Key Insights

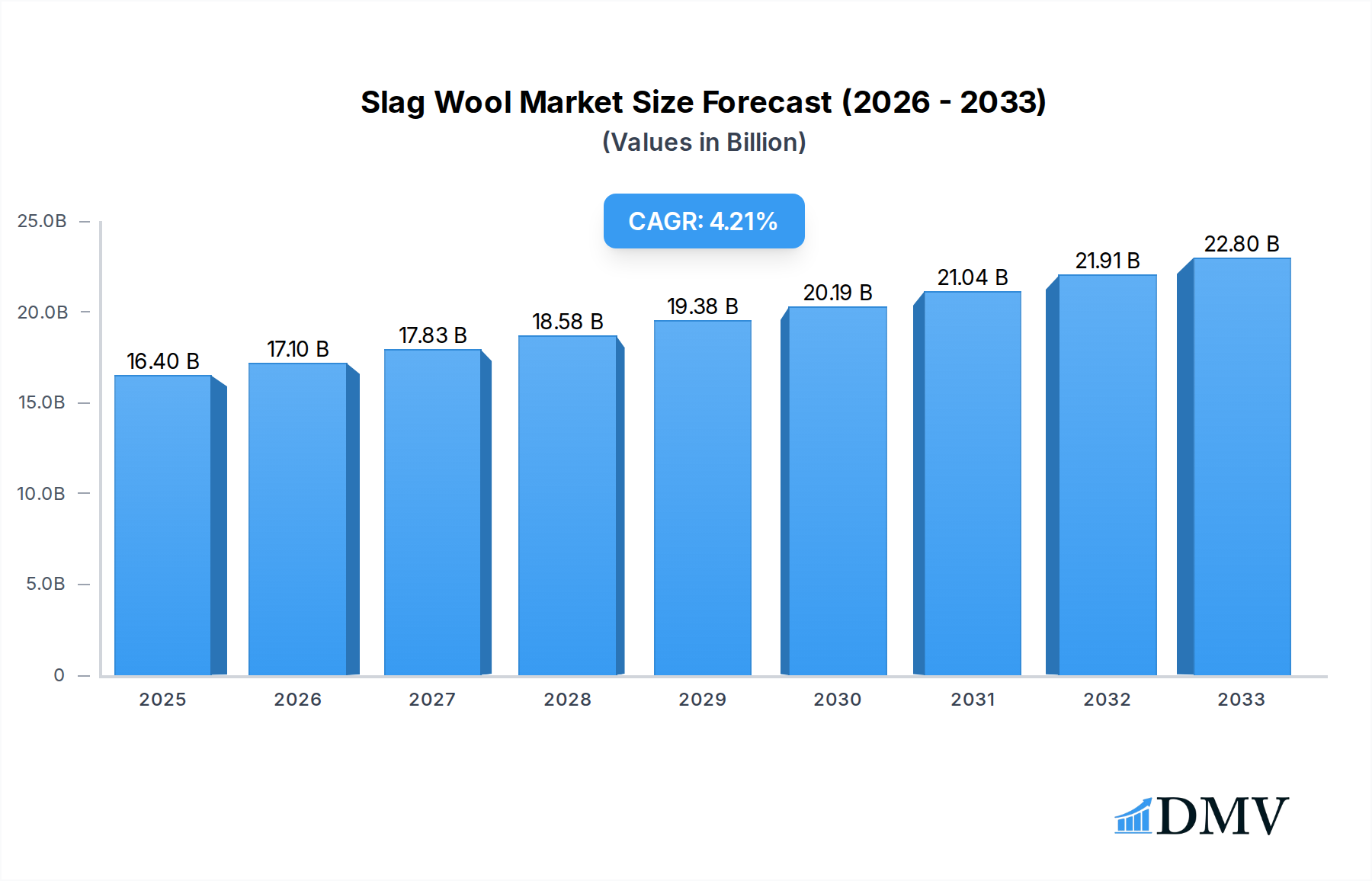

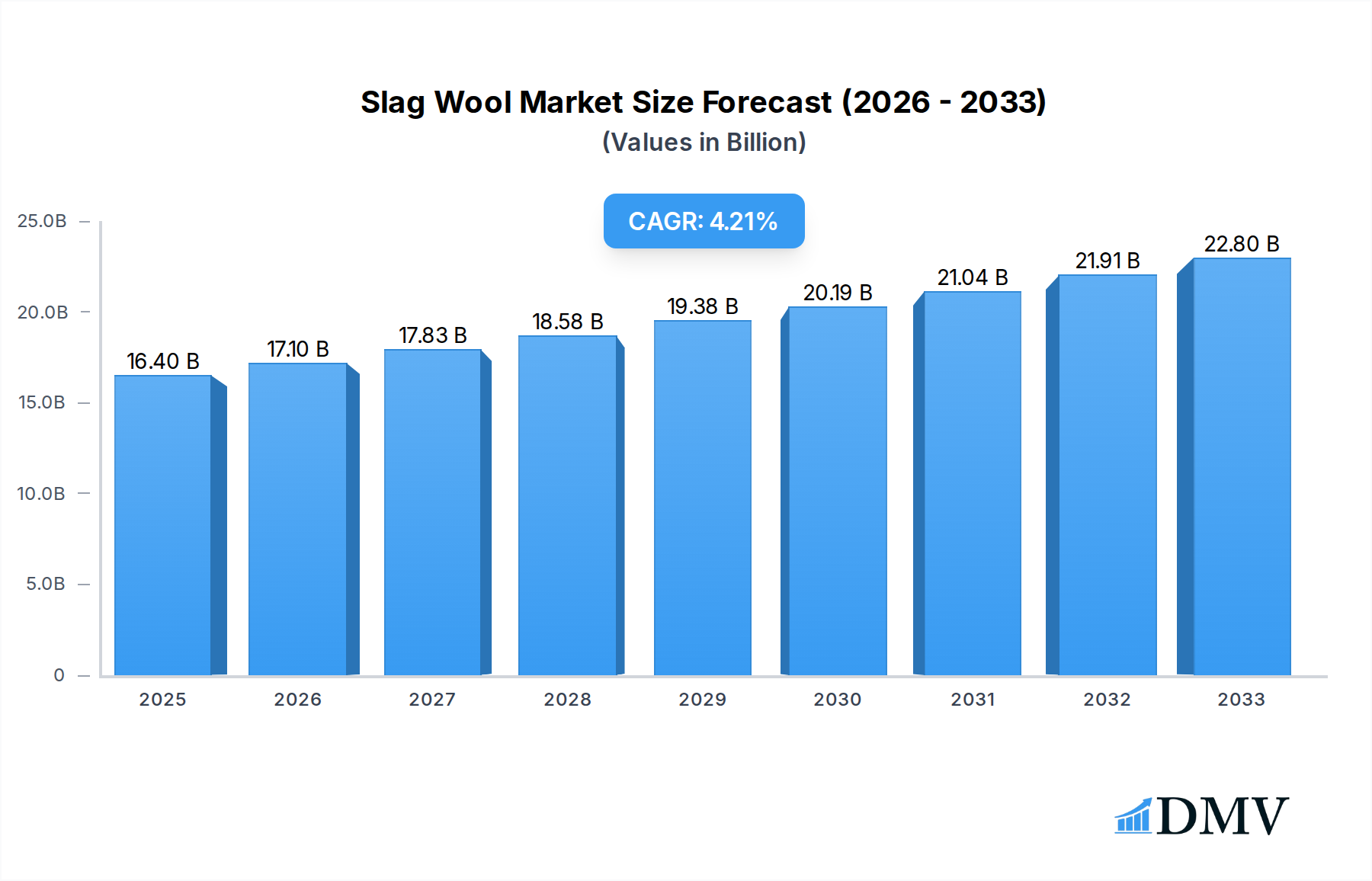

The global Slag Wool market is poised for significant expansion, projected to reach an estimated $16.4 billion in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4.3% expected between 2025 and 2033. The burgeoning demand for effective insulation solutions across various sectors is the primary catalyst. Specifically, the building insulation and fire prevention segment is a key driver, fueled by increasing awareness and stringent regulations regarding energy efficiency and safety in construction. Industrial applications, including pipe network and furnace insulation, also contribute substantially, driven by the need to optimize operational efficiency and reduce energy wastage in manufacturing and processing industries. Furthermore, the growing use of slag wool as a damping material in automotive and other industries, alongside its emerging applications in agriculture for soilless culture, signals a diversified and expanding market.

Slag Wool Market Size (In Billion)

Several factors are shaping the trajectory of the slag wool market. Key drivers include governmental initiatives promoting sustainable construction practices, advancements in manufacturing technologies leading to improved product performance, and a growing emphasis on reducing greenhouse gas emissions through enhanced thermal management. While the market benefits from these tailwinds, certain restraints, such as the initial cost of installation compared to some alternative materials and the logistical challenges associated with raw material sourcing in specific regions, need to be navigated. However, ongoing innovation in slag wool production, focusing on cost-effectiveness and enhanced properties, is expected to mitigate these challenges. The market's segmentation by type, offering a range of densities and thermal properties, allows for tailored solutions across diverse applications, further solidifying its growth potential.

Slag Wool Company Market Share

Here is an SEO-optimized and insightful report description for Slag Wool, designed for high search visibility and stakeholder engagement.

Slag Wool Market Composition & Trends

The global slag wool market is characterized by a dynamic competitive landscape, with key players like USG, Paroc, and Hebei Huaneng Zhongtian strategically positioned to capitalize on evolving industry demands. This report delves into the intricate market composition, examining the influence of innovation catalysts such as advancements in manufacturing processes and the development of higher-performance slag wool products. Regulatory landscapes, particularly those focused on energy efficiency standards and fire safety regulations, play a pivotal role in shaping market penetration for slag wool applications in building insulation and fire prevention. The threat of substitute products, while present, is mitigated by slag wool's superior fire resistance and acoustic properties. End-user profiles are diverse, spanning the construction sector, industrial facilities, and even niche agricultural applications for soilless culture. Mergers and acquisitions (M&A) activities are anticipated to further consolidate market share, with estimated deal values in the billions of dollars driving strategic growth. Understanding these elements is crucial for stakeholders navigating this complex market.

- Market Share Distribution: Detailed analysis of leading company market shares, projected to reach over $30 billion by 2033.

- M&A Deal Values: Insights into significant past and projected M&A transactions, with total values estimated to exceed $15 billion.

- Innovation Focus: Identification of key areas driving product development, such as enhanced thermal performance and improved handling characteristics.

- Regulatory Impact: Evaluation of how global building codes and environmental policies are influencing demand for sustainable insulation solutions.

Slag Wool Industry Evolution

The slag wool industry has witnessed a remarkable evolution, transitioning from a basic insulating material to a sophisticated solution integral to modern construction and industrial processes. Throughout the historical period of 2019–2024, the market experienced steady growth, driven by increasing awareness of energy conservation and stringent fire safety mandates. The base year of 2025 marks a pivotal point, with significant technological advancements poised to further accelerate this trajectory. Market growth trajectories are robust, with projected compound annual growth rates (CAGRs) exceeding 7% during the forecast period of 2025–2033. This expansion is fueled by substantial investments in research and development, leading to the creation of slag wool products with superior thermal conductivity and acoustic dampening capabilities. Consumer demands are increasingly shifting towards sustainable and non-combustible insulation materials, a trend that slag wool is exceptionally well-positioned to meet. The adoption of slag wool in diverse applications, from high-rise buildings to industrial furnaces, underscores its versatility and performance advantages. Ongoing industry developments are focused on enhancing the recyclability of slag wool and reducing its environmental footprint, further solidifying its position as a preferred insulation choice in a world prioritizing sustainability and safety.

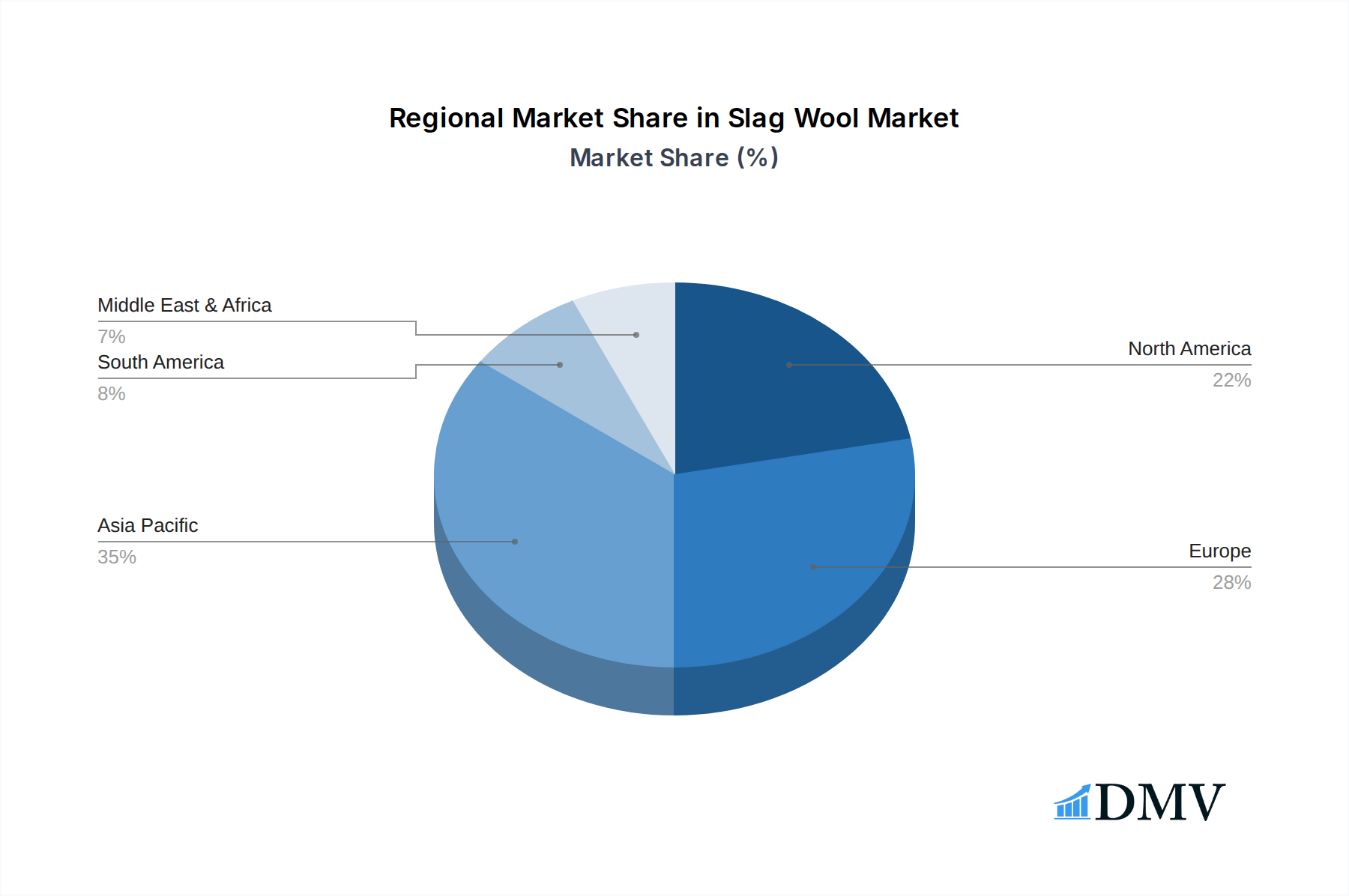

Leading Regions, Countries, or Segments in Slag Wool

The slag wool market exhibits pronounced regional dominance and segment leadership, primarily driven by economic development, stringent building regulations, and industrial output. North America and Europe currently represent the largest markets, owing to their established construction sectors and a deep-rooted emphasis on energy-efficient building practices and robust fire safety standards. Asia Pacific, however, is emerging as the fastest-growing region, propelled by rapid urbanization, infrastructure development, and a burgeoning manufacturing base.

Within the Application segment, Building Insulation and Fire Prevention is the undisputed leader, accounting for over 60% of the global market share. This dominance is directly attributable to:

- Investment Trends: Significant government and private sector investments in green building initiatives and retrofitting older structures for improved energy efficiency.

- Regulatory Support: Stringent building codes mandating high thermal performance and non-combustibility for new constructions and renovations. For instance, building energy codes in major economies often specify R-values achievable with quality slag wool insulation.

- Consumer Demand: Growing homeowner and developer preference for materials that enhance comfort, reduce energy bills, and provide superior fire protection.

- Market Size: The global market for building insulation alone is projected to reach over $25 billion by 2033.

The Type segment exhibiting significant traction is 120-200 and 100-180. This is because these density ranges offer an optimal balance of thermal resistance, compressive strength, and cost-effectiveness for a wide array of building and industrial applications.

- Performance Metrics: These density specifications provide excellent thermal performance with lambda values as low as 0.032 W/mK, crucial for meeting demanding insulation requirements.

- Application Versatility: Suitable for applications ranging from cavity walls and flat roofs to industrial pipe insulation and furnace linings.

- Cost-Effectiveness: Offering a competitive price-to-performance ratio compared to other high-performance insulation materials.

- Growth Potential: Projected growth for these specific types is estimated to be over 8% CAGR during the forecast period.

Furthermore, the Industrial heating Pipe Network and Furnace Insulation application segment is a significant contributor, driven by the need for high-temperature resistance and energy savings in manufacturing and power generation. The Damping Material application is also gaining traction due to the increasing demand for noise reduction in automotive and construction industries.

Slag Wool Product Innovations

Slag wool product innovations are significantly enhancing its performance and application versatility. Recent advancements focus on creating slag wool with improved fire resistance ratings, achieving Euroclass A1 classification for unparalleled fire safety. Innovations in binder technologies are leading to lower VOC emissions, making slag wool a more environmentally friendly choice for indoor applications. Furthermore, the development of hydrophobic treatments enhances moisture resistance, crucial for longevity in building insulation. Performance metrics are continually improving, with enhanced thermal conductivity values and increased compressive strength allowing for thinner insulation layers. These product innovations are driving the adoption of slag wool in new markets and solidifying its position as a premium insulation material.

Propelling Factors for Slag Wool Growth

Several key growth drivers are propelling the slag wool market forward. Technologically, advancements in manufacturing processes are leading to higher quality and more cost-effective slag wool products, improving thermal performance and fire resistance ratings. Economically, the global push for energy efficiency in buildings and industrial operations directly translates to increased demand for effective insulation like slag wool, leading to significant cost savings on energy bills. Regulatory influences, such as stricter building codes mandating higher insulation standards and enhanced fire safety measures, further solidify slag wool's market position. For instance, the widespread adoption of passive house standards in many regions necessitates materials with exceptional thermal performance. The growing awareness of sustainability and the circular economy also benefits slag wool, as it is often derived from recycled industrial by-products.

Obstacles in the Slag Wool Market

Despite its robust growth, the slag wool market faces several obstacles. Regulatory challenges, particularly concerning the classification and handling of mineral wool products in certain regions, can impede market access and adoption. Supply chain disruptions, exacerbated by geopolitical events and raw material availability fluctuations, can impact production costs and lead times, potentially increasing the price of slag wool. Competitive pressures from alternative insulation materials, such as fiberglass, foam boards, and natural insulations, remain a constant threat, necessitating continuous innovation and cost competitiveness. For example, fluctuations in the price of petroleum-based materials can affect the competitiveness of foam insulation. The perception of slag wool as an industrial byproduct, rather than a premium building material, can also present a marketing hurdle, requiring concerted efforts to educate stakeholders on its performance and safety benefits.

Future Opportunities in Slag Wool

The slag wool market is ripe with emerging opportunities. The increasing global focus on retrofitting older buildings for improved energy efficiency presents a substantial growth avenue, as slag wool offers excellent performance for both thermal and acoustic upgrades. The burgeoning green building sector, driven by sustainability certifications like LEED and BREEAM, will continue to fuel demand. Furthermore, advancements in product development, such as the creation of more specialized slag wool formulations for high-temperature industrial applications and acoustic dampening in urban environments, will unlock new market segments. The growing adoption of modular construction and prefabricated building components also offers opportunities for pre-formed slag wool insulation solutions. Exploring new geographical markets with developing construction industries and increasing environmental awareness also represents a significant untapped potential.

Major Players in the Slag Wool Ecosystem

- USG

- Paroc

- Hebei Huaneng Zhongtian

- Changyi Jiayuan Jiancai

- Hejian 100 keda Chemical

- Shanghai Boda Insulation Materials

- Beijing Huiteng Insulation Materials

- Dachengxian Yichuan Insulation Materials

- Dacheng Litanbei Insulation Materials

- Tiger Rock Wool

- Zhengye Insulation Materials

- Shanghai Yannuo New Materials

- Langfang Juheng Building Materials

- Changchun ShiLu Insulation Materials

- Langfang Taiyue Insulation Materials

- Hongli Insulation Materials

- Langfang ZhiRui Insulation Materials

- Langfang Qiyuan Insulation Materials

- Langfang Zhongyang Insulation Materials

- Langfang Zhibang Insulation Materials

- Dacheng Yimansi Insulation Materials

- Langfang Fuerda Building Materials

Key Developments in Slag Wool Industry

- 2023 October: Launch of next-generation slag wool with enhanced fire resistance and reduced binder content, targeting high-performance building applications.

- 2024 January: Strategic partnership formed between USG and a major industrial manufacturer to optimize slag wool production from by-products, aiming to reduce production costs by an estimated 10%.

- 2024 March: Paroc expands its manufacturing capacity in Europe to meet growing demand for sustainable insulation solutions, projecting a 15% market share increase.

- 2024 June: Hebei Huaneng Zhongtian announces investment in new recycling technologies to improve the circularity of slag wool production, aiming for a 90% recycled content.

- 2025 February: Introduction of a new slag wool product specifically designed for acoustic dampening in commercial buildings, receiving early positive feedback from architects and developers.

Strategic Slag Wool Market Forecast

The strategic slag wool market forecast indicates a period of sustained and accelerated growth, driven by a confluence of technological advancements, favorable economic conditions, and increasingly stringent regulatory frameworks. The anticipated growth is underpinned by the material's inherent strengths in fire prevention, thermal insulation, and acoustic performance, making it an indispensable component in modern construction and industrial applications. Continued investment in product innovation, focusing on enhanced sustainability and ease of installation, will further broaden its appeal. Emerging markets in developing economies, coupled with a global emphasis on energy efficiency and circular economy principles, present significant untapped potential. The market is projected to witness significant expansion, with strategic collaborations and mergers playing a key role in shaping its future landscape and ensuring robust market dominance for key players.

Slag Wool Segmentation

-

1. Application

- 1.1. Building Insulation and Fire Prevention

- 1.2. Industrial heating Pipe Network and Furnace Insulation

- 1.3. Damping Material

- 1.4. Agriculture Soilless Culture

- 1.5. Others

-

2. Types

- 2.1. 120-200

- 2.2. 60-120

- 2.3. 100-180

- 2.4. 40-100

- 2.5. 80-140

Slag Wool Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Slag Wool Regional Market Share

Geographic Coverage of Slag Wool

Slag Wool REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Slag Wool Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Building Insulation and Fire Prevention

- 5.1.2. Industrial heating Pipe Network and Furnace Insulation

- 5.1.3. Damping Material

- 5.1.4. Agriculture Soilless Culture

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 120-200

- 5.2.2. 60-120

- 5.2.3. 100-180

- 5.2.4. 40-100

- 5.2.5. 80-140

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Slag Wool Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Building Insulation and Fire Prevention

- 6.1.2. Industrial heating Pipe Network and Furnace Insulation

- 6.1.3. Damping Material

- 6.1.4. Agriculture Soilless Culture

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 120-200

- 6.2.2. 60-120

- 6.2.3. 100-180

- 6.2.4. 40-100

- 6.2.5. 80-140

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Slag Wool Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Building Insulation and Fire Prevention

- 7.1.2. Industrial heating Pipe Network and Furnace Insulation

- 7.1.3. Damping Material

- 7.1.4. Agriculture Soilless Culture

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 120-200

- 7.2.2. 60-120

- 7.2.3. 100-180

- 7.2.4. 40-100

- 7.2.5. 80-140

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Slag Wool Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Building Insulation and Fire Prevention

- 8.1.2. Industrial heating Pipe Network and Furnace Insulation

- 8.1.3. Damping Material

- 8.1.4. Agriculture Soilless Culture

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 120-200

- 8.2.2. 60-120

- 8.2.3. 100-180

- 8.2.4. 40-100

- 8.2.5. 80-140

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Slag Wool Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Building Insulation and Fire Prevention

- 9.1.2. Industrial heating Pipe Network and Furnace Insulation

- 9.1.3. Damping Material

- 9.1.4. Agriculture Soilless Culture

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 120-200

- 9.2.2. 60-120

- 9.2.3. 100-180

- 9.2.4. 40-100

- 9.2.5. 80-140

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Slag Wool Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Building Insulation and Fire Prevention

- 10.1.2. Industrial heating Pipe Network and Furnace Insulation

- 10.1.3. Damping Material

- 10.1.4. Agriculture Soilless Culture

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 120-200

- 10.2.2. 60-120

- 10.2.3. 100-180

- 10.2.4. 40-100

- 10.2.5. 80-140

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 USG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Paroc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hebei Huaneng Zhongtian

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Changyi Jiayuan Jiancai

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hejian 100 keda Chemical

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Shanghai Boda Insulation Materials

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Beijing Huiteng Insulation Materials

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Dachengxian Yichuan Insulation Materials

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Dacheng Litanbei Insulation Materials

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tiger Rock Wool

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Zhengye Insulation Materials

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Shanghai Yannuo New Materials

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Langfang Juheng Building Materials

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Changchun ShiLu Insulation Materials

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Langfang Taiyue Insulation Materials

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Hongli Insulation Materials

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Langfang ZhiRui Insulation Materials

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Langfang Qiyuan Insulation Materials

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Langfang Zhongyang Insulation Materials

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Langfang Zhibang Insulation Materials

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Dacheng Yimansi Insulation Materials

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Langfang Fuerda Building Materials

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.1 USG

List of Figures

- Figure 1: Global Slag Wool Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Slag Wool Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Slag Wool Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Slag Wool Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Slag Wool Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Slag Wool Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Slag Wool Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Slag Wool Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Slag Wool Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Slag Wool Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Slag Wool Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Slag Wool Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Slag Wool Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Slag Wool Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Slag Wool Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Slag Wool Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Slag Wool Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Slag Wool Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Slag Wool Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Slag Wool Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Slag Wool Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Slag Wool Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Slag Wool Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Slag Wool Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Slag Wool Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Slag Wool Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Slag Wool Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Slag Wool Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Slag Wool Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Slag Wool Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Slag Wool Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Slag Wool Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Slag Wool Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Slag Wool Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Slag Wool Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Slag Wool Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Slag Wool Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Slag Wool Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Slag Wool Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Slag Wool Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Slag Wool?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Slag Wool?

Key companies in the market include USG, Paroc, Hebei Huaneng Zhongtian, Changyi Jiayuan Jiancai, Hejian 100 keda Chemical, Shanghai Boda Insulation Materials, Beijing Huiteng Insulation Materials, Dachengxian Yichuan Insulation Materials, Dacheng Litanbei Insulation Materials, Tiger Rock Wool, Zhengye Insulation Materials, Shanghai Yannuo New Materials, Langfang Juheng Building Materials, Changchun ShiLu Insulation Materials, Langfang Taiyue Insulation Materials, Hongli Insulation Materials, Langfang ZhiRui Insulation Materials, Langfang Qiyuan Insulation Materials, Langfang Zhongyang Insulation Materials, Langfang Zhibang Insulation Materials, Dacheng Yimansi Insulation Materials, Langfang Fuerda Building Materials.

3. What are the main segments of the Slag Wool?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.4 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Slag Wool," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Slag Wool report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Slag Wool?

To stay informed about further developments, trends, and reports in the Slag Wool, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence