Key Insights

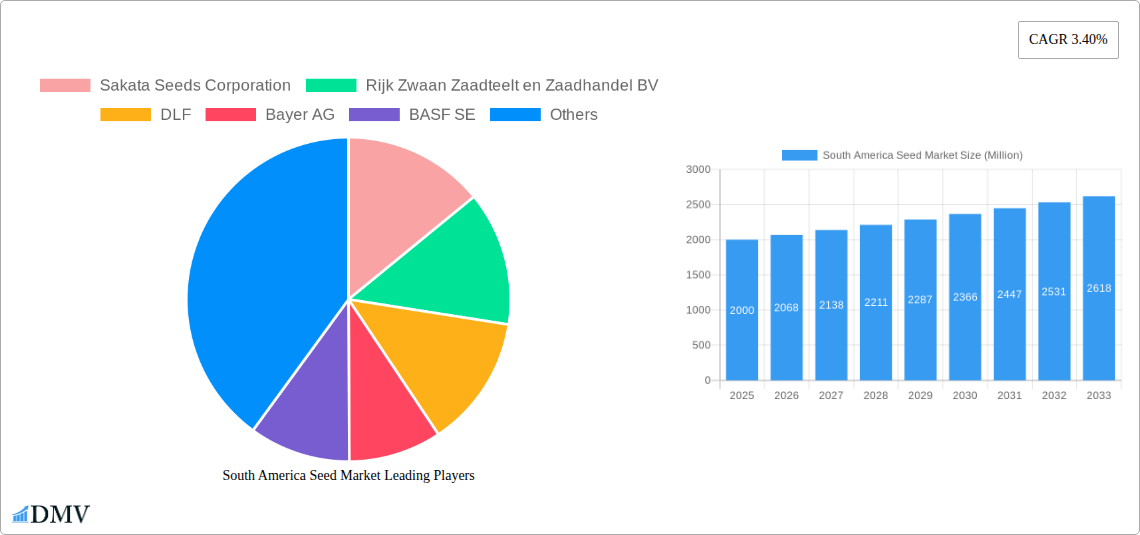

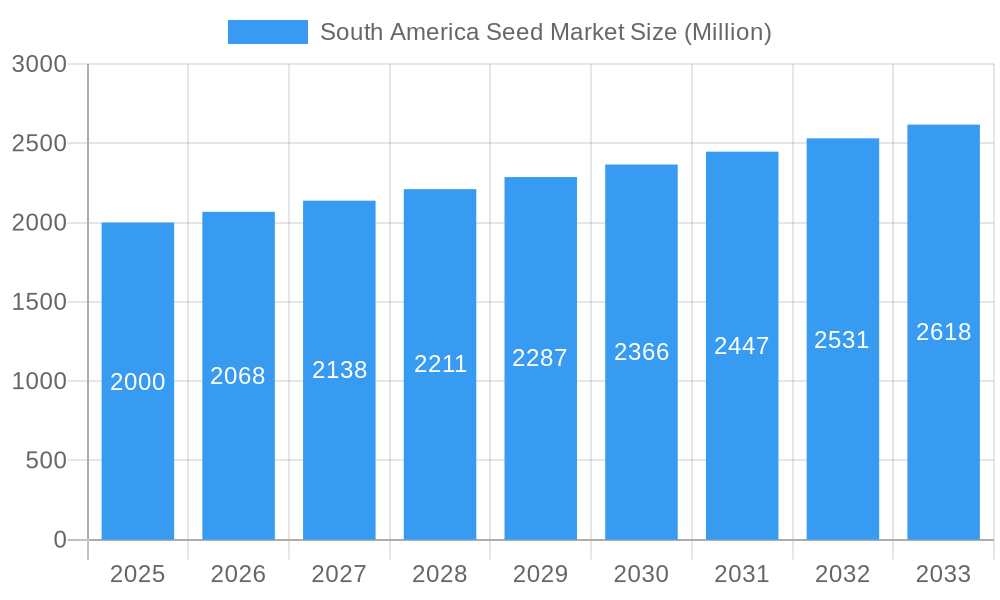

The South American seed market, valued at approximately $XX million in 2025, is projected to experience steady growth with a Compound Annual Growth Rate (CAGR) of 3.40% from 2025 to 2033. This growth is driven by several factors. Increased demand for high-yielding and disease-resistant crop varieties, particularly in key agricultural regions like Brazil and Argentina, fuels market expansion. The rising adoption of advanced breeding technologies, such as hybrids, further enhances crop productivity and contributes to market growth. Furthermore, the shift towards protected cultivation methods, offering better crop control and yield stability, is a significant trend. While challenges remain, such as fluctuating weather patterns impacting yields and the dependence on global seed suppliers, the overall market outlook remains positive. The increasing focus on food security and the growing adoption of sustainable agricultural practices are anticipated to support market growth in the long term. Segment-wise, open-field cultivation currently dominates, but protected cultivation is experiencing significant growth, particularly for high-value vegetable crops. Brazil and Argentina represent the largest national markets, reflecting their substantial agricultural sectors.

South America Seed Market Market Size (In Billion)

The leading players in the South American seed market, including Sakata Seeds Corporation, Rijk Zwaan, DLF, Bayer AG, BASF SE, Limagrain, KWS SAAT, Advanta Seeds (UPL), Syngenta Group, and Corteva Agriscience, are actively involved in research and development to introduce innovative seed varieties tailored to local needs. Competition is intense, with companies focusing on strategic partnerships, mergers, and acquisitions to expand their market presence and product portfolios. Future growth will likely be influenced by government policies supporting agricultural development, technological advancements in seed production and distribution, and the overall global economic conditions affecting agricultural investment. The continued focus on improving crop yields and addressing climate change challenges will remain key drivers for market expansion throughout the forecast period.

South America Seed Market Company Market Share

South America Seed Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the South America seed market, offering a comprehensive overview of its current state and future trajectory. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report delves into market segmentation, key players, growth drivers, and challenges, providing valuable insights for stakeholders across the seed industry. With a projected market value exceeding xx Million by 2033, this report is an indispensable resource for strategic decision-making.

South America Seed Market Composition & Trends

The South America seed market exhibits a moderately concentrated landscape, with major players like Bayer AG, BASF SE, Corteva Agriscience, and Syngenta Group holding significant market share. The combined market share of the top five players is estimated at xx%, indicating opportunities for smaller players to carve out niches. Market concentration is influenced by factors such as economies of scale in research and development, extensive distribution networks, and strong brand recognition.

Innovation is a key driver, with companies investing heavily in breeding technologies like hybrids to improve crop yields and resilience. The regulatory landscape is evolving, with varying regulations across countries affecting seed approvals and labeling. Substitute products, including traditional seed saving practices, pose a competitive challenge, though their impact is relatively limited due to the advantages offered by improved hybrid seeds. End-users primarily comprise commercial farmers and smaller-scale agricultural operations, with the latter segment increasingly adopting advanced seed technologies. The historical period (2019-2024) witnessed several M&A activities, with deal values totaling approximately xx Million, primarily focused on consolidating market positions and accessing new technologies.

- Market Share Distribution (2025): Bayer AG (xx%), BASF SE (xx%), Corteva Agriscience (xx%), Syngenta Group (xx%), Others (xx%)

- M&A Activity (2019-2024): Total Deal Value: xx Million

- Key Innovation Catalysts: Hybrid seed technology, biotechnology advancements, precision agriculture.

- Regulatory Landscape: Varies across countries, impacting seed approvals and labeling requirements.

South America Seed Market Industry Evolution

The South America seed market has witnessed consistent growth over the past five years, with a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024). This growth is driven by several factors, including increasing agricultural output to meet growing food demands, rising adoption of improved seed varieties, government initiatives promoting agricultural modernization, and expansion of cultivated land. The market is expected to maintain a robust growth trajectory, with a projected CAGR of xx% during the forecast period (2025-2033), reaching a market value exceeding xx Million by 2033. Technological advancements, particularly in precision breeding techniques and biotechnology, are playing a crucial role in shaping industry evolution. The increasing adoption of hybrid seeds, coupled with the development of disease-resistant and climate-resilient varieties, is significantly enhancing crop yields and contributing to overall market expansion. Shifting consumer demands for sustainably produced food are influencing industry practices, driving demand for environmentally friendly seed technologies and sustainable farming methods. The rising awareness among farmers about the benefits of improved seed varieties has been a major catalyst driving this growth. Furthermore, increasing investments in agricultural research and development contribute to continuous improvement in seed quality and attributes leading to higher yields and enhanced profitability.

Leading Regions, Countries, or Segments in South America Seed Market

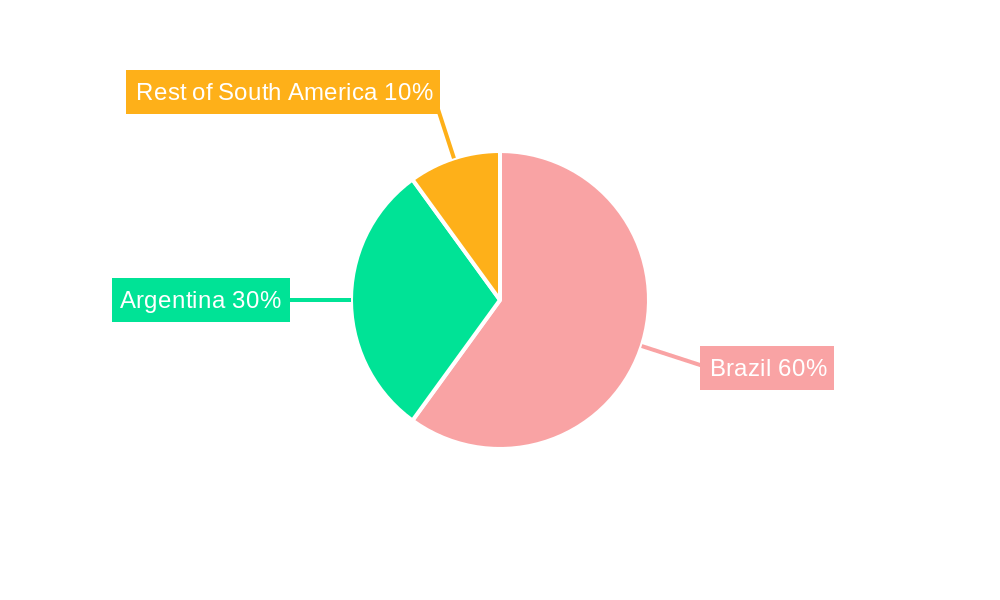

Brazil dominates the South America seed market, accounting for approximately xx% of the total market value in 2025. Its large agricultural sector, favorable climate conditions, and government support for agricultural development contribute to its leading position. Argentina follows as the second-largest market, contributing xx% to the total market value, driven by its strong agricultural export sector. The "Rest of South America" region exhibits significant growth potential, though it lags behind Brazil and Argentina due to factors like smaller agricultural land areas and lower investment in agricultural infrastructure.

Within cultivation mechanisms, open field cultivation holds the largest market share, driven by the vast expanse of arable land suitable for this method. However, protected cultivation is experiencing significant growth, fueled by rising demand for high-quality produce and technological advancements enabling cost-effective protected cultivation. In crop types, row crops (e.g., soybeans, corn) represent the largest segment, owing to their high economic value and widespread cultivation. The pulses and vegetable segments are also experiencing steady growth, driven by increasing consumption of these crops. Hybrid seeds are the dominant breeding technology, owing to their superior yields and other improved agronomic traits.

- Key Drivers for Brazil's Dominance: Large agricultural land, favorable climate, government support, strong export sector.

- Key Drivers for Argentina's Market: Strong agricultural exports, large-scale farming practices.

- Growth Potential in the "Rest of South America": Expanding agricultural land, increasing investments in infrastructure and technology.

- Dominant Cultivation Mechanism: Open Field

- Dominant Crop Type: Row Crops

- Dominant Breeding Technology: Hybrids

South America Seed Market Product Innovations

Recent innovations focus on developing seeds with enhanced traits such as improved yield, disease resistance, herbicide tolerance, and climate resilience. Companies are actively utilizing advanced breeding techniques, including marker-assisted selection (MAS) and gene editing technologies, to create superior seed varieties. These innovations aim to address challenges like climate change, pest infestations, and weed pressure, contributing to higher crop yields and profitability for farmers. The development of seeds with improved nutritional content and enhanced shelf life is also gaining traction, driven by increasing consumer demand for healthier and more sustainable food options. Unique selling propositions often center around high yield potential, reduced input costs (e.g., reduced pesticide use), and enhanced crop resilience.

Propelling Factors for South America Seed Market Growth

Several factors are propelling the growth of the South America seed market. Firstly, technological advancements in seed breeding and biotechnology, such as hybrid technology and genetic modification, are leading to improved seed varieties with higher yields and better disease resistance. Secondly, increasing government support and investment in agricultural infrastructure are encouraging farmers to adopt modern farming practices and high-yielding seeds. Thirdly, a growing population and rising incomes in the region are driving demand for food, resulting in increased agricultural production and a higher demand for improved seeds. Lastly, favorable climate conditions in parts of South America provide a conducive environment for crop cultivation.

Obstacles in the South America Seed Market

The South America seed market faces several challenges. Regulatory hurdles, including lengthy approval processes and varying regulations across different countries, can hinder the introduction of new seed varieties and technologies. Supply chain disruptions, due to factors such as logistical bottlenecks and climate-related events, can affect seed availability and prices. Intense competition among established players and the emergence of new entrants contribute to price pressures. Furthermore, price volatility of agricultural commodities and fluctuating currency exchange rates affect profitability for seed companies. These factors impact the market’s growth potential and require careful management.

Future Opportunities in South America Seed Market

The South America seed market offers significant opportunities for growth. The increasing demand for sustainably produced food creates opportunities for the development and marketing of organic and bio-based seed varieties. Advancements in precision agriculture and digital technologies will allow for more efficient seed management and tailored crop solutions. Expanding into new markets within South America, focusing on underserved regions with high agricultural potential, can open up new avenues for growth. Furthermore, there is a great potential in developing specialized seed varieties tailored to specific regional conditions and consumer demands.

Major Players in the South America Seed Market Ecosystem

- Sakata Seeds Corporation

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- DLF

- Bayer AG

- BASF SE

- Groupe Limagrain

- KWS SAAT SE & Co KGaA

- Advanta Seeds - UPL

- Syngenta Group

- Corteva Agriscience

Key Developments in South America Seed Market Industry

- July 2023: BASF expanded its Xitavo soybean seed portfolio with 11 new high-yielding varieties for the 2024 growing season, featuring Enlist E3 technology. This expansion strengthens BASF's position in the soybean seed market and addresses the growing need for weed control solutions.

- May 2023: Advanta Seeds partnered with Embrapa to develop hybrid canola seeds with nematode management potential. This collaboration enhances the resilience of canola crops and improves yields, contributing to improved crop production and farmer income.

- April 2023: Syngenta Seeds and Ginkgo Bioworks collaborated to develop new traits for next-generation seed technology. This partnership leverages biotechnology to create healthier and more resilient crops, contributing to long-term sustainability in agriculture.

Strategic South America Seed Market Forecast

The South America seed market is poised for continued growth, driven by several factors. Increasing investment in agricultural research and development, along with the adoption of advanced technologies, will lead to the development of improved seed varieties with enhanced traits. Rising consumer demand for sustainably produced food will fuel the growth of organic and bio-based seed options. Government initiatives supporting agricultural modernization and infrastructure development will further stimulate market expansion. These factors suggest a promising outlook for the South America seed market, with significant opportunities for growth and innovation in the coming years.

South America Seed Market Segmentation

-

1. Breeding Technology

-

1.1. Hybrids

- 1.1.1. Non-Transgenic Hybrids

- 1.1.2. Herbicide Tolerant Hybrids

- 1.1.3. Insect Resistant Hybrids

- 1.1.4. Other Traits

- 1.2. Open Pollinated Varieties & Hybrid Derivatives

-

1.1. Hybrids

-

2. Cultivation Mechanism

- 2.1. Open Field

- 2.2. Protected Cultivation

-

3. Crop Type

-

3.1. Row Crops

-

3.1.1. Fiber Crops

- 3.1.1.1. Cotton

- 3.1.1.2. Other Fiber Crops

-

3.1.2. Forage Crops

- 3.1.2.1. Alfalfa

- 3.1.2.2. Forage Corn

- 3.1.2.3. Forage Sorghum

- 3.1.2.4. Other Forage Crops

-

3.1.3. Grains & Cereals

- 3.1.3.1. Rice

- 3.1.3.2. Wheat

- 3.1.3.3. Other Grains & Cereals

-

3.1.4. Oilseeds

- 3.1.4.1. Canola, Rapeseed & Mustard

- 3.1.4.2. Soybean

- 3.1.4.3. Sunflower

- 3.1.4.4. Other Oilseeds

- 3.1.5. Pulses

-

3.1.1. Fiber Crops

-

3.2. Vegetables

-

3.2.1. Brassicas

- 3.2.1.1. Cabbage

- 3.2.1.2. Carrot

- 3.2.1.3. Cauliflower & Broccoli

- 3.2.1.4. Other Brassicas

-

3.2.2. Cucurbits

- 3.2.2.1. Cucumber & Gherkin

- 3.2.2.2. Pumpkin & Squash

- 3.2.2.3. Other Cucurbits

-

3.2.3. Roots & Bulbs

- 3.2.3.1. Garlic

- 3.2.3.2. Onion

- 3.2.3.3. Potato

- 3.2.3.4. Other Roots & Bulbs

-

3.2.4. Solanaceae

- 3.2.4.1. Chilli

- 3.2.4.2. Eggplant

- 3.2.4.3. Tomato

- 3.2.4.4. Other Solanaceae

-

3.2.5. Unclassified Vegetables

- 3.2.5.1. Asparagus

- 3.2.5.2. Lettuce

- 3.2.5.3. Okra

- 3.2.5.4. Peas

- 3.2.5.5. Spinach

- 3.2.5.6. Other Unclassified Vegetables

-

3.2.1. Brassicas

-

3.1. Row Crops

-

4. Breeding Technology

-

4.1. Hybrids

- 4.1.1. Non-Transgenic Hybrids

- 4.1.2. Herbicide Tolerant Hybrids

- 4.1.3. Insect Resistant Hybrids

- 4.1.4. Other Traits

- 4.2. Open Pollinated Varieties & Hybrid Derivatives

-

4.1. Hybrids

-

5. Cultivation Mechanism

- 5.1. Open Field

- 5.2. Protected Cultivation

-

6. Crop Type

-

6.1. Row Crops

-

6.1.1. Fiber Crops

- 6.1.1.1. Cotton

- 6.1.1.2. Other Fiber Crops

-

6.1.2. Forage Crops

- 6.1.2.1. Alfalfa

- 6.1.2.2. Forage Corn

- 6.1.2.3. Forage Sorghum

- 6.1.2.4. Other Forage Crops

-

6.1.3. Grains & Cereals

- 6.1.3.1. Rice

- 6.1.3.2. Wheat

- 6.1.3.3. Other Grains & Cereals

-

6.1.4. Oilseeds

- 6.1.4.1. Canola, Rapeseed & Mustard

- 6.1.4.2. Soybean

- 6.1.4.3. Sunflower

- 6.1.4.4. Other Oilseeds

- 6.1.5. Pulses

-

6.1.1. Fiber Crops

-

6.2. Vegetables

-

6.2.1. Brassicas

- 6.2.1.1. Cabbage

- 6.2.1.2. Carrot

- 6.2.1.3. Cauliflower & Broccoli

- 6.2.1.4. Other Brassicas

-

6.2.2. Cucurbits

- 6.2.2.1. Cucumber & Gherkin

- 6.2.2.2. Pumpkin & Squash

- 6.2.2.3. Other Cucurbits

-

6.2.3. Roots & Bulbs

- 6.2.3.1. Garlic

- 6.2.3.2. Onion

- 6.2.3.3. Potato

- 6.2.3.4. Other Roots & Bulbs

-

6.2.4. Solanaceae

- 6.2.4.1. Chilli

- 6.2.4.2. Eggplant

- 6.2.4.3. Tomato

- 6.2.4.4. Other Solanaceae

-

6.2.5. Unclassified Vegetables

- 6.2.5.1. Asparagus

- 6.2.5.2. Lettuce

- 6.2.5.3. Okra

- 6.2.5.4. Peas

- 6.2.5.5. Spinach

- 6.2.5.6. Other Unclassified Vegetables

-

6.2.1. Brassicas

-

6.1. Row Crops

South America Seed Market Segmentation By Geography

-

1. South America

- 1.1. Brazil

- 1.2. Argentina

- 1.3. Chile

- 1.4. Colombia

- 1.5. Peru

- 1.6. Venezuela

- 1.7. Ecuador

- 1.8. Bolivia

- 1.9. Paraguay

- 1.10. Uruguay

South America Seed Market Regional Market Share

Geographic Coverage of South America Seed Market

South America Seed Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.1.1. Hybrids

- 5.1.1.1. Non-Transgenic Hybrids

- 5.1.1.2. Herbicide Tolerant Hybrids

- 5.1.1.3. Insect Resistant Hybrids

- 5.1.1.4. Other Traits

- 5.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1. Hybrids

- 5.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.2.1. Open Field

- 5.2.2. Protected Cultivation

- 5.3. Market Analysis, Insights and Forecast - by Crop Type

- 5.3.1. Row Crops

- 5.3.1.1. Fiber Crops

- 5.3.1.1.1. Cotton

- 5.3.1.1.2. Other Fiber Crops

- 5.3.1.2. Forage Crops

- 5.3.1.2.1. Alfalfa

- 5.3.1.2.2. Forage Corn

- 5.3.1.2.3. Forage Sorghum

- 5.3.1.2.4. Other Forage Crops

- 5.3.1.3. Grains & Cereals

- 5.3.1.3.1. Rice

- 5.3.1.3.2. Wheat

- 5.3.1.3.3. Other Grains & Cereals

- 5.3.1.4. Oilseeds

- 5.3.1.4.1. Canola, Rapeseed & Mustard

- 5.3.1.4.2. Soybean

- 5.3.1.4.3. Sunflower

- 5.3.1.4.4. Other Oilseeds

- 5.3.1.5. Pulses

- 5.3.1.1. Fiber Crops

- 5.3.2. Vegetables

- 5.3.2.1. Brassicas

- 5.3.2.1.1. Cabbage

- 5.3.2.1.2. Carrot

- 5.3.2.1.3. Cauliflower & Broccoli

- 5.3.2.1.4. Other Brassicas

- 5.3.2.2. Cucurbits

- 5.3.2.2.1. Cucumber & Gherkin

- 5.3.2.2.2. Pumpkin & Squash

- 5.3.2.2.3. Other Cucurbits

- 5.3.2.3. Roots & Bulbs

- 5.3.2.3.1. Garlic

- 5.3.2.3.2. Onion

- 5.3.2.3.3. Potato

- 5.3.2.3.4. Other Roots & Bulbs

- 5.3.2.4. Solanaceae

- 5.3.2.4.1. Chilli

- 5.3.2.4.2. Eggplant

- 5.3.2.4.3. Tomato

- 5.3.2.4.4. Other Solanaceae

- 5.3.2.5. Unclassified Vegetables

- 5.3.2.5.1. Asparagus

- 5.3.2.5.2. Lettuce

- 5.3.2.5.3. Okra

- 5.3.2.5.4. Peas

- 5.3.2.5.5. Spinach

- 5.3.2.5.6. Other Unclassified Vegetables

- 5.3.2.1. Brassicas

- 5.3.1. Row Crops

- 5.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.4.1. Hybrids

- 5.4.1.1. Non-Transgenic Hybrids

- 5.4.1.2. Herbicide Tolerant Hybrids

- 5.4.1.3. Insect Resistant Hybrids

- 5.4.1.4. Other Traits

- 5.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.4.1. Hybrids

- 5.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 5.5.1. Open Field

- 5.5.2. Protected Cultivation

- 5.6. Market Analysis, Insights and Forecast - by Crop Type

- 5.6.1. Row Crops

- 5.6.1.1. Fiber Crops

- 5.6.1.1.1. Cotton

- 5.6.1.1.2. Other Fiber Crops

- 5.6.1.2. Forage Crops

- 5.6.1.2.1. Alfalfa

- 5.6.1.2.2. Forage Corn

- 5.6.1.2.3. Forage Sorghum

- 5.6.1.2.4. Other Forage Crops

- 5.6.1.3. Grains & Cereals

- 5.6.1.3.1. Rice

- 5.6.1.3.2. Wheat

- 5.6.1.3.3. Other Grains & Cereals

- 5.6.1.4. Oilseeds

- 5.6.1.4.1. Canola, Rapeseed & Mustard

- 5.6.1.4.2. Soybean

- 5.6.1.4.3. Sunflower

- 5.6.1.4.4. Other Oilseeds

- 5.6.1.5. Pulses

- 5.6.1.1. Fiber Crops

- 5.6.2. Vegetables

- 5.6.2.1. Brassicas

- 5.6.2.1.1. Cabbage

- 5.6.2.1.2. Carrot

- 5.6.2.1.3. Cauliflower & Broccoli

- 5.6.2.1.4. Other Brassicas

- 5.6.2.2. Cucurbits

- 5.6.2.2.1. Cucumber & Gherkin

- 5.6.2.2.2. Pumpkin & Squash

- 5.6.2.2.3. Other Cucurbits

- 5.6.2.3. Roots & Bulbs

- 5.6.2.3.1. Garlic

- 5.6.2.3.2. Onion

- 5.6.2.3.3. Potato

- 5.6.2.3.4. Other Roots & Bulbs

- 5.6.2.4. Solanaceae

- 5.6.2.4.1. Chilli

- 5.6.2.4.2. Eggplant

- 5.6.2.4.3. Tomato

- 5.6.2.4.4. Other Solanaceae

- 5.6.2.5. Unclassified Vegetables

- 5.6.2.5.1. Asparagus

- 5.6.2.5.2. Lettuce

- 5.6.2.5.3. Okra

- 5.6.2.5.4. Peas

- 5.6.2.5.5. Spinach

- 5.6.2.5.6. Other Unclassified Vegetables

- 5.6.2.1. Brassicas

- 5.6.1. Row Crops

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. South America

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6. South America Seed Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.1.1. Hybrids

- 6.1.1.1. Non-Transgenic Hybrids

- 6.1.1.2. Herbicide Tolerant Hybrids

- 6.1.1.3. Insect Resistant Hybrids

- 6.1.1.4. Other Traits

- 6.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.1.1. Hybrids

- 6.2. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.2.1. Open Field

- 6.2.2. Protected Cultivation

- 6.3. Market Analysis, Insights and Forecast - by Crop Type

- 6.3.1. Row Crops

- 6.3.1.1. Fiber Crops

- 6.3.1.1.1. Cotton

- 6.3.1.1.2. Other Fiber Crops

- 6.3.1.2. Forage Crops

- 6.3.1.2.1. Alfalfa

- 6.3.1.2.2. Forage Corn

- 6.3.1.2.3. Forage Sorghum

- 6.3.1.2.4. Other Forage Crops

- 6.3.1.3. Grains & Cereals

- 6.3.1.3.1. Rice

- 6.3.1.3.2. Wheat

- 6.3.1.3.3. Other Grains & Cereals

- 6.3.1.4. Oilseeds

- 6.3.1.4.1. Canola, Rapeseed & Mustard

- 6.3.1.4.2. Soybean

- 6.3.1.4.3. Sunflower

- 6.3.1.4.4. Other Oilseeds

- 6.3.1.5. Pulses

- 6.3.1.1. Fiber Crops

- 6.3.2. Vegetables

- 6.3.2.1. Brassicas

- 6.3.2.1.1. Cabbage

- 6.3.2.1.2. Carrot

- 6.3.2.1.3. Cauliflower & Broccoli

- 6.3.2.1.4. Other Brassicas

- 6.3.2.2. Cucurbits

- 6.3.2.2.1. Cucumber & Gherkin

- 6.3.2.2.2. Pumpkin & Squash

- 6.3.2.2.3. Other Cucurbits

- 6.3.2.3. Roots & Bulbs

- 6.3.2.3.1. Garlic

- 6.3.2.3.2. Onion

- 6.3.2.3.3. Potato

- 6.3.2.3.4. Other Roots & Bulbs

- 6.3.2.4. Solanaceae

- 6.3.2.4.1. Chilli

- 6.3.2.4.2. Eggplant

- 6.3.2.4.3. Tomato

- 6.3.2.4.4. Other Solanaceae

- 6.3.2.5. Unclassified Vegetables

- 6.3.2.5.1. Asparagus

- 6.3.2.5.2. Lettuce

- 6.3.2.5.3. Okra

- 6.3.2.5.4. Peas

- 6.3.2.5.5. Spinach

- 6.3.2.5.6. Other Unclassified Vegetables

- 6.3.2.1. Brassicas

- 6.3.1. Row Crops

- 6.4. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.4.1. Hybrids

- 6.4.1.1. Non-Transgenic Hybrids

- 6.4.1.2. Herbicide Tolerant Hybrids

- 6.4.1.3. Insect Resistant Hybrids

- 6.4.1.4. Other Traits

- 6.4.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.4.1. Hybrids

- 6.5. Market Analysis, Insights and Forecast - by Cultivation Mechanism

- 6.5.1. Open Field

- 6.5.2. Protected Cultivation

- 6.6. Market Analysis, Insights and Forecast - by Crop Type

- 6.6.1. Row Crops

- 6.6.1.1. Fiber Crops

- 6.6.1.1.1. Cotton

- 6.6.1.1.2. Other Fiber Crops

- 6.6.1.2. Forage Crops

- 6.6.1.2.1. Alfalfa

- 6.6.1.2.2. Forage Corn

- 6.6.1.2.3. Forage Sorghum

- 6.6.1.2.4. Other Forage Crops

- 6.6.1.3. Grains & Cereals

- 6.6.1.3.1. Rice

- 6.6.1.3.2. Wheat

- 6.6.1.3.3. Other Grains & Cereals

- 6.6.1.4. Oilseeds

- 6.6.1.4.1. Canola, Rapeseed & Mustard

- 6.6.1.4.2. Soybean

- 6.6.1.4.3. Sunflower

- 6.6.1.4.4. Other Oilseeds

- 6.6.1.5. Pulses

- 6.6.1.1. Fiber Crops

- 6.6.2. Vegetables

- 6.6.2.1. Brassicas

- 6.6.2.1.1. Cabbage

- 6.6.2.1.2. Carrot

- 6.6.2.1.3. Cauliflower & Broccoli

- 6.6.2.1.4. Other Brassicas

- 6.6.2.2. Cucurbits

- 6.6.2.2.1. Cucumber & Gherkin

- 6.6.2.2.2. Pumpkin & Squash

- 6.6.2.2.3. Other Cucurbits

- 6.6.2.3. Roots & Bulbs

- 6.6.2.3.1. Garlic

- 6.6.2.3.2. Onion

- 6.6.2.3.3. Potato

- 6.6.2.3.4. Other Roots & Bulbs

- 6.6.2.4. Solanaceae

- 6.6.2.4.1. Chilli

- 6.6.2.4.2. Eggplant

- 6.6.2.4.3. Tomato

- 6.6.2.4.4. Other Solanaceae

- 6.6.2.5. Unclassified Vegetables

- 6.6.2.5.1. Asparagus

- 6.6.2.5.2. Lettuce

- 6.6.2.5.3. Okra

- 6.6.2.5.4. Peas

- 6.6.2.5.5. Spinach

- 6.6.2.5.6. Other Unclassified Vegetables

- 6.6.2.1. Brassicas

- 6.6.1. Row Crops

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sakata Seeds Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 DLF

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Bayer AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 BASF SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Groupe Limagrain

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 KWS SAAT SE & Co KGaA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Advanta Seeds - UPL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Syngenta Grou

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Corteva Agriscience

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Sakata Seeds Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South America Seed Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South America Seed Market Share (%) by Company 2025

List of Tables

- Table 1: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 2: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 3: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 4: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 5: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 6: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 7: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 8: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 9: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 10: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 11: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 12: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 13: South America Seed Market Revenue Million Forecast, by Region 2020 & 2033

- Table 14: South America Seed Market Volume Kiloton Forecast, by Region 2020 & 2033

- Table 15: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 16: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 17: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 18: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 19: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 20: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 21: South America Seed Market Revenue Million Forecast, by Breeding Technology 2020 & 2033

- Table 22: South America Seed Market Volume Kiloton Forecast, by Breeding Technology 2020 & 2033

- Table 23: South America Seed Market Revenue Million Forecast, by Cultivation Mechanism 2020 & 2033

- Table 24: South America Seed Market Volume Kiloton Forecast, by Cultivation Mechanism 2020 & 2033

- Table 25: South America Seed Market Revenue Million Forecast, by Crop Type 2020 & 2033

- Table 26: South America Seed Market Volume Kiloton Forecast, by Crop Type 2020 & 2033

- Table 27: South America Seed Market Revenue Million Forecast, by Country 2020 & 2033

- Table 28: South America Seed Market Volume Kiloton Forecast, by Country 2020 & 2033

- Table 29: Brazil South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Brazil South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 31: Argentina South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Argentina South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 33: Chile South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Chile South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 35: Colombia South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Colombia South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 37: Peru South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Peru South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 39: Venezuela South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Venezuela South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 41: Ecuador South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Ecuador South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 43: Bolivia South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Bolivia South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 45: Paraguay South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Paraguay South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

- Table 47: Uruguay South America Seed Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Uruguay South America Seed Market Volume (Kiloton) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America Seed Market?

The projected CAGR is approximately 3.40%.

2. Which companies are prominent players in the South America Seed Market?

Key companies in the market include Sakata Seeds Corporation, Rijk Zwaan Zaadteelt en Zaadhandel BV, DLF, Bayer AG, BASF SE, Groupe Limagrain, KWS SAAT SE & Co KGaA, Advanta Seeds - UPL, Syngenta Grou, Corteva Agriscience.

3. What are the main segments of the South America Seed Market?

The market segments include Breeding Technology, Cultivation Mechanism, Crop Type, Breeding Technology, Cultivation Mechanism, Crop Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Seed Treatment As A Solution To Enhance Yield; Growing Awareness For Seed Treatment Among The Farmers; Rising Trend Of Organic Farming.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Limitations Across Farm-Level Seed Treatment; Rising Environmental Concerns.

8. Can you provide examples of recent developments in the market?

July 2023: BASF expanded its Xitavo soybean seed portfolio with the addition of its 11 new high-yielding varieties for the 2024 growing season, featuring the Enlist E3 technology to combat difficult weeds.May 2023: Advanta Seeds made an agreement with Embrapa (Brazilian Agricultural Research Corporation) to develop hybrid canola seeds with nematode management potential.April 2023: Syngenta Seeds and Ginkgo Bioworks collaborated to develop new traits for the next generation of seed technology to produce healthier and more resilient crops.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America Seed Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America Seed Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America Seed Market?

To stay informed about further developments, trends, and reports in the South America Seed Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence