Key Insights

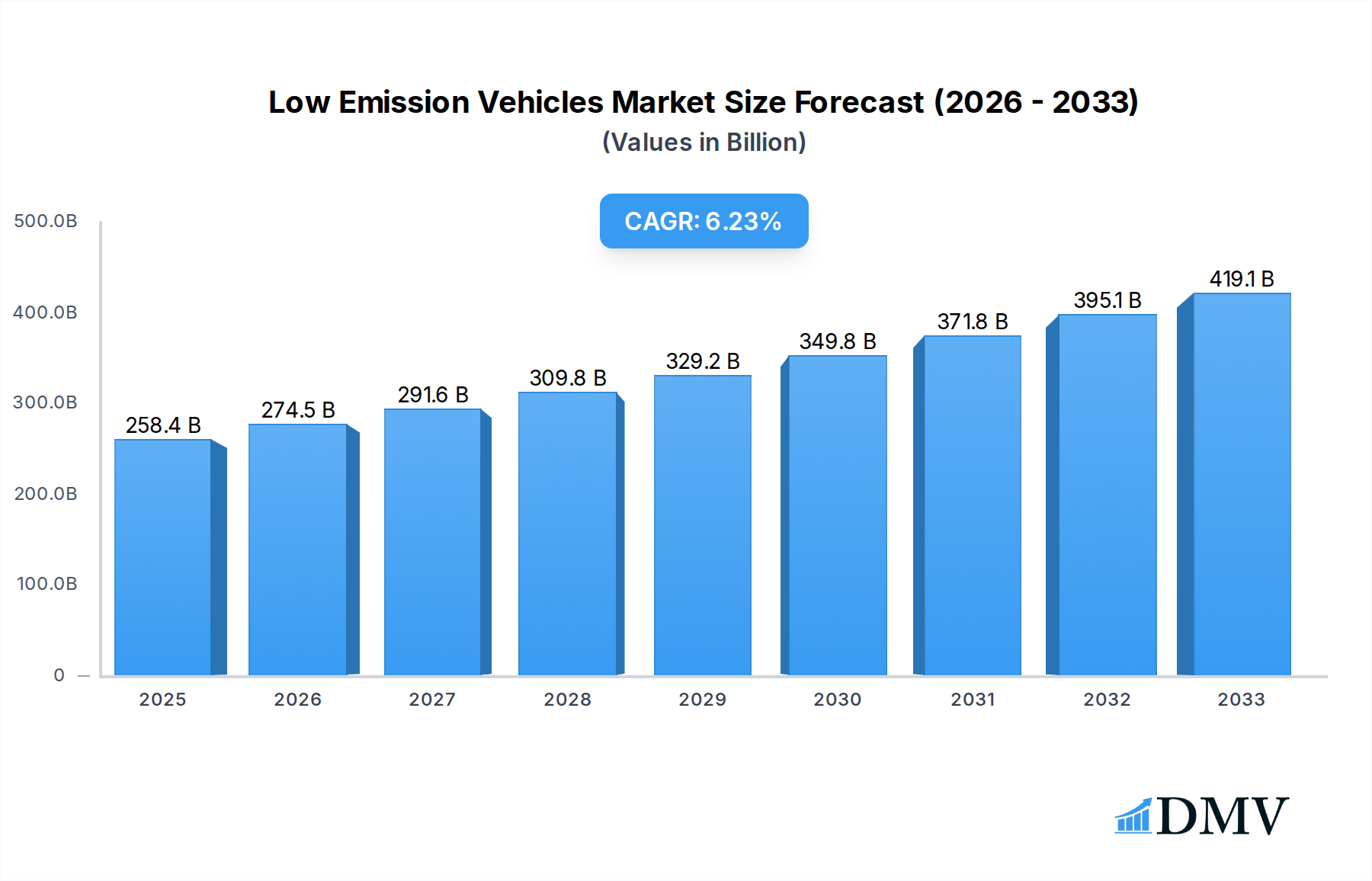

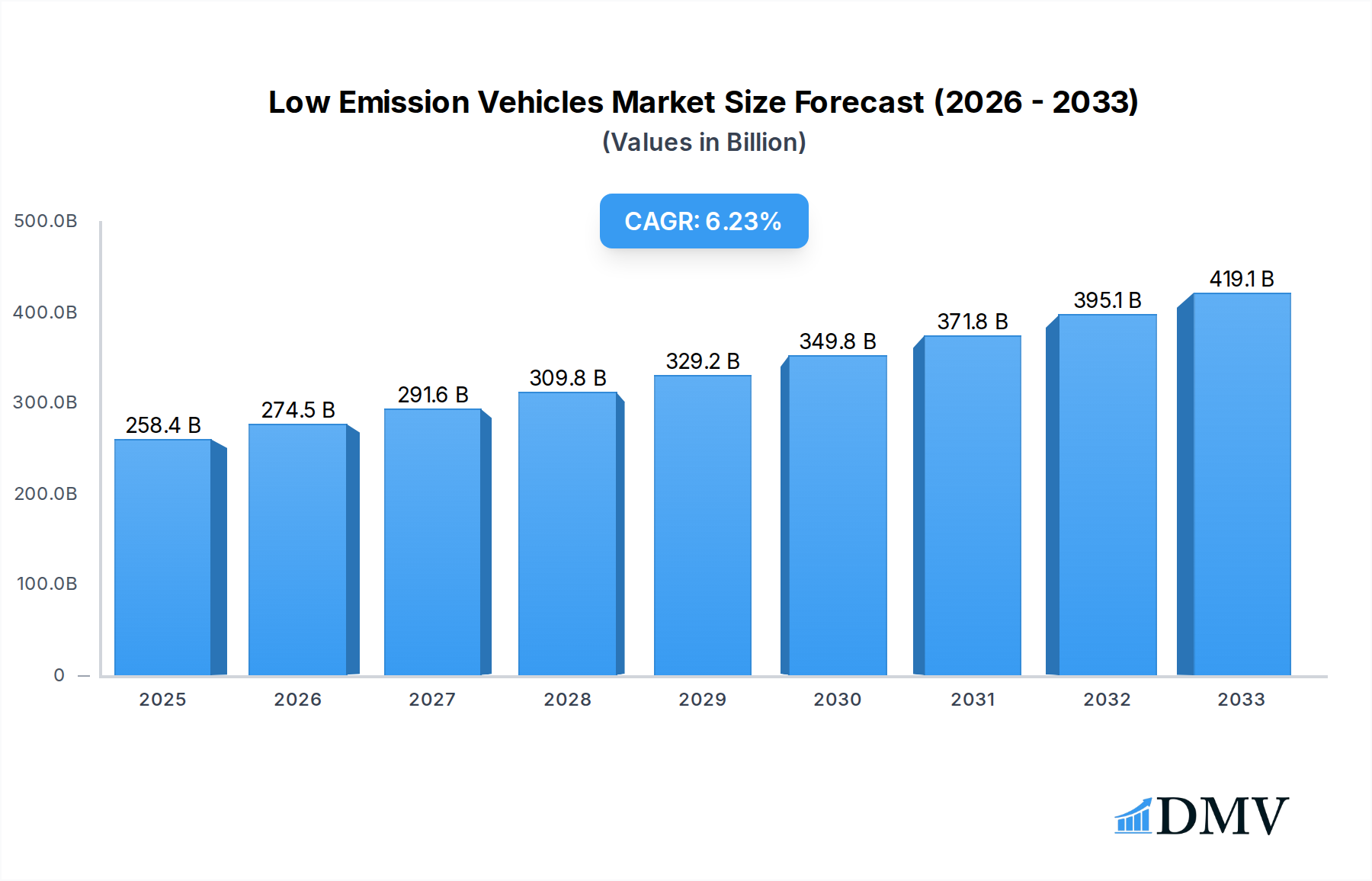

The global Low Emission Vehicles market is poised for significant expansion, driven by a confluence of stringent environmental regulations, growing consumer awareness regarding climate change, and advancements in electric vehicle (EV) technology. With a market size of approximately $258.36 billion in 2025, the sector is projected to experience robust growth, indicated by a Compound Annual Growth Rate (CAGR) of 6.31%. This growth trajectory is primarily fueled by substantial investments in charging infrastructure, coupled with declining battery costs that are making electric and hybrid vehicles more accessible and appealing to a broader consumer base. Key applications include passenger cars, which represent the largest segment due to increasing demand for sustainable personal mobility, and commercial vehicles, where fleet operators are motivated by long-term operational cost savings and corporate social responsibility initiatives. The ongoing shift towards decarbonization across the automotive industry underscores the pivotal role low emission vehicles will play in shaping future transportation.

Low Emission Vehicles Market Size (In Billion)

Emerging trends within the low emission vehicle landscape include the rapid evolution of battery technology, leading to enhanced range and faster charging times, and the increasing integration of smart features and autonomous driving capabilities. Pure electric vehicles (PEVs) are at the forefront of this transformation, capturing significant market share, while hybrid electric vehicles (HEVs) continue to offer a viable transitional solution for consumers and fleet managers. However, challenges such as the initial higher purchase price compared to traditional internal combustion engine (ICE) vehicles and the need for widespread charging infrastructure development, particularly in developing regions, remain significant restraints. Despite these hurdles, the overwhelming global commitment to reducing carbon footprints and achieving net-zero emissions ensures a dynamic and upward growth path for the low emission vehicles market in the coming years, with major automotive players like Toyota, Volkswagen, and BYD leading the charge in innovation and production.

Low Emission Vehicles Company Market Share

Low Emission Vehicles Market Composition & Trends

The global Low Emission Vehicles (LEV) market is a dynamic and rapidly evolving landscape, characterized by increasing market concentration among a few key players while simultaneously fostering a competitive environment driven by innovation. This report offers a comprehensive analysis of the LEV market composition, examining its intricate trends and future trajectory. With a study period spanning 2019–2033, a base year of 2025, and a forecast period of 2025–2033, this analysis delves deep into market share distribution, technological advancements, and the crucial role of regulatory frameworks in shaping market dynamics. We evaluate the impact of substitute products, profile end-user segments, and scrutinize Mergers & Acquisitions (M&A) activities, which have seen significant deal values in the billions, driving consolidation and fostering synergistic growth. The LEV sector is at the forefront of the global shift towards sustainable transportation, with substantial investments pouring into research and development to create cleaner, more efficient mobility solutions. Understanding the interplay of these factors is paramount for stakeholders seeking to navigate and capitalize on this burgeoning market.

- Market Share Distribution: Witnessing a gradual shift with established automotive giants and new entrants vying for dominance in the passenger cars and commercial vehicles segments.

- Innovation Catalysts: Driven by advancements in battery technology, charging infrastructure, and powertrain efficiency for pure electric vehicles (PEVs) and hybrid electric vehicles (HEVs).

- Regulatory Landscapes: Stringent emission standards and government incentives worldwide are pivotal in accelerating LEV adoption rates.

- Substitute Products: The competition between traditional internal combustion engine (ICE) vehicles and LEVs continues, with LEVs gaining significant traction.

- End-User Profiles: A diverse range of consumers and businesses are embracing LEVs due to cost savings, environmental consciousness, and performance benefits.

- M&A Activities: Billions in M&A deals indicate strategic consolidations, partnerships, and acquisitions aimed at securing market position and technological expertise.

- Market Concentration: While the market is growing, a notable concentration exists among leading manufacturers like Tesla Motor Company, BYD, and major legacy automakers.

- Intellectual Property: Billions invested in patents related to battery technology, electric drivetrains, and autonomous driving features for LEVs.

- Market Value: Projected to reach trillions by the end of the forecast period, underscoring the immense economic potential.

- Investment Trends: Billions are being channeled into R&D and manufacturing expansions for electric and hybrid vehicle platforms.

Low Emission Vehicles Industry Evolution

The Low Emission Vehicles (LEV) industry has undergone a remarkable transformation, marked by exponential growth trajectories and profound technological advancements that are reshaping global transportation paradigms. From its nascent stages, the industry has consistently pushed the boundaries of innovation, driven by an unwavering commitment to environmental sustainability and evolving consumer demands. The historical period from 2019 to 2024 witnessed a surge in the development and adoption of cleaner vehicle technologies, laying a robust foundation for the accelerated growth observed in the estimated year of 2025. As we progress through the forecast period of 2025–2033, the LEV market is poised for unprecedented expansion, fueled by a confluence of factors including increasingly stringent emissions regulations, substantial government incentives, and a growing consumer awareness regarding the environmental impact of conventional vehicles.

Technological breakthroughs have been instrumental in this evolution. Advancements in battery energy density and charging speeds have significantly mitigated range anxiety, a major barrier to early adoption. Pure Electric Vehicles (PEVs), once considered niche, are now mainstream, offering competitive performance and lower running costs. Hybrid Electric Vehicles (HEVs) continue to play a crucial role, providing a transitional solution for consumers not yet ready for full electrification. The development of advanced powertrain systems, lightweight materials, and sophisticated energy management software has further enhanced the efficiency and performance of LEVs.

Consumer preferences have also shifted dramatically. A growing segment of the population prioritizes environmental responsibility and is actively seeking sustainable transportation options. This shift, coupled with the decreasing total cost of ownership for LEVs due to lower fuel and maintenance expenses, is creating a powerful demand pull. The passenger car segment has been the primary driver of this growth, but we are witnessing a significant uptick in the adoption of LEVs within the commercial vehicle sector, driven by fleet operators seeking to reduce operational costs and meet corporate sustainability goals.

Major automotive manufacturers, including Tesla Motor Company, Toyota, BYD, Ford Motor Company, General Motors Ltd, Honda Motors Ltd, Hyundai Motors, BMW, Daimler, Mitsubishi Motor Corporation, and Isuzu Motors, are investing billions in research and development and retooling their manufacturing facilities to meet this burgeoning demand. This aggressive investment signals a clear industry-wide pivot towards electrification. The evolution of the LEV industry is not merely about replacing traditional vehicles; it's about a fundamental redefinition of mobility, focusing on sustainability, efficiency, and an improved environmental footprint for generations to come. The market is projected to witness a compound annual growth rate (CAGR) exceeding 20% during the forecast period, with market revenues reaching trillions by 2033. Adoption rates for PEVs are expected to surpass 50% in key markets by the end of the forecast period.

Leading Regions, Countries, or Segments in Low Emission Vehicles

The Low Emission Vehicles (LEV) market is witnessing a pronounced dominance by Pure Electric Vehicles (PEVs) within the Application: Passenger Cars segment, particularly in leading regions and countries that have proactively embraced sustainable transportation policies and technological innovation. This segment's ascendance is driven by a powerful synergy of regulatory support, robust investment trends, and rapidly evolving consumer preferences.

Key Drivers of PEV Dominance in Passenger Cars:

- Aggressive Government Incentives and Subsidies: Countries and regions like China, Europe (particularly Norway, Germany, and France), and several states in the USA have implemented substantial purchase subsidies, tax credits, and exemptions for PEVs. These financial incentives directly reduce the upfront cost, making PEVs more accessible to a wider consumer base, thus driving significant adoption rates. Billions have been allocated globally to support these programs.

- Stringent Emission Regulations: Increasingly stringent CO2 emission standards and outright bans on the sale of new internal combustion engine (ICE) vehicles in future years are compelling automakers to accelerate their PEV production and portfolio expansion. This regulatory pressure acts as a powerful catalyst for market growth.

- Rapidly Expanding Charging Infrastructure: Significant investments, running into billions, have been made in developing public and private charging networks. The increasing availability and speed of charging stations are crucial in alleviating range anxiety and making PEV ownership more practical for daily use, especially for passenger cars.

- Technological Advancements and Product Diversification: Leading manufacturers such as Tesla Motor Company, BYD, and legacy automakers like Ford Motor Company, Hyundai Motors, and BMW are introducing an ever-wider array of PEV models in the passenger car segment. These range from affordable compact cars to premium SUVs and sedans, offering consumers a variety of choices that cater to different needs and budgets. Innovations in battery technology leading to increased range and faster charging have been pivotal.

- Growing Consumer Environmental Awareness and Demand: A significant segment of the consumer market, particularly in urban areas, is increasingly conscious of environmental issues and seeks sustainable mobility solutions. The lower running costs, quieter operation, and the perception of advanced technology associated with PEVs are also strong attractors.

- Favorable Total Cost of Ownership (TCO): Despite potentially higher initial purchase prices, the lower electricity costs compared to gasoline and reduced maintenance requirements often result in a lower TCO for PEVs over their lifecycle, making them an economically attractive option for passenger car owners.

- Investment in R&D and Manufacturing: Billions have been invested by companies like Toyota, Honda Motors Ltd, General Motors Ltd, Mitsubishi Motor Corporation, and Daimler in developing dedicated PEV platforms and scaling up production capacities, ensuring a steady supply of competitive models.

While Hybrid Electric Vehicles (HEVs) and Commercial Vehicles are also experiencing growth, the sheer volume of sales, the breadth of available models, and the concentrated focus of government policies and consumer enthusiasm have propelled PEVs in the passenger car segment to the forefront of the LEV revolution. The market share of PEVs in passenger cars is projected to exceed 70% in leading markets by 2033, underscoring their undeniable leadership.

Low Emission Vehicles Product Innovations

Product innovation in the Low Emission Vehicles (LEV) market is rapidly advancing, focusing on enhancing performance, extending range, and improving user experience. Key advancements include the development of solid-state batteries promising faster charging and increased safety, with billions invested in this frontier technology. New powertrain designs are optimizing energy efficiency, leading to longer driving ranges for Pure Electric Vehicles (PEVs), with some models now exceeding 500 miles on a single charge. The integration of sophisticated battery management systems and regenerative braking technologies further boosts efficiency. For Hybrid Electric Vehicles (HEVs), innovations are centered on seamless integration of electric and gasoline powertrains for optimal fuel economy and reduced emissions. Furthermore, the adoption of advanced driver-assistance systems (ADAS) and connectivity features are enhancing the appeal and functionality of LEVs, making them more competitive and desirable.

Propelling Factors for Low Emission Vehicles Growth

The global Low Emission Vehicles (LEV) market is propelled by a potent mix of technological, economic, and regulatory influences. Government mandates and incentives, including purchase subsidies and tax credits, are significantly reducing the cost barrier for consumers and fleet operators. Technological advancements, particularly in battery density and charging infrastructure, are addressing range anxiety and improving practicality for Pure Electric Vehicles (PEVs) and Hybrid Electric Vehicles (HEVs). The increasing awareness of climate change and the desire for a sustainable future are driving consumer demand for eco-friendly transportation. Furthermore, the declining total cost of ownership due to lower fuel and maintenance costs makes LEVs an economically attractive proposition. Billions in investments from both private companies and governments are fueling further research, development, and manufacturing expansion, creating a virtuous cycle of innovation and adoption.

Obstacles in the Low Emission Vehicles Market

Despite robust growth, the Low Emission Vehicles (LEV) market faces significant obstacles. High upfront purchase costs for some PEVs remain a barrier for a segment of consumers. Limited charging infrastructure in certain regions and the time required for charging can also deter potential buyers, especially for long-distance travel. Supply chain disruptions, particularly for critical battery components like lithium and cobalt, can lead to production delays and price volatility, impacting market growth. Grid capacity concerns in areas with high LEV penetration also present a challenge. Furthermore, consumer education and awareness gaps regarding the benefits and practicalities of LEVs still exist in some markets, alongside ongoing competitive pressures from established internal combustion engine (ICE) vehicle manufacturers who are also innovating. Quantifiable impacts include potential price increases of billions on key components and delays in model rollouts.

Future Opportunities in Low Emission Vehicles

The Low Emission Vehicles (LEV) market is ripe with emerging opportunities. The expansion of charging infrastructure into underserved rural areas and apartment complexes will unlock new consumer segments. Advances in battery technology, such as solid-state batteries and improved recycling processes, will further enhance affordability and sustainability. The growing demand for electric Commercial Vehicles, including trucks and buses, presents a significant growth avenue, driven by operational cost savings and corporate sustainability goals. The development of Vehicle-to-Grid (V2G) technology offers opportunities for LEVs to contribute to grid stability and generate revenue for owners. Furthermore, the integration of autonomous driving capabilities with LEV platforms will create new mobility services and enhance the overall user experience, opening up billions in new market potential.

Major Players in the Low Emission Vehicles Ecosystem

- Tesla Motor Company

- BYD

- Toyota

- Ford Motor Company

- General Motors Ltd

- Hyundai Motors

- Honda Motors Ltd

- BMW

- Daimler

- Mitsubishi Motor Corporation

- Isuzu Motors

Key Developments in Low Emission Vehicles Industry

- 2023 November: Tesla Motor Company unveils its next-generation Cybertruck, boasting significant advancements in electric truck technology and design.

- 2024 January: BYD announces ambitious plans to expand its global electric vehicle manufacturing footprint, investing billions in new production facilities.

- 2024 February: Ford Motor Company launches a new all-electric F-150 Lightning variant with extended range and enhanced towing capabilities.

- 2024 March: Toyota Motor Corporation showcases its latest solid-state battery technology, promising a revolution in EV charging speed and safety.

- 2024 April: General Motors Ltd announces a significant acceleration of its EV production targets, aiming to bring several new electric models to market by 2025.

- 2024 May: Hyundai Motors introduces its innovative E-GMP platform, underpinning a new generation of high-performance electric vehicles with rapid charging capabilities.

- 2024 June: Honda Motors Ltd unveils a strategic partnership focused on battery development and sourcing for its upcoming range of electric vehicles.

- 2024 July: BMW Group announces a substantial increase in its investment in electrification and digital services, signaling a strong commitment to LEVs.

- 2024 August: Daimler Truck AG reveals its long-term strategy for electric and hydrogen-powered trucks, targeting significant market share in commercial LEVs.

- 2024 September: Mitsubishi Motor Corporation announces plans to reintroduce more electrified models, focusing on hybrid and plug-in hybrid technologies in key markets.

- 2024 October: Isuzu Motors unveils its first all-electric light-duty truck, expanding its presence in the commercial LEV sector.

Strategic Low Emission Vehicles Market Forecast

The strategic low emission vehicles market forecast is overwhelmingly positive, driven by accelerating technological advancements and robust global policy support. The continuous innovation in battery technology, leading to higher energy densities and faster charging times, alongside the expansion of charging infrastructure, will significantly boost the adoption of Pure Electric Vehicles (PEVs) and Hybrid Electric Vehicles (HEVs) in both passenger car and commercial vehicle segments. Government incentives and increasingly stringent emission regulations worldwide are critical growth catalysts, pushing manufacturers to invest billions in electrification. The projected market growth, reaching trillions by 2033, signifies a profound shift towards sustainable mobility, presenting substantial opportunities for stakeholders who can adapt to this evolving landscape and cater to the burgeoning demand for cleaner transportation solutions.

Low Emission Vehicles Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Pure Electric Vehicles

- 2.2. Hybrid Electric Vehicles

- 2.3. Others

Low Emission Vehicles Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

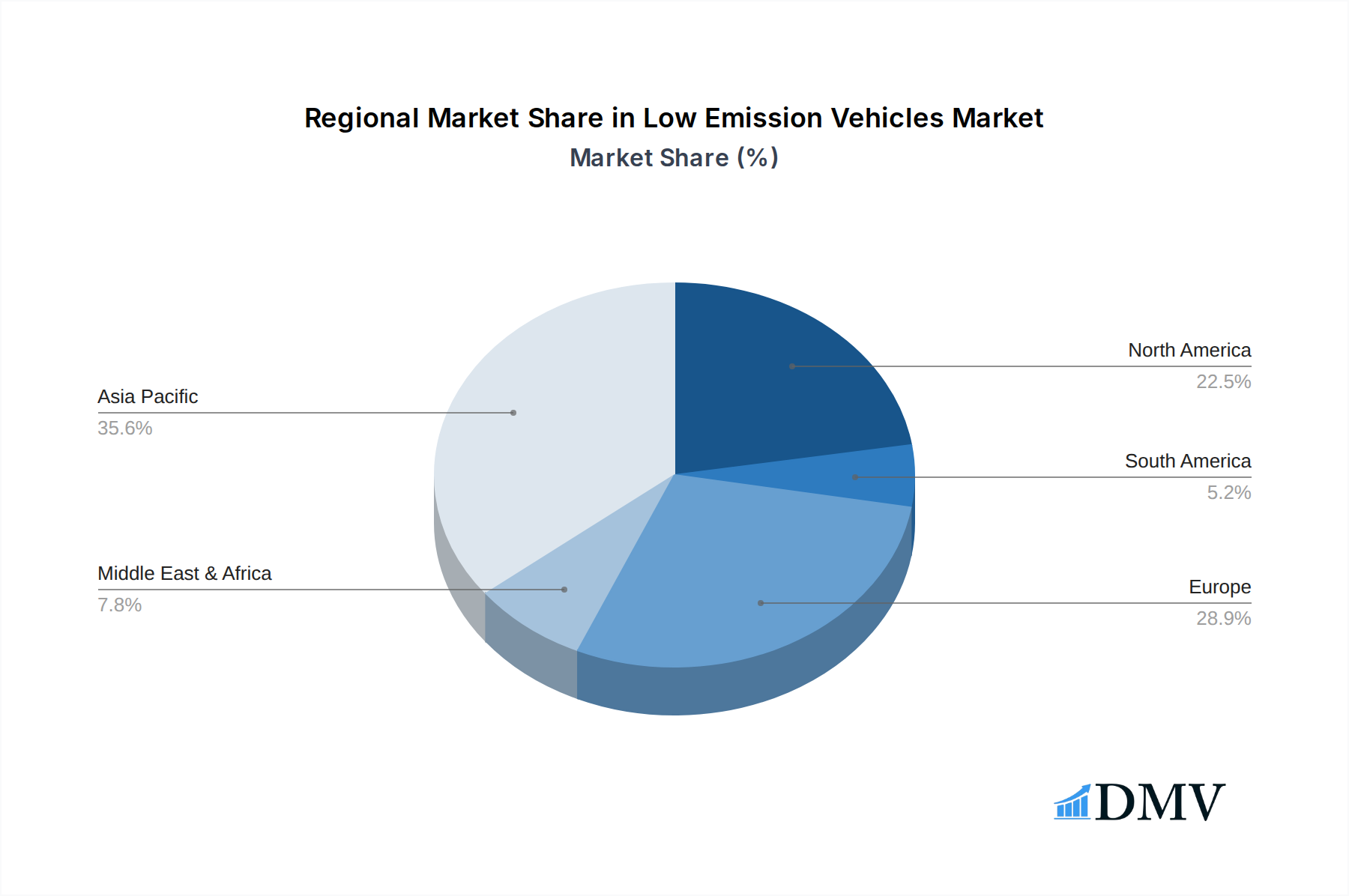

Low Emission Vehicles Regional Market Share

Geographic Coverage of Low Emission Vehicles

Low Emission Vehicles REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.31% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Pure Electric Vehicles

- 5.2.2. Hybrid Electric Vehicles

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Pure Electric Vehicles

- 6.2.2. Hybrid Electric Vehicles

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Pure Electric Vehicles

- 7.2.2. Hybrid Electric Vehicles

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Pure Electric Vehicles

- 8.2.2. Hybrid Electric Vehicles

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Pure Electric Vehicles

- 9.2.2. Hybrid Electric Vehicles

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Low Emission Vehicles Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Pure Electric Vehicles

- 10.2.2. Hybrid Electric Vehicles

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Tesla Motor Company

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Mitsubishi Motor Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Daimler

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ford Motor Company

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 General Motors Ltd

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Honda Motors Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hyundai Motors

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Toyota

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BMW

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Isuzu Motors

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BYD

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Tesla Motor Company

List of Figures

- Figure 1: Global Low Emission Vehicles Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Low Emission Vehicles Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Low Emission Vehicles Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Low Emission Vehicles Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Low Emission Vehicles Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Low Emission Vehicles Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Low Emission Vehicles Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Low Emission Vehicles Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Low Emission Vehicles Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Low Emission Vehicles Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Low Emission Vehicles Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Low Emission Vehicles Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Low Emission Vehicles Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Low Emission Vehicles Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Low Emission Vehicles Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Low Emission Vehicles Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Low Emission Vehicles Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Low Emission Vehicles Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Low Emission Vehicles Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Low Emission Vehicles Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Low Emission Vehicles Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Low Emission Vehicles Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Low Emission Vehicles Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Low Emission Vehicles Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Low Emission Vehicles Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Low Emission Vehicles Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Low Emission Vehicles Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Low Emission Vehicles Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Low Emission Vehicles Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Low Emission Vehicles Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Low Emission Vehicles Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Low Emission Vehicles Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Low Emission Vehicles Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Low Emission Vehicles Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Low Emission Vehicles Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Low Emission Vehicles Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Low Emission Vehicles Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Low Emission Vehicles Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Low Emission Vehicles Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Low Emission Vehicles Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Low Emission Vehicles?

The projected CAGR is approximately 6.31%.

2. Which companies are prominent players in the Low Emission Vehicles?

Key companies in the market include Tesla Motor Company, Mitsubishi Motor Corporation, Daimler, Ford Motor Company, General Motors Ltd, Honda Motors Ltd, Hyundai Motors, Toyota, BMW, Isuzu Motors, BYD.

3. What are the main segments of the Low Emission Vehicles?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Low Emission Vehicles," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Low Emission Vehicles report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Low Emission Vehicles?

To stay informed about further developments, trends, and reports in the Low Emission Vehicles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence