Key Insights

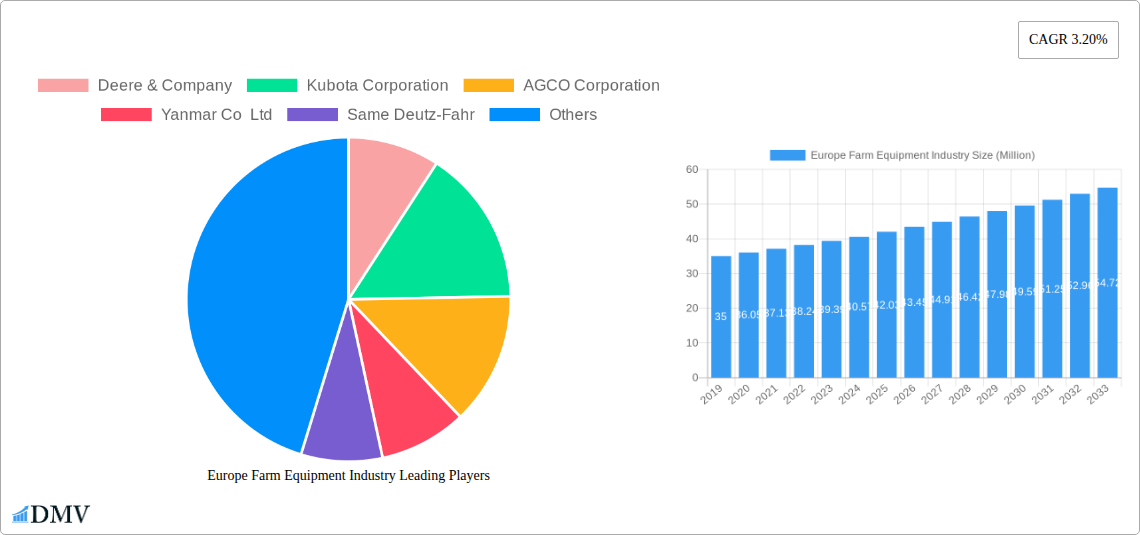

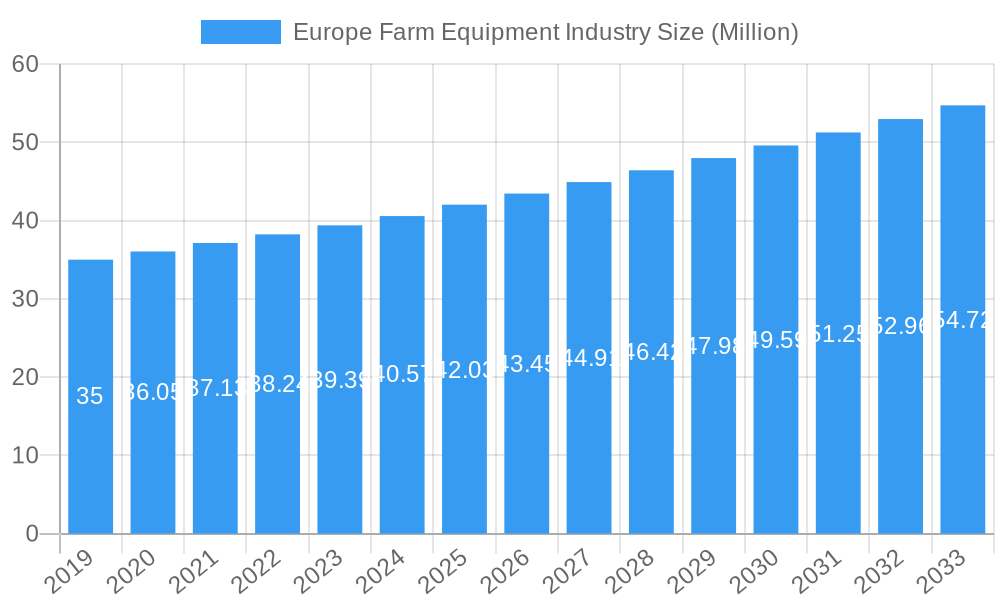

The European Farm Equipment Industry is poised for steady expansion, projected to reach $42.03 million by 2025, growing at a Compound Annual Growth Rate (CAGR) of 3.20% through 2033. This robust growth is primarily propelled by the increasing adoption of advanced agricultural technologies and machinery designed to enhance efficiency and productivity on farms across the continent. Key drivers include the persistent need for greater mechanization to address labor shortages, the growing demand for precision agriculture solutions that optimize resource utilization (such as water, fertilizers, and pesticides), and the ongoing consolidation of farms, leading to larger operations requiring more sophisticated equipment. Furthermore, government initiatives and subsidies aimed at modernizing agricultural practices and promoting sustainable farming methods are significantly bolstering the market. The industry is also witnessing a strong trend towards the development and integration of smart farming technologies, including GPS-guided tractors, automated harvesters, and data-driven analytics platforms, all of which contribute to higher yields and reduced operational costs.

Europe Farm Equipment Industry Market Size (In Million)

Despite the positive outlook, the market faces certain restraints. The high initial investment cost associated with acquiring advanced farm machinery can be a significant barrier for small and medium-sized agricultural enterprises. Additionally, the complex maintenance and repair requirements of sophisticated equipment, coupled with the need for skilled operators, can also pose challenges. Regulatory hurdles related to emissions and environmental standards, while driving innovation, can also add to production costs and complexity for manufacturers. The market segmentation reveals a detailed breakdown across production, consumption, imports, exports, and price trends, offering a comprehensive view of market dynamics. Major players like Deere & Company, Kubota Corporation, and AGCO Corporation are actively investing in research and development to introduce innovative products and expand their market reach within Europe, particularly focusing on countries like Germany, France, and the United Kingdom.

Europe Farm Equipment Industry Company Market Share

Europe Farm Equipment Industry Market: Comprehensive Analysis & Forecast 2019–2033

This in-depth report offers a vital analysis of the Europe Farm Equipment Industry, providing stakeholders with critical insights into market dynamics, growth trajectories, and future opportunities. Covering the period from 2019 to 2033, with a base year of 2025, this report is indispensable for understanding the evolving landscape of agricultural machinery in Europe. We meticulously dissect production, consumption, import/export markets, price trends, and industry developments, equipping you with the data-driven intelligence needed to make informed strategic decisions in this high-growth sector. Leverage our detailed segmentation and player analysis to identify competitive advantages and navigate market complexities.

Europe Farm Equipment Industry Market Composition & Trends

The Europe Farm Equipment Industry is characterized by a moderately concentrated market, with key players like Deere & Company, CNH Industrial NV, and AGCO Corporation holding significant market share. Innovation remains a primary catalyst, driven by the demand for precision agriculture, automation, and sustainable farming practices. Regulatory landscapes, particularly those related to environmental standards and emissions, are increasingly shaping product development and market entry. While substitute products exist in the form of rental services and older machinery, the drive for efficiency and yield optimization favors advanced equipment. End-user profiles are diverse, ranging from large-scale commercial farms to smaller family-owned operations, each with unique equipment needs. Mergers and acquisitions (M&A) activities, though not always publicly disclosed in value, play a crucial role in market consolidation and technology integration. For instance, strategic partnerships and smaller acquisitions aim to bolster product portfolios and expand market reach, contributing to an estimated total M&A deal value in the range of XXX Million. The market share distribution sees established manufacturers commanding substantial portions, with emerging players carving out niches in specialized equipment.

Europe Farm Equipment Industry Industry Evolution

The evolution of the Europe Farm Equipment Industry is a compelling narrative of technological advancement and adaptation to changing agricultural paradigms. Over the historical period (2019-2024) and into the estimated year of 2025, the industry has witnessed a consistent growth trajectory, driven by an increasing need for enhanced productivity and efficiency in farming operations. This growth is intricately linked to the adoption of precision agriculture technologies, which have moved from niche applications to mainstream integration. Smart farming solutions, including GPS-guided tractors, automated steering systems, and sensor-equipped machinery, are becoming standard, contributing to an estimated annual growth rate of X.XX%.

Consumer demand has shifted significantly towards equipment that offers greater fuel efficiency, reduced environmental impact, and enhanced operator comfort and safety. This is partly due to stringent European Union regulations and a growing awareness among farmers about sustainable practices. The integration of IoT and data analytics into farm machinery allows for real-time monitoring, predictive maintenance, and optimized resource management, leading to significant cost savings and improved yields. For example, the adoption of variable rate application technology for fertilizers and pesticides has seen a substantial increase, estimated at XX% in the last two years alone, directly impacting the demand for sophisticated sprayers and cultivators.

Technological advancements are not limited to core functionalities. The development of electric and hybrid farm equipment is gaining traction, driven by environmental concerns and the desire to reduce operational costs. Furthermore, the automation of complex tasks, such as harvesting and weeding, is becoming increasingly feasible with the advent of AI-powered robotics and advanced sensor arrays. This trend is expected to accelerate, addressing labor shortages and improving the precision of agricultural tasks. The overall market growth is further propelled by government subsidies and incentives aimed at modernizing agricultural practices across member states. The estimated market size for the Europe Farm Equipment Industry in 2025 is projected to reach XXX Million, reflecting the robust performance and ongoing innovation within the sector.

Leading Regions, Countries, or Segments in Europe Farm Equipment Industry

The dominance within the Europe Farm Equipment Industry is multifaceted, with several regions and segments showcasing exceptional performance. From a Production Analysis perspective, Germany and France emerge as leading manufacturing hubs, leveraging strong industrial bases and technological expertise. These countries benefit from a robust ecosystem of component suppliers and skilled labor, enabling them to produce high-quality agricultural machinery for both domestic and export markets. Investment trends in these regions are consistently high, with significant capital flowing into R&D and advanced manufacturing facilities.

In terms of Consumption Analysis, Western European countries, including Germany, France, the UK, and the Netherlands, represent the largest markets. This is driven by a combination of large-scale agricultural operations, high levels of mechanization, and a strong emphasis on precision farming. Regulatory support for modernizing agricultural practices and subsidies for adopting advanced technologies further fuel consumption. For instance, France's national agricultural policy often includes provisions for financial aid towards purchasing new, efficient farm equipment.

The Import Market Analysis (Value & Volume) reveals significant trade flows into Europe, particularly for specialized machinery and components not manufactured locally. Countries like the Netherlands, with its extensive agricultural trade networks, act as crucial import gateways. The value of imports is projected to reach XXX Million in 2025, with volumes driven by the demand for tractors, combine harvesters, and advanced implements.

Conversely, the Export Market Analysis (Value & Volume) highlights Europe's strong position as a global supplier of farm equipment. Germany and Italy are key exporters, with their products renowned for quality and innovation. The export market is expected to generate revenues of XXX Million in 2025. Key drivers for this export dominance include the high technological content of European machinery and the ability to meet stringent international quality standards.

The Price Trend Analysis indicates a steady upward trend, influenced by raw material costs, technological advancements, and inflation. However, the increasing adoption of high-efficiency, precision equipment often justifies these higher price points through improved long-term operational economics. The most dominant segment within the industry, in terms of revenue generation, is Tractors, followed closely by Combine Harvesters and Tillage Equipment, reflecting the foundational needs of modern agriculture. Investment trends in these core segments remain robust, supported by continuous product development and market demand.

Europe Farm Equipment Industry Product Innovations

The Europe Farm Equipment Industry is a hotbed of innovation, consistently delivering advanced machinery designed to boost efficiency and sustainability. Recent breakthroughs include the development of autonomous tractors capable of performing complex field operations with minimal human intervention, utilizing sophisticated GPS and sensor technology. Furthermore, smart harvesters are now equipped with real-time yield monitoring and grain quality analysis systems, providing farmers with invaluable data for immediate decision-making. Innovations in material science are leading to lighter yet more durable components, enhancing fuel efficiency and reducing soil compaction. The integration of advanced AI and machine learning algorithms is enabling predictive maintenance for equipment, minimizing downtime and optimizing operational longevity. These advancements not only improve performance metrics like yield by an estimated X% and fuel efficiency by X%, but also contribute to a more sustainable and profitable farming future.

Propelling Factors for Europe Farm Equipment Industry Growth

Several key factors are propelling the growth of the Europe Farm Equipment Industry.

- Technological Advancements: The relentless pursuit of precision agriculture, automation, and smart farming solutions drives demand for cutting-edge machinery. Innovations in AI, IoT, and robotics are transforming farming practices, enhancing productivity and efficiency.

- Increasing Demand for Food Security: A growing global population necessitates higher agricultural output, creating sustained demand for modern, efficient farm equipment that can maximize yields.

- Sustainable Farming Initiatives: Growing environmental consciousness and stringent regulations encourage the adoption of eco-friendly machinery, such as those with lower emissions and improved fuel efficiency. Government incentives further support this transition.

- Labor Shortages in Agriculture: Automation and advanced machinery are increasingly being adopted to mitigate the impact of a shrinking agricultural workforce, ensuring continuity and efficiency in farm operations.

- Farm Modernization and Consolidation: Larger, more efficient farms require advanced equipment to manage vast landholdings effectively, leading to increased investment in sophisticated machinery.

Obstacles in the Europe Farm Equipment Industry Market

Despite its growth, the Europe Farm Equipment Industry faces several significant obstacles.

- High Initial Investment Costs: The advanced technology embedded in modern farm equipment translates to substantial upfront costs, which can be a deterrent for small and medium-sized farmers.

- Regulatory Complexities: Navigating diverse and evolving environmental, safety, and emissions regulations across different European countries can be challenging and costly for manufacturers.

- Supply Chain Disruptions: Global supply chain vulnerabilities, as witnessed in recent years, can lead to component shortages, production delays, and increased manufacturing costs, impacting product availability and pricing.

- Skills Gap in Maintenance and Operation: The complexity of advanced machinery requires specialized skills for operation and maintenance. A shortage of qualified technicians can hinder the adoption and effective utilization of new equipment.

- Economic Volatility and Farm Profitability: Fluctuations in agricultural commodity prices and overall farm profitability can directly impact farmers' willingness and ability to invest in new machinery.

Future Opportunities in Europe Farm Equipment Industry

The Europe Farm Equipment Industry is ripe with emerging opportunities.

- Expansion of Autonomous and Robotic Solutions: The development and widespread adoption of fully autonomous tractors and specialized robotic systems for tasks like weeding and harvesting represent a significant growth area.

- Electrification and Alternative Powertrains: The demand for electric and hybrid farm equipment is set to surge, driven by environmental regulations and a desire for lower operating costs.

- Data-Driven Farming Services: Opportunities lie in integrating farm equipment with advanced data analytics platforms, offering farmers insights into crop management, soil health, and operational efficiency.

- Circular Economy and Sustainable Manufacturing: Developing equipment with longer lifespans, easier repairability, and utilizing recycled materials presents an opportunity for environmentally conscious manufacturers.

- Emerging Markets within Europe: While Western Europe is mature, Eastern European agricultural sectors are undergoing modernization, presenting a growing demand for advanced farm machinery.

Major Players in the Europe Farm Equipment Industry Ecosystem

- Deere & Company

- Kubota Corporation

- AGCO Corporation

- Yanmar Co Ltd

- Same Deutz-Fahr

- CNH Industrial NV

- CLAAS KGaA mbH

- Kuhn Group

- Lely France

Key Developments in Europe Farm Equipment Industry Industry

- November 2023: CNH Industrial NV unveiled the CR11 New Holland combine at Agritechnica '23. Its 775-horsepower C16 engine powers 2x24-inch rotors, while the 567-bushel (20,000-liter) grain tank ensures ample storage capacity. With a rapid six bushels (210 liters) per second unload rate, the CR11 minimizes grain loss.

- November 2023: Yanmar Co. Ltd partnered with International Tractors Limited (ITL) to strengthen the product portfolio, network & service capabilities to serve customer needs. Through the extensive network of both companies, this strategic partnership was poised to broaden the market reach for both brands substantially. ITL and Yanmar aimed to provide unparalleled customer service & technologically advanced products across Europe by harnessing their collective expertise and resources.

- September 2023: John Deere and Yara partnered and improved fertilizer efficiency and crop yields through a combination of Yara’s agronomic expertise and John Deere’s Precision Technology. This collaboration provided farmers with data-driven recommendations, optimized nutrient use, and maximized productivity.

Strategic Europe Farm Equipment Industry Market Forecast

The strategic forecast for the Europe Farm Equipment Industry is exceptionally promising, driven by an unwavering commitment to innovation and sustainability. The continued integration of digital technologies, including AI, IoT, and automation, will redefine agricultural efficiency, leading to significant improvements in yield and resource management. The electrification of machinery, spurred by stringent environmental regulations and increasing consumer demand for eco-friendly solutions, presents a substantial growth opportunity. Furthermore, the ongoing modernization of agricultural practices across the continent, coupled with governmental support and farm consolidation trends, will sustain robust demand for advanced machinery. Investments in R&D for autonomous farming solutions and data-driven insights will unlock new revenue streams and enhance competitive advantages, solidifying Europe's position as a global leader in agricultural mechanization. The market is poised for sustained growth, driven by these pivotal factors and an ever-evolving agricultural landscape.

Europe Farm Equipment Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Farm Equipment Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Farm Equipment Industry Regional Market Share

Geographic Coverage of Europe Farm Equipment Industry

Europe Farm Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 6. Europe Farm Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deere & Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kubota Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AGCO Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yanmar Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Same Deutz-Fahr

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CNH Industrial NV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 CLAAS KGaA mbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kuhn Group*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Lely France

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Deere & Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Farm Equipment Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Farm Equipment Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Farm Equipment Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Farm Equipment Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Farm Equipment Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Farm Equipment Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Farm Equipment Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Farm Equipment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Europe Farm Equipment Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Farm Equipment Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Farm Equipment Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Farm Equipment Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Farm Equipment Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Farm Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Farm Equipment Industry?

The projected CAGR is approximately 3.20%.

2. Which companies are prominent players in the Europe Farm Equipment Industry?

Key companies in the market include Deere & Company, Kubota Corporation, AGCO Corporation, Yanmar Co Ltd, Same Deutz-Fahr, CNH Industrial NV, CLAAS KGaA mbH, Kuhn Group*List Not Exhaustive, Lely France.

3. What are the main segments of the Europe Farm Equipment Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.03 Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Shortage of Skilled Labor.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

November 2023: CNH Industrial NV unveiled CR11 New Holland combine at Agritechnica '23. Its 775-horsepower C16 engine powers 2x24-inch rotors, while the 567-bushel (20,000-liter) grain tank ensures ample storage capacity. With a rapid six bushels (210 liters) per second unload rate, the CR11 minimizes grain loss.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Farm Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Farm Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Farm Equipment Industry?

To stay informed about further developments, trends, and reports in the Europe Farm Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence