Key Insights

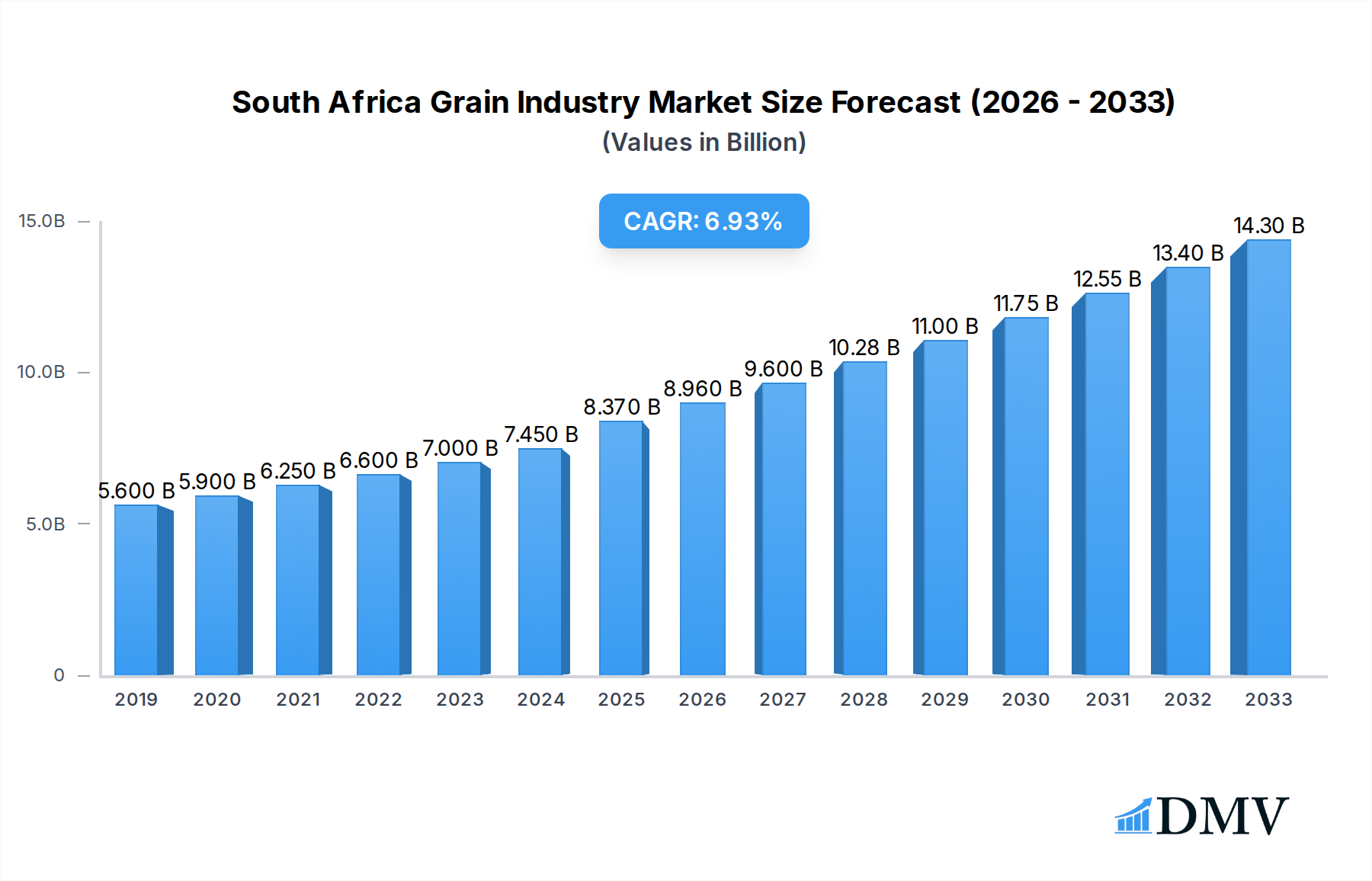

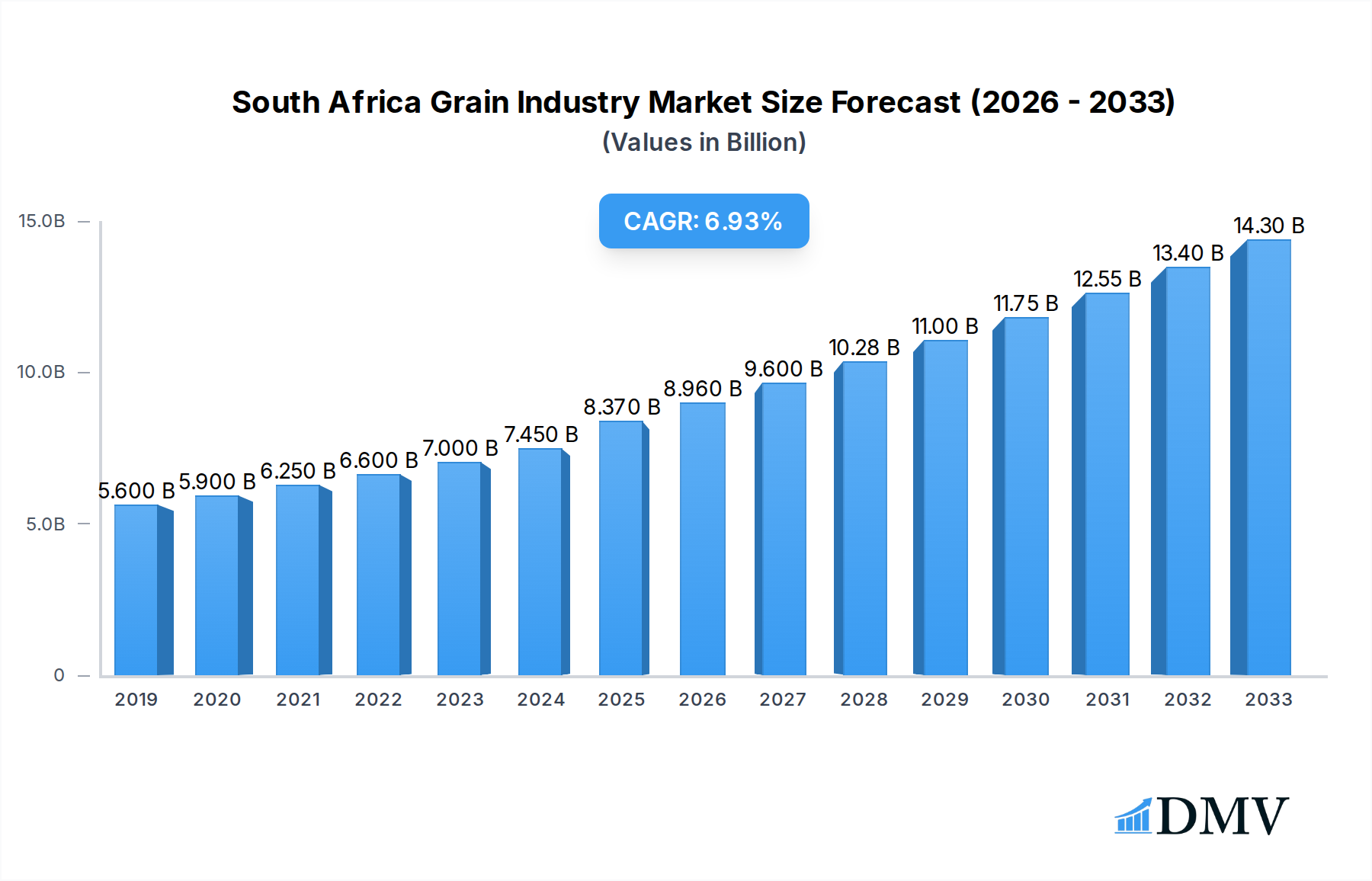

The South Africa Grain Industry is poised for significant expansion, with an estimated market size of 8370 million in 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of 7.00% through 2033. This growth is propelled by a confluence of factors, including increasing domestic food demand driven by population growth and evolving dietary preferences, coupled with a rising emphasis on food security within the nation. Furthermore, advancements in agricultural technology, such as improved seed varieties and precision farming techniques, are enhancing yields and efficiency, thereby contributing to market expansion. The demand for key grains like maize, wheat, and rice remains consistently high, underpinning the industry's stable trajectory.

South Africa Grain Industry Market Size (In Billion)

The market's upward momentum is further bolstered by favorable government policies aimed at supporting agricultural production and export initiatives. However, the industry faces certain headwinds. Volatile weather patterns and climate change pose a significant threat to crop yields and consistency, impacting supply chains and pricing. Fluctuations in global commodity prices and increasing competition from international markets also present challenges. Despite these restraints, the industry's diversification into value-added products and the growing adoption of sustainable farming practices are expected to mitigate risks and foster sustained growth. Key players like OVK, Senwes, and Kaap Agri are actively investing in innovation and expanding their operational footprints to capitalize on these evolving market dynamics.

South Africa Grain Industry Company Market Share

South Africa Grain Industry Market Composition & Trends

The South African grain industry, a vital contributor to the nation's food security and economy, exhibits a dynamic market composition influenced by robust growth trajectories and evolving stakeholder demands. Market concentration is notably influenced by key players such as OVK, Senwes, GWK, AFGRI, Kaap Agri, Grain SA, and BKB Ltd, each holding significant market share. Innovation catalysts range from precision agriculture technologies to the development of drought-resistant crop varieties, driving efficiency and yield improvements. The regulatory landscape, while generally supportive, navigates complex issues concerning land reform, trade policies, and food safety standards. Substitute products, though less prevalent for staple grains, include alternative protein sources and imported grains, posing a competitive factor. End-user profiles are diverse, encompassing food processors, animal feed manufacturers, and direct consumers, each with specific quality and price sensitivities. Merger and acquisition (M&A) activities are strategic, aimed at consolidating market presence and expanding value chains. For instance, M&A deal values in the historical period (2019-2024) are estimated to have reached XX Million, indicating active consolidation.

- Market Share Distribution: Dominant players like Senwes and AFGRI are estimated to hold combined market shares exceeding 50% in key segments like maize.

- M&A Activities: Strategic acquisitions and partnerships are observed among large agribusinesses aiming for vertical integration, with an estimated aggregate deal value of XX Million in the historical period.

- Innovation Trends: Focus on digital farming solutions, sustainable practices, and value-added grain processing products.

South Africa Grain Industry Industry Evolution

The South African grain industry has undergone a significant evolution, marked by consistent market growth trajectories and transformative technological advancements. Over the historical period from 2019 to 2024, the industry demonstrated resilience and adaptability, navigating global economic fluctuations and domestic challenges. The base year, 2025, serves as a pivotal point for assessing current market dynamics and future potential, with the forecast period extending to 2033. Shifting consumer demands, driven by increasing awareness of health, sustainability, and traceability, have compelled producers and processors to innovate. For example, the demand for organically grown grains and those with a reduced environmental footprint has seen a substantial uptick. Technological advancements have been a cornerstone of this evolution. The adoption of precision agriculture techniques, including GPS-guided machinery, drone-based crop monitoring, and data analytics for yield optimization, has become increasingly prevalent. These technologies contribute to enhanced resource management, reduced waste, and improved crop yields, with adoption rates in precision farming tools estimated to have grown by XX% annually during the historical period. Furthermore, advancements in seed technology, focusing on higher yields, disease resistance, and climate resilience, have played a critical role. The industry's growth has also been propelled by governmental support initiatives aimed at boosting local production and ensuring food security. The estimated Compound Annual Growth Rate (CAGR) for the South African grain market is projected to be XX% from 2025 to 2033, reflecting a steady expansion driven by both domestic consumption and export potential. The study period, encompassing 2019–2033, allows for a comprehensive analysis of long-term trends and the impact of various economic and environmental factors on the industry's sustained growth and adaptation.

Leading Regions, Countries, or Segments in South Africa Grain Industry

The South African grain industry's dominance is multifaceted, with specific regions and crop segments exhibiting exceptional performance and driving overall market growth. Among the key grain types, Maize: consistently emerges as the leading segment, both in terms of production volume and economic contribution. This dominance is particularly pronounced in regions like the Free State and North West provinces, which are the breadbaskets of South Africa, benefiting from favorable climatic conditions and fertile soils. The demand for maize is driven by its widespread use as a staple food, a critical ingredient in animal feed, and for industrial purposes like brewing and starch production.

- Maize Dominance Drivers:

- Favorable Climate & Soil: The high-yield potential in key agricultural provinces like the Free State and North West.

- Versatile Applications: Extensive use as a primary food source, animal feed, and industrial raw material.

- Government Support: Policies aimed at promoting maize production and export, contributing to an estimated XX% of the total grain output in the base year.

- Technological Integration: Increased adoption of advanced farming techniques leading to higher yields and improved quality.

Wheat: also holds significant importance, particularly in the Western Cape region, where specific agro-climatic conditions are conducive to its cultivation. While production volumes may be lower than maize, wheat plays a crucial role in the baking and food processing sectors, meeting the demand for bread, pasta, and other wheat-based products. The region's strong infrastructure, including port facilities for potential exports, further solidifies its standing.

- Wheat Importance:

- Regional Specialization: Western Cape's unique suitability for wheat cultivation.

- Food Industry Demand: Essential for the baking and food manufacturing sectors, supporting an estimated XX% of the nation's grain consumption.

- Research & Development: Continuous efforts to develop higher-yielding and disease-resistant wheat varieties.

Barley: finds its niche primarily in the Western Cape and some parts of the Eastern Cape. Its demand is largely driven by the brewing industry, making it a strategically important crop for the beverage sector. The market for barley has seen steady growth, influenced by the expansion of the craft beer and spirits market in South Africa.

- Barley Growth Factors:

- Brewing Industry Linkage: Direct correlation with the expansion of the domestic brewing and spirits market.

- Specialized Farming: Cultivation concentrated in regions with optimal conditions for quality malting barley.

- Export Potential: Growing interest in South African barley for international malting purposes.

Sorghum: and Rice: , while not produced in the same massive volumes as maize or wheat, are crucial for niche markets and dietary diversity. Sorghum is particularly important in drier regions and as a traditional food source, offering a resilient and nutritious option. Rice production in South Africa is more limited, with a significant portion being imported; however, localized efforts to increase domestic rice cultivation are underway, focusing on water-efficient varieties and sustainable farming practices.

- Sorghum & Rice Significance:

- Sorghum Resilience: Adapted to arid conditions, crucial for food security in challenging environments.

- Rice Development: Emerging focus on domestic production to reduce import reliance, targeting specific regions with water management capabilities.

- Nutritional Value: Both grains offer unique nutritional profiles, catering to diverse dietary needs.

The interplay between these segments and their respective regional strongholds creates a robust and diversified South African grain industry, with an estimated total market value of XX Million in the base year. The study period 2019–2033, including the forecast period 2025–2033, will provide critical insights into how these segments evolve and contribute to the overall market dynamics, influenced by factors such as climate change, technological adoption, and shifting consumer preferences.

South Africa Grain Industry Product Innovations

Product innovations within the South African grain industry are primarily focused on enhancing value, improving nutritional profiles, and promoting sustainability. Advancements in grain processing technologies have led to the development of fortified grain products, enriched with essential vitamins and minerals to combat nutritional deficiencies. For instance, companies are investing in biofortification techniques for maize to increase its vitamin A content. Furthermore, the industry is witnessing a surge in demand for gluten-free grain alternatives and specialized flour blends catering to evolving dietary needs and preferences. Innovations in packaging solutions are also gaining traction, with a focus on extending shelf life and reducing food waste. Performance metrics for these innovations include improved nutrient bioavailability, extended product usability, and reduced environmental impact, with new product launches estimated to contribute XX% to market growth in the forecast period.

Propelling Factors for South Africa Grain Industry Growth

The South African grain industry's growth is propelled by a confluence of technological advancements, supportive economic policies, and increasing demand for food products.

- Technological Advancements: The adoption of precision agriculture, including IoT-enabled farm management systems and advanced crop analytics, is enhancing yield efficiency and resource management.

- Economic Influences: A growing population and a burgeoning middle class are driving increased consumption of grain-based products and animal feed. Government initiatives promoting agricultural modernization and export incentives also play a crucial role.

- Regulatory Support: Policies aimed at improving food security, supporting smallholder farmers, and encouraging investment in the agricultural sector create a favorable business environment. For example, estimated government subsidies and support programs are projected to be in the range of XX Million annually.

Obstacles in the South Africa Grain Industry Market

Despite its growth potential, the South African grain industry faces several obstacles that could impede its progress.

- Regulatory Challenges: Complex land reform policies and inconsistent agricultural regulations can create uncertainty for investors and producers.

- Supply Chain Disruptions: Inefficient logistics, inadequate infrastructure, and climate-related events like droughts and floods can disrupt the supply chain, leading to price volatility and reduced availability.

- Competitive Pressures: Competition from imported grains, particularly in segments where domestic production is less competitive, exerts pressure on local producers. Additionally, fluctuating global commodity prices can impact profitability. The estimated financial impact of these disruptions on market growth is in the range of XX% reduction in projected gains.

Future Opportunities in South Africa Grain Industry

The future of the South African grain industry presents numerous opportunities for growth and innovation.

- New Markets: Expanding export markets, particularly within the African continent and to Asia, offers significant potential for revenue generation.

- Technological Adoption: Further integration of artificial intelligence and machine learning in farm management can unlock unprecedented levels of efficiency and predictive capabilities.

- Consumer Trends: Capitalizing on the growing demand for plant-based proteins and sustainable food products presents opportunities for value-added grain derivatives and alternative grain crops. Value-added products are expected to see a market expansion of XX% in the forecast period.

Major Players in the South Africa Grain Industry Ecosystem

- OVK

- Senwes

- GWK

- AFGRI

- Kaap Agri

- Grain SA

- BKB Ltd

Key Developments in South Africa Grain Industry Industry

- 2023/Ongoing: Increased investment in drought-resistant seed varieties and precision farming technology to mitigate climate change impacts.

- 2023/Q4: Launch of new fortified maize meal products by major food processors aimed at addressing malnutrition.

- 2024/Q1: Grain SA advocating for enhanced infrastructure development to improve logistics and reduce post-harvest losses.

- 2024/Q2: Expansion of contract farming initiatives to empower smallholder farmers and increase overall production.

- 2024/Q3: Strategic partnerships formed between technology providers and agribusinesses for digital transformation in agriculture.

Strategic South Africa Grain Industry Market Forecast

The strategic forecast for the South African grain industry indicates robust growth driven by increasing domestic consumption, export potential, and continued technological adoption. The base year 2025 marks a period of consolidation and technological integration, paving the way for sustained expansion through 2033. Key growth catalysts include the rising demand for animal feed to support the expanding livestock sector and the increasing preference for diversified and healthier grain products. Government support for agricultural modernization and private sector investment in value-added processing will further solidify the industry's trajectory. The forecast period is expected to witness an estimated market growth of XX%, reaching a projected market value of XX Million by 2033, driven by both volume expansion and an increase in higher-value processed grain products.

South Africa Grain Industry Segmentation

- 1. Maize

- 2. Barley

- 3. Sorghum

- 4. Rice

- 5. Wheat

- 6. Maize

- 7. Barley

- 8. Sorghum

- 9. Rice

- 10. Wheat

South Africa Grain Industry Segmentation By Geography

- 1. South Africa

South Africa Grain Industry Regional Market Share

Geographic Coverage of South Africa Grain Industry

South Africa Grain Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Maize

- 5.2. Market Analysis, Insights and Forecast - by Barley

- 5.3. Market Analysis, Insights and Forecast - by Sorghum

- 5.4. Market Analysis, Insights and Forecast - by Rice

- 5.5. Market Analysis, Insights and Forecast - by Wheat

- 5.6. Market Analysis, Insights and Forecast - by Maize

- 5.7. Market Analysis, Insights and Forecast - by Barley

- 5.8. Market Analysis, Insights and Forecast - by Sorghum

- 5.9. Market Analysis, Insights and Forecast - by Rice

- 5.10. Market Analysis, Insights and Forecast - by Wheat

- 5.11. Market Analysis, Insights and Forecast - by Region

- 5.11.1. South Africa

- 6. South Africa Grain Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Maize

- 6.2. Market Analysis, Insights and Forecast - by Barley

- 6.3. Market Analysis, Insights and Forecast - by Sorghum

- 6.4. Market Analysis, Insights and Forecast - by Rice

- 6.5. Market Analysis, Insights and Forecast - by Wheat

- 6.6. Market Analysis, Insights and Forecast - by Maize

- 6.7. Market Analysis, Insights and Forecast - by Barley

- 6.8. Market Analysis, Insights and Forecast - by Sorghum

- 6.9. Market Analysis, Insights and Forecast - by Rice

- 6.10. Market Analysis, Insights and Forecast - by Wheat

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 OVK

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Senwes

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 GWK

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 AFGRI

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kaap Agri

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Grain SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BKB Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 OVK

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Africa Grain Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Africa Grain Industry Share (%) by Company 2025

List of Tables

- Table 1: South Africa Grain Industry Revenue Million Forecast, by Maize 2020 & 2033

- Table 2: South Africa Grain Industry Volume Kiloton Forecast, by Maize 2020 & 2033

- Table 3: South Africa Grain Industry Revenue Million Forecast, by Barley 2020 & 2033

- Table 4: South Africa Grain Industry Volume Kiloton Forecast, by Barley 2020 & 2033

- Table 5: South Africa Grain Industry Revenue Million Forecast, by Sorghum 2020 & 2033

- Table 6: South Africa Grain Industry Volume Kiloton Forecast, by Sorghum 2020 & 2033

- Table 7: South Africa Grain Industry Revenue Million Forecast, by Rice 2020 & 2033

- Table 8: South Africa Grain Industry Volume Kiloton Forecast, by Rice 2020 & 2033

- Table 9: South Africa Grain Industry Revenue Million Forecast, by Wheat 2020 & 2033

- Table 10: South Africa Grain Industry Volume Kiloton Forecast, by Wheat 2020 & 2033

- Table 11: South Africa Grain Industry Revenue Million Forecast, by Maize 2020 & 2033

- Table 12: South Africa Grain Industry Volume Kiloton Forecast, by Maize 2020 & 2033

- Table 13: South Africa Grain Industry Revenue Million Forecast, by Barley 2020 & 2033

- Table 14: South Africa Grain Industry Volume Kiloton Forecast, by Barley 2020 & 2033

- Table 15: South Africa Grain Industry Revenue Million Forecast, by Sorghum 2020 & 2033

- Table 16: South Africa Grain Industry Volume Kiloton Forecast, by Sorghum 2020 & 2033

- Table 17: South Africa Grain Industry Revenue Million Forecast, by Rice 2020 & 2033

- Table 18: South Africa Grain Industry Volume Kiloton Forecast, by Rice 2020 & 2033

- Table 19: South Africa Grain Industry Revenue Million Forecast, by Wheat 2020 & 2033

- Table 20: South Africa Grain Industry Volume Kiloton Forecast, by Wheat 2020 & 2033

- Table 21: South Africa Grain Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 22: South Africa Grain Industry Volume Kiloton Forecast, by Region 2020 & 2033

- Table 23: South Africa Grain Industry Revenue Million Forecast, by Maize 2020 & 2033

- Table 24: South Africa Grain Industry Volume Kiloton Forecast, by Maize 2020 & 2033

- Table 25: South Africa Grain Industry Revenue Million Forecast, by Barley 2020 & 2033

- Table 26: South Africa Grain Industry Volume Kiloton Forecast, by Barley 2020 & 2033

- Table 27: South Africa Grain Industry Revenue Million Forecast, by Sorghum 2020 & 2033

- Table 28: South Africa Grain Industry Volume Kiloton Forecast, by Sorghum 2020 & 2033

- Table 29: South Africa Grain Industry Revenue Million Forecast, by Rice 2020 & 2033

- Table 30: South Africa Grain Industry Volume Kiloton Forecast, by Rice 2020 & 2033

- Table 31: South Africa Grain Industry Revenue Million Forecast, by Wheat 2020 & 2033

- Table 32: South Africa Grain Industry Volume Kiloton Forecast, by Wheat 2020 & 2033

- Table 33: South Africa Grain Industry Revenue Million Forecast, by Maize 2020 & 2033

- Table 34: South Africa Grain Industry Volume Kiloton Forecast, by Maize 2020 & 2033

- Table 35: South Africa Grain Industry Revenue Million Forecast, by Barley 2020 & 2033

- Table 36: South Africa Grain Industry Volume Kiloton Forecast, by Barley 2020 & 2033

- Table 37: South Africa Grain Industry Revenue Million Forecast, by Sorghum 2020 & 2033

- Table 38: South Africa Grain Industry Volume Kiloton Forecast, by Sorghum 2020 & 2033

- Table 39: South Africa Grain Industry Revenue Million Forecast, by Rice 2020 & 2033

- Table 40: South Africa Grain Industry Volume Kiloton Forecast, by Rice 2020 & 2033

- Table 41: South Africa Grain Industry Revenue Million Forecast, by Wheat 2020 & 2033

- Table 42: South Africa Grain Industry Volume Kiloton Forecast, by Wheat 2020 & 2033

- Table 43: South Africa Grain Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 44: South Africa Grain Industry Volume Kiloton Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Africa Grain Industry?

The projected CAGR is approximately 7.00%.

2. Which companies are prominent players in the South Africa Grain Industry?

Key companies in the market include OVK, Senwes, GWK, AFGRI , Kaap Agri, Grain SA , BKB Ltd.

3. What are the main segments of the South Africa Grain Industry?

The market segments include Maize, Barley, Sorghum, Rice, Wheat, Maize, Barley, Sorghum, Rice, Wheat.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.37 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Consumption of Cashew Nuts in the Country; Favorable Government Initiatives.

6. What are the notable trends driving market growth?

High Regional Trade of Grains is Driving the Market.

7. Are there any restraints impacting market growth?

Hazardous Climatic Condition Hinders Cashew Production; Stringent Regulations Related to Food Quality Standards.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Kiloton.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Africa Grain Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Africa Grain Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Africa Grain Industry?

To stay informed about further developments, trends, and reports in the South Africa Grain Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence