Key Insights

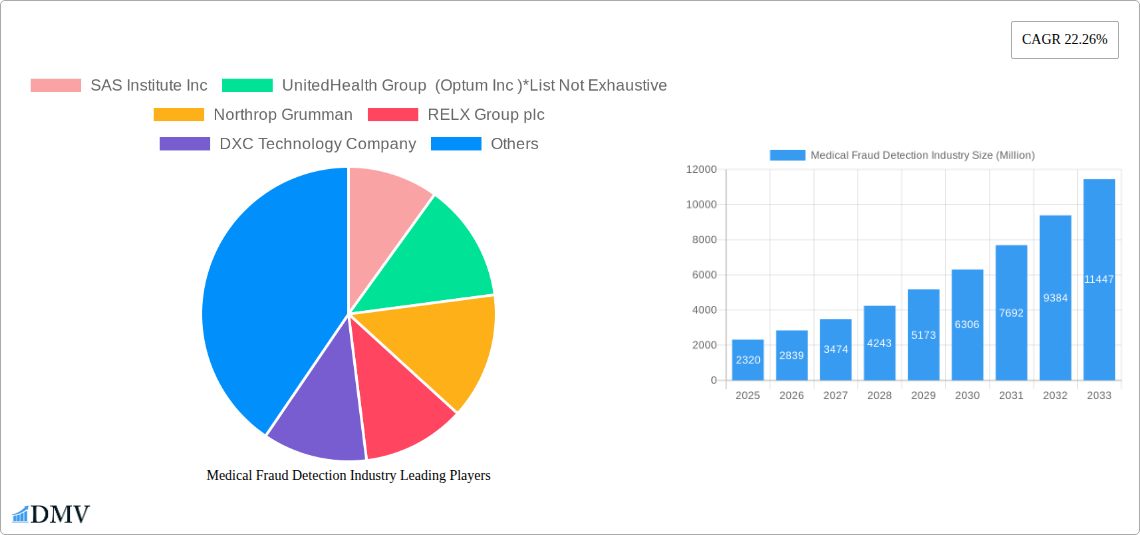

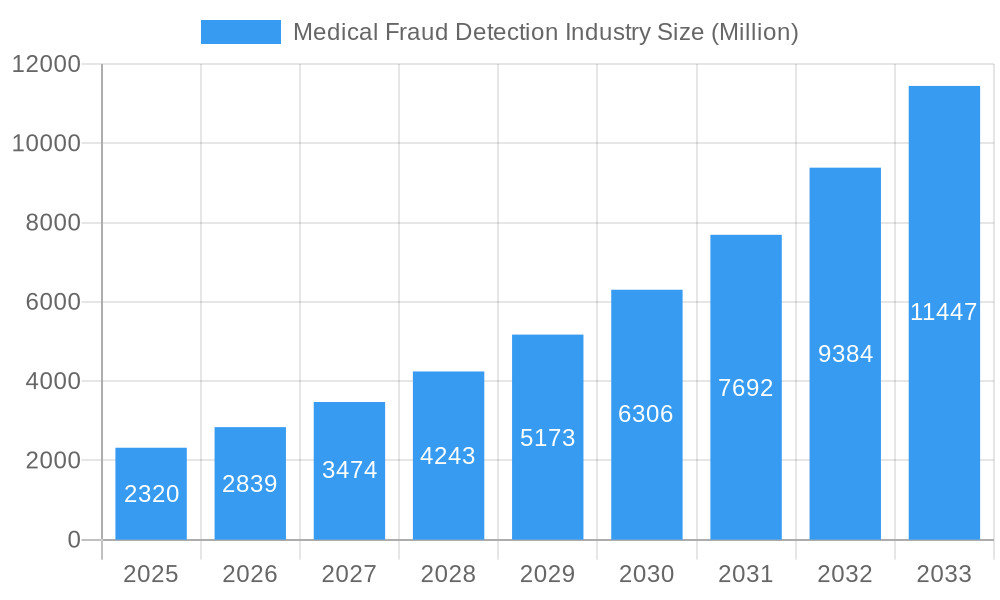

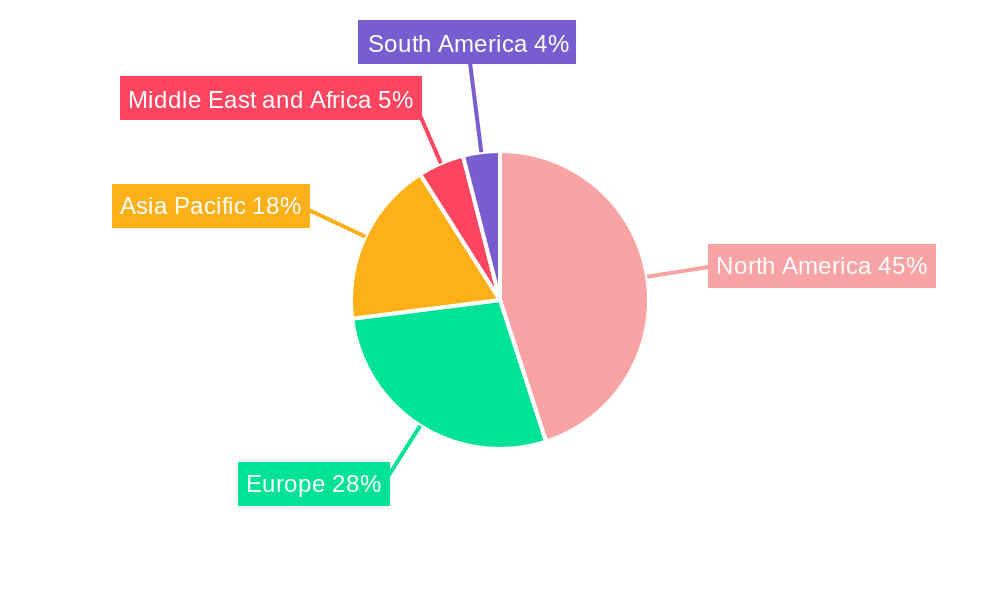

The medical fraud detection market, valued at $2.32 billion in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 22.26% from 2025 to 2033. This significant expansion is driven by several key factors. Rising healthcare costs and increasing instances of fraudulent activities, such as insurance claim manipulation and provider fraud, necessitate robust detection systems. Furthermore, advancements in analytics, particularly in predictive and prescriptive analytics, allow for more accurate identification of suspicious patterns and proactive mitigation strategies. The increasing adoption of data-driven approaches by both private insurance payers and government agencies fuels market growth. Regulations aimed at curbing healthcare fraud also contribute to the market's upward trajectory. The market is segmented by analytics type (descriptive, predictive, prescriptive), application (insurance claim review, payment integrity), and end-user (private payers, government agencies, others). North America currently holds a significant market share, driven by advanced technology adoption and stringent regulatory frameworks. However, Asia-Pacific is anticipated to witness substantial growth due to its expanding healthcare sector and increasing government initiatives to combat fraud.

Medical Fraud Detection Industry Market Size (In Billion)

The competitive landscape includes established players like SAS Institute, UnitedHealth Group (Optum), Northrop Grumman, and RELX Group, alongside technology companies such as IBM and DXC Technology. These companies offer a range of solutions, from sophisticated analytical platforms to specialized consulting services. The market's future growth will likely be influenced by factors such as the development of artificial intelligence (AI) and machine learning (ML)-powered fraud detection tools, the integration of blockchain technology for enhanced data security and transparency, and evolving regulatory landscapes globally. Companies that can effectively leverage these technological advancements and tailor their solutions to specific regional needs will be well-positioned to capitalize on this expanding market.

Medical Fraud Detection Industry Company Market Share

Medical Fraud Detection Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Medical Fraud Detection Industry, projecting a market value exceeding $XX Million by 2033. The study covers the period 2019-2033, with 2025 as the base and estimated year. This report is designed for stakeholders seeking strategic insights into market trends, technological advancements, and competitive landscapes.

Medical Fraud Detection Industry Market Composition & Trends

The Medical Fraud Detection Industry is characterized by a moderately concentrated market, with key players such as SAS Institute Inc, UnitedHealth Group (Optum Inc), Northrop Grumman, RELX Group plc, DXC Technology Company, International Business Machines Corporation (IBM), ExlService Holdings Inc, CGI Inc, McKesson Corporation, and OSP Labs holding significant market share. Market concentration is estimated at xx%, with the top 5 players controlling approximately xx% of the market in 2025. The industry is driven by increasing healthcare expenditures, rising fraud cases, and stringent regulatory compliance requirements.

- Market Share Distribution (2025): SAS Institute Inc (xx%), UnitedHealth Group (Optum Inc) (xx%), Others (xx%).

- Innovation Catalysts: Advancements in AI, machine learning, and big data analytics are fostering innovation.

- Regulatory Landscape: HIPAA and other regulations are driving demand for robust fraud detection solutions.

- Substitute Products: Limited viable substitutes exist, indicating strong market resilience.

- M&A Activities: The industry has witnessed significant M&A activity, with deal values totaling over $XX Million in the historical period (2019-2024). Consolidation is expected to continue, driven by the need for enhanced technological capabilities and broader market reach.

Medical Fraud Detection Industry Industry Evolution

The Medical Fraud Detection Industry has experienced substantial growth during the historical period (2019-2024), with a CAGR of xx%. This growth is attributed to a confluence of factors, including the increasing sophistication of fraud schemes, heightened regulatory scrutiny, and the rising adoption of advanced analytics technologies. The market is projected to maintain a robust growth trajectory during the forecast period (2025-2033), reaching $XX Million by 2033, with a projected CAGR of xx%. Technological advancements, particularly in AI and machine learning, are significantly enhancing the accuracy and efficiency of fraud detection systems. The increasing demand for real-time fraud detection capabilities is also fueling market expansion. Furthermore, the shift towards value-based healthcare models is further driving the demand for more sophisticated and proactive fraud detection solutions, as healthcare providers and payers seek to optimize resource allocation and minimize financial losses. This evolution is reflected in the increasing adoption of predictive and prescriptive analytics, alongside the continued use of descriptive analytics. The adoption rate of advanced analytics solutions increased by xx% between 2020 and 2024, and this trend is expected to continue. Rising consumer awareness of medical fraud and a growing demand for transparent healthcare practices are also driving the need for enhanced fraud detection solutions.

Leading Regions, Countries, or Segments in Medical Fraud Detection Industry

North America currently dominates the Medical Fraud Detection Industry, driven by high healthcare spending, stringent regulations, and the early adoption of advanced technologies.

- By Type: Predictive analytics holds the largest market share, followed by descriptive and prescriptive analytics. The predictive analytics segment is experiencing rapid growth due to its ability to proactively identify potential fraud.

- By Application: Review of insurance claims is the dominant application segment, driven by the large volume of claims processed annually and the high incidence of fraudulent claims within this segment. Payment integrity is also a rapidly growing segment.

- By End User: Private insurance payers are the largest end-user segment, closely followed by government agencies. The growing focus on cost containment and compliance across both sectors is pushing demand for advanced solutions.

Key Drivers:

- North America: High healthcare expenditure, stringent regulations, early adoption of AI and ML technologies.

- Europe: Increasing government initiatives to combat healthcare fraud, growing awareness of fraud risks.

- Asia Pacific: Rising healthcare spending, expanding insurance coverage, technological advancements.

Medical Fraud Detection Industry Product Innovations

Recent innovations include the integration of AI and machine learning algorithms to enhance fraud detection accuracy and efficiency. New products leverage advanced analytics, natural language processing, and biometric authentication to detect increasingly sophisticated fraud schemes. These advancements lead to improved accuracy in identifying fraudulent claims, reducing false positives, and enhancing the overall effectiveness of fraud detection processes. The emphasis is shifting towards predictive and prescriptive analytics, empowering proactive fraud prevention and mitigation strategies.

Propelling Factors for Medical Fraud Detection Industry Growth

The growth of the Medical Fraud Detection Industry is primarily driven by the escalating cost of healthcare fraud, stricter government regulations, and rapid technological advancements. AI and machine learning are transforming the ability to analyze large datasets, identify patterns, and predict fraudulent activities. This coupled with the increasing use of big data analytics allows for efficient processing and analysis of vast amounts of healthcare data, enabling quicker and more effective fraud detection. The implementation of stricter regulatory requirements globally is also driving demand for these solutions.

Obstacles in the Medical Fraud Detection Industry Market

Key obstacles include the high cost of implementing advanced analytics solutions, the complexity of healthcare data, and the challenges associated with data integration and interoperability. Data privacy regulations pose additional challenges, requiring careful consideration of ethical and legal implications when using patient data. Competitive pressures are another important factor influencing market growth. The market is also impacted by a shortage of skilled professionals specializing in healthcare data analytics and fraud detection.

Future Opportunities in Medical Fraud Detection Industry

Future opportunities lie in the expansion into emerging markets, the integration of blockchain technology for enhanced data security and transparency, and the development of more sophisticated AI-powered solutions that can adapt to evolving fraud tactics. The increasing use of telehealth and remote patient monitoring creates new challenges and opportunities for fraud detection.

Major Players in the Medical Fraud Detection Industry Ecosystem

- SAS Institute Inc

- UnitedHealth Group (Optum Inc)

- Northrop Grumman

- RELX Group plc

- DXC Technology Company

- International Business Machines Corporation (IBM)

- ExlService Holdings Inc

- CGI Inc

- McKesson Corporation

- OSP Labs

Key Developments in Medical Fraud Detection Industry Industry

- March 2022: Veriff launched biometrics-powered identity verification solutions for healthcare, leveraging AI and facial recognition.

- February 2022: The CLHIA launched an initiative to pool claims data and use AI for enhanced fraud detection.

Strategic Medical Fraud Detection Industry Market Forecast

The Medical Fraud Detection Industry is poised for significant growth, driven by the rising prevalence of healthcare fraud, technological advancements, and increasing regulatory scrutiny. The forecast period (2025-2033) is expected to witness substantial adoption of AI-powered solutions and expansion into new markets, offering substantial opportunities for industry players. The market's future trajectory points towards an increasing focus on preventative measures and proactive fraud detection capabilities, underpinned by continuous technological innovation.

Medical Fraud Detection Industry Segmentation

-

1. Type

- 1.1. Descriptive Analytics

- 1.2. Predictive Analytics

- 1.3. Prescriptive Analytics

-

2. Application

- 2.1. Review of Insurance Claims

- 2.2. Payment Integrity

-

3. End User

- 3.1. Private Insurance Payers

- 3.2. Government Agencies

- 3.3. Other End Users

Medical Fraud Detection Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Medical Fraud Detection Industry Regional Market Share

Geographic Coverage of Medical Fraud Detection Industry

Medical Fraud Detection Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Descriptive Analytics

- 5.1.2. Predictive Analytics

- 5.1.3. Prescriptive Analytics

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Review of Insurance Claims

- 5.2.2. Payment Integrity

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Private Insurance Payers

- 5.3.2. Government Agencies

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Medical Fraud Detection Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Descriptive Analytics

- 6.1.2. Predictive Analytics

- 6.1.3. Prescriptive Analytics

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Review of Insurance Claims

- 6.2.2. Payment Integrity

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Private Insurance Payers

- 6.3.2. Government Agencies

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Medical Fraud Detection Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Descriptive Analytics

- 7.1.2. Predictive Analytics

- 7.1.3. Prescriptive Analytics

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Review of Insurance Claims

- 7.2.2. Payment Integrity

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Private Insurance Payers

- 7.3.2. Government Agencies

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Medical Fraud Detection Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Descriptive Analytics

- 8.1.2. Predictive Analytics

- 8.1.3. Prescriptive Analytics

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Review of Insurance Claims

- 8.2.2. Payment Integrity

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Private Insurance Payers

- 8.3.2. Government Agencies

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Medical Fraud Detection Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Descriptive Analytics

- 9.1.2. Predictive Analytics

- 9.1.3. Prescriptive Analytics

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Review of Insurance Claims

- 9.2.2. Payment Integrity

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Private Insurance Payers

- 9.3.2. Government Agencies

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East and Africa Medical Fraud Detection Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Descriptive Analytics

- 10.1.2. Predictive Analytics

- 10.1.3. Prescriptive Analytics

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Review of Insurance Claims

- 10.2.2. Payment Integrity

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Private Insurance Payers

- 10.3.2. Government Agencies

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. South America Medical Fraud Detection Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Descriptive Analytics

- 11.1.2. Predictive Analytics

- 11.1.3. Prescriptive Analytics

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Review of Insurance Claims

- 11.2.2. Payment Integrity

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Private Insurance Payers

- 11.3.2. Government Agencies

- 11.3.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SAS Institute Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 UnitedHealth Group (Optum Inc )*List Not Exhaustive

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Northrop Grumman

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 RELX Group plc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 DXC Technology Company

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 International Business Machines Corporation (IBM)

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ExlService Holdings Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 CGI Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 McKesson Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 OSP Labs

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 SAS Institute Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Fraud Detection Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Medical Fraud Detection Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Medical Fraud Detection Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Medical Fraud Detection Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Medical Fraud Detection Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Medical Fraud Detection Industry Revenue (Million), by End User 2025 & 2033

- Figure 7: North America Medical Fraud Detection Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America Medical Fraud Detection Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Medical Fraud Detection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Medical Fraud Detection Industry Revenue (Million), by Type 2025 & 2033

- Figure 11: Europe Medical Fraud Detection Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Medical Fraud Detection Industry Revenue (Million), by Application 2025 & 2033

- Figure 13: Europe Medical Fraud Detection Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Medical Fraud Detection Industry Revenue (Million), by End User 2025 & 2033

- Figure 15: Europe Medical Fraud Detection Industry Revenue Share (%), by End User 2025 & 2033

- Figure 16: Europe Medical Fraud Detection Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Medical Fraud Detection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Medical Fraud Detection Industry Revenue (Million), by Type 2025 & 2033

- Figure 19: Asia Pacific Medical Fraud Detection Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Medical Fraud Detection Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Asia Pacific Medical Fraud Detection Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Medical Fraud Detection Industry Revenue (Million), by End User 2025 & 2033

- Figure 23: Asia Pacific Medical Fraud Detection Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Asia Pacific Medical Fraud Detection Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Medical Fraud Detection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Medical Fraud Detection Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East and Africa Medical Fraud Detection Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Medical Fraud Detection Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East and Africa Medical Fraud Detection Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Medical Fraud Detection Industry Revenue (Million), by End User 2025 & 2033

- Figure 31: Middle East and Africa Medical Fraud Detection Industry Revenue Share (%), by End User 2025 & 2033

- Figure 32: Middle East and Africa Medical Fraud Detection Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Middle East and Africa Medical Fraud Detection Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Medical Fraud Detection Industry Revenue (Million), by Type 2025 & 2033

- Figure 35: South America Medical Fraud Detection Industry Revenue Share (%), by Type 2025 & 2033

- Figure 36: South America Medical Fraud Detection Industry Revenue (Million), by Application 2025 & 2033

- Figure 37: South America Medical Fraud Detection Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: South America Medical Fraud Detection Industry Revenue (Million), by End User 2025 & 2033

- Figure 39: South America Medical Fraud Detection Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: South America Medical Fraud Detection Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: South America Medical Fraud Detection Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Global Medical Fraud Detection Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 8: Global Medical Fraud Detection Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 13: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 14: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Global Medical Fraud Detection Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Spain Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 23: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 25: Global Medical Fraud Detection Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: China Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: India Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Australia Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Korea Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 33: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 34: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 35: Global Medical Fraud Detection Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: GCC Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Africa Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Global Medical Fraud Detection Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 40: Global Medical Fraud Detection Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 41: Global Medical Fraud Detection Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 42: Global Medical Fraud Detection Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 43: Brazil Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Argentina Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Medical Fraud Detection Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Fraud Detection Industry?

The projected CAGR is approximately 22.26%.

2. Which companies are prominent players in the Medical Fraud Detection Industry?

Key companies in the market include SAS Institute Inc, UnitedHealth Group (Optum Inc )*List Not Exhaustive, Northrop Grumman, RELX Group plc, DXC Technology Company, International Business Machines Corporation (IBM), ExlService Holdings Inc, CGI Inc, McKesson Corporation, OSP Labs.

3. What are the main segments of the Medical Fraud Detection Industry?

The market segments include Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.32 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Healthcare Expenditure; Rise in the Number of Patients Opting for Health Insurance; Growing Pressure to Increase Operational Efficiency and Reduce Healthcare Spending; Increasing Fraudulent Activities in Healthcare.

6. What are the notable trends driving market growth?

Review of Insurance Claims by Application Segment is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Unwillingness to Adopt Healthcare Fraud Analytics.

8. Can you provide examples of recent developments in the market?

In March 2022, Veriff released a new suite of biometrics-powered identity verification solutions designed specifically for the healthcare industry. According to the company, the new offering will utilize artificial intelligence and facial recognition technologies to perform user identification.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Fraud Detection Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Fraud Detection Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Fraud Detection Industry?

To stay informed about further developments, trends, and reports in the Medical Fraud Detection Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence