations of single-axis and multi-axis FOARS fitting into compact form factors suitable for integration into smaller drones and guided munitions. The incorporation of advanced digital signal processing algorithms is enhancing noise reduction and improving the dynamic range, while also enabling self-calibration and diagnostic capabilities, further increasing reliability and reducing operational burdens. These innovations are opening doors to new applications beyond traditional defense and aerospace, including advanced robotics and high-speed autonomous vehicles.

Propelling Factors for Fiber Optic Angular Rate Sensors Growth

The growth of the Fiber Optic Angular Rate Sensors market is propelled by a confluence of technological, economic, and regulatory factors. The increasing demand for highly accurate and reliable navigation and stabilization systems across the defense sector, particularly for unmanned aerial vehicles (UAVs), precision-guided munitions, and advanced fighter jets, is a primary driver. Economic stimulus in defense spending globally, coupled with significant investments in space exploration and commercial satellite constellations, further fuels this demand. Regulatory mandates for enhanced safety and performance in aviation, such as the need for improved flight control and navigation redundancy, also contribute significantly. Furthermore, the growing adoption of autonomous systems in various industries, including maritime, robotics, and automotive, is creating new avenues for FOARS integration. The technological superiority of FOARS over traditional gyroscopes, offering greater accuracy, wider bandwidth, and immunity to environmental factors like vibration and temperature, positions them for sustained growth.

Obstacles in the Fiber Optic Angular Rate Sensors Market

Despite robust growth prospects, the Fiber Optic Angular Rate Sensors market faces several obstacles that could temper its expansion. The high initial cost of advanced FOARS, particularly for high-end interferometric fiber optic gyroscopes (IFOGs), can be a significant barrier for adoption in cost-sensitive applications and by smaller enterprises. Stringent qualification processes and long development cycles associated with aerospace and defense certifications can also slow down the introduction of new products and hinder market penetration. Furthermore, supply chain vulnerabilities for specialized optical components and rare earth elements can lead to production delays and cost fluctuations. Intense competition from emerging technologies, such as advanced MEMS gyroscopes and solid-state gyroscopes that are becoming increasingly cost-effective and capable, also presents a challenge, particularly in lower-tier applications where cost is a primary consideration. The market is also susceptible to geopolitical shifts that could impact defense spending and international trade, indirectly affecting demand for FOARS.

Future Opportunities in Fiber Optic Angular Rate Sensors

The Fiber Optic Angular Rate Sensors market is poised for significant future opportunities driven by emerging technological trends and expanding application areas. The proliferation of the Internet of Things (IoT) and the increasing demand for precise data in smart infrastructure, industrial automation, and smart cities present new avenues for FOARS deployment. The ongoing development of autonomous vehicles, including drones for delivery, surveillance, and agricultural applications, will create substantial demand for compact and cost-effective FOARS. Furthermore, advancements in quantum sensing technologies, while still in early stages, could eventually integrate with or complement FOARS, offering even greater levels of precision. The expansion of space exploration initiatives, including commercial space tourism and lunar/Martian missions, will necessitate highly reliable and durable FOARS. Finally, the growing focus on inertial navigation systems for underwater autonomous vehicles (UAVs) and offshore exploration will continue to be a significant growth driver.

Major Players in the Fiber Optic Angular Rate Sensors Ecosystem

- Northrop Grumman

- KVH Industries

- Safran

- Honeywell

- Kearfott

- AVIC

- Optolink

- iXblue

- L3 Harris

- Fizoptika CJSC

- JAE

- Emcore

- Civitanavi

- Mitsubishi Precision

Key Developments in Fiber Optic Angular Rate Sensors Industry

- 2023: Northrop Grumman announces a new generation of compact IFOGs for drone applications.

- 2023: KVH Industries introduces enhanced digital output FOARS for enhanced integration in tactical systems.

- 2024: Safran secures a major contract for supplying FOARS for a new fighter jet program.

- 2024: iXblue expands its product line with ultra-high-accuracy sensors for satellite navigation.

- 2024: L3 Harris completes the acquisition of a specialized FOARS technology company.

- 2024: Emcore unveils miniaturized FOARS with improved power efficiency.

- 2025: Civitanavi showcases new FOARS with integrated self-diagnostic capabilities.

- 2025: Fizoptika CJSC announces advancements in FBG-based angular rate sensors.

Strategic Fiber Optic Angular Rate Sensors Market Forecast

The strategic outlook for the Fiber Optic Angular Rate Sensors market remains exceptionally strong, with future growth catalysts deeply rooted in technological innovation and expanding applications. The increasing sophistication of defense systems, coupled with the rapid growth of the commercial aerospace sector, will continue to be primary demand drivers. The burgeoning market for autonomous systems across various industries, from robotics to maritime and even personal mobility, presents substantial new opportunities for FOARS adoption. Continued investment in research and development focused on enhancing sensor accuracy, reducing size and weight, and improving cost-effectiveness will unlock further market potential. The market is projected to witness sustained growth, driven by these fundamental factors, ensuring Fiber Optic Angular Rate Sensors remain at the forefront of precision navigation and stabilization for the foreseeable future. The market is expected to reach $xx billion by 2033.

Fiber Optic Angular Rate Sensors Segmentation

-

1. Application

- 1.1. Aviation and Space

- 1.2. Ship and Submarine

- 1.3. Others

-

2. Types

- 2.1. Single-Axis

- 2.2. Multi-Axis

Fiber Optic Angular Rate Sensors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fiber Optic Angular Rate Sensors Regional Market Share

Geographic Coverage of Fiber Optic Angular Rate Sensors

Fiber Optic Angular Rate Sensors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aviation and Space

- 5.1.2. Ship and Submarine

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Single-Axis

- 5.2.2. Multi-Axis

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aviation and Space

- 6.1.2. Ship and Submarine

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Single-Axis

- 6.2.2. Multi-Axis

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aviation and Space

- 7.1.2. Ship and Submarine

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Single-Axis

- 7.2.2. Multi-Axis

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aviation and Space

- 8.1.2. Ship and Submarine

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Single-Axis

- 8.2.2. Multi-Axis

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aviation and Space

- 9.1.2. Ship and Submarine

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Single-Axis

- 9.2.2. Multi-Axis

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fiber Optic Angular Rate Sensors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aviation and Space

- 10.1.2. Ship and Submarine

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Single-Axis

- 10.2.2. Multi-Axis

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Northrop Grumman

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 KVH Industries

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Safran

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Honeywell

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kearfott

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 AVIC

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Optolink

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 iXblue

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 L3 Harris

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Fizoptika CJSC

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 JAE

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Emcore

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Civitanavi

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Mitsubishi Precision

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Northrop Grumman

List of Figures

- Figure 1: Global Fiber Optic Angular Rate Sensors Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fiber Optic Angular Rate Sensors Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Fiber Optic Angular Rate Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fiber Optic Angular Rate Sensors Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Fiber Optic Angular Rate Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fiber Optic Angular Rate Sensors Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fiber Optic Angular Rate Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fiber Optic Angular Rate Sensors Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Fiber Optic Angular Rate Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fiber Optic Angular Rate Sensors Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Fiber Optic Angular Rate Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fiber Optic Angular Rate Sensors Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Fiber Optic Angular Rate Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fiber Optic Angular Rate Sensors Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Fiber Optic Angular Rate Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fiber Optic Angular Rate Sensors Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Fiber Optic Angular Rate Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fiber Optic Angular Rate Sensors Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Fiber Optic Angular Rate Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fiber Optic Angular Rate Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fiber Optic Angular Rate Sensors Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Fiber Optic Angular Rate Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fiber Optic Angular Rate Sensors Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Fiber Optic Angular Rate Sensors Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fiber Optic Angular Rate Sensors Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Fiber Optic Angular Rate Sensors Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Fiber Optic Angular Rate Sensors Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fiber Optic Angular Rate Sensors Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fiber Optic Angular Rate Sensors?

The projected CAGR is approximately 14.2%.

2. Which companies are prominent players in the Fiber Optic Angular Rate Sensors?

Key companies in the market include Northrop Grumman, KVH Industries, Safran, Honeywell, Kearfott, AVIC, Optolink, iXblue, L3 Harris, Fizoptika CJSC, JAE, Emcore, Civitanavi, Mitsubishi Precision.

3. What are the main segments of the Fiber Optic Angular Rate Sensors?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fiber Optic Angular Rate Sensors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fiber Optic Angular Rate Sensors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fiber Optic Angular Rate Sensors?

To stay informed about further developments, trends, and reports in the Fiber Optic Angular Rate Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence