Key Insights

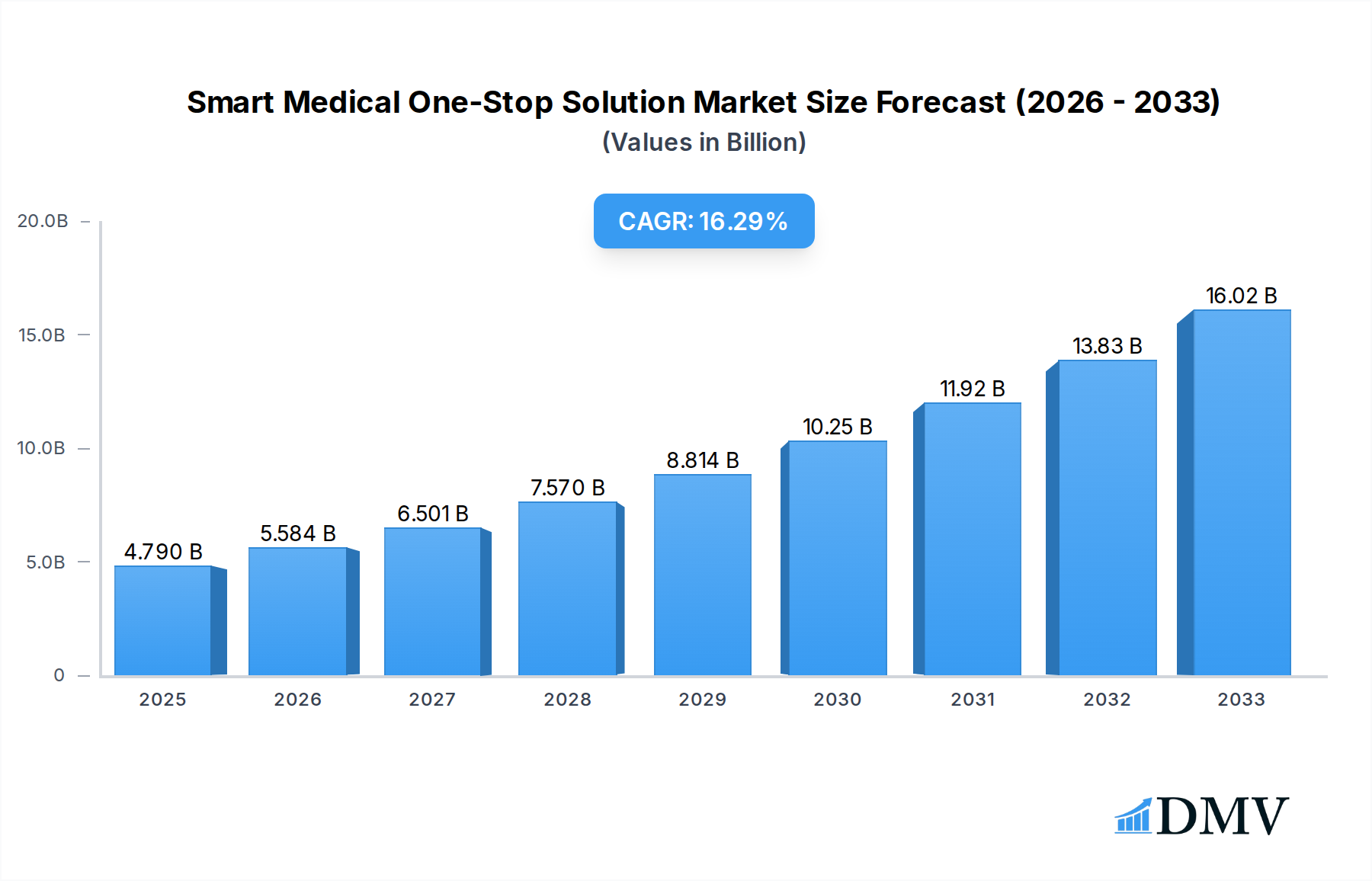

The global Smart Medical One-Stop Solution market is poised for significant expansion, projected to reach $4.79 billion in 2025 with a robust Compound Annual Growth Rate (CAGR) of 16.64%. This impressive growth trajectory is fueled by a confluence of escalating healthcare demands, rapid technological advancements in medical devices and software, and an increasing emphasis on integrated patient care systems. The market is witnessing a paradigm shift towards intelligent, interconnected healthcare ecosystems designed to streamline operations, enhance diagnostic accuracy, and improve patient outcomes. Key drivers include the growing prevalence of chronic diseases, the aging global population, and the urgent need for efficient healthcare delivery models. Furthermore, the digital transformation within healthcare, encompassing AI-powered diagnostics, IoT-enabled patient monitoring, and cloud-based data management, is a crucial catalyst. The adoption of smart solutions is particularly pronounced in hospitals seeking to optimize resource allocation, manage patient flow effectively, and reduce administrative burdens. Clinics and other medical institutions are also increasingly investing in these comprehensive systems to elevate their service offerings and maintain competitiveness.

Smart Medical One-Stop Solution Market Size (In Billion)

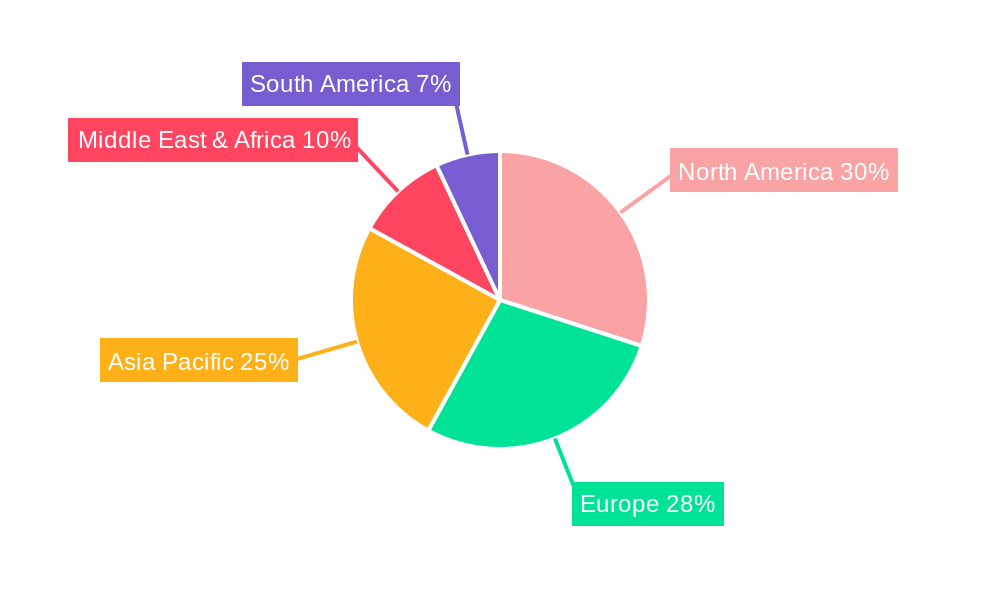

The market's segmentation into Front Office Business Systems and Logistics Business Systems highlights the multifaceted nature of these integrated solutions. Front office systems focus on patient registration, appointment scheduling, billing, and electronic health records (EHRs), directly impacting patient experience and administrative efficiency. Logistics systems, on the other hand, encompass inventory management, supply chain optimization, and equipment tracking, ensuring seamless operational flow and cost reduction. Key trends shaping the market include the rise of telemedicine and remote patient monitoring, the integration of big data analytics for predictive healthcare, and the increasing adoption of cybersecurity measures to protect sensitive patient data. While the market benefits from strong growth drivers, potential restraints such as high initial implementation costs, data privacy concerns, and the need for skilled IT professionals could pose challenges. However, the overwhelming benefits of enhanced efficiency, improved patient care, and cost savings are expected to drive sustained market penetration across North America, Europe, and the rapidly growing Asia Pacific region, with China and India emerging as significant growth hubs.

Smart Medical One-Stop Solution Company Market Share

Smart Medical One-Stop Solution Market Composition & Trends

The global Smart Medical One-Stop Solution market is characterized by a dynamic and evolving landscape, influenced by a confluence of technological innovation, increasing healthcare demands, and strategic consolidations. Market concentration is a key factor, with major players like GE Healthcare, Philips, and Medtronic holding significant market share, estimated to be over 60% combined. However, emerging players such as Neusoft Corporation, Shenzhen SUNDRAY Technology, and Midea Biomedical are progressively carving out their niches, especially in the Asia-Pacific region. Innovation catalysts are primarily driven by advancements in artificial intelligence (AI), the Internet of Medical Things (IoMT), big data analytics, and wearable technology, all of which are integral to providing comprehensive healthcare solutions. The regulatory landscape, while generally supportive of digital health initiatives, presents a complex patchwork of compliance requirements across different jurisdictions, impacting the speed and scope of market penetration. Substitute products, primarily fragmented or less integrated healthcare IT solutions, are steadily being replaced by the holistic approach offered by one-stop solutions. End-user profiles range from large hospital networks seeking to optimize operational efficiency and patient care to smaller clinics aiming to enhance their diagnostic and administrative capabilities. Merger and acquisition (M&A) activities are robust, with deal values projected to exceed $25 billion during the study period (2019–2033), as companies strategically acquire complementary technologies and expand their geographical reach. For instance, recent M&A activities have focused on integrating AI-powered diagnostic tools and remote patient monitoring platforms. The market share distribution indicates a healthy competition, with the top five players holding approximately 75% of the market by the base year of 2025, but this is expected to see a gradual shift towards a more fragmented landscape by 2033 due to sustained innovation from mid-tier and niche providers.

Smart Medical One-Stop Solution Industry Evolution

The Smart Medical One-Stop Solution industry has undergone a remarkable transformation, evolving from rudimentary digital health offerings to sophisticated, integrated platforms designed to streamline every facet of healthcare delivery. Over the study period (2019–2033), the market has witnessed consistent and robust growth trajectories, fueled by a confluence of technological advancements, shifting consumer demands, and supportive government initiatives. In the historical period (2019–2024), the industry saw foundational growth, with early adopters recognizing the potential of digital integration. Adoption metrics during this phase were primarily driven by the need for improved hospital management systems and initial forays into telemedicine. By the base year of 2025, the market is projected to reach an estimated $150 billion, with a projected compound annual growth rate (CAGR) of approximately 18% during the forecast period (2025–2033). This exponential growth is underpinned by rapid technological advancements. The integration of Artificial Intelligence (AI) and Machine Learning (ML) has been a pivotal development, enabling predictive diagnostics, personalized treatment plans, and enhanced operational efficiency within healthcare institutions. The Internet of Medical Things (IoMT) has further revolutionized the industry by facilitating seamless data flow between medical devices, patients, and healthcare providers, leading to improved remote patient monitoring and proactive health management.

Shifting consumer demands have also played a crucial role in shaping the industry's evolution. Patients today expect greater convenience, personalized care, and greater access to their health information. This has spurred the development of patient portals, mobile health applications, and telehealth services, all of which are key components of a comprehensive one-stop solution. Medical institutions, in response to these demands and the increasing pressure to optimize costs and improve patient outcomes, are actively investing in smart medical solutions. The adoption of Electronic Health Records (EHRs) has become widespread, laying the groundwork for more sophisticated data integration and analysis. Furthermore, the COVID-19 pandemic acted as a significant accelerator, highlighting the critical need for robust digital health infrastructure, including telemedicine, remote monitoring, and efficient healthcare resource management. This surge in demand for resilient and agile healthcare systems has propelled the market forward, encouraging further innovation and investment. The industry's evolution is marked by a transition from standalone software solutions to fully integrated ecosystems that encompass everything from front-office administrative tasks and patient engagement to sophisticated diagnostic tools and supply chain management. This all-encompassing approach is not merely a trend but a fundamental shift in how healthcare is conceived, delivered, and managed, promising continued innovation and expansion throughout the forecast period.

Leading Regions, Countries, or Segments in Smart Medical One-Stop Solution

The global Smart Medical One-Stop Solution market is a complex ecosystem where regional strengths, national policies, and specific application segments converge to drive growth and innovation. Among the key segments, the Hospital application stands out as the dominant force, commanding the largest market share and influencing the direction of innovation. This dominance is attributed to several critical factors, including the inherent complexity of hospital operations, the substantial patient volumes they manage, and their significant investment capacity in advanced healthcare technologies. Hospitals, by their nature, require integrated solutions that can manage everything from patient registration and scheduling (Front Office Business System) to inventory management and equipment maintenance (Logistics Business System). The sheer volume of data generated within a hospital setting, encompassing patient records, diagnostic imaging, laboratory results, and administrative information, necessitates a unified and intelligent system to ensure efficiency, accuracy, and improved patient outcomes.

The United States and China are identified as the leading countries in this segment, driven by substantial healthcare expenditures, proactive government initiatives promoting digital health adoption, and the presence of major market players like GE Healthcare, Philips, and Neusoft Corporation. In the United States, a mature healthcare market with a strong emphasis on technological integration and patient-centric care fuels the demand for comprehensive one-stop solutions. Federal incentives and a robust research and development ecosystem further bolster this growth. China, on the other hand, is experiencing rapid expansion due to massive investments in its healthcare infrastructure, a burgeoning population, and government-backed initiatives to digitalize healthcare services. The rapid proliferation of smart hospitals and the increasing adoption of AI in diagnostics are key drivers here.

Within the Hospital application, the Front Office Business System segment is particularly influential. This sub-segment encompasses patient management, appointment scheduling, billing, and revenue cycle management. Its criticality lies in its direct impact on patient experience and operational efficiency. A well-integrated front office system reduces wait times, streamlines patient intake, and optimizes financial workflows, directly contributing to both patient satisfaction and institutional profitability. Key drivers for the dominance of hospitals and front office systems include:

- High Investment Capacity: Hospitals possess the financial resources to invest in expensive, integrated smart medical solutions, including advanced diagnostic equipment, robust IT infrastructure, and comprehensive software suites.

- Complex Operational Needs: Managing large patient volumes, diverse medical specialties, and intricate administrative processes necessitates integrated systems that can handle a wide array of functions seamlessly.

- Regulatory Compliance & Data Management: Hospitals are under immense pressure to comply with stringent healthcare regulations (e.g., HIPAA in the US, GDPR in Europe) and manage vast amounts of sensitive patient data. One-stop solutions offer the infrastructure for secure and efficient data handling and reporting.

- Focus on Patient Experience: Improving patient journey, from initial contact to post-treatment follow-up, is a paramount concern. Front office systems are central to achieving this by offering convenient appointment booking, clear communication channels, and efficient administrative processes.

- Government Initiatives and Funding: Many governments worldwide are actively promoting the adoption of digital health technologies in hospitals through grants, subsidies, and supportive policies, recognizing their role in improving healthcare accessibility and quality.

While Clinics and Medical Institutions also represent significant markets, their adoption rates and investment capacities are generally lower compared to large hospitals, leading to a more fragmented demand for specific functionalities rather than fully integrated one-stop solutions. However, the growth in telehealth and remote patient monitoring is driving increased adoption of integrated solutions even in these smaller settings, suggesting a future convergence of needs across all healthcare providers. The strategic importance of the hospital segment and its front office operations will continue to shape the direction of the Smart Medical One-Stop Solution market for the foreseeable future.

Smart Medical One-Stop Solution Product Innovations

Product innovations in the Smart Medical One-Stop Solution market are rapidly transforming healthcare delivery by offering unprecedented integration and intelligence. Companies are focusing on developing AI-powered diagnostic tools that can analyze medical images with remarkable accuracy, reducing diagnostic turnaround times and improving early detection rates. For instance, solutions incorporating advanced machine learning algorithms for radiology and pathology are becoming increasingly sophisticated. Furthermore, the seamless integration of IoMT devices, from smart wearables for continuous patient monitoring to connected medical equipment, allows for real-time data capture and transmission. This enables proactive interventions and personalized treatment plans, moving healthcare from reactive to predictive. Unique selling propositions often lie in the ability of these solutions to unify disparate data streams into a single, actionable platform, enhancing clinician workflow and patient engagement through intuitive interfaces and patient portals. Technological advancements are also emphasizing interoperability, ensuring that new solutions can seamlessly integrate with existing hospital IT infrastructure, minimizing disruption and maximizing ROI for healthcare providers.

Propelling Factors for Smart Medical One-Stop Solution Growth

Several key growth drivers are propelling the Smart Medical One-Stop Solution market forward. Technologically, the exponential advancements in Artificial Intelligence (AI), Machine Learning (ML), and the Internet of Medical Things (IoMT) are fundamental. These technologies enable predictive diagnostics, personalized medicine, and seamless data integration, enhancing both clinical and operational efficiency. Economically, the increasing global healthcare expenditure, driven by aging populations and the rising prevalence of chronic diseases, creates a perpetual demand for innovative healthcare solutions. Government initiatives and policies promoting digital health adoption, such as incentives for EHR implementation and telehealth expansion, also play a crucial role. For example, the widespread adoption of AI-powered diagnostic imaging analysis by regulatory bodies like the FDA is a significant catalyst.

Obstacles in the Smart Medical One-Stop Solution Market

Despite robust growth, the Smart Medical One-Stop Solution market faces several significant obstacles. Regulatory challenges remain a primary concern, with varying data privacy and security compliance requirements across different countries and regions (e.g., HIPAA in the US, GDPR in Europe) posing complex integration hurdles. Supply chain disruptions, exacerbated by geopolitical events and global pandemics, can impact the availability of critical hardware components and lead to increased costs and delivery delays, affecting market expansion. Competitive pressures from both established giants like GE Healthcare and Philips, and agile niche players, can lead to price wars and necessitate continuous innovation to maintain market share. Quantifiable impacts include potential delays in product rollouts by up to 18 months and an estimated 10-15% increase in operational costs due to compliance complexities.

Future Opportunities in Smart Medical One-Stop Solution

Emerging opportunities in the Smart Medical One-Stop Solution market are abundant and poised to shape its future trajectory. The expansion into underdeveloped markets in Africa and Southeast Asia presents a significant untapped potential, driven by increasing healthcare needs and growing digital infrastructure. The continued advancement of personalized medicine, enabled by genomic data integration and AI-driven insights, offers a fertile ground for innovation. Furthermore, the growing consumer demand for convenient, at-home healthcare solutions is driving the expansion of telehealth and remote patient monitoring, creating new revenue streams and user bases. The integration of blockchain technology for enhanced data security and interoperability also represents a promising avenue for future development, ensuring greater trust and efficiency in healthcare data management.

Major Players in the Smart Medical One-Stop Solution Ecosystem

- GE Healthcare

- Philips

- Abbott

- Boston Scientific

- Telekom Malaysia

- Medtronic

- Neusoft Corporation

- Shenzhen SUNDRAY Technology

- Avalue Technology

- Shenzhen Mindray Bio-Medical Electronics

- Midea Biomedical

- Draeger

- VBRl Sverige

- Alghanim Technologies

- Nihon Kohden

- Biotronik

- Glory View Technology

- Huawei

Key Developments in Smart Medical One-Stop Solution Industry

- 2023 September: Philips announced a strategic partnership with Microsoft to accelerate digital transformation in healthcare, focusing on AI-driven solutions for patient monitoring and care management.

- 2023 October: GE Healthcare launched its new AI-powered imaging platform, EdisonAI, enhancing diagnostic accuracy and workflow efficiency for radiologists.

- 2024 January: Medtronic acquired a leading remote patient monitoring company, expanding its portfolio of connected care solutions for chronic disease management.

- 2024 March: Neusoft Corporation revealed a comprehensive smart hospital solution suite, integrating AI, big data, and cloud computing for comprehensive hospital management.

- 2024 April: Shenzhen SUNDRAY Technology introduced its latest generation of IoMT devices, offering enhanced real-time patient data collection and transmission capabilities.

- 2024 May: Huawei unveiled its cloud-based healthcare platform, aiming to provide scalable and secure digital solutions for medical institutions globally.

- 2024 June: Midea Biomedical announced its entry into the smart medical device market with a range of connected diagnostic equipment designed for clinics and small hospitals.

- 2024 July: Abbott received regulatory approval for its new AI-enabled cardiac monitoring system, enabling more precise detection of arrhythmias.

- 2024 August: Boston Scientific expanded its digital health offerings with a new platform for post-operative patient management, aiming to reduce readmission rates.

Strategic Smart Medical One-Stop Solution Market Forecast

The strategic Smart Medical One-Stop Solution market forecast indicates a robust growth trajectory driven by continuous technological advancements and increasing demand for integrated healthcare. The convergence of AI, IoMT, and big data analytics will further enhance the capabilities of these solutions, enabling predictive and personalized healthcare at an unprecedented scale. Emerging markets in Asia-Pacific and Latin America, along with the growing focus on preventative care and telehealth, represent significant opportunities for market expansion. The market potential is immense, with projected market sizes reaching over $500 billion by 2033, underscoring the transformative impact of these comprehensive digital health ecosystems on global healthcare delivery.

Smart Medical One-Stop Solution Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Medical Institutions

-

2. Types

- 2.1. Front Office Business System

- 2.2. Logistics Business System

Smart Medical One-Stop Solution Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Smart Medical One-Stop Solution Regional Market Share

Geographic Coverage of Smart Medical One-Stop Solution

Smart Medical One-Stop Solution REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.64% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Medical Institutions

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Front Office Business System

- 5.2.2. Logistics Business System

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Medical Institutions

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Front Office Business System

- 6.2.2. Logistics Business System

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Medical Institutions

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Front Office Business System

- 7.2.2. Logistics Business System

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Medical Institutions

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Front Office Business System

- 8.2.2. Logistics Business System

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Medical Institutions

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Front Office Business System

- 9.2.2. Logistics Business System

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Smart Medical One-Stop Solution Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Medical Institutions

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Front Office Business System

- 10.2.2. Logistics Business System

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 GE Healthcare

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Philips

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Abbott

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Boston Scientific

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Telekom Malaysia

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Medtronic

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Neusoft Corporation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shenzhen SUNDRAY Technology

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Avalue Technology

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Shenzhen Mindray Bio-Medical Electronics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Midea Biomedical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Draeger

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 VBRl Sverige

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Alghanim Technologies

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Nihon Kohden

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Biotronik

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Glory View Technology

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Huawei

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 GE Healthcare

List of Figures

- Figure 1: Global Smart Medical One-Stop Solution Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Smart Medical One-Stop Solution Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Smart Medical One-Stop Solution Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Smart Medical One-Stop Solution Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Smart Medical One-Stop Solution Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Smart Medical One-Stop Solution Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Smart Medical One-Stop Solution Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Smart Medical One-Stop Solution Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Smart Medical One-Stop Solution Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Smart Medical One-Stop Solution Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Smart Medical One-Stop Solution Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Smart Medical One-Stop Solution Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Smart Medical One-Stop Solution Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Smart Medical One-Stop Solution Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Smart Medical One-Stop Solution Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Smart Medical One-Stop Solution Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Smart Medical One-Stop Solution Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Smart Medical One-Stop Solution Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Smart Medical One-Stop Solution Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Smart Medical One-Stop Solution Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Smart Medical One-Stop Solution Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Smart Medical One-Stop Solution Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Smart Medical One-Stop Solution Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Smart Medical One-Stop Solution Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Smart Medical One-Stop Solution Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Smart Medical One-Stop Solution Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Smart Medical One-Stop Solution Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Smart Medical One-Stop Solution Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Smart Medical One-Stop Solution Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Smart Medical One-Stop Solution Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Smart Medical One-Stop Solution Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Smart Medical One-Stop Solution Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Smart Medical One-Stop Solution Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Medical One-Stop Solution?

The projected CAGR is approximately 16.64%.

2. Which companies are prominent players in the Smart Medical One-Stop Solution?

Key companies in the market include GE Healthcare, Philips, Abbott, Boston Scientific, Telekom Malaysia, Medtronic, Neusoft Corporation, Shenzhen SUNDRAY Technology, Avalue Technology, Shenzhen Mindray Bio-Medical Electronics, Midea Biomedical, Draeger, VBRl Sverige, Alghanim Technologies, Nihon Kohden, Biotronik, Glory View Technology, Huawei.

3. What are the main segments of the Smart Medical One-Stop Solution?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.79 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Medical One-Stop Solution," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Medical One-Stop Solution report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Medical One-Stop Solution?

To stay informed about further developments, trends, and reports in the Smart Medical One-Stop Solution, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence