Key Insights

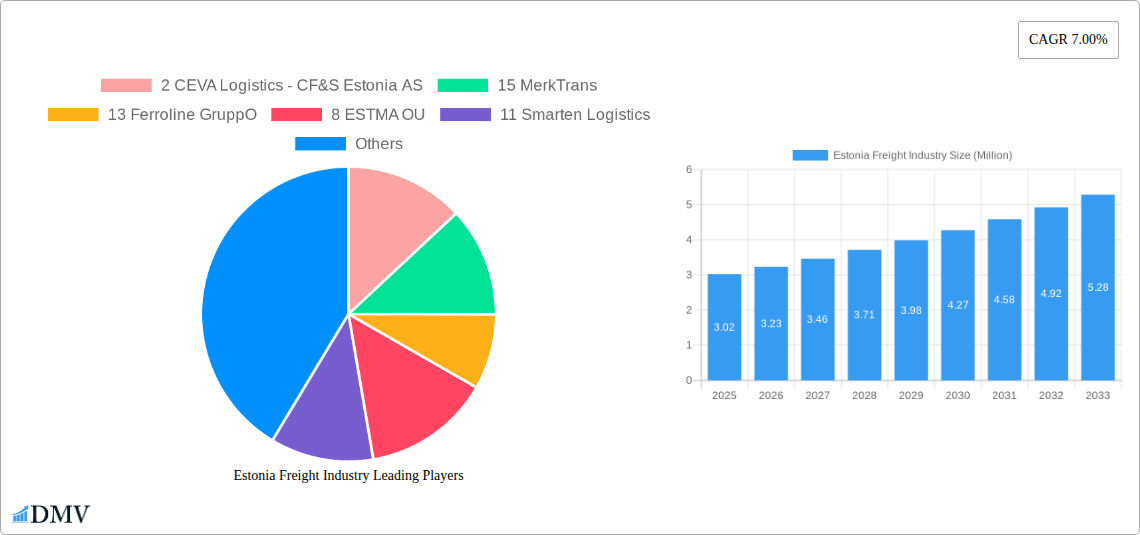

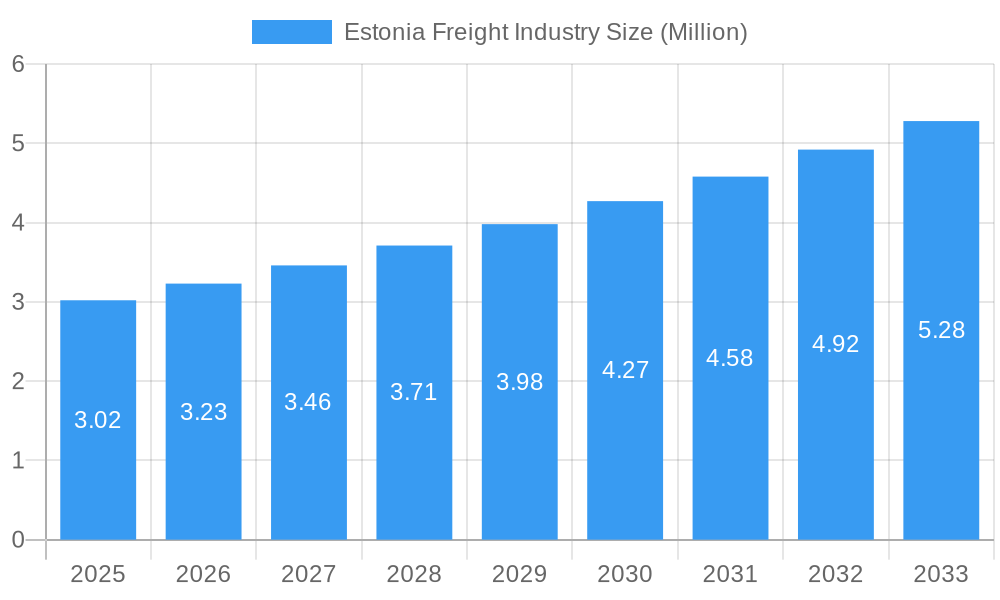

The Estonian freight industry, valued at €3.02 million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 7% from 2025 to 2033. This expansion is fueled by several key drivers. The increasing cross-border trade facilitated by Estonia's strategic location within the European Union and its robust digital infrastructure plays a significant role. Furthermore, the growth of e-commerce and the resulting demand for efficient last-mile delivery solutions are significantly impacting the market. Expansion of manufacturing and automotive sectors within Estonia, as well as growth in related industries like construction and distributive trade (including FMCG), create consistent demand for freight services. While specific restraints aren't detailed, potential challenges could include fluctuations in global fuel prices, infrastructure limitations, and the competitive landscape characterized by both large multinational players (like DHL and DSV) and smaller, local logistics providers such as MerkTrans, Ferroline GruppO, and others. The market segmentation reveals a diverse range of services including rail freight forwarding, warehousing, value-added services, and various end-user industries. The dominance of specific segments will likely shift according to economic conditions and investment in infrastructure. The continued focus on efficiency, technological innovation (e.g., implementing advanced tracking systems and route optimization software), and the adoption of sustainable practices will shape the competitive dynamics within the Estonian freight market over the forecast period.

Estonia Freight Industry Market Size (In Million)

The Estonian freight market presents opportunities for both established and emerging players. Companies specializing in niche services, such as those catering to the specific needs of the healthcare and pharmaceuticals sector, or those leveraging technology for enhanced efficiency, are well-positioned to capitalize on market growth. Furthermore, consolidation within the market – where smaller providers are potentially acquired by larger firms – is a likely trend, leading to increased market concentration. Sustained economic growth in Estonia and the wider EU will be a key factor driving overall market performance. Strategic partnerships and investments in modernizing infrastructure will be crucial for industry players to maintain competitiveness and achieve sustainable growth in the coming years.

Estonia Freight Industry Company Market Share

Estonia Freight Industry Market Composition & Trends

This insightful report provides a comprehensive analysis of the Estonia freight industry, covering the period 2019-2033. We delve into the market's intricate composition, identifying key trends shaping its evolution. The Estonian freight market, valued at xx Million in 2024, is characterized by a moderately concentrated landscape. While a few major players dominate, numerous smaller firms contribute significantly to the overall activity. The market share distribution is uneven, with the top five players controlling approximately xx% of the market (2024 data). Innovation is driven by technological advancements in logistics technology and the adoption of sustainable practices. The regulatory landscape, while generally supportive, faces ongoing adjustments to address the evolving industry needs. Substitute products, such as alternative transportation modes, present a level of competitive pressure, influencing pricing strategies and operational efficiency. M&A activity has been moderate in recent years, with total deal values reaching approximately xx Million during the historical period.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2024.

- Innovation Catalysts: Technological advancements in logistics technology, sustainability initiatives.

- Regulatory Landscape: Supportive but subject to ongoing adjustments.

- Substitute Products: Alternative transportation modes exert competitive pressure.

- End-User Profiles: Manufacturing and automotive, oil and gas, distributive trade (FMCG included), and other sectors.

- M&A Activity: Moderate, with total deal values reaching approximately xx Million (2019-2024).

Estonia Freight Industry Industry Evolution

The Estonian freight industry demonstrates a dynamic evolution, marked by significant growth trajectories and transformative technological advancements. From 2019 to 2024, the market experienced a Compound Annual Growth Rate (CAGR) of xx%, driven largely by expanding e-commerce and increased cross-border trade. This growth is projected to continue, with a forecasted CAGR of xx% from 2025 to 2033, reaching a market value of xx Million by 2033. Technological advancements, such as the implementation of advanced transportation management systems (TMS) and warehouse management systems (WMS), are streamlining operations and boosting efficiency. The rising adoption of digital solutions, including blockchain technology for enhanced supply chain transparency and big data analytics for optimized routing and forecasting, is a crucial driver. Consumer demands are shifting towards faster delivery times, increased transparency, and sustainable practices, prompting companies to adopt innovative solutions and operational models. Growth in specific segments, like e-commerce logistics, is outpacing the overall market average.

Leading Regions, Countries, or Segments in Estonia Freight Industry

The Estonian freight industry shows significant strength across various segments and geographic areas. While a comprehensive regional breakdown is challenging given data limitations, the major growth drivers are consistently identified across the industry.

- By Function: Freight transport accounts for the largest share, owing to its foundational role in moving goods across the country and internationally.

- By End User: The manufacturing and automotive sector displays the highest volume due to significant production and export activity. Distributive trade (wholesale and retail, including FMCG) is another major contributor, driven by consumer demand and efficient supply chain needs.

- By Rail Function: Freight forwarding emerges as a leading segment within the rail sector due to the efficiency of rail for long-distance transport. Warehousing is also significant given Estonia's strategic location as a transit hub.

Key factors driving dominance in these segments include substantial investments in infrastructure, government support for logistics development, and the strategic location of Estonia, facilitating efficient movement of goods within the Baltic region and further afield. The high degree of digitalization within the Estonian economy also strongly supports the growth of these segments.

Estonia Freight Industry Product Innovations

Recent innovations focus on enhancing efficiency, sustainability, and visibility across the supply chain. This includes the adoption of IoT sensors for real-time tracking, AI-powered route optimization software, and automated warehousing solutions. These innovations are improving delivery times, reducing costs, and minimizing environmental impact. Unique selling propositions center around offering customized, flexible, and technology-driven solutions tailored to meet specific client needs. The integration of these advancements enhances efficiency and customer satisfaction.

Propelling Factors for Estonia Freight Industry Growth

Growth in the Estonian freight industry is fueled by several key factors. Firstly, the country's strategic geographic location within the Baltic region acts as a vital transit hub, linking East and West. Secondly, robust economic growth and expanding e-commerce drive increased demand for freight services. Thirdly, ongoing investments in infrastructure development, including port and rail improvements, enhance transport capacity and efficiency. Finally, supportive government policies and a business-friendly environment encourage further investment and innovation within the sector.

Obstacles in the Estonia Freight Industry Market

The Estonian freight industry faces challenges including seasonal fluctuations in demand, which can lead to capacity constraints. Furthermore, the reliance on a limited number of major players can create vulnerabilities to price volatility and supply chain disruptions. International geopolitical factors can also influence trade flows and logistics costs. The ongoing transition to more sustainable transportation options requires investment and adaptation across the sector.

Future Opportunities in Estonia Freight Industry

Future opportunities lie in expanding into new niche markets, particularly in the growing e-commerce and healthcare sectors. Technological advancements, such as drone delivery and autonomous vehicles, present possibilities for enhanced efficiency and reduced costs. Furthermore, promoting sustainable logistics solutions, emphasizing environmentally friendly transportation modes, can attract environmentally conscious clients and positively impact the industry's long-term prospects.

Major Players in the Estonia Freight Industry Ecosystem

- CEVA Logistics - CF&S Estonia AS

- MerkTrans

- Ferroline GruppO

- ESTMA OU

- Smarten Logistics

- KGK Logistics

- TT Estonia

- Parme Trans

- Hanson Logistics

- DHL EXPRESS

- DSV

- Group logistics OU

- Delamode Estonia

- Ace Logistics Estonia

- CF&S Estonia AS

- Rhenus Logistics

- Tallinna Toiduveod AS

Key Developments in Estonia Freight Industry Industry

- July 2023: DHL Express opens a new Americas region hub in Atlanta, strengthening its global network and enhancing service capabilities between the U.S. and Europe. This demonstrates a significant investment in infrastructure and highlights the ongoing expansion of global logistics networks.

- July 2023: CEVA Logistics implements warehouse automation in the Netherlands, significantly boosting efficiency and capacity during peak seasons. This exemplifies the adoption of advanced technologies to optimize warehouse operations and improve overall productivity.

Strategic Estonia Freight Industry Market Forecast

The Estonian freight industry is poised for sustained growth, driven by increasing e-commerce, continued investments in infrastructure, and the adoption of innovative technologies. The forecast predicts a robust expansion in market size over the next decade, making it an attractive sector for investment and innovation. The focus on sustainable practices and digitalization will further shape the industry's future trajectory.

Estonia Freight Industry Segmentation

-

1. Function

-

1.1. Freight Transport

- 1.1.1. Road

- 1.1.2. Inland Water

- 1.1.3. Air

- 1.1.4. Rail

- 1.2. Freight Forwarding

- 1.3. Warehousing

- 1.4. Value Added Services and Other Functions

-

1.1. Freight Transport

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Oil and Gas, Mining and Quarrying

- 2.3. Agriculture,Fishing and Forestry

- 2.4. Construction

- 2.5. Distribu

- 2.6. Healthcare and Pharmaceuticals

- 2.7. Other End Users

Estonia Freight Industry Segmentation By Geography

- 1. Estonia

Estonia Freight Industry Regional Market Share

Geographic Coverage of Estonia Freight Industry

Estonia Freight Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Function

- 5.1.1. Freight Transport

- 5.1.1.1. Road

- 5.1.1.2. Inland Water

- 5.1.1.3. Air

- 5.1.1.4. Rail

- 5.1.2. Freight Forwarding

- 5.1.3. Warehousing

- 5.1.4. Value Added Services and Other Functions

- 5.1.1. Freight Transport

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Oil and Gas, Mining and Quarrying

- 5.2.3. Agriculture,Fishing and Forestry

- 5.2.4. Construction

- 5.2.5. Distribu

- 5.2.6. Healthcare and Pharmaceuticals

- 5.2.7. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Estonia

- 5.1. Market Analysis, Insights and Forecast - by Function

- 6. Estonia Freight Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Function

- 6.1.1. Freight Transport

- 6.1.1.1. Road

- 6.1.1.2. Inland Water

- 6.1.1.3. Air

- 6.1.1.4. Rail

- 6.1.2. Freight Forwarding

- 6.1.3. Warehousing

- 6.1.4. Value Added Services and Other Functions

- 6.1.1. Freight Transport

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Oil and Gas, Mining and Quarrying

- 6.2.3. Agriculture,Fishing and Forestry

- 6.2.4. Construction

- 6.2.5. Distribu

- 6.2.6. Healthcare and Pharmaceuticals

- 6.2.7. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Function

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 2 CEVA Logistics - CF&S Estonia AS

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 15 MerkTrans

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 13 Ferroline GruppO

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 8 ESTMA OU

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 11 Smarten Logistics

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 16 KGK Logistics**List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 5 TT Estonia

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 9 Parme Trans

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 6 Hanson Logistics

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 DHL EXPRESS

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 3 DSV

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 4 Group logistics OU

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 7 Delamode Estonia

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 10 Ace Logistics Estonia

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 14 CF&S Estonia AS

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 1 Rhenus Logistics

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 12 Tallinna Toiduveod AS

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.1 2 CEVA Logistics - CF&S Estonia AS

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Estonia Freight Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Estonia Freight Industry Share (%) by Company 2025

List of Tables

- Table 1: Estonia Freight Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 2: Estonia Freight Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Estonia Freight Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Estonia Freight Industry Revenue Million Forecast, by Function 2020 & 2033

- Table 5: Estonia Freight Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Estonia Freight Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Estonia Freight Industry?

The projected CAGR is approximately 7.00%.

2. Which companies are prominent players in the Estonia Freight Industry?

Key companies in the market include 2 CEVA Logistics - CF&S Estonia AS, 15 MerkTrans, 13 Ferroline GruppO, 8 ESTMA OU, 11 Smarten Logistics, 16 KGK Logistics**List Not Exhaustive, 5 TT Estonia, 9 Parme Trans, 6 Hanson Logistics, DHL EXPRESS, 3 DSV, 4 Group logistics OU, 7 Delamode Estonia, 10 Ace Logistics Estonia, 14 CF&S Estonia AS, 1 Rhenus Logistics, 12 Tallinna Toiduveod AS.

3. What are the main segments of the Estonia Freight Industry?

The market segments include Function, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Investments in the logistics infrastructure; Government Initiatives.

6. What are the notable trends driving market growth?

Rapid Growth of E commerce in the Region.

7. Are there any restraints impacting market growth?

Poor Infrastructure.

8. Can you provide examples of recent developments in the market?

July 2023: DHL Express, the world's leading provider of express shipping services, has announced the grand opening of its Americas region hub based at the Hartsfield-Jackson Atlanta International Airport (ATL). With a focus on sustainability, the USD 84.5 million investment further strengthens the company's connections and service capabilities between the U.S. and key global markets, increasing capacity, speeding transit times, and adding resilience to its network. Spanning 100,000 square feet, the state-of-the-art hub establishes direct connections between 19 cities in the Southeastern U.S. and key global markets, including Europe and major DHL hubs worldwide.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Estonia Freight Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Estonia Freight Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Estonia Freight Industry?

To stay informed about further developments, trends, and reports in the Estonia Freight Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence