Key Insights

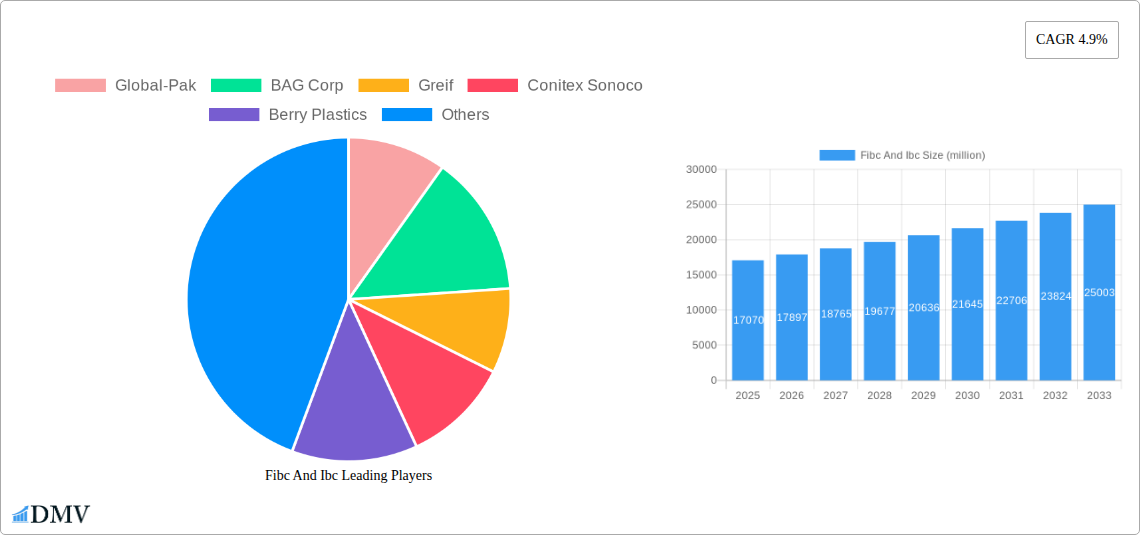

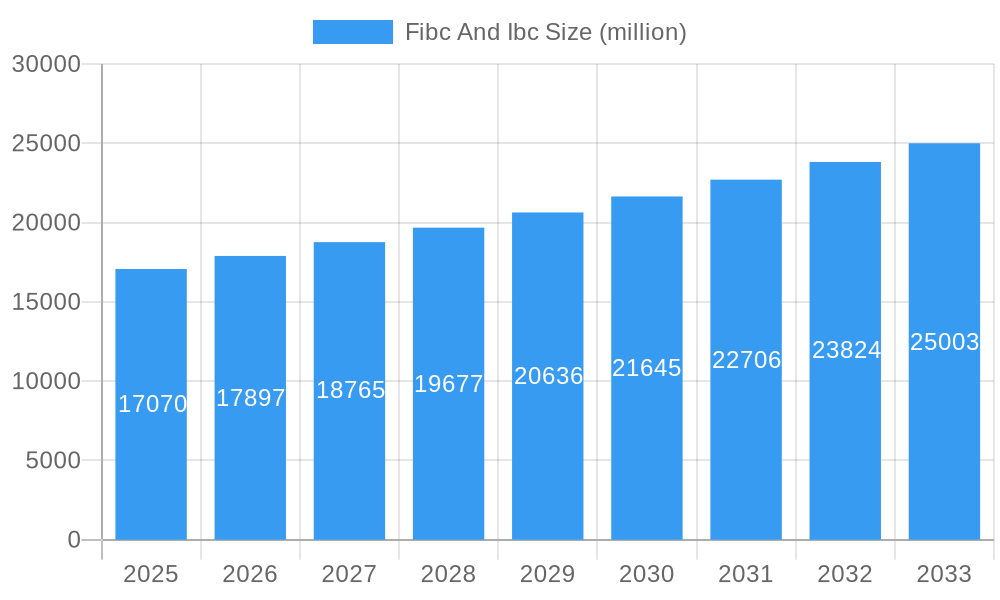

The global market for Flexible Intermediate Bulk Containers (FIBCs) and Intermediate Bulk Containers (IBCs) is poised for substantial growth, projected to reach $17,070 million by 2025. This expansion is driven by an increasing demand for efficient and cost-effective bulk material handling solutions across a multitude of industries. The 4.9% CAGR anticipated over the forecast period underscores the market's robust upward trajectory. Key applications driving this growth include the chemical industry, where FIBCs and IBCs are indispensable for the safe transport and storage of a wide range of chemicals, and the food industry, benefiting from hygienic and efficient packaging solutions. The pharmaceutical sector also represents a significant and growing segment, requiring specialized containers that meet stringent regulatory standards. The versatility of these container types, from the flexible nature of FIBCs to the robust structure of IBCs, allows them to cater to diverse material properties and handling requirements.

Fibc And Ibc Market Size (In Billion)

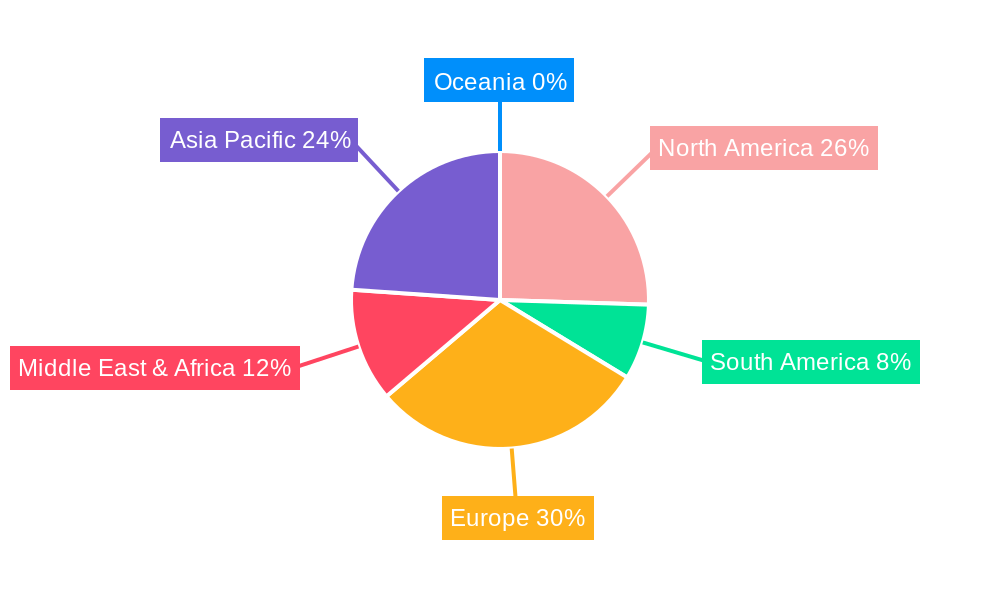

Emerging trends such as the increasing adoption of sustainable and recyclable packaging materials are shaping the future of this market. Manufacturers are innovating with lighter yet stronger materials, reducing transportation costs and environmental impact. The growing e-commerce sector and the global supply chain complexities further amplify the need for reliable bulk packaging. However, challenges such as fluctuating raw material prices, particularly for plastics and metals, and the cost associated with stringent regulatory compliance can present headwinds. Geographically, the Asia Pacific region, led by China and India, is expected to be a dominant force due to its burgeoning manufacturing base and expanding industrial activities. North America and Europe continue to be significant markets, driven by established industries and a focus on operational efficiency and safety. The market landscape is characterized by the presence of both large multinational corporations and smaller, specialized players, fostering a competitive environment focused on product innovation and customer service.

Fibc And Ibc Company Market Share

Fibc And Ibc Market Composition & Trends

This comprehensive report delves into the intricate market composition and dynamic trends shaping the global Flexible Intermediate Bulk Container (FIBC) and Intermediate Bulk Container (IBC) industry. Spanning the historical period of 2019–2024 and projecting through to 2033, with a base and estimated year of 2025, this analysis provides unparalleled insights for stakeholders. The market, while competitive, exhibits a degree of concentration among key players, with the top five companies holding an estimated xx% market share. Innovation acts as a primary catalyst, driven by the increasing demand for sustainable and efficient bulk material handling solutions. Regulatory landscapes, particularly concerning food-grade certifications and hazardous material transportation, are continuously evolving, influencing product development and market access. Substitute products, such as traditional sacks and rigid containers, pose a consistent, albeit diminishing, competitive threat. End-user profiles reveal a strong reliance on the Chemical Industry (estimated market share of xx% of total application), Food Industry (xx%), and Pharmaceutical Industry (xx%), with "Others" accounting for the remaining xx%. Mergers and Acquisitions (M&A) activities have been notable, with a total deal value estimated in the range of $xxx million to $xxx million during the historical period, indicating strategic consolidation and expansion efforts.

- Market Concentration: Leading companies like Greif, SCHÜTZ, and Mauser Group dominate, influencing pricing and innovation.

- Innovation Catalysts: Focus on enhanced durability, anti-static properties, and specialized liners for diverse applications.

- Regulatory Landscapes: Stringent compliance with UN, FDA, and ATEX standards drives product differentiation.

- Substitute Products: Traditional woven sacks and steel/plastic drums present ongoing, albeit reduced, competition.

- End-User Profiles: Industrial chemicals, agriculture, food processing, and pharmaceuticals are primary demand drivers.

- M&A Activities: Strategic acquisitions to expand geographical reach and product portfolios.

Fibc And Ibc Industry Evolution

The FIBC and IBC industry has undergone a significant transformation throughout the study period, driven by evolving industrial needs and technological advancements. From 2019 to 2024, the market witnessed a steady upward trajectory, fueled by the growing global demand for efficient and cost-effective bulk packaging solutions. This period was characterized by a compound annual growth rate (CAGR) of approximately xx% for FIBCs and xx% for IBCs. The advent of advanced manufacturing techniques, including automated weaving and specialized coating technologies, has significantly enhanced the strength, durability, and safety of these containers. Consumer demand has shifted towards more sustainable and recyclable packaging options, prompting manufacturers to invest in eco-friendly materials and production processes. Furthermore, the increasing globalization of supply chains has necessitated robust and reliable bulk containment solutions, further bolstering market growth. The adoption rate of advanced FIBCs with specialized features, such as Type C (conductive) and Type D (static dissipative) bags for hazardous materials, has seen a notable increase, driven by stringent safety regulations in industries like chemical and pharmaceutical manufacturing. Similarly, the demand for IBCs with enhanced chemical resistance and improved dispensing systems has grown, particularly within the chemical and food processing sectors. Technological advancements in material science have also played a pivotal role, leading to the development of lighter yet stronger materials, contributing to reduced transportation costs and environmental impact. The industry's evolution is a testament to its adaptability, responding effectively to both macro-economic trends and specific end-user requirements for improved performance, safety, and sustainability.

Leading Regions, Countries, or Segments in Fibc And Ibc

The global FIBC and IBC market exhibits distinct regional dominance and segment leadership, with Asia-Pacific emerging as the leading region, driven by its robust manufacturing capabilities and rapidly expanding industrial base. Within Asia-Pacific, China stands out as a key player, contributing significantly to both production and consumption. The dominance of this region is underpinned by several factors, including favorable government policies supporting manufacturing, substantial investments in infrastructure, and a vast domestic market across various application segments.

In terms of Application, the Chemical Industry commands the largest market share, estimated at xx% of the total application segment. This leadership is attributable to the inherent need for safe, reliable, and cost-effective containment solutions for a wide array of chemicals, ranging from raw materials to finished products. The stringent safety regulations governing the transportation and storage of chemicals further necessitate the use of specialized FIBCs and IBCs, particularly those with UN certifications and enhanced anti-static properties. The Food Industry follows closely, accounting for approximately xx% of the market. The growing demand for packaged food products, coupled with the need for hygienic and food-grade compliant packaging solutions, drives the adoption of FIBCs and IBCs. Key drivers in this segment include the increasing global population, urbanization, and the rise of the processed food sector. The Pharmaceutical Industry represents a significant, albeit smaller, segment, estimated at xx%. The pharmaceutical sector demands the highest standards of purity, containment, and sterility, making specialized, high-quality FIBCs and IBCs crucial for the safe transport of active pharmaceutical ingredients (APIs) and finished drug products. "Others," encompassing sectors like agriculture, construction, and mining, contribute the remaining xx% to the application segment, showcasing the versatile utility of these bulk packaging solutions.

When examining the Type of containers, FIBCs generally hold a larger market share due to their versatility and cost-effectiveness for a broad range of applications, estimated at xx% of the total type segment. Their lightweight nature and ability to be folded for storage and transportation make them highly practical. IBCs, while commanding a smaller but significant share (estimated at xx%), offer superior rigidity, reusability, and containment for liquids and semi-liquids, making them indispensable in specific industries like chemical and food processing where spill prevention and precise dispensing are paramount.

- Leading Region: Asia-Pacific

- Key Drivers: Strong manufacturing base, rapid industrialization, significant domestic demand.

- Dominant Country: China, as a manufacturing hub and major consumer.

- Leading Application Segment: Chemical Industry

- Key Drivers: Safety regulations, demand for hazardous material containment, efficiency in bulk handling.

- Investment Trends: Manufacturers investing in specialized, UN-certified FIBCs and robust IBCs.

- Second Largest Application Segment: Food Industry

- Key Drivers: Growing global food demand, hygiene requirements, food-grade compliance.

- Regulatory Support: Adherence to international food safety standards.

- Growing Application Segment: Pharmaceutical Industry

- Key Drivers: Need for sterile, high-purity containment, stringent regulatory requirements.

- Dominant Container Type: FIBCs

- Key Drivers: Versatility, cost-effectiveness, lightweight nature for diverse applications.

- Significant Container Type: IBCs

- Key Drivers: Reusability, rigidity, superior containment for liquids and semi-liquids.

Fibc And Ibc Product Innovations

Recent product innovations in the FIBC and IBC market are centered on enhancing sustainability, safety, and efficiency. Manufacturers are increasingly developing FIBCs made from recycled or biodegradable materials, significantly reducing their environmental footprint. Advancements in static control technology have led to the creation of Type D FIBCs that safely handle highly flammable materials without the need for grounding, a critical development for the chemical industry. In the IBC segment, innovations include smart features such as integrated sensors for real-time monitoring of product levels and temperature, alongside improved valve systems for enhanced dispensing and reduced waste. The introduction of multi-trip IBCs with enhanced durability and ease of cleaning further promotes reusability and cost savings for end-users. These innovations aim to not only meet evolving regulatory demands but also to provide superior performance and operational benefits.

Propelling Factors for Fibc And Ibc Growth

The FIBC and IBC market is propelled by a confluence of factors driving sustained growth. The increasing global demand for bulk materials across industries like chemicals, food, and pharmaceuticals necessitates efficient and cost-effective containment solutions. Technological advancements in manufacturing processes and material science contribute by enhancing the durability, safety, and functionality of these containers. For example, the development of anti-static FIBCs has opened up new markets in hazardous material handling. Stringent safety and environmental regulations worldwide are pushing for more secure and compliant packaging, favoring certified FIBCs and IBCs. Furthermore, the growing emphasis on supply chain efficiency and cost optimization by businesses worldwide makes these reusable and space-saving solutions highly attractive.

Obstacles in the Fibc And Ibc Market

Despite robust growth prospects, the FIBC and IBC market faces several obstacles. Fluctuations in raw material prices, particularly for polypropylene, can impact production costs and profit margins. Increasingly stringent environmental regulations regarding plastic waste management and recycling present a challenge, requiring continuous investment in sustainable solutions. Supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can lead to delays and increased costs. Furthermore, the presence of unorganized players offering lower-priced, potentially lower-quality products creates price pressure and can affect market perception.

Future Opportunities in Fibc And Ibc

The future of the FIBC and IBC market is ripe with opportunities. The burgeoning e-commerce sector presents a growing demand for bulk packaging for various goods. The increasing focus on sustainable and circular economy initiatives will drive demand for biodegradable and highly recyclable FIBCs and IBCs. Emerging economies in regions like Africa and Southeast Asia offer significant untapped potential due to ongoing industrialization. Furthermore, smart packaging solutions, integrating IoT capabilities for real-time tracking and monitoring, represent a significant technological frontier. The development of specialized FIBCs and IBCs for niche applications, such as advanced agriculture and renewable energy sectors, also holds considerable promise.

Major Players in the Fibc And Ibc Ecosystem

- Global-Pak

- BAG Corp

- Greif

- Conitex Sonoco

- Berry Plastics

- AmeriGlobe

- LC Packaging

- RDA Bulk Packaging

- Sackmaker

- Langston

- Taihua Group

- Halsted

- Intertape Polymer

- SCHÜTZ

- Mauser Group

- Shijiheng

- Snyder Industries

- ZhenJiang JinShan Packing Factory

- Time Technoplast Limited

- Myers Industries

- Hoover Ferguson Group

Key Developments in Fibc And Ibc Industry

- 2023 November: Greif acquires a majority stake in a leading European FIBC manufacturer to expand its European footprint.

- 2024 January: SCHÜTZ launches a new generation of IBCs with enhanced chemical resistance and improved sealing technology.

- 2024 March: Conitex Sonoco announces significant investment in expanding its recycled content FIBC production capabilities.

- 2024 April: Intertape Polymer Group acquires a competitor, strengthening its position in the North American FIBC market.

- 2024 May: Time Technoplast Limited introduces a range of biodegradable FIBCs targeting the agricultural sector.

Strategic Fibc And Ibc Market Forecast

The strategic outlook for the FIBC and IBC market remains exceptionally positive, driven by overarching global trends. The continuous industrialization in emerging economies, coupled with the growing demand for efficient bulk material handling across core sectors like chemicals and food, will serve as primary growth catalysts. Furthermore, the increasing regulatory emphasis on safety and environmental compliance is fostering innovation in product development, pushing manufacturers towards more sustainable and high-performance solutions. The market is poised for significant expansion as companies prioritize supply chain optimization and cost reduction, making advanced FIBCs and IBCs indispensable tools for operational excellence. The forecasted growth trajectory indicates sustained demand and strategic opportunities for market players.

Fibc And Ibc Segmentation

-

1. Application

- 1.1. Chemical Industry

- 1.2. Food Industry

- 1.3. Pharmaceutical Industry

- 1.4. Others

-

2. Type

- 2.1. FIBCs

- 2.2. IBCs

Fibc And Ibc Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fibc And Ibc Regional Market Share

Geographic Coverage of Fibc And Ibc

Fibc And Ibc REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Chemical Industry

- 5.1.2. Food Industry

- 5.1.3. Pharmaceutical Industry

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. FIBCs

- 5.2.2. IBCs

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Fibc And Ibc Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Chemical Industry

- 6.1.2. Food Industry

- 6.1.3. Pharmaceutical Industry

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. FIBCs

- 6.2.2. IBCs

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Fibc And Ibc Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Chemical Industry

- 7.1.2. Food Industry

- 7.1.3. Pharmaceutical Industry

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. FIBCs

- 7.2.2. IBCs

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Fibc And Ibc Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Chemical Industry

- 8.1.2. Food Industry

- 8.1.3. Pharmaceutical Industry

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. FIBCs

- 8.2.2. IBCs

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Fibc And Ibc Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Chemical Industry

- 9.1.2. Food Industry

- 9.1.3. Pharmaceutical Industry

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. FIBCs

- 9.2.2. IBCs

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Fibc And Ibc Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Chemical Industry

- 10.1.2. Food Industry

- 10.1.3. Pharmaceutical Industry

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. FIBCs

- 10.2.2. IBCs

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Fibc And Ibc Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Chemical Industry

- 11.1.2. Food Industry

- 11.1.3. Pharmaceutical Industry

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. FIBCs

- 11.2.2. IBCs

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Global-Pak

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 BAG Corp

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Greif

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Conitex Sonoco

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Berry Plastics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AmeriGlobe

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 LC Packaging

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 RDA Bulk Packaging

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sackmaker

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Langston

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Taihua Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Halsted

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Intertape Polymer

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 SCHÜTZ

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Mauser Group

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Shijiheng

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Snyder Industries

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 ZhenJiang JinShan Packing Factory

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Time Technoplast Limited

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Myers Industries

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Hoover Ferguson Group

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 Global-Pak

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fibc And Ibc Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Fibc And Ibc Revenue (million), by Application 2025 & 2033

- Figure 3: North America Fibc And Ibc Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fibc And Ibc Revenue (million), by Type 2025 & 2033

- Figure 5: North America Fibc And Ibc Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Fibc And Ibc Revenue (million), by Country 2025 & 2033

- Figure 7: North America Fibc And Ibc Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fibc And Ibc Revenue (million), by Application 2025 & 2033

- Figure 9: South America Fibc And Ibc Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fibc And Ibc Revenue (million), by Type 2025 & 2033

- Figure 11: South America Fibc And Ibc Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Fibc And Ibc Revenue (million), by Country 2025 & 2033

- Figure 13: South America Fibc And Ibc Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fibc And Ibc Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Fibc And Ibc Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fibc And Ibc Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Fibc And Ibc Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Fibc And Ibc Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Fibc And Ibc Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fibc And Ibc Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fibc And Ibc Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fibc And Ibc Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Fibc And Ibc Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Fibc And Ibc Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fibc And Ibc Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fibc And Ibc Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Fibc And Ibc Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fibc And Ibc Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Fibc And Ibc Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Fibc And Ibc Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Fibc And Ibc Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Fibc And Ibc Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Fibc And Ibc Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Fibc And Ibc Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Fibc And Ibc Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Fibc And Ibc Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Fibc And Ibc Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Fibc And Ibc Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Fibc And Ibc Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fibc And Ibc Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fibc And Ibc?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the Fibc And Ibc?

Key companies in the market include Global-Pak, BAG Corp, Greif, Conitex Sonoco, Berry Plastics, AmeriGlobe, LC Packaging, RDA Bulk Packaging, Sackmaker, Langston, Taihua Group, Halsted, Intertape Polymer, SCHÜTZ, Mauser Group, Shijiheng, Snyder Industries, ZhenJiang JinShan Packing Factory, Time Technoplast Limited, Myers Industries, Hoover Ferguson Group.

3. What are the main segments of the Fibc And Ibc?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17070 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fibc And Ibc," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fibc And Ibc report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fibc And Ibc?

To stay informed about further developments, trends, and reports in the Fibc And Ibc, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence