Key Insights

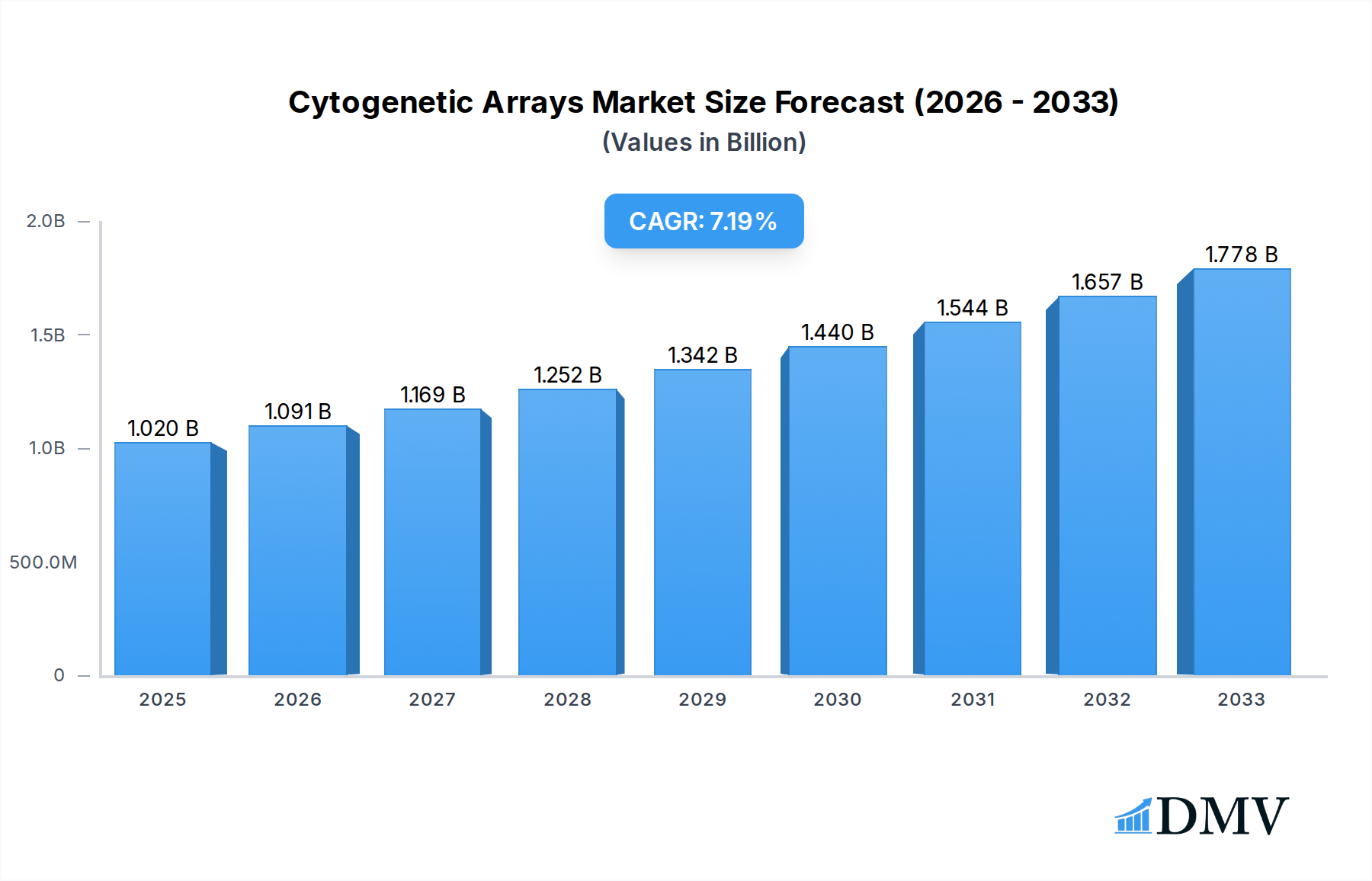

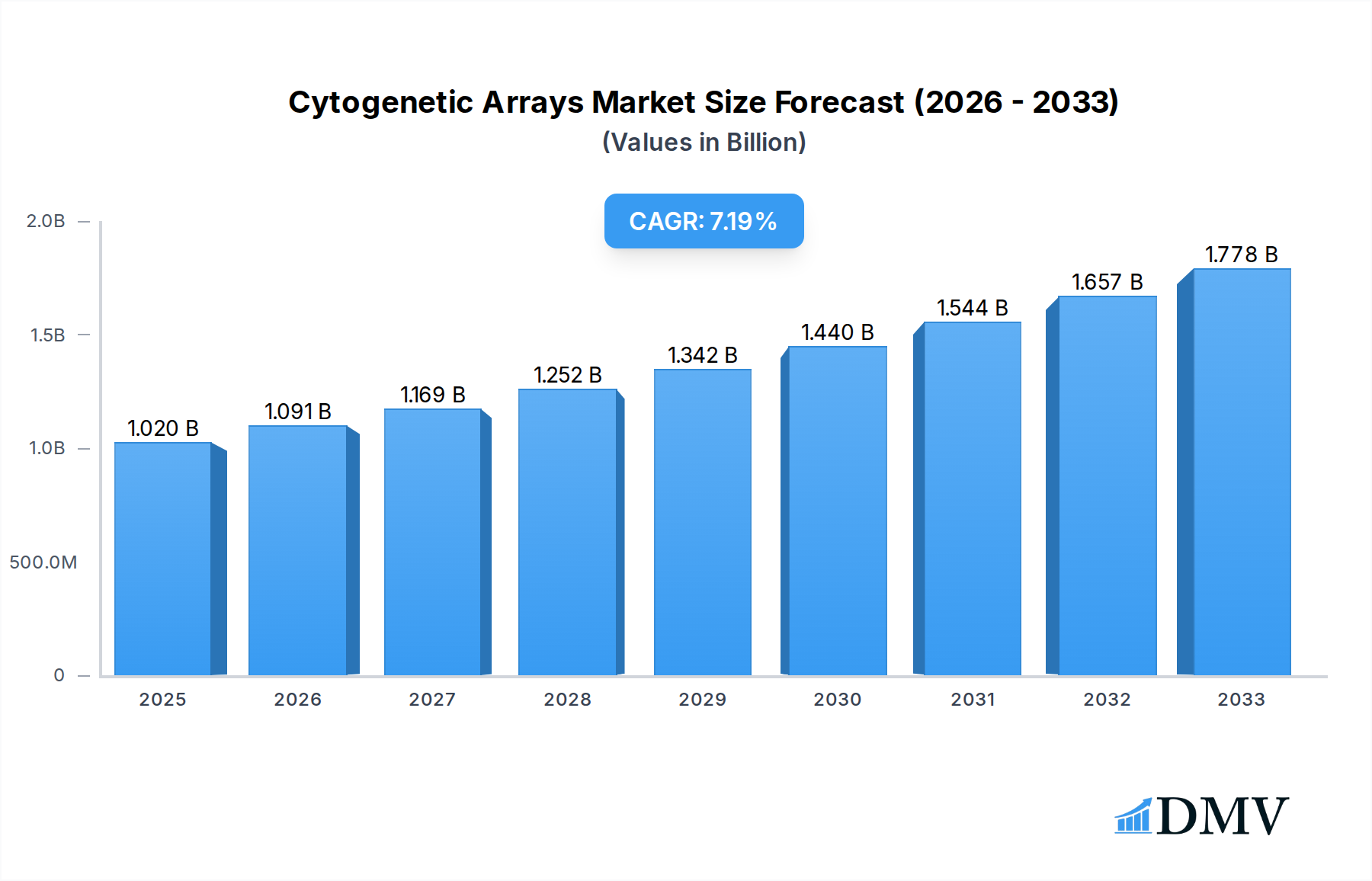

The global Cytogenetic Arrays market is poised for significant expansion, projected to reach an estimated $1.02 billion in 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 7.1% anticipated from 2025 to 2033. The primary drivers fueling this market dynamism include advancements in assisted reproduction technologies, the escalating demand for sophisticated genetic research tools, and the increasing awareness and diagnosis of genetic disorders. As per advances in genomics and the growing adoption of precision medicine, cytogenetic arrays are becoming indispensable for identifying chromosomal abnormalities, contributing to personalized treatment strategies. The market's expansion is further bolstered by ongoing technological innovations that enhance the sensitivity, specificity, and cost-effectiveness of array-based diagnostics.

Cytogenetic Arrays Market Size (In Billion)

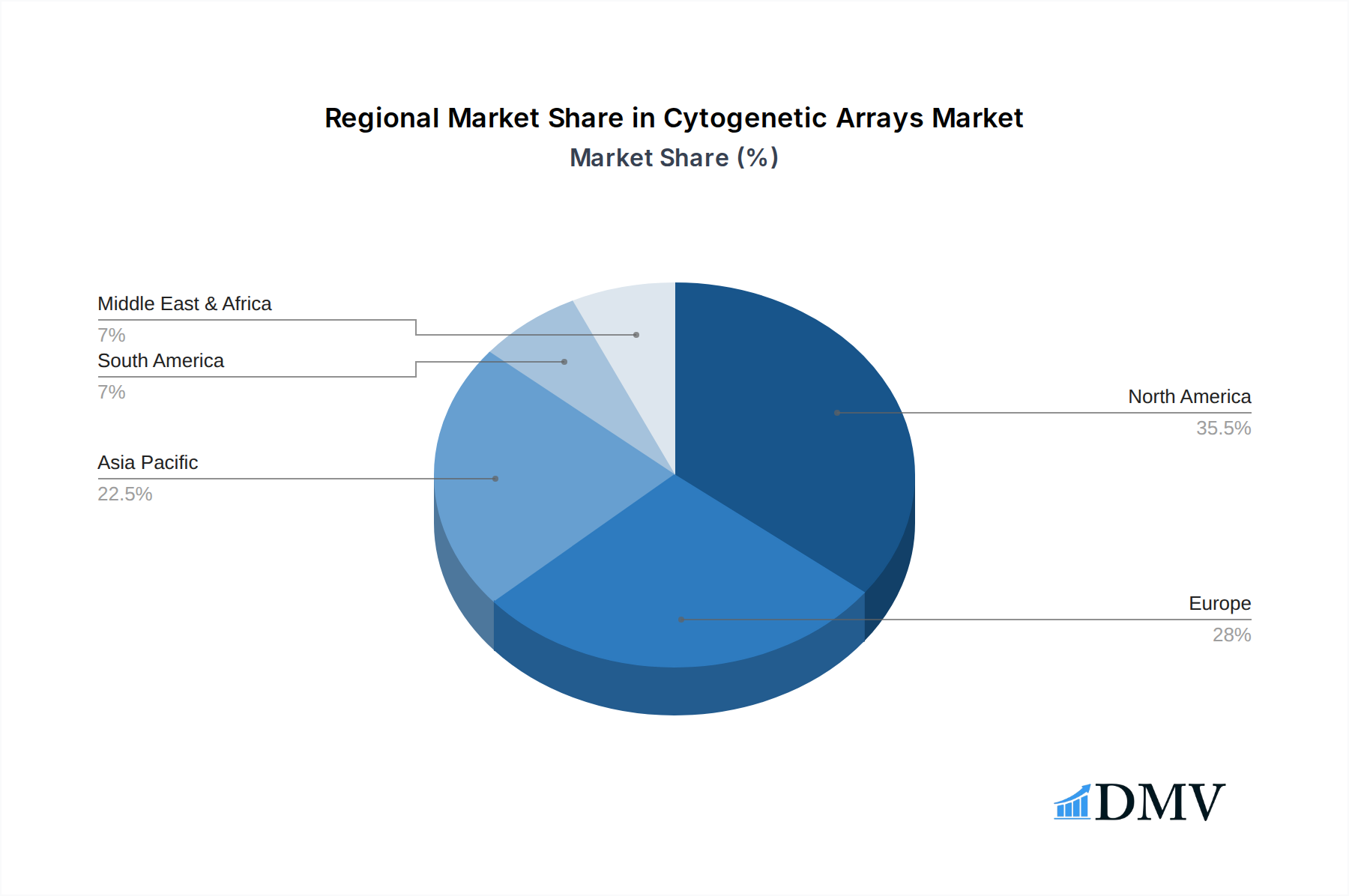

The market is segmented into key applications, with Assisted Reproduction and Scientific Research emerging as dominant forces, reflecting the critical role of cytogenetic analysis in reproductive health and molecular biology. The "Others" category, likely encompassing diagnostic and clinical research applications, also presents substantial growth opportunities. In terms of types, Whole-Genome Sequencing Arrays and Comparative Genomic Hybridization (CGH) Arrays are expected to lead, catering to diverse research and diagnostic needs. Geographically, North America and Europe currently hold significant market shares due to well-established healthcare infrastructures and strong research ecosystems. However, the Asia Pacific region is anticipated to witness the fastest growth, driven by increasing healthcare investments, a burgeoning research landscape, and a rising incidence of genetic disorders. Key industry players like Illumina, Thermo Fisher, and Oxford Nanopore are actively investing in research and development, introducing novel solutions and expanding their product portfolios to meet the evolving demands of this dynamic market.

Cytogenetic Arrays Company Market Share

Cytogenetic Arrays Market Composition & Trends

The global cytogenetic arrays market, valued at over a billion dollars in 2023, is characterized by a moderately concentrated landscape with key players like Illumina, Thermo Fisher Scientific, Agilent Technologies, and Roche driving innovation and market share. The study period, 2019–2033, encompassing historical data from 2019–2024 and a forecast period of 2025–2033 with a 2025 base and estimated year, reveals a dynamic environment shaped by evolving research methodologies and clinical applications. Innovation catalysts are primarily centered around advancements in array technology, such as higher density probes and improved resolution for detecting microdeletions and microduplications. Regulatory landscapes, while generally supportive of diagnostic advancements, vary by region, influencing market access and adoption rates. Substitute products, including next-generation sequencing (NGS), present an ongoing competitive pressure, though cytogenetic arrays retain advantages in specific diagnostic workflows and cost-effectiveness for certain applications. End-user profiles are diverse, ranging from academic research institutions and diagnostic laboratories to pharmaceutical companies engaged in drug discovery and development. Merger and acquisition (M&A) activities, with deal values potentially reaching billions, have been strategic, aimed at consolidating market positions, expanding product portfolios, and acquiring novel technologies. The market share distribution is influenced by the breadth of product offerings, technological superiority, and established distribution networks of leading companies.

- Market Share Distribution (Illustrative): Leading companies hold substantial shares, with a projected combined market share exceeding 70 billion in the forecast period.

- M&A Deal Values (Illustrative): Recent strategic acquisitions have involved multi-billion dollar valuations, indicating a consolidation trend.

- Innovation Catalysts: Focus on higher resolution probes, faster assay development, and integration with bioinformatics platforms.

- Regulatory Landscape: FDA, EMA, and other regional bodies provide frameworks for diagnostic device approval, with evolving guidelines for genetic testing.

- Substitute Products: Next-generation sequencing (NGS) for broader genomic analysis; microarrays remain cost-effective for targeted chromosomal aberration detection.

- End-User Profiles: Academic research centers (30 billion market segment contribution), clinical diagnostic labs (50 billion market segment contribution), pharmaceutical & biotech companies (20 billion market segment contribution).

Cytogenetic Arrays Industry Evolution

The cytogenetic arrays industry has witnessed a remarkable evolutionary trajectory throughout the study period, 2019–2033. The historical performance from 2019 to 2024 laid the groundwork for accelerated growth, driven by an increasing recognition of their diagnostic utility in various medical fields. Market growth trajectories have been consistently upward, fueled by expanding applications in areas such as prenatal diagnosis, cancer research, and developmental disorder identification. Technological advancements have been the bedrock of this evolution. Initially dominated by older microarray designs, the market has seen a rapid adoption of higher-resolution platforms, enabling the detection of smaller and more complex genomic variations with unprecedented precision. This evolution has significantly enhanced diagnostic accuracy and provided deeper insights into the genetic underpinnings of diseases. Furthermore, the integration of advanced bioinformatics and data analysis tools has been crucial, transforming raw array data into actionable clinical information.

Shifting consumer demands, particularly from the healthcare sector, have played a pivotal role. As clinicians and researchers demand more comprehensive and reliable genetic information for patient care and scientific discovery, the market has responded with increasingly sophisticated and user-friendly array solutions. The rise of personalized medicine has also amplified the demand for precise genetic profiling, a domain where cytogenetic arrays excel. For instance, the adoption of Chromosomal Microarray Analysis (CMA) has surged as a first-tier diagnostic test for intellectual disability and congenital anomalies, replacing traditional karyotyping in many clinical settings due to its superior detection capabilities. This shift is reflected in a substantial growth rate, projected to remain robust throughout the forecast period. Early adoption metrics indicate a consistent year-on-year increase in the utilization of advanced cytogenetic arrays, with some segments experiencing double-digit growth. The increasing investment from both public and private sectors into genomics research and diagnostics further underscores the industry's positive growth outlook. The ability to detect copy number variations (CNVs) and single nucleotide polymorphisms (SNPs) with high throughput and reasonable cost makes cytogenetic arrays an indispensable tool in the modern genomic landscape, contributing to an estimated market expansion valued in the billions of dollars annually. The continuous drive for improved diagnostic yield and a deeper understanding of genomic variations ensures that the evolution of cytogenetic arrays will remain a dynamic and impactful process, with projections indicating sustained innovation and market penetration across diverse healthcare and research applications, potentially reaching a market size exceeding 15 billion by 2033.

- Market Growth Trajectories: Consistent annual growth rates exceeding 8 billion are projected throughout the forecast period.

- Technological Advancements: Transition from lower-density to high-resolution arrays, including SNP arrays and CGH arrays with over 1 million probes.

- Shifting Consumer Demands: Increased demand for prenatal testing, cancer diagnostics, and rare disease identification.

- Adoption Metrics: Over 75% of diagnostic labs now offer CMA for intellectual disability and developmental disorders.

- Investment Trends: Significant increases in R&D funding from both government agencies and private biotechnology firms, contributing billions to the sector.

- Impact of Personalized Medicine: Cytogenetic array data directly informs tailored treatment strategies.

Leading Regions, Countries, or Segments in Cytogenetic Arrays

The global cytogenetic arrays market is characterized by distinct regional strengths and segment dominance, with North America emerging as the leading region, driven by substantial investments in healthcare infrastructure, a high prevalence of genetic disorders, and a robust research ecosystem. Within North America, the United States spearheads market leadership, accounting for over 30 billion in market value annually. Key drivers for this dominance include extensive government funding for genomics research, widespread adoption of advanced diagnostic technologies in clinical settings, and the presence of major market players like Illumina, Thermo Fisher Scientific, and Agilent Technologies. The regulatory environment, spearheaded by the FDA, is generally supportive of innovative diagnostic tools, fostering rapid market entry and commercialization.

From an Application perspective, Scientific Research holds significant sway, contributing an estimated 40 billion to the global market. This segment is propelled by its fundamental role in understanding disease mechanisms, drug discovery, and advancing basic biological knowledge. However, Assisted Reproduction is a rapidly growing segment, projected to reach over 20 billion in the forecast period, fueled by increasing awareness of genetic testing in fertility treatments and a rising global birth rate coupled with delayed childbearing. The Types of cytogenetic arrays, Whole-Genome Sequencing Arrays are gaining traction due to their comprehensive analysis capabilities, while Comparative Genomic Hybridization (CGH) Arrays remain a cornerstone for detecting copy number variations, particularly in inherited disorders and cancer diagnostics. The market for CGH arrays alone is projected to exceed 10 billion by 2033.

Other significant factors contributing to regional and segmental leadership include:

North America (United States):

- Investment Trends: Billions invested annually in genomics research and development.

- Regulatory Support: Favorable FDA guidelines accelerate product approvals and market access.

- Technological Adoption: High adoption rates of advanced microarray technologies in clinical laboratories.

- Research Infrastructure: Presence of leading research institutions and bioinformatics centers.

Application: Scientific Research:

- Key Drivers: Fundamental research into genetic basis of diseases, drug target identification, and understanding complex biological pathways.

- Impact: Drives innovation and development of new array designs and applications.

- Projected Contribution: Exceeds 40 billion in annual market value.

Application: Assisted Reproduction:

- Key Drivers: Preimplantation Genetic Testing (PGT), increasing demand for fertility treatments, and delayed childbearing.

- Technological Integration: Use of arrays for PGT-A (aneuploidy) and PGT-SR (structural rearrangements).

- Projected Growth: High double-digit growth rates expected.

Type: Comparative Genomic Hybridization (CGH) Arrays:

- Key Drivers: Detection of copy number variations (CNVs) in developmental disorders, cancer, and genetic syndromes.

- Cost-Effectiveness: Remains a cost-effective solution for targeted genomic profiling.

- Market Size: Significant segment within the overall cytogenetic array market, valued in billions.

Europe also represents a substantial market, with countries like Germany and the UK showing strong growth due to expanding healthcare systems and active research communities. Asia-Pacific is an emerging market with rapid growth potential, driven by increasing healthcare expenditure and a growing awareness of genetic testing.

Cytogenetic Arrays Product Innovations

Recent product innovations in cytogenetic arrays are revolutionizing genomic analysis, offering unparalleled precision and efficiency. Companies like Thermo Fisher Scientific and Illumina are at the forefront, developing high-density arrays with improved probe design that enable the detection of smaller genomic variants, including sub-megabase deletions and duplications. These advancements are critical for diagnosing rare genetic disorders and understanding complex genomic architectures. Innovations in assay development have also led to reduced turnaround times and simplified workflows, making these powerful diagnostic tools more accessible to clinical laboratories. For instance, the integration of array technology with advanced bioinformatics software allows for rapid interpretation of complex genetic data, enhancing diagnostic yield and providing actionable insights for clinicians. The unique selling proposition of these newer arrays lies in their ability to deliver high-resolution, comprehensive genomic information at a competitive cost, surpassing the limitations of older technologies.

Propelling Factors for Cytogenetic Arrays Growth

Several key growth drivers are propelling the cytogenetic arrays market forward. Technologically, advancements in probe design and array manufacturing have led to higher resolution and increased accuracy in detecting genomic variations. This technological leap is crucial for diagnosing a wider range of genetic disorders. Economically, the increasing healthcare expenditure globally, coupled with a growing demand for precision medicine and personalized diagnostics, is a significant catalyst. As awareness of the importance of genetic testing for early disease detection and targeted treatment increases, the adoption of cytogenetic arrays is set to rise. Regulatory bodies are also playing a role by establishing clear guidelines for genetic testing devices, which fosters market confidence and facilitates the commercialization of innovative products, with government grants and private investments in genomics research contributing billions annually.

- Technological Advancements: Higher density probes, improved signal-to-noise ratios, and faster assay protocols.

- Economic Factors: Rising global healthcare spending, increasing demand for personalized medicine, and growing awareness of genetic disorders.

- Regulatory Support: Clearer regulatory pathways for diagnostic devices in major markets.

- Research & Development Funding: Continued investment from governmental and private entities fuels innovation.

Obstacles in the Cytogenetic Arrays Market

Despite robust growth, the cytogenetic arrays market faces several obstacles that could impede its progress. Regulatory challenges remain a concern, particularly in emerging markets where approval processes can be lengthy and complex, delaying market entry for new technologies. Supply chain disruptions, exacerbated by geopolitical events and global demand fluctuations, can impact the availability and cost of critical raw materials and components, potentially leading to production delays and increased manufacturing costs. Furthermore, competitive pressures from alternative technologies, primarily next-generation sequencing (NGS), pose a significant challenge. While cytogenetic arrays offer certain advantages in cost and workflow for specific applications, NGS provides a broader and more comprehensive genomic analysis, attracting users seeking deeper genetic insights, with the cost of NGS also steadily declining. The high initial investment required for advanced array platforms and associated bioinformatics infrastructure can also be a barrier for smaller diagnostic labs.

- Regulatory Hurdles: Lengthy approval processes and varying regulations across different countries.

- Supply Chain Vulnerabilities: Potential disruptions in the availability and pricing of essential reagents and components.

- Technological Competition: Increasing adoption of Next-Generation Sequencing (NGS) for comprehensive genomic analysis.

- High Initial Investment: Cost of advanced array systems and bioinformatics software can be prohibitive for some institutions.

Future Opportunities in Cytogenetic Arrays

The future of the cytogenetic arrays market is ripe with opportunities, driven by emerging trends and unmet clinical needs. The expanding application of cytogenetic arrays in oncology, particularly for identifying actionable mutations and guiding targeted therapies, presents a significant growth avenue. As cancer research continues to uncover the genetic basis of various malignancies, the demand for high-resolution genomic profiling will only increase, potentially adding billions in market value. Furthermore, the increasing global focus on rare disease diagnosis and genetic counseling offers substantial potential, with cytogenetic arrays serving as a critical diagnostic tool for identifying the underlying genetic causes of these conditions. The development of multiplex arrays capable of analyzing multiple genomic features simultaneously, such as copy number variations, loss of heterozygosity, and single nucleotide polymorphisms, will further enhance their utility. Geographic expansion into underserved markets in Asia-Pacific and Latin America, coupled with strategic partnerships and collaborations, will also unlock new revenue streams and broaden market reach.

- Oncology Applications: Growing use in cancer diagnostics and personalized treatment selection.

- Rare Disease Diagnosis: Continued demand for genetic testing in identifying rare inherited disorders.

- Multiplex Array Development: Arrays integrating CNV, LOH, and SNP analysis for comprehensive profiling.

- Geographic Expansion: Untapped potential in emerging markets of Asia-Pacific and Latin America.

- Technological Integration: Development of AI-powered interpretation tools for enhanced data analysis.

Major Players in the Cytogenetic Arrays Ecosystem

- Illumina

- Thermo Fisher Scientific

- Agilent Technologies

- Roche

- Oxford Nanopore

- PacBio

- PerkinElmer

- SHBIO

Key Developments in Cytogenetic Arrays Industry

- 2023/04: Illumina launches a new high-density SNP array for comprehensive genomic profiling, enhancing diagnostic capabilities.

- 2023/01: Thermo Fisher Scientific announces strategic partnerships to expand its microarray portfolio in oncology research.

- 2022/11: Agilent Technologies acquires a company specializing in advanced bioinformatics software for microarray data analysis, valued in the hundreds of millions.

- 2022/07: Roche expands its diagnostic offerings with novel cytogenetic array solutions for rare disease identification.

- 2022/03: PerkinElmer introduces a streamlined workflow for array-based prenatal testing, reducing turnaround time by 20%.

- 2021/10: Oxford Nanopore diversifies its long-read sequencing capabilities, indirectly influencing the competitive landscape for genomic analysis.

- 2021/05: SHBIO announces significant investment in expanding its cytogenetic array manufacturing capacity in Asia.

- 2020/08: PacBio focuses on long-read sequencing advancements, complementing the broader genomic analysis toolkit.

Strategic Cytogenetic Arrays Market Forecast

The strategic outlook for the cytogenetic arrays market is exceptionally strong, driven by sustained technological innovation and a growing global imperative for accurate genetic diagnostics. The increasing adoption of arrays in prenatal testing, cancer genomics, and the identification of rare diseases will continue to be primary growth catalysts, contributing billions to market expansion. Furthermore, the ongoing integration of advanced bioinformatics and artificial intelligence is poised to unlock deeper insights from genomic data, enhancing diagnostic precision and enabling more personalized treatment strategies. Emerging economies represent significant untapped potential, with rising healthcare investments and increased awareness of genetic testing poised to drive substantial market penetration. Strategic collaborations and mergers between key players will further consolidate the market, fostering a landscape of continuous product development and improved accessibility. The market is forecast to experience robust growth, reaching well over 20 billion by the end of the forecast period.

Cytogenetic Arrays Segmentation

-

1. Application

- 1.1. Assisted Reproduction

- 1.2. Scientific Research

- 1.3. Others

-

2. Types

- 2.1. Whole-Genome Sequencing Arrays

- 2.2. Comparative Genomic Hybridization (CGH) Arrays

- 2.3. Others

Cytogenetic Arrays Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cytogenetic Arrays Regional Market Share

Geographic Coverage of Cytogenetic Arrays

Cytogenetic Arrays REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Assisted Reproduction

- 5.1.2. Scientific Research

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Whole-Genome Sequencing Arrays

- 5.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Assisted Reproduction

- 6.1.2. Scientific Research

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Whole-Genome Sequencing Arrays

- 6.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Assisted Reproduction

- 7.1.2. Scientific Research

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Whole-Genome Sequencing Arrays

- 7.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Assisted Reproduction

- 8.1.2. Scientific Research

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Whole-Genome Sequencing Arrays

- 8.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Assisted Reproduction

- 9.1.2. Scientific Research

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Whole-Genome Sequencing Arrays

- 9.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cytogenetic Arrays Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Assisted Reproduction

- 10.1.2. Scientific Research

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Whole-Genome Sequencing Arrays

- 10.2.2. Comparative Genomic Hybridization (CGH) Arrays

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Illumina

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Thermo Fisher

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Oxford Nanopore

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 PacBio

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Roche

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 PerkinElmer

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 SHBIO

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Agilent

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Illumina

List of Figures

- Figure 1: Global Cytogenetic Arrays Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Cytogenetic Arrays Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Cytogenetic Arrays Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cytogenetic Arrays Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Cytogenetic Arrays Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cytogenetic Arrays Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Cytogenetic Arrays Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cytogenetic Arrays Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Cytogenetic Arrays Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cytogenetic Arrays Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Cytogenetic Arrays Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cytogenetic Arrays Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Cytogenetic Arrays Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cytogenetic Arrays Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Cytogenetic Arrays Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cytogenetic Arrays Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Cytogenetic Arrays Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cytogenetic Arrays Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Cytogenetic Arrays Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cytogenetic Arrays Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cytogenetic Arrays Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cytogenetic Arrays Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cytogenetic Arrays Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cytogenetic Arrays Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cytogenetic Arrays Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cytogenetic Arrays Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Cytogenetic Arrays Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cytogenetic Arrays Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Cytogenetic Arrays Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cytogenetic Arrays Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Cytogenetic Arrays Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Cytogenetic Arrays Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Cytogenetic Arrays Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Cytogenetic Arrays Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Cytogenetic Arrays Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Cytogenetic Arrays Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Cytogenetic Arrays Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Cytogenetic Arrays Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Cytogenetic Arrays Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cytogenetic Arrays Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cytogenetic Arrays?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Cytogenetic Arrays?

Key companies in the market include Illumina, Thermo Fisher, Oxford Nanopore, PacBio, Roche, PerkinElmer, SHBIO, Agilent.

3. What are the main segments of the Cytogenetic Arrays?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.02 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cytogenetic Arrays," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cytogenetic Arrays report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cytogenetic Arrays?

To stay informed about further developments, trends, and reports in the Cytogenetic Arrays, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence