Key Insights

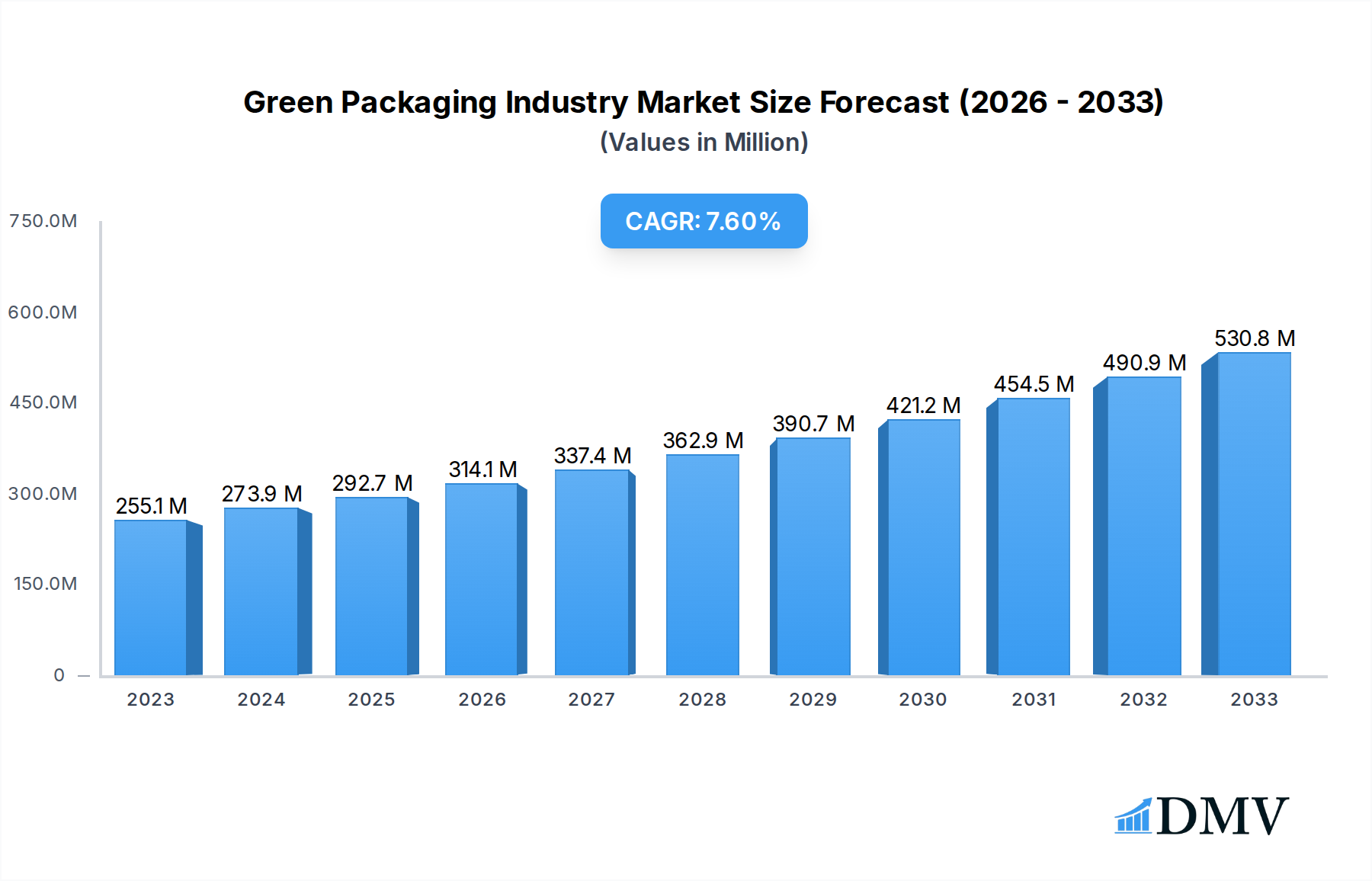

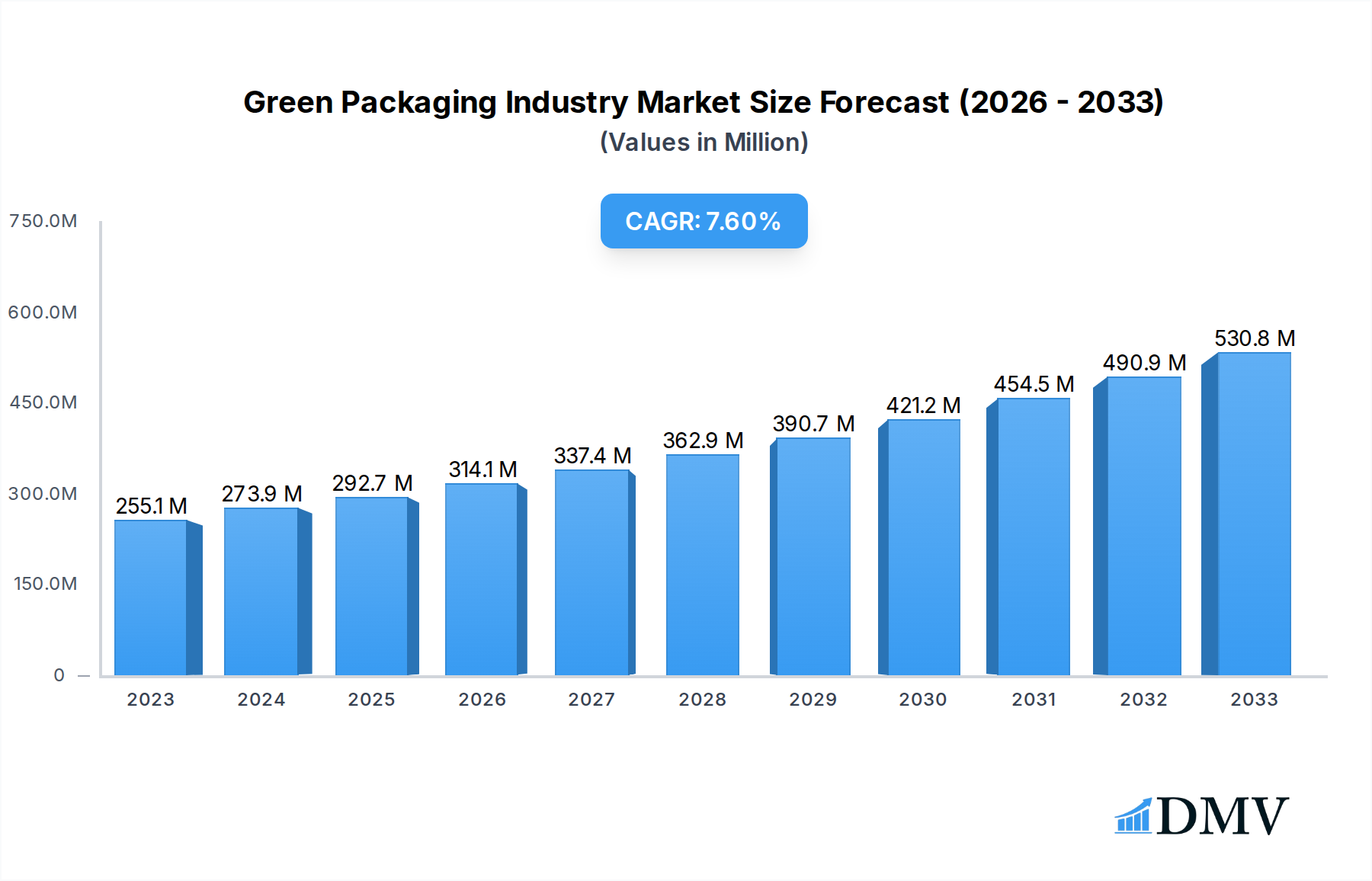

The global Green Packaging market is poised for substantial expansion, projected to reach USD 292.71 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.67% during the forecast period of 2025-2033. This growth is fueled by a confluence of increasing consumer awareness regarding environmental sustainability, stringent government regulations promoting eco-friendly alternatives, and a growing preference for products packaged in recyclable, biodegradable, and reusable materials. The industry is witnessing a significant shift from traditional packaging solutions to innovative green alternatives across various sectors. Key drivers include the rising demand for ethically sourced and environmentally responsible products, particularly within the food and beverage, and cosmetics and personal care industries. Furthermore, advancements in material science are continuously introducing novel biodegradable and compostable packaging options, expanding the addressable market and offering greater flexibility to manufacturers.

Green Packaging Industry Market Size (In Million)

The dominant trend within the Green Packaging market is the increasing adoption of reusable packaging solutions, driven by their long-term cost-effectiveness and significant reduction in waste generation. Degradable and recycled packaging also represent substantial segments, catering to diverse application needs. Material innovations are leaning towards paper-based and glass packaging due to their inherent recyclability and lower environmental impact compared to certain plastics. While the market presents immense opportunities, certain restraints, such as higher initial costs for some green packaging alternatives and the need for robust recycling infrastructure, are being addressed through technological advancements and policy initiatives. The Pharmaceutical and Healthcare sector, alongside the burgeoning Cosmetics and Personal Care industries, are key end-users, demonstrating a strong commitment to adopting sustainable packaging to align with their brand values and consumer expectations.

Green Packaging Industry Company Market Share

Green Packaging Industry Market Composition & Trends

This comprehensive report delves into the intricate green packaging market, analyzing its current composition, key trends, and future trajectory. The study encompasses the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, building upon historical data from 2019–2024. Market concentration is evaluated, identifying dominant players and their market share distribution. Innovation catalysts, including advancements in sustainable packaging materials and eco-friendly packaging solutions, are meticulously examined. The report scrutinizes the evolving regulatory landscape for sustainable packaging, including mandates for reduced plastic usage and increased recyclability. Substitute products and their impact on market dynamics are also assessed, alongside detailed end-user profiles spanning Pharmaceutical and Healthcare, Cosmetics and Personal Care, and Food and Beverage sectors. Mergers and acquisitions (M&A) activities are analyzed, with an estimated M&A deal value of $35,000 Million, highlighting strategic consolidations within the biodegradable packaging market and reusable packaging market.

- Market Concentration: Assesses the influence of major eco-friendly packaging manufacturers.

- Innovation Catalysts: Explores advancements in recycled packaging, degradable packaging, and novel material science.

- Regulatory Landscapes: Covers evolving global policies promoting sustainable packaging solutions.

- Substitute Products: Analyzes the competitive impact of alternative eco-friendly packaging materials.

- End-User Profiles: Delineates demand drivers across key industries like food packaging sustainability and healthcare packaging solutions.

- M&A Activities: Identifies strategic consolidations and their impact on packaging market growth.

Green Packaging Industry Industry Evolution

The green packaging industry is undergoing a profound transformation, driven by a confluence of escalating environmental consciousness, stringent regulations, and innovative technological advancements. Over the study period of 2019–2033, the market has witnessed a remarkable surge in demand for sustainable packaging solutions. This evolution is characterized by significant market growth trajectories, projected to achieve a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033, with the green packaging market size expected to reach approximately $950,000 Million by 2033. Technological advancements have been pivotal, with breakthroughs in biodegradable packaging materials, such as compostable bioplastics derived from corn starch and sugarcane, and the development of advanced recycled packaging processes that enhance the quality and usability of post-consumer waste. Furthermore, the rise of the circular economy principles has spurred the adoption of reusable packaging systems, reducing waste generation and promoting resource efficiency. Shifting consumer demands are a critical factor, with an increasing preference for products packaged in eco-friendly materials. This is evident in the growing market share of paper packaging and metal packaging as alternatives to traditional plastics, particularly within the food and beverage packaging and cosmetics and personal care packaging sectors. The pharmaceutical and healthcare packaging segment is also increasingly adopting sustainable alternatives due to regulatory pressures and corporate social responsibility initiatives. Adoption metrics indicate a significant increase in the use of recyclable packaging and compostable packaging, with an estimated 65% of consumers now actively seeking out products with environmentally friendly packaging. The integration of smart technologies, such as QR codes for traceability and recycling guidance on packaging, further enhances the appeal and functionality of sustainable packaging. This continuous innovation and adaptation are reshaping the entire packaging industry, positioning green packaging as the future standard.

Leading Regions, Countries, or Segments in Green Packaging Industry

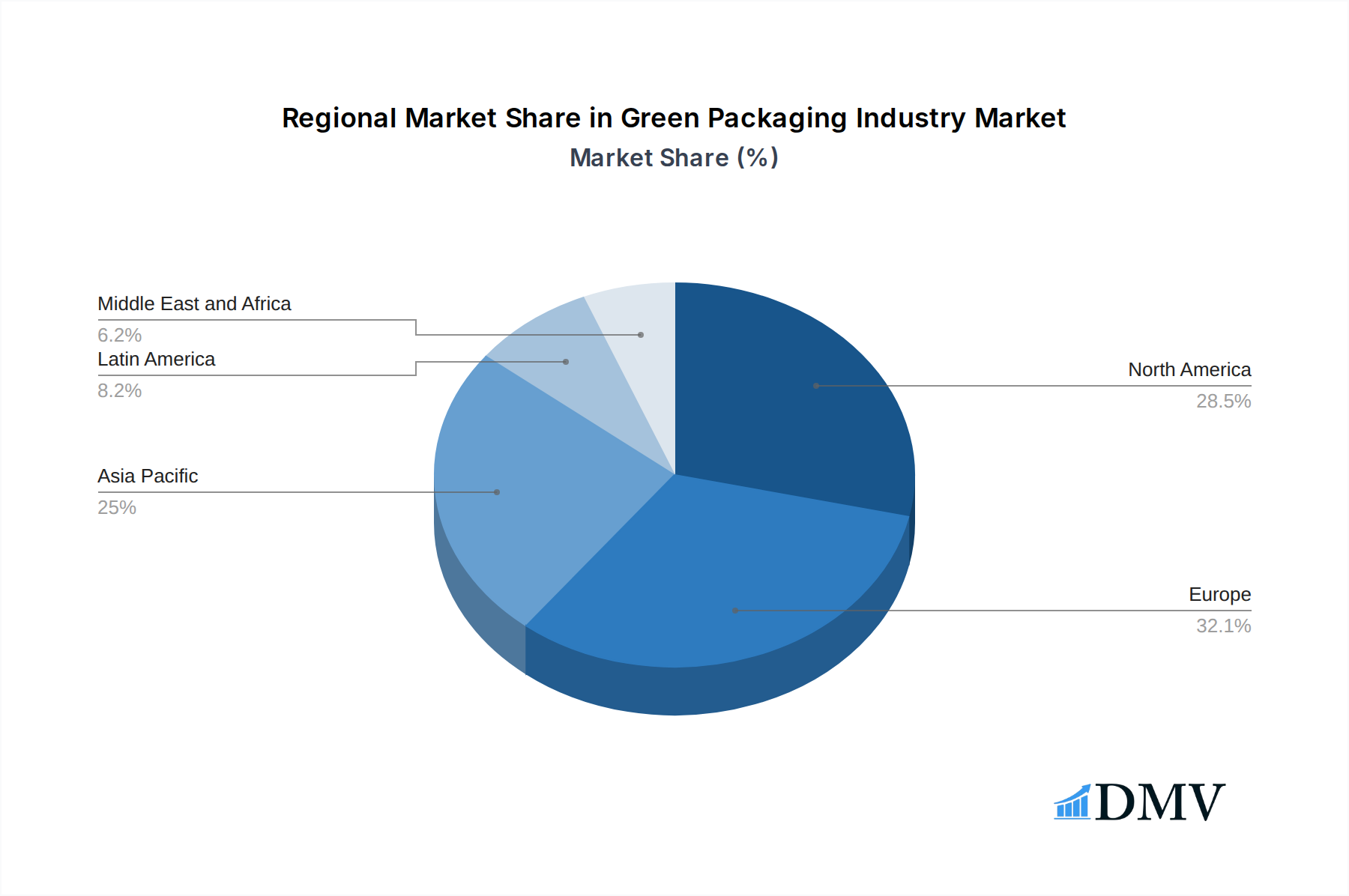

The green packaging industry exhibits distinct regional and segmental dominance, with key drivers influencing growth across various packaging segments. North America and Europe stand out as leading regions, propelled by robust regulatory frameworks, heightened consumer awareness regarding environmental sustainability, and significant investments in eco-friendly packaging solutions. Within North America, the United States spearheads the adoption of reusable packaging and degradable packaging, driven by corporate sustainability goals and consumer demand for plastic-free packaging. The food and beverage segment is a primary driver, with manufacturers actively seeking sustainable food packaging options to meet consumer expectations and comply with evolving regulations. In Europe, countries like Germany and the United Kingdom are at the forefront of recycled packaging innovation, supported by strong government initiatives promoting the circular economy and Extended Producer Responsibility (EPR) schemes. The cosmetics and personal care sector in these regions is witnessing a significant shift towards premium sustainable packaging, with brands leveraging glass packaging and paper packaging to enhance their eco-conscious image.

Key drivers for dominance include:

- Investment Trends: Substantial R&D investments in biodegradable packaging materials and recyclable packaging technologies.

- Regulatory Support: Stringent government policies mandating recycled content, single-use plastic reduction, and improved recyclability of packaging materials.

- Consumer Preferences: Growing consumer demand for environmentally friendly packaging across all end-user segments.

- Industry Initiatives: Proactive efforts by green packaging manufacturers to develop and market sustainable alternatives.

The recycled packaging segment, in particular, is experiencing exponential growth, fueled by the increasing availability of high-quality recycled feedstocks and advancements in recycling technologies that allow for a wider range of plastic and paper packaging to be effectively reprocessed. The food and beverage industry remains the largest end-user, with the demand for sustainable beverage packaging and eco-friendly food containers continually rising. The pharmaceutical and healthcare sector is also increasingly adopting sustainable alternatives, driven by regulatory compliance and a growing emphasis on corporate social responsibility. The plastic packaging segment, while still significant, is seeing a progressive shift towards bio-based and recycled plastics, alongside a greater emphasis on designing for recyclability and reuse. The paper packaging segment is experiencing a renaissance, driven by its inherent recyclability and the development of innovative coatings and barriers that enhance its performance for various applications, including food packaging.

Green Packaging Industry Product Innovations

The green packaging industry is a hotbed of innovation, with a constant stream of new products and applications designed to minimize environmental impact. Key advancements include the development of novel biodegradable packaging materials derived from agricultural waste and algae, offering compostable alternatives to conventional plastics. Innovations in recycled packaging technology are enhancing the purity and functionality of post-consumer recycled content, enabling its use in higher-value applications. For instance, the development of advanced barrier coatings for paper packaging is making it suitable for moisture-sensitive food products, previously reliant on multi-layer plastics. Reusable packaging systems are evolving with smart features, such as integrated tracking and return logistics, to improve efficiency and adoption rates. Performance metrics for these innovations often showcase reduced carbon footprints, lower material usage, and enhanced end-of-life recyclability or biodegradability.

Propelling Factors for Green Packaging Industry Growth

The green packaging industry is propelled by a robust interplay of technological, economic, and regulatory influences. Technological advancements in sustainable packaging materials, such as bioplastics and advanced recycled composites, are creating viable alternatives to traditional plastics. Economically, increasing consumer preference for eco-friendly packaging translates into market demand and premium pricing opportunities for sustainable products, estimated to drive market growth by an additional 5% annually. Regulatory mandates worldwide, including bans on single-use plastics and requirements for recycled content, are compelling manufacturers to adopt sustainable packaging solutions. For example, the EU's Packaging and Packaging Waste Directive significantly influences material choices and design for recyclability within the European packaging market.

Obstacles in the Green Packaging Industry Market

Despite its significant growth potential, the green packaging industry faces several obstacles. Regulatory complexities and variations across different regions can create challenges for global manufacturers. Supply chain disruptions, particularly in sourcing consistent and high-quality recycled packaging materials, can impact production volumes and costs. Furthermore, the initial cost of implementing sustainable packaging solutions can be higher than conventional alternatives, posing a barrier for smaller businesses. Competitive pressures from established plastic packaging suppliers and the need for extensive consumer education on proper disposal of biodegradable packaging also present challenges.

Future Opportunities in Green Packaging Industry

Emerging opportunities in the green packaging industry are vast and multifaceted. The expansion of compostable packaging into new food service applications and the development of innovative reusable packaging models for e-commerce present significant growth avenues. Advancements in chemical recycling are poised to unlock new possibilities for recycling traditionally difficult-to-recycle plastics, thereby boosting the supply of recycled plastic packaging. Furthermore, the growing demand for transparency and traceability in sustainable packaging opens doors for smart packaging solutions. The untapped potential in emerging economies, coupled with increasing environmental awareness, offers substantial market expansion opportunities for eco-friendly packaging.

Major Players in the Green Packaging Industry Ecosystem

- International Paper Company

- Sonoco Products Company

- Ball Corporation

- Westrock Company

- Ardagh Group SA

- TetraPak International SA

- Crown Holdings Inc

- BASF SE

- DS Smith PLC

- Mondi PLC

- Smurfit Kappa Group PLC

- Huhtamaki OYJ

- Amcor Limited

- Sealed Air Corporation

- Genpak LLC

Key Developments in Green Packaging Industry Industry

- July 2022: Mondi and converter Fiorini International collaborated to develop a new paper packaging option for Italian premium pasta product manufacturer Antico Pastificio Umbro. When applied to all pasta products, the new packaging, which is 100% recyclable, could reduce the amount of plastic used by up to 20 tonnes annually, impacting the sustainable food packaging market.

- April 2022: DS Smith introduced a corrugated cardboard box for the e-commerce shipment of medical devices. The corrugated cardboard box features a single-material solution instead of glued packaging with a single-use plastic insert, highlighting advancements in e-commerce packaging solutions and medical device packaging.

Strategic Green Packaging Industry Market Forecast

The strategic green packaging market forecast indicates robust and sustained growth, driven by escalating environmental regulations, a paradigm shift in consumer preferences towards sustainability, and continuous innovation in eco-friendly packaging materials and technologies. The market is projected to expand significantly, with an estimated market value of $950,000 Million by 2033. Key growth catalysts include the increasing adoption of reusable packaging systems, the development of advanced biodegradable packaging solutions, and the enhanced use of recycled packaging across diverse end-user industries such as Food and Beverage and Pharmaceuticals. This optimistic outlook is underpinned by substantial investments in research and development and a growing commitment from global corporations to achieve their sustainability targets, solidifying the dominance of green packaging as the future of the industry.

Green Packaging Industry Segmentation

-

1. Process

- 1.1. Reusable Packaging

- 1.2. Degradable Packaging

- 1.3. Recycled Packaging

-

2. Material Type

- 2.1. Glass

- 2.2. Plastic

- 2.3. Metal

- 2.4. Paper

-

3. End User

- 3.1. Pharmaceutical and Healthcare

- 3.2. Cosmetics and Personal Care

- 3.3. Food and Beverage

- 3.4. Other End Users

Green Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Green Packaging Industry Regional Market Share

Geographic Coverage of Green Packaging Industry

Green Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.67% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Process

- 5.1.1. Reusable Packaging

- 5.1.2. Degradable Packaging

- 5.1.3. Recycled Packaging

- 5.2. Market Analysis, Insights and Forecast - by Material Type

- 5.2.1. Glass

- 5.2.2. Plastic

- 5.2.3. Metal

- 5.2.4. Paper

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Pharmaceutical and Healthcare

- 5.3.2. Cosmetics and Personal Care

- 5.3.3. Food and Beverage

- 5.3.4. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Process

- 6. Global Green Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Process

- 6.1.1. Reusable Packaging

- 6.1.2. Degradable Packaging

- 6.1.3. Recycled Packaging

- 6.2. Market Analysis, Insights and Forecast - by Material Type

- 6.2.1. Glass

- 6.2.2. Plastic

- 6.2.3. Metal

- 6.2.4. Paper

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Pharmaceutical and Healthcare

- 6.3.2. Cosmetics and Personal Care

- 6.3.3. Food and Beverage

- 6.3.4. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Process

- 7. North America Green Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Process

- 7.1.1. Reusable Packaging

- 7.1.2. Degradable Packaging

- 7.1.3. Recycled Packaging

- 7.2. Market Analysis, Insights and Forecast - by Material Type

- 7.2.1. Glass

- 7.2.2. Plastic

- 7.2.3. Metal

- 7.2.4. Paper

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Pharmaceutical and Healthcare

- 7.3.2. Cosmetics and Personal Care

- 7.3.3. Food and Beverage

- 7.3.4. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Process

- 8. Europe Green Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Process

- 8.1.1. Reusable Packaging

- 8.1.2. Degradable Packaging

- 8.1.3. Recycled Packaging

- 8.2. Market Analysis, Insights and Forecast - by Material Type

- 8.2.1. Glass

- 8.2.2. Plastic

- 8.2.3. Metal

- 8.2.4. Paper

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Pharmaceutical and Healthcare

- 8.3.2. Cosmetics and Personal Care

- 8.3.3. Food and Beverage

- 8.3.4. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Process

- 9. Asia Pacific Green Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Process

- 9.1.1. Reusable Packaging

- 9.1.2. Degradable Packaging

- 9.1.3. Recycled Packaging

- 9.2. Market Analysis, Insights and Forecast - by Material Type

- 9.2.1. Glass

- 9.2.2. Plastic

- 9.2.3. Metal

- 9.2.4. Paper

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Pharmaceutical and Healthcare

- 9.3.2. Cosmetics and Personal Care

- 9.3.3. Food and Beverage

- 9.3.4. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Process

- 10. Latin America Green Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Process

- 10.1.1. Reusable Packaging

- 10.1.2. Degradable Packaging

- 10.1.3. Recycled Packaging

- 10.2. Market Analysis, Insights and Forecast - by Material Type

- 10.2.1. Glass

- 10.2.2. Plastic

- 10.2.3. Metal

- 10.2.4. Paper

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Pharmaceutical and Healthcare

- 10.3.2. Cosmetics and Personal Care

- 10.3.3. Food and Beverage

- 10.3.4. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Process

- 11. Middle East and Africa Green Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Process

- 11.1.1. Reusable Packaging

- 11.1.2. Degradable Packaging

- 11.1.3. Recycled Packaging

- 11.2. Market Analysis, Insights and Forecast - by Material Type

- 11.2.1. Glass

- 11.2.2. Plastic

- 11.2.3. Metal

- 11.2.4. Paper

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Pharmaceutical and Healthcare

- 11.3.2. Cosmetics and Personal Care

- 11.3.3. Food and Beverage

- 11.3.4. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Process

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 International Paper Company*List Not Exhaustive

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sonoco Products Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ball Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Westrock Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ardagh Group SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TetraPak International SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Crown Holdings Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 BASF SE

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DS Smith PLC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mondi PLC

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Smurfit Kappa Group PLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Huhtamaki OYJ

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Amcor Limited

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Sealed Air Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Genpak LLC

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 International Paper Company*List Not Exhaustive

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Green Packaging Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Green Packaging Industry Revenue (Million), by Process 2025 & 2033

- Figure 3: North America Green Packaging Industry Revenue Share (%), by Process 2025 & 2033

- Figure 4: North America Green Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 5: North America Green Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 6: North America Green Packaging Industry Revenue (Million), by End User 2025 & 2033

- Figure 7: North America Green Packaging Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America Green Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Green Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Green Packaging Industry Revenue (Million), by Process 2025 & 2033

- Figure 11: Europe Green Packaging Industry Revenue Share (%), by Process 2025 & 2033

- Figure 12: Europe Green Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 13: Europe Green Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 14: Europe Green Packaging Industry Revenue (Million), by End User 2025 & 2033

- Figure 15: Europe Green Packaging Industry Revenue Share (%), by End User 2025 & 2033

- Figure 16: Europe Green Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Green Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Green Packaging Industry Revenue (Million), by Process 2025 & 2033

- Figure 19: Asia Pacific Green Packaging Industry Revenue Share (%), by Process 2025 & 2033

- Figure 20: Asia Pacific Green Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 21: Asia Pacific Green Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 22: Asia Pacific Green Packaging Industry Revenue (Million), by End User 2025 & 2033

- Figure 23: Asia Pacific Green Packaging Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Asia Pacific Green Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Green Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Green Packaging Industry Revenue (Million), by Process 2025 & 2033

- Figure 27: Latin America Green Packaging Industry Revenue Share (%), by Process 2025 & 2033

- Figure 28: Latin America Green Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 29: Latin America Green Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 30: Latin America Green Packaging Industry Revenue (Million), by End User 2025 & 2033

- Figure 31: Latin America Green Packaging Industry Revenue Share (%), by End User 2025 & 2033

- Figure 32: Latin America Green Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Green Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Green Packaging Industry Revenue (Million), by Process 2025 & 2033

- Figure 35: Middle East and Africa Green Packaging Industry Revenue Share (%), by Process 2025 & 2033

- Figure 36: Middle East and Africa Green Packaging Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 37: Middle East and Africa Green Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 38: Middle East and Africa Green Packaging Industry Revenue (Million), by End User 2025 & 2033

- Figure 39: Middle East and Africa Green Packaging Industry Revenue Share (%), by End User 2025 & 2033

- Figure 40: Middle East and Africa Green Packaging Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Green Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 2: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 3: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Global Green Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 6: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 7: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 8: Global Green Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 10: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 11: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 12: Global Green Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 14: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 15: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 16: Global Green Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 18: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 19: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 20: Global Green Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Green Packaging Industry Revenue Million Forecast, by Process 2020 & 2033

- Table 22: Global Green Packaging Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 23: Global Green Packaging Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 24: Global Green Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Green Packaging Industry?

The projected CAGR is approximately 7.67%.

2. Which companies are prominent players in the Green Packaging Industry?

Key companies in the market include International Paper Company*List Not Exhaustive, Sonoco Products Company, Ball Corporation, Westrock Company, Ardagh Group SA, TetraPak International SA, Crown Holdings Inc, BASF SE, DS Smith PLC, Mondi PLC, Smurfit Kappa Group PLC, Huhtamaki OYJ, Amcor Limited, Sealed Air Corporation, Genpak LLC.

3. What are the main segments of the Green Packaging Industry?

The market segments include Process, Material Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 292.71 Million as of 2022.

5. What are some drivers contributing to market growth?

Government Initiatives toward Sustainable Packaging; Downsizing of Packaging; Shift in Consumer Preferences toward Recyclable and Eco-friendly Materials.

6. What are the notable trends driving market growth?

Sustainable Plastic Packaging Solutions to Hold Major Share in Market.

7. Are there any restraints impacting market growth?

Capacity Constraint of Manufacturing Plants; High Cost of Raw Materials.

8. Can you provide examples of recent developments in the market?

July 2022: Mondi and converter FioriniInternational collaborated to develop a new paper packaging option for Italian premium pasta product manufacturer Antico PastificioUmbro. When applied to all pasta products, the new packaging, which is 100% recyclable, could reduce the amount of plastic used by up to 20 tonnes annually.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Green Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Green Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Green Packaging Industry?

To stay informed about further developments, trends, and reports in the Green Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence