Key Insights

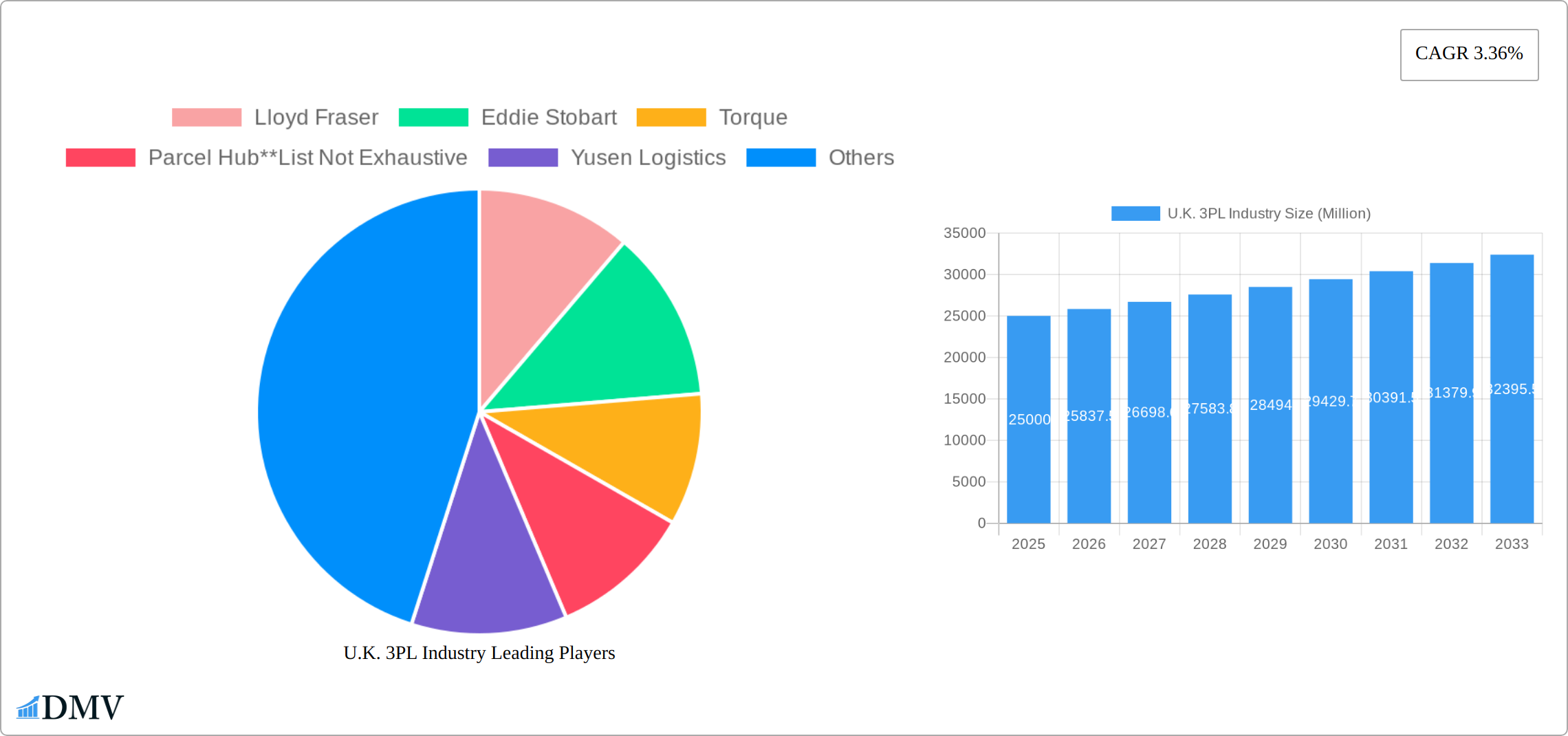

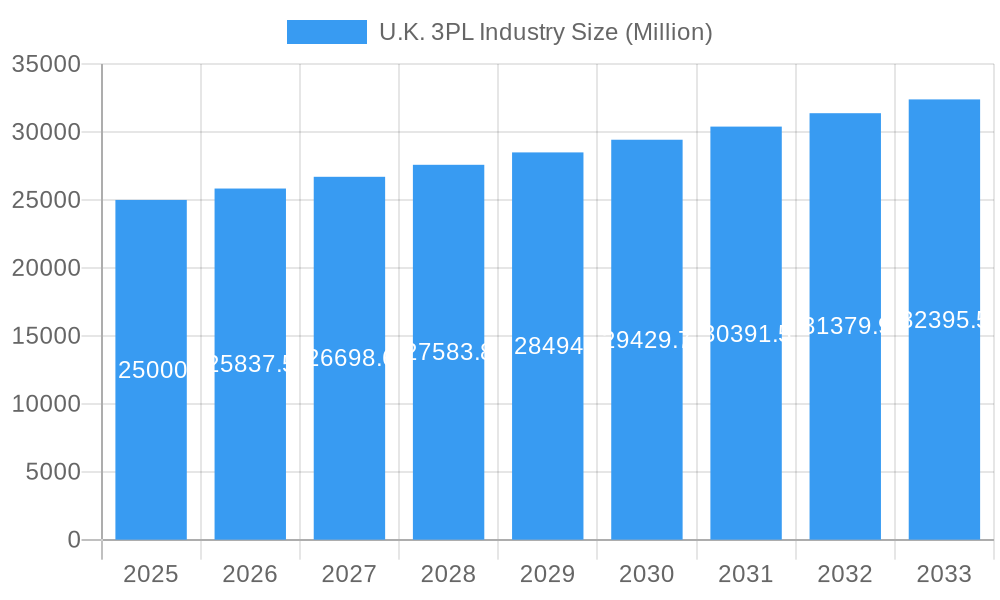

The United Kingdom's Third-Party Logistics (3PL) market, valued at approximately 21.2 billion in 2025, is projected for robust growth with a Compound Annual Growth Rate (CAGR) of 3.36% from 2025 to 2033. Key growth drivers include the sustained expansion of e-commerce, significantly increasing demand for warehousing and distribution, particularly within the distributive trade. Furthermore, sectors such as manufacturing, automotive, pharmaceuticals, and healthcare are increasingly leveraging specialized 3PL expertise for enhanced efficiency and cost reduction. The complexity of supply chains in oil & gas and chemicals also fuels outsourcing. Technological advancements in Warehouse Management Systems (WMS) and Transportation Management Systems (TMS) are crucial for improving operational efficiency and visibility. However, challenges like driver shortages, escalating fuel costs, and Brexit-related complexities present restraints. Intense competition among established global players and prominent UK-based firms necessitates a focus on value-added services and specialization. The market segmentation by services (transportation, warehousing & distribution) and end-users offers strategic opportunities for targeted growth.

U.K. 3PL Industry Market Size (In Billion)

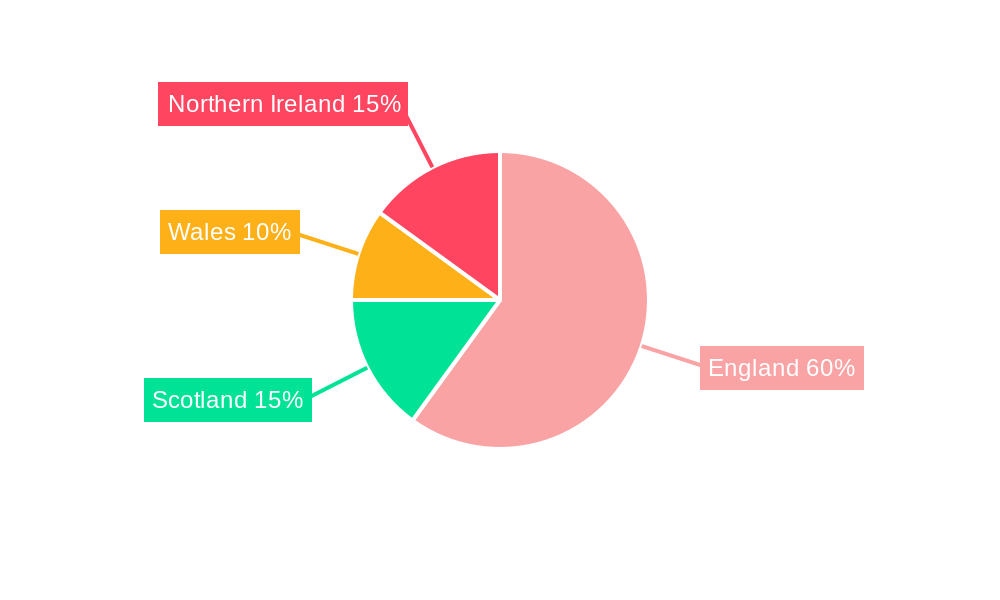

The UK's geographical landscape presents unique opportunities and challenges for 3PL providers. Serving diverse end-users across England, Wales, Scotland, and Northern Ireland requires extensive logistics networks, fostering regional specialization and the emergence of smaller, localized providers. The forecast period (2025-2033) anticipates continued market consolidation through acquisitions aimed at expanding service portfolios and geographic reach. Technological innovation, including AI and automation in warehousing and transportation, will be pivotal in addressing rising labor costs and operational constraints. A growing emphasis on sustainable and environmentally responsible logistics solutions will also shape the future trajectory of the UK 3PL market.

U.K. 3PL Industry Company Market Share

U.K. 3PL Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the U.K. 3PL (Third-Party Logistics) industry, offering invaluable insights for stakeholders across the supply chain. Covering the period from 2019 to 2033, with a base year of 2025, this report forecasts market trends, identifies key players, and explores future opportunities within this dynamic sector. The report incorporates data-driven analysis, examining market segmentation, innovation, and regulatory changes to present a holistic view of the U.K. 3PL landscape. Expect detailed breakdowns of market share, M&A activity, and growth projections, allowing you to make informed strategic decisions.

U.K. 3PL Industry Market Composition & Trends

The UK 3PL market exhibits a moderately concentrated structure, with several major players commanding significant market share. Prominent companies such as Lloyd Fraser, Eddie Stobart, Torque, Parcel Hub, Yusen Logistics, Wincanton, XPO Logistics, FedEx, CEVA Logistics, Tarlu Ltd, Kuehne + Nagel, Bibby Distribution, United Parcel Service of America, Xpediator, Schenker Limited, Pointbid Logistics Systems Ltd, DHL Supply Chain, and Rhenus Logistics are key competitors vying for market dominance. Industry analysis suggests that the top five companies will hold approximately [Insert Percentage]% of the market in 2025, with the remaining [Insert Percentage]% dispersed among numerous smaller firms. This competitive landscape is further shaped by ongoing consolidation and strategic acquisitions.

- Market Concentration: A moderately concentrated market with a few dominant players and a large number of smaller businesses. This dynamic creates both opportunities for growth and intense competition.

- Innovation Drivers: Explosive e-commerce growth, rapid technological advancements (including automation, AI, and robotics), and the escalating demand for specialized logistics solutions are key drivers of market evolution and innovation.

- Regulatory Environment: The UK 3PL industry operates within a stringent regulatory framework encompassing data privacy (GDPR), environmental sustainability (e.g., carbon emissions targets), and transportation compliance. Adherence to these regulations is crucial for operational viability and maintaining a strong reputation.

- Substitute Services: While limited direct substitutes exist due to the specialized nature of 3PL services, smaller businesses may opt for in-house logistics functions as a partial alternative. However, the scalability and cost-effectiveness of 3PL solutions typically outweigh in-house options for larger enterprises.

- Client Base: The UK 3PL industry serves a diverse range of sectors, including manufacturing, automotive, oil & gas, distributive trade (with significant e-commerce representation), pharmaceuticals, healthcare, and construction. This broad client base contributes to market resilience and provides opportunities for diversification.

- Mergers & Acquisitions (M&A): The UK 3PL market is witnessing significant M&A activity. A prime example is Kuehne+Nagel's acquisition of Morgan Cargo in 2023, valued at an estimated £[Insert Value] Million, reflecting the ongoing consolidation trend. The cumulative value of M&A deals between 2019 and 2024 reached an estimated £[Insert Value] Million, indicating substantial investment and market restructuring.

U.K. 3PL Industry Industry Evolution

The U.K. 3PL market has experienced consistent growth throughout the historical period (2019-2024), driven by the expansion of e-commerce, increasing globalization, and the rising demand for efficient and cost-effective supply chain solutions. The market is expected to continue this trajectory, with a Compound Annual Growth Rate (CAGR) of xx% projected from 2025 to 2033, reaching a market value of £xx Million by 2033. Technological advancements, such as the adoption of warehouse management systems (WMS), transportation management systems (TMS), and robotic process automation (RPA) are significantly improving efficiency and optimizing operations within the 3PL sector. Furthermore, the growing emphasis on sustainability and supply chain resilience is pushing the industry towards innovative solutions like green logistics and blockchain technology. Changing consumer expectations, including faster delivery times and increased transparency, are also pushing 3PL providers to adapt and innovate. The adoption rate of advanced technologies, like AI-powered route optimization, is projected to reach xx% by 2033.

Leading Regions, Countries, or Segments in U.K. 3PL Industry

The U.K. 3PL market is geographically diverse, with significant activity across various regions. However, the South East of England, due to its proximity to major ports and airports and high concentration of businesses, is likely the leading region. In terms of segments, Distributive Trade (Wholesale and Retail Trade including E-commerce) represents the largest segment, driven by the booming online retail market.

By Service:

- Domestic Transportation Management: This segment is experiencing strong growth driven by increasing domestic e-commerce deliveries and intra-UK movement of goods.

- International Transportation Management: International trade dynamics and global supply chain complexities contribute to the growth of this segment.

- Value-added Warehousing and Distribution: Demand for specialized services like contract packaging, kitting, and inventory management fuels growth in this segment.

By End-User:

- Distributive Trade (Wholesale and Retail Trade Including E-commerce): This is the largest and fastest-growing segment, owing to the surge in e-commerce and the need for efficient last-mile delivery.

- Manufacturing and Automotive: The manufacturing and automotive sectors represent significant clients for 3PL providers due to their complex supply chains.

- Pharmaceuticals and Healthcare: This sector’s demand for temperature-controlled logistics and specialized handling drives segment growth.

Key Drivers:

- High investment in infrastructure: Significant investments are being made in warehousing and transportation infrastructure to support growing demand.

- Government initiatives: Government regulations and incentives promoting logistics efficiency and sustainability are driving industry growth.

- Technological advancements: The adoption of new technologies enhances operational efficiency and provides competitive advantages.

U.K. 3PL Industry Product Innovations

The U.K. 3PL industry is witnessing continuous product innovation, focusing on improving efficiency, transparency, and sustainability. New technologies like AI-powered route optimization, blockchain for enhanced supply chain visibility, and automated warehousing solutions are becoming increasingly prevalent. These innovations are leading to improved delivery times, reduced costs, and enhanced customer satisfaction. Unique selling propositions now include customized solutions, advanced data analytics, and proactive risk management.

Propelling Factors for U.K. 3PL Industry Growth

The U.K. 3PL industry's growth is fueled by several key factors. The rise of e-commerce significantly increases demand for efficient last-mile delivery and warehousing solutions. Technological advancements, such as automation and AI, enhance operational efficiency and reduce costs. Government initiatives promoting sustainable logistics practices and infrastructure development further support industry expansion. Favorable economic conditions and increased cross-border trade contribute to the overall market growth.

Obstacles in the U.K. 3PL Industry Market

The U.K. 3PL industry faces several challenges. Driver shortages and fluctuating fuel prices impact transportation costs and operational efficiency. Stringent environmental regulations necessitate investments in sustainable logistics practices, which can be costly. Increased competition from both established players and new entrants puts pressure on profit margins. Supply chain disruptions caused by global events, such as pandemics or geopolitical instability, continue to pose significant risks.

Future Opportunities in U.K. 3PL Industry

The U.K. 3PL industry presents significant future opportunities. The expanding e-commerce market necessitates optimized last-mile delivery solutions. The increasing adoption of advanced technologies like AI and blockchain will improve efficiency and transparency. The focus on sustainability will drive demand for environmentally friendly logistics solutions. Expansion into niche markets, such as cold chain logistics or specialized healthcare delivery, presents attractive growth prospects.

Major Players in the U.K. 3PL Industry Ecosystem

- Lloyd Fraser

- Eddie Stobart

- Torque

- Parcel Hub

- Yusen Logistics

- Wincanton

- XPO Logistics

- FedEx

- CEVA Logistics

- Tarlu Ltd

- Kuehne + Nagel

- Bibby Distribution

- United Parcel Service of America

- Xpediator

- Schenker Limited

- Pointbid Logistics Systems Ltd

- DHL Supply Chain

- Rhenus Logistics

Key Developments in U.K. 3PL Industry Industry

- June 2023: Kuehne+Nagel's acquisition of Morgan Cargo strengthens its position in the perishable goods market. This expands their capabilities and increases their global footprint, with an estimated £xx Million investment.

- February 2023: Wincanton's new contract with Wickes underscores the growing demand for comprehensive supply chain solutions in the home improvement sector. This significant contract secures Wincanton's market position and highlights the importance of strong partnerships.

Strategic U.K. 3PL Industry Market Forecast

The U.K. 3PL market is poised for continued growth, driven by e-commerce expansion, technological advancements, and increasing demand for efficient and sustainable supply chain solutions. The projected CAGR of xx% indicates significant market potential. The focus on innovation, strategic partnerships, and adapting to evolving customer demands will be crucial for success in this dynamic market. The market's value is projected to exceed £xx Million by 2033, creating lucrative opportunities for both established players and new entrants.

U.K. 3PL Industry Segmentation

-

1. Services

- 1.1. Domestic Transportation Management

- 1.2. International Transportation Management

- 1.3. Value-added Warehousing and Distribution

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Oil & Gas and Chemicals

- 2.3. Distribu

- 2.4. Pharmaceuticals and Healthcare

- 2.5. Construction

- 2.6. Other End Users

U.K. 3PL Industry Segmentation By Geography

- 1. U.K.

U.K. 3PL Industry Regional Market Share

Geographic Coverage of U.K. 3PL Industry

U.K. 3PL Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Domestic Transportation Management

- 5.1.2. International Transportation Management

- 5.1.3. Value-added Warehousing and Distribution

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Oil & Gas and Chemicals

- 5.2.3. Distribu

- 5.2.4. Pharmaceuticals and Healthcare

- 5.2.5. Construction

- 5.2.6. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. U.K.

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. U.K. 3PL Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Domestic Transportation Management

- 6.1.2. International Transportation Management

- 6.1.3. Value-added Warehousing and Distribution

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Oil & Gas and Chemicals

- 6.2.3. Distribu

- 6.2.4. Pharmaceuticals and Healthcare

- 6.2.5. Construction

- 6.2.6. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Lloyd Fraser

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Eddie Stobart

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Torque

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Parcel Hub**List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Yusen Logistics

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Wincanton

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 XPO Logistics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 FedEx

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 CEVA Logistics

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tarlu Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Kuehne Nagel

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Bibby Distribution

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 United Parcel Service of America

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Xpediator

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Schenker Limited

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Pointbid Logistics Systems Ltd

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 DHL Supply Chain

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Rhenus Logistics

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.1 Lloyd Fraser

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.K. 3PL Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: U.K. 3PL Industry Share (%) by Company 2025

List of Tables

- Table 1: U.K. 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 2: U.K. 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: U.K. 3PL Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: U.K. 3PL Industry Revenue billion Forecast, by Services 2020 & 2033

- Table 5: U.K. 3PL Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: U.K. 3PL Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.K. 3PL Industry?

The projected CAGR is approximately 0.3%.

2. Which companies are prominent players in the U.K. 3PL Industry?

Key companies in the market include Lloyd Fraser, Eddie Stobart, Torque, Parcel Hub**List Not Exhaustive, Yusen Logistics, Wincanton, XPO Logistics, FedEx, CEVA Logistics, Tarlu Ltd, Kuehne Nagel, Bibby Distribution, United Parcel Service of America, Xpediator, Schenker Limited, Pointbid Logistics Systems Ltd, DHL Supply Chain, Rhenus Logistics.

3. What are the main segments of the U.K. 3PL Industry?

The market segments include Services, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.2 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Government Initiatives4.; Increase of Trade.

6. What are the notable trends driving market growth?

Growth in Logistics Parks and Fulfilment Centers.

7. Are there any restraints impacting market growth?

4.; Shortage of Labor.

8. Can you provide examples of recent developments in the market?

June 2023: Kuehne+Nagel signed an agreement to acquire Morgan Cargo, a leading South African, UK and Kenyan freight forwarder specialised in the transport and handling of perishable goods. During 2022 the company handled more than 40,000 tonnes of air freight and more than 20,000 TEU of sea freight globally, managed by approximately 450 logistics experts.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.K. 3PL Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.K. 3PL Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.K. 3PL Industry?

To stay informed about further developments, trends, and reports in the U.K. 3PL Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence