Key Insights

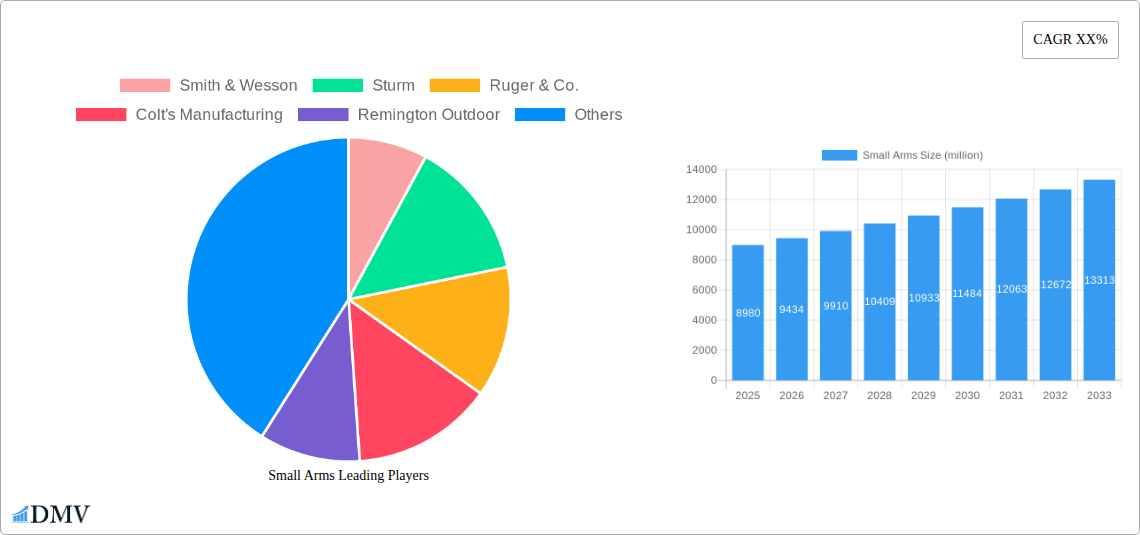

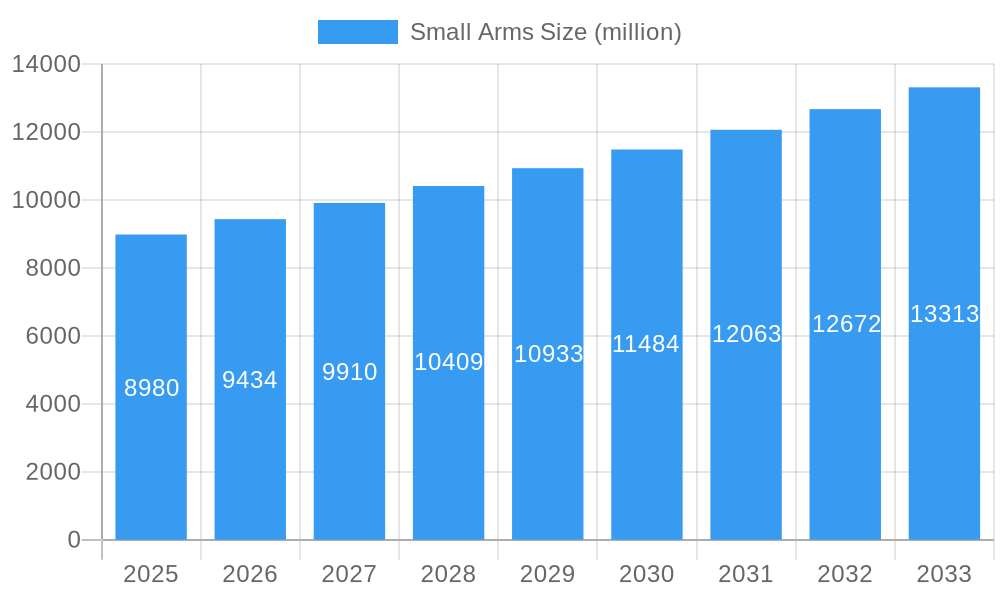

The global small arms market is poised for significant expansion, projected to reach an estimated $8.98 billion in 2025. This growth is propelled by a sustained compound annual growth rate (CAGR) of 5.1% over the forecast period of 2025-2033. The market's dynamism is fueled by increasing defense budgets worldwide, a persistent need for law enforcement modernization, and rising security concerns across both developed and developing nations. The application segment, dominated by civil and military uses, is witnessing robust demand for a diverse range of firearms, including advanced pistols, rifles, and sub-machine guns. Technological advancements, such as the integration of smart features, improved ergonomics, and enhanced material science, are also contributing to market expansion as manufacturers strive to offer more reliable, accurate, and user-friendly products.

Small Arms Market Size (In Billion)

While the market demonstrates a healthy upward trajectory, certain factors could temper its full potential. Geopolitical instability in some regions, coupled with stringent regulatory frameworks governing firearm sales and ownership in others, presents considerable restraints. Nevertheless, the overarching demand for enhanced security and personal protection, alongside continuous innovation in weapon design and manufacturing processes, is expected to drive the small arms market forward. Key players in the industry, such as Smith & Wesson, GLOCK, and SIG SAUER, are actively engaged in research and development to introduce next-generation products, further stimulating market growth and catering to evolving customer needs across various applications and geographical regions.

Small Arms Company Market Share

Small Arms Market: Comprehensive Analysis & Forecast (2019-2033)

This in-depth market research report provides an unparalleled analysis of the global small arms industry, forecasting its trajectory from 2019 to 2033. With a base year of 2025 and a detailed forecast period spanning 2025-2033, this report is an essential resource for stakeholders seeking to understand current trends, identify growth opportunities, and navigate the complexities of this dynamic sector. We delve into the intricate market composition, evolutionary trends, leading regional and segment dominance, groundbreaking product innovations, propelling factors, inherent obstacles, and future opportunities. The report meticulously examines key players and pivotal industry developments, offering a strategic forecast for sustained growth and market penetration. Dive into the detailed segmentation across Civil, Military, and Law Enforcement applications, and explore the diverse product types including Revolvers & Pistols, Rifles & Carbines, Assault Rifles, Sub-Machine Guns, and Light Machine Guns.

Small Arms Market Composition & Trends

The global small arms market is characterized by a moderate to high concentration, with key players like GLOCK, Inc., SIG SAUER, Smith & Wesson, Sturm, Ruger & Co., and Beretta holding significant market share, collectively accounting for an estimated $80 billion in revenue in 2025. Innovation is primarily driven by advancements in material science for lighter and more durable components, improved ergonomics, and the integration of smart technologies for enhanced accuracy and security. Regulatory landscapes vary significantly by region, influencing market access and product development; for instance, stricter regulations in Western Europe impact certain firearm types, while more liberal policies in North America foster robust civilian markets. Substitute products, such as non-lethal defense options and advanced surveillance technologies, pose a minor but growing threat in specific civilian applications. End-user profiles are diverse, ranging from law enforcement agencies prioritizing reliability and stopping power, to military forces demanding modularity and high-volume fire capabilities, and civilian consumers seeking sport shooting, hunting, and self-defense. Mergers and acquisitions (M&A) activity, valued at approximately $5 billion in the historical period (2019-2024), has been instrumental in consolidating market share and acquiring specialized technologies, with notable deals including the acquisition of smaller defense contractors by larger entities like General Dynamics and Olin Corporation.

- Market Share Distribution (Estimated 2025):

- Top 5 Companies: 60%

- Top 10 Companies: 80%

- Fragmented Market Share: 20%

- M&A Deal Values (Historical Period 2019-2024):

- Total Estimated Value: $5 billion

- Average Deal Size: $100 million

Small Arms Industry Evolution

The small arms industry has undergone significant evolution throughout the study period (2019–2033), driven by a confluence of technological breakthroughs, shifting geopolitical landscapes, and evolving consumer demands. From 2019 to 2024, the market demonstrated a steady growth trajectory, with an average annual growth rate of 3.5%, primarily fueled by increased defense spending in emerging economies and a sustained demand for personal defense firearms in established markets. The estimated market size in 2025 stands at a robust $100 billion. Technological advancements have been a critical catalyst, with a notable shift towards modular designs, advanced material composites (like polymer frames and advanced alloys), and improved firearm sighting systems. The integration of precision manufacturing techniques, including CNC machining and additive manufacturing, has led to enhanced product performance, tighter tolerances, and reduced production costs. Furthermore, the development of smart firearms, incorporating digital security features and data logging capabilities, has begun to gain traction, particularly within law enforcement and military sectors, albeit with early adoption rates still in their nascent stages.

Consumer demand has also played a pivotal role in shaping the industry. In the civilian segment, there has been a discernible rise in interest in versatile firearms suitable for sport shooting, competitive events, and personal protection, leading to increased demand for semi-automatic pistols and modern sporting rifles. The "concealed carry" trend in various countries has further boosted the market for compact and lightweight firearms. For military and law enforcement, the emphasis has shifted towards lighter, more adaptable weapon systems that can be quickly reconfigured for different operational environments, alongside a growing demand for suppressed weapon systems to enhance operational security and reduce acoustic signature. The geopolitical climate, marked by regional conflicts and an increased focus on internal security, has consistently bolstered demand for a wide array of small arms. The adoption of advanced training simulators and virtual reality platforms is also influencing the purchasing decisions of end-users, as it allows for more effective and cost-efficient skill development. Forecasts indicate that this evolutionary momentum will continue, with projected annual growth rates of 4.2% for the forecast period (2025–2033), reaching an estimated market value of $135 billion by 2033. This sustained growth is underpinned by continuous innovation and an enduring need for effective personal and national security solutions.

Leading Regions, Countries, or Segments in Small Arms

The Military Application segment stands as the dominant force within the global small arms ecosystem, projected to command an estimated $55 billion of the market in 2025. This supremacy is driven by sustained government investments in defense modernization programs, ongoing geopolitical tensions, and the constant need for robust armaments to maintain national security. Countries such as the United States, with its substantial defense budget and active global military presence, are significant contributors to this dominance. Furthermore, emerging economies are increasingly prioritizing military acquisitions to bolster their defense capabilities, thereby expanding the market for a wide array of small arms, including Assault Rifles, Light Machine Guns, and specialized combat pistols.

Within the Military Application, the Rifles & Carbines product type represents the largest sub-segment, with an estimated market value of $25 billion in 2025. This is directly attributable to their role as standard-issue infantry weapons and the constant evolution of these platforms to meet modern combat requirements. Countries are investing heavily in advanced modular rifle systems that offer greater versatility, accuracy, and interoperability with various accessories and optics.

The United States emerges as the leading country in the global small arms market, driven by a unique combination of factors. Its significant defense spending, estimated at over $800 billion annually, provides a massive market for military and law enforcement procurement. Simultaneously, a strong civilian firearms culture, robust legal frameworks for firearm ownership (though subject to ongoing debate and regional variations), and a high demand for personal defense weapons contribute to a thriving consumer market. The estimated total market value within the United States is projected to exceed $40 billion in 2025.

Key drivers underpinning the dominance of the Military Application segment and the United States include:

- Government Procurement Cycles: Continuous defense budget allocations and modernization initiatives in major military powers.

- Geopolitical Instability: Regional conflicts and the perceived need for enhanced national security fuel demand.

- Technological Advancements in Military Firearm Design: Focus on lighter, more modular, and accurate weapon systems.

- Strong Civilian Demand in the US: The prevalence of self-defense laws and a culture of gun ownership.

- Law Enforcement Modernization: Police forces globally are upgrading their standard-issue firearms for improved effectiveness.

- Terrorism and Insurgency: The persistent threat of terrorism necessitates well-armed security forces worldwide.

Small Arms Product Innovations

Recent product innovations in the small arms industry are revolutionizing performance and user experience. Companies are leveraging advanced composite materials for lighter, more durable firearm components, such as the polymer frames in GLOCK pistols and the carbon-fiber reinforced stocks on many modern rifles. Enhanced ergonomic designs, including adjustable grips and improved stock configurations, are significantly boosting shooter comfort and control. Furthermore, the integration of advanced optics and digital sighting systems, offering features like ballistic calculators and night vision compatibility, is improving accuracy and target acquisition speed across all weapon types. The development of modular firearm platforms, allowing for quick and easy conversion between different configurations (e.g., from a carbine to a short-barreled rifle), enhances adaptability for diverse operational needs in both military and civilian applications.

Propelling Factors for Small Arms Growth

The small arms market is propelled by several key factors. Technological advancements in materials, ergonomics, and optics are driving demand for updated and more effective weaponry. Increasing geopolitical tensions and regional conflicts worldwide necessitate robust defense spending and a continuous need for military and law enforcement arms. The growing emphasis on personal security and self-defense in both developed and developing nations fuels a significant civilian market. Furthermore, government modernization initiatives for their armed forces and police departments, coupled with favorable regulatory environments in certain key markets, continue to provide a strong impetus for growth.

Obstacles in the Small Arms Market

Despite robust growth, the small arms market faces significant obstacles. Stringent and evolving gun control regulations in numerous countries present a major barrier to market access and product sales, leading to increased compliance costs. Supply chain disruptions, as experienced during recent global events, can impact manufacturing timelines and material availability, potentially delaying production and increasing costs. Intensifying competitive pressures among established players and emerging manufacturers, particularly in price-sensitive segments, can squeeze profit margins. Furthermore, public perception and ethical concerns surrounding firearms can lead to boycotts and increased scrutiny, impacting sales and brand reputation. The estimated economic impact of regulatory hurdles on market expansion is projected at $10 billion annually.

Future Opportunities in Small Arms

Emerging opportunities in the small arms market are abundant. The increasing adoption of smart firearm technologies, integrating digital security and data analytics, presents a significant growth avenue. Expansion into emerging markets with growing defense budgets and increasing demand for personal security offers substantial potential. The development of environmentally sustainable manufacturing processes and advanced ammunition technologies, such as guided projectiles, will cater to evolving military and civilian preferences. Furthermore, the growing interest in competitive shooting sports and responsible recreational hunting will continue to drive demand for specialized civilian firearms.

Major Players in the Small Arms Ecosystem

- Smith & Wesson

- Sturm, Ruger & Co.

- Colt’s Manufacturing

- Remington Outdoor

- Olin Corporation

- Ordnance Factory Board (OFB)

- General Dynamics

- FN Herstal

- O.F. Mossberg & Sons

- Taurus USA

- SSS Defence

- GLOCK, Inc.

- SIG SAUER

- Beretta

Key Developments in Small Arms Industry

- 2021: Smith & Wesson launches the M&P Shield Plus pistol, enhancing concealed carry options.

- 2022: SIG SAUER introduces the MCX-SPEAR LT, a versatile rifle platform for military applications.

- 2023: GLOCK unveils its G47 MOS pistol, expanding its modular optic system offerings.

- 2023: SSS Defence introduces innovative lightweight rifle designs for enhanced maneuverability.

- 2024: Beretta showcases advancements in sub-machine gun technology with improved recoil management.

- 2024: Olin Corporation continues to focus on advanced ammunition development for military and law enforcement.

- 2025: General Dynamics is expected to announce new contracts for modular weapon systems.

- 2026: FN Herstal anticipates launching next-generation light machine gun prototypes.

- 2027: Taurus USA is projected to expand its pistol offerings with enhanced safety features.

- 2028: Remington Outdoor is expected to highlight advancements in sporting rifle accuracy.

- 2029: Ordnance Factory Board (OFB) is anticipated to disclose new indigenous rifle development projects.

- 2030: Sturm, Ruger & Co. is likely to present new innovations in bolt-action rifle technology.

- 2031: Colt's Manufacturing may reveal modernized versions of iconic firearm platforms.

- 2032: O.F. Mossberg & Sons is expected to showcase advancements in shotgun technology for tactical applications.

- 2033: The industry anticipates a greater integration of AI-assisted targeting systems in high-end firearms.

Strategic Small Arms Market Forecast

The strategic small arms market forecast indicates sustained growth driven by ongoing demand from military and law enforcement agencies for advanced weaponry, coupled with a resilient civilian market fueled by personal security concerns and sporting activities. Innovations in smart firearm technology and lighter, more durable materials will continue to shape product development. Emerging economies represent significant growth opportunities, while established markets will benefit from continuous modernization programs. The market is expected to navigate regulatory complexities through product adaptation and lobbying efforts, positioning it for continued expansion and increased market penetration in the coming years. The projected market value by 2033 is estimated to reach $135 billion.

Small Arms Segmentation

-

1. Application

- 1.1. Civil

- 1.2. Military

- 1.3. Law Enforcement

-

2. Types

- 2.1. Revolvers & Pistols

- 2.2. Rifles & Carbines

- 2.3. Assault Rifles

- 2.4. Sub-Machine Guns

- 2.5. Light Machine Guns

Small Arms Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

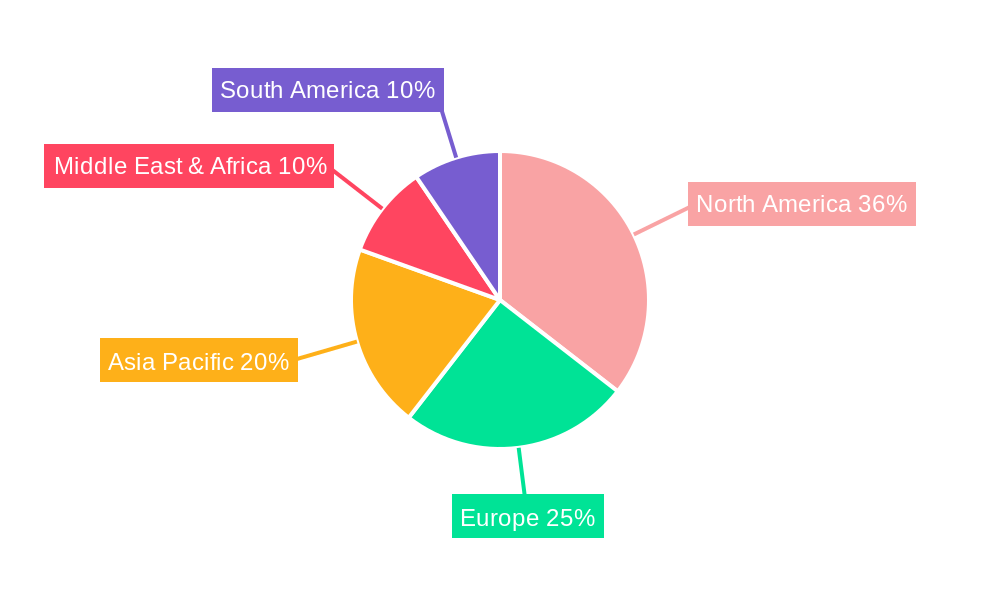

Small Arms Regional Market Share

Geographic Coverage of Small Arms

Small Arms REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Civil

- 5.1.2. Military

- 5.1.3. Law Enforcement

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Revolvers & Pistols

- 5.2.2. Rifles & Carbines

- 5.2.3. Assault Rifles

- 5.2.4. Sub-Machine Guns

- 5.2.5. Light Machine Guns

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Small Arms Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Civil

- 6.1.2. Military

- 6.1.3. Law Enforcement

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Revolvers & Pistols

- 6.2.2. Rifles & Carbines

- 6.2.3. Assault Rifles

- 6.2.4. Sub-Machine Guns

- 6.2.5. Light Machine Guns

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Small Arms Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Civil

- 7.1.2. Military

- 7.1.3. Law Enforcement

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Revolvers & Pistols

- 7.2.2. Rifles & Carbines

- 7.2.3. Assault Rifles

- 7.2.4. Sub-Machine Guns

- 7.2.5. Light Machine Guns

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Small Arms Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Civil

- 8.1.2. Military

- 8.1.3. Law Enforcement

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Revolvers & Pistols

- 8.2.2. Rifles & Carbines

- 8.2.3. Assault Rifles

- 8.2.4. Sub-Machine Guns

- 8.2.5. Light Machine Guns

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Small Arms Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Civil

- 9.1.2. Military

- 9.1.3. Law Enforcement

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Revolvers & Pistols

- 9.2.2. Rifles & Carbines

- 9.2.3. Assault Rifles

- 9.2.4. Sub-Machine Guns

- 9.2.5. Light Machine Guns

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Small Arms Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Civil

- 10.1.2. Military

- 10.1.3. Law Enforcement

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Revolvers & Pistols

- 10.2.2. Rifles & Carbines

- 10.2.3. Assault Rifles

- 10.2.4. Sub-Machine Guns

- 10.2.5. Light Machine Guns

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Small Arms Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Civil

- 11.1.2. Military

- 11.1.3. Law Enforcement

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Revolvers & Pistols

- 11.2.2. Rifles & Carbines

- 11.2.3. Assault Rifles

- 11.2.4. Sub-Machine Guns

- 11.2.5. Light Machine Guns

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smith & Wesson

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sturm

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ruger & Co.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Colt’s Manufacturing

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Remington Outdoor

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Olin Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ordnance Factory Board (OFB)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 General Dynamics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 FN Herstal

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 O.F. Mossberg & Sons

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Taurus USA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 SSS Defence

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 GLOCK

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Inc.

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 SIG SAUER

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Beretta

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Smith & Wesson

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Small Arms Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Small Arms Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Small Arms Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Small Arms Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Small Arms Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Small Arms Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Small Arms Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Small Arms Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Small Arms Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Small Arms Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Small Arms Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Small Arms Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Small Arms Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Small Arms Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Small Arms Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Small Arms Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Small Arms Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Small Arms Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Small Arms Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Small Arms Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Small Arms Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Small Arms Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Small Arms Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Small Arms Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Small Arms Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Small Arms Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Small Arms Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Small Arms Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Small Arms Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Small Arms Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Small Arms Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Small Arms Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Small Arms Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Small Arms Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Small Arms Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Small Arms Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Small Arms Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Small Arms Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Small Arms Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Small Arms Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Small Arms?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Small Arms?

Key companies in the market include Smith & Wesson, Sturm, Ruger & Co., Colt’s Manufacturing, Remington Outdoor, Olin Corporation, Ordnance Factory Board (OFB), General Dynamics, FN Herstal, O.F. Mossberg & Sons, Taurus USA, SSS Defence, GLOCK, Inc., SIG SAUER, Beretta.

3. What are the main segments of the Small Arms?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Small Arms," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Small Arms report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Small Arms?

To stay informed about further developments, trends, and reports in the Small Arms, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence