Key Insights

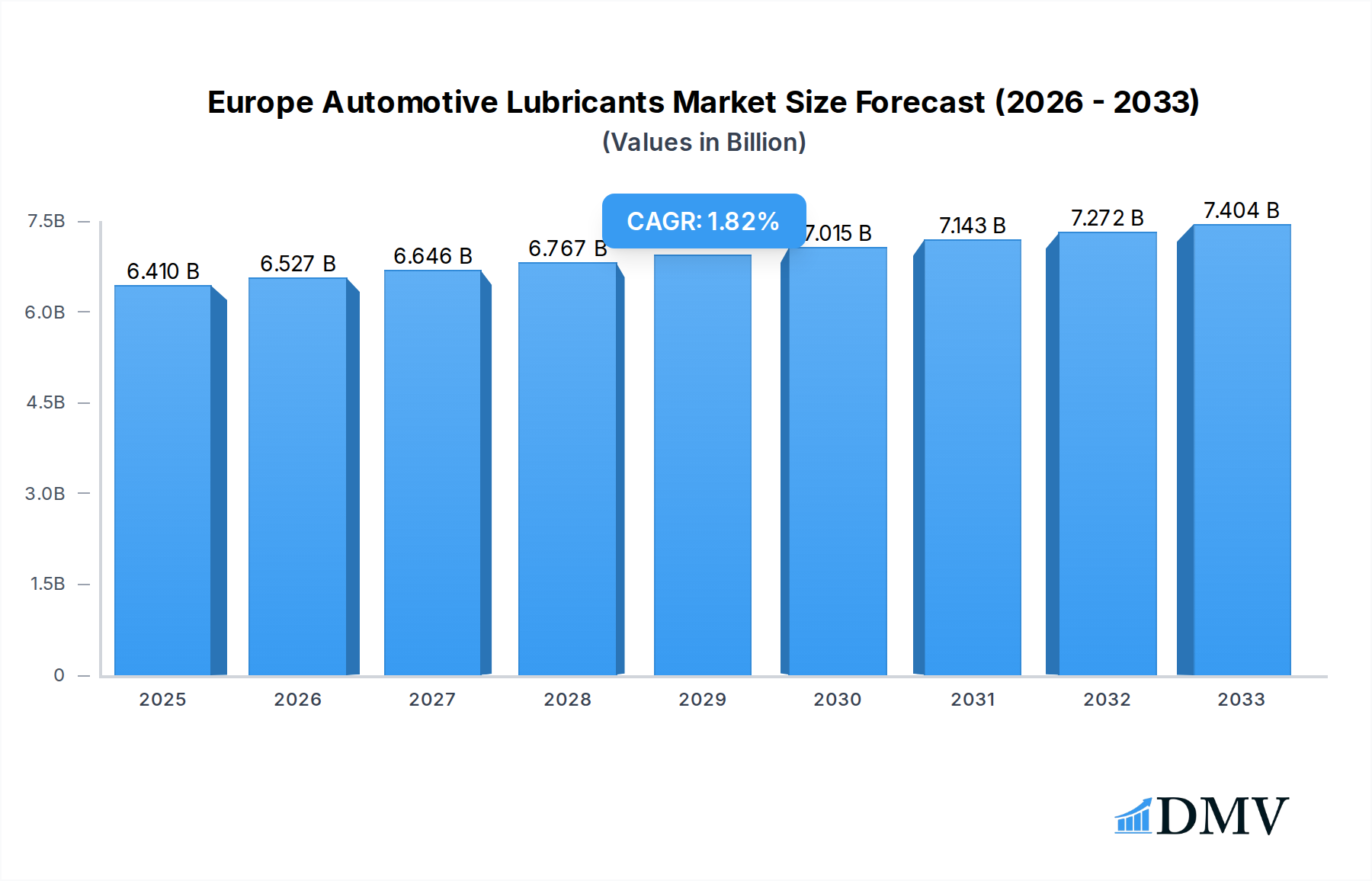

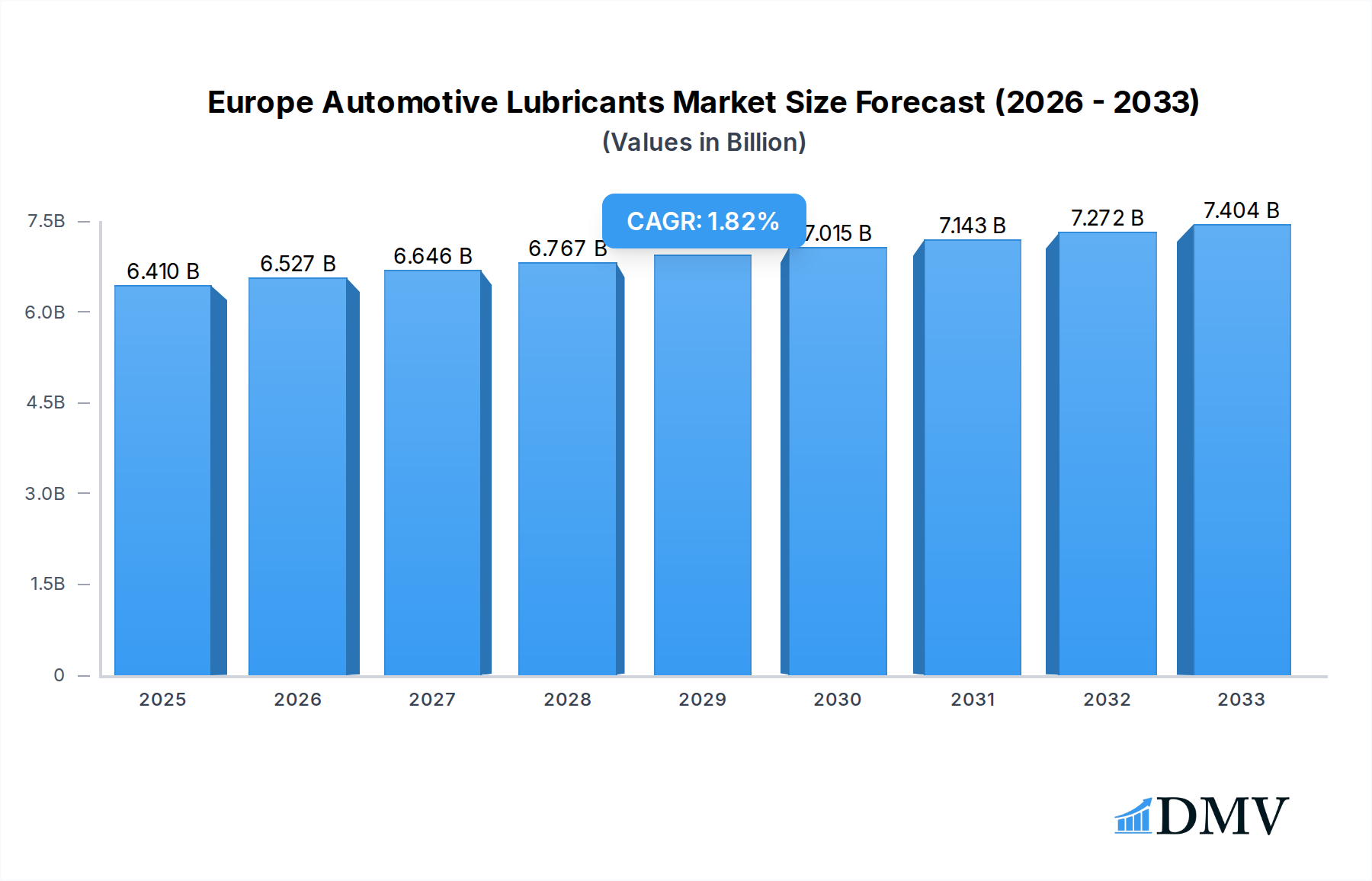

The European automotive lubricants market is projected to reach a robust USD 6.41 billion in 2025, demonstrating steady growth with a compound annual growth rate (CAGR) of 1.81% through 2033. This expansion is fueled by a combination of factors, including the increasing average age of the vehicle parc, leading to a higher demand for maintenance and replacement lubricants, and the persistent popularity of internal combustion engine vehicles. Furthermore, the growing adoption of advanced lubricant formulations, designed to enhance fuel efficiency and extend engine life, is a significant driver. The market is segmented across various vehicle types, with passenger vehicles holding a dominant share, followed by commercial vehicles and motorcycles. Product-wise, engine oils represent the largest segment, owing to their critical role in vehicle performance and longevity. This sustained demand underscores the essential nature of lubricants in maintaining the functionality and extending the lifespan of the vast European automotive fleet.

Europe Automotive Lubricants Market Market Size (In Billion)

Despite the overall positive outlook, the market faces certain constraints. Evolving emission standards and the accelerating transition towards electric vehicles (EVs) pose a long-term challenge, as EVs require different lubrication solutions. Additionally, fluctuating raw material prices, particularly for base oils and additives, can impact profitability and market pricing strategies. However, the continued presence of a significant internal combustion engine vehicle fleet, coupled with advancements in synthetic lubricant technology that offer superior protection and performance even in stringent operating conditions, will continue to support market growth. Key players like BP PLC (Castrol), CHEVRON CORPORATION, ExxonMobil Corporation, and Royal Dutch Shell Plc are actively investing in research and development to innovate and adapt to these changing market dynamics, focusing on high-performance and sustainable lubricant solutions.

Europe Automotive Lubricants Market Company Market Share

Here is an SEO-optimized, insightful report description for the Europe Automotive Lubricants Market, crafted with high-ranking keywords and adhering to all your specified requirements:

Europe Automotive Lubricants Market Market Composition & Trends

The Europe automotive lubricants market is a dynamic landscape shaped by rigorous environmental regulations, evolving vehicle technologies, and fierce competition among global and regional players. Market concentration is moderate, with key participants like Royal Dutch Shell Plc, ExxonMobil Corporation, and BP PLC (Castrol) holding significant shares. Innovation is driven by the demand for fuel-efficient, low-emission lubricants, including synthetic and bio-based formulations, critical for meeting Euro 7 standards and beyond. Regulatory frameworks, such as REACH and CLP, mandate stringent product safety and environmental impact assessments, influencing product development and market entry strategies. Substitute products, while limited in direct replacement for engine oils, are emerging in the form of advanced additive technologies and specialized fluids for electric vehicle (EV) powertrains. End-user profiles vary from large fleet operators seeking cost optimization and performance to individual consumers prioritizing brand reputation and advanced protection. Mergers and acquisitions (M&A) activity, while not a dominant feature, plays a role in market consolidation and technology acquisition. The total market value for automotive lubricants in Europe is projected to reach an estimated $XX billion by 2025, with a projected growth rate of XX% during the forecast period.

- Market Share Distribution: Dominated by major oil and gas corporations and specialized lubricant manufacturers.

- M&A Deal Values: Driven by strategic acquisitions for technology, market access, and product portfolio expansion.

- Innovation Catalysts: Stringent emission standards, growing EV adoption, and demand for extended drain intervals.

- Regulatory Landscapes: REACH, CLP, and evolving Euro emission standards significantly influence product formulation and market access.

- Substitute Products: Advancements in additive technology and specialized EV fluids.

- End-User Profiles: Fleet operators, OEMs, and retail consumers with diverse performance and cost expectations.

Europe Automotive Lubricants Market Industry Evolution

The Europe automotive lubricants market has witnessed a significant evolution driven by a confluence of technological advancements, stringent environmental mandates, and shifting consumer preferences. Historically, the market was dominated by conventional mineral-based lubricants, catering to internal combustion engine (ICE) vehicles with simpler engineering. However, the past decade has seen a dramatic acceleration in the adoption of advanced lubricant technologies. The continuous push for improved fuel economy and reduced emissions, spurred by legislative bodies and consumer awareness, has propelled the demand for high-performance synthetic and semi-synthetic engine oils. These advanced formulations offer superior thermal stability, enhanced wear protection, and extended drain intervals, directly contributing to lower operational costs and a reduced environmental footprint. The forecast period (2025–2033) is poised to witness even more profound transformations. The burgeoning electric vehicle (EV) segment, while not requiring traditional engine oils, introduces new demands for specialized coolants, transmission fluids, and greases designed for unique thermal management and driveline requirements. This shift presents both challenges and opportunities for established lubricant manufacturers, necessitating adaptation and innovation in product development.

Furthermore, the integration of advanced additive packages has become a critical differentiator. These additives are meticulously engineered to enhance lubricant performance across a wide range of operating conditions, from extreme temperatures to high pressure. They contribute to reduced friction, improved cleanliness, and enhanced protection against corrosion and oxidation, thereby extending the lifespan of critical engine and driveline components. The historical period (2019–2024) has already showcased this trend, with a discernible upward trajectory in the market share of premium synthetic lubricants. The base year (2025) represents a pivotal point, with the market exhibiting strong momentum towards sustainable and technologically advanced solutions. The study period (2019–2033) encapsulates this dynamic transition, from the dominance of ICE-centric lubricants to a diversified portfolio that increasingly accommodates the demands of hybrid and fully electric powertrains. This evolutionary path underscores the industry's resilience and its capacity to adapt to the transformative changes occurring within the automotive sector. The total market size is estimated to reach $XX billion in 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% from 2025 to 2033.

Leading Regions, Countries, or Segments in Europe Automotive Lubricants Market

The European automotive lubricants market is characterized by regional variations in demand, regulatory stringency, and technological adoption. Among the vehicle types, Passenger Vehicles consistently represent the largest segment, driven by the sheer volume of private car ownership across the continent. However, Commercial Vehicles present a significant growth opportunity due to their higher mileage, demanding operational environments, and the increasing adoption of advanced engine technologies designed for efficiency and reduced emissions. The Motorcycle segment, while smaller in overall volume, exhibits a distinct demand for specialized, high-performance lubricants tailored to the unique requirements of two-wheeled engines.

In terms of product type, Engine Oils remain the dominant category, accounting for a substantial portion of the market share. This is directly linked to the vast fleet of internal combustion engine vehicles still in operation. Nevertheless, the growth in electric vehicles is beginning to influence the demand for specialized Transmission & Gear Oils and novel Hydraulic Fluids designed for EV powertrains and associated systems. The increasing sophistication of automotive transmissions and drivelines across all vehicle types also fuels the demand for advanced transmission fluids. Greases, while a smaller segment, are crucial for various automotive components requiring long-term lubrication and protection against wear and corrosion.

Geographically, Germany, France, and the United Kingdom are the leading countries in terms of market size and value, owing to their large automotive manufacturing bases and significant vehicle parc. Regulatory support, such as ambitious CO2 reduction targets and incentives for low-emission vehicles, acts as a significant driver for advanced lubricant adoption in these regions. Investment trends in automotive manufacturing, particularly in areas focusing on electrification and autonomous driving, directly correlate with the demand for specialized lubricants. The European Union's unified regulatory framework, while fostering consistency, also presents a complex landscape for manufacturers to navigate. The overall market size is estimated at $XX billion in 2025.

- Dominant Vehicle Type: Passenger Vehicles, followed by Commercial Vehicles with robust growth potential.

- Key Product Categories: Engine Oils hold the largest share, with growing demand for Transmission & Gear Oils and specialized EV fluids.

- Leading Countries: Germany, France, United Kingdom, driven by large vehicle parc and OEM presence.

- Investment Trends: Significant investment in EV infrastructure and manufacturing capacity across major European economies.

- Regulatory Support: EU-wide emission standards and national incentives for low-emission technologies.

Europe Automotive Lubricants Market Product Innovations

The Europe automotive lubricants market is experiencing a surge in product innovations driven by the imperative for sustainability, enhanced performance, and the evolving needs of electric vehicles. Manufacturers are heavily investing in the development of low-viscosity synthetic engine oils that significantly improve fuel efficiency and reduce CO2 emissions, crucial for meeting stringent Euro 7 standards. Advanced additive technologies are now integral, offering superior wear protection, extended drain intervals, and optimized performance in extreme temperatures. For the burgeoning EV market, specialized dielectric coolants, advanced transmission fluids for e-axles, and high-performance greases are emerging, designed to manage thermal loads and ensure the longevity of electric powertrains. These innovations are characterized by their unique selling propositions: reduced friction coefficients, enhanced energy transfer capabilities, and superior material compatibility, paving the way for a new era of automotive lubrication. The total market value is estimated at $XX billion in 2025.

Propelling Factors for Europe Automotive Lubricants Market Growth

Several key factors are propelling the growth of the Europe automotive lubricants market. The ongoing transition to electric vehicles, while altering the composition of lubricants required, is driving demand for specialized fluids in powertrains and battery cooling systems. Stringent environmental regulations, particularly Euro 7 emission standards, are compelling automakers and lubricant manufacturers to develop more fuel-efficient and lower-emission lubricants, favoring advanced synthetic formulations. The increasing average age of vehicles in the European fleet also necessitates high-quality lubricants that can extend component life and maintain optimal performance. Furthermore, technological advancements in engine design and driveline systems are demanding lubricants with higher performance capabilities, such as improved thermal stability and wear resistance. The market is projected to reach $XX billion by 2025.

- EV Transition: Increasing adoption of electric vehicles necessitates specialized coolants, transmission fluids, and greases.

- Stringent Emission Standards: Euro 7 and other regulations are driving demand for fuel-efficient and low-emission lubricants.

- Aging Vehicle Parc: Older vehicles require high-quality lubricants for continued optimal performance and longevity.

- Technological Advancements: Sophisticated engine and driveline designs demand high-performance lubricant solutions.

Obstacles in the Europe Automotive Lubricants Market Market

Despite robust growth drivers, the Europe automotive lubricants market faces several obstacles. The rapid shift towards electric vehicles poses a significant challenge to traditional engine oil manufacturers, requiring substantial R&D investment to pivot to EV-specific fluid technologies. Intense competition among established players and emerging brands, coupled with price sensitivity in certain market segments, can compress profit margins. Supply chain disruptions, exacerbated by geopolitical events and raw material price volatility, can impact production costs and availability. Moreover, navigating the complex and evolving regulatory landscape across different European nations can be a substantial hurdle for market entry and product compliance. The market is valued at $XX billion in 2025.

- EV Disruption: Declining demand for traditional engine oils due to EV adoption.

- Intense Competition: Price wars and margin pressure from numerous market participants.

- Supply Chain Volatility: Geopolitical risks and raw material price fluctuations impacting production.

- Regulatory Complexity: Navigating diverse national and EU-wide compliance requirements.

Future Opportunities in Europe Automotive Lubricants Market

The Europe automotive lubricants market is ripe with future opportunities. The burgeoning electric vehicle market presents a significant avenue for growth in specialized EV fluids, including dielectric coolants, e-axle lubricants, and advanced greases. The increasing demand for sustainable and bio-based lubricants, driven by consumer preference and corporate ESG initiatives, offers a distinct niche for environmentally conscious products. The aftermarket segment, particularly for premium and specialty lubricants, is expected to expand as vehicle owners seek to maintain their vehicles for longer. Furthermore, advancements in additive technology are creating opportunities for hyper-specialized lubricants catering to niche applications and high-performance vehicles. The market is projected to be valued at $XX billion by 2025.

- EV Fluid Development: Significant growth potential in lubricants for electric powertrains.

- Sustainable Lubricants: Demand for bio-based and eco-friendly formulations.

- Premium Aftermarket: Growing opportunity for high-performance and specialty lubricants.

- Additive Technology: Innovation in specialized additives for niche applications.

Major Players in the Europe Automotive Lubricants Market Ecosystem

- BP PLC (Castrol)

- CHEVRON CORPORATION

- Eni SpA

- ExxonMobil Corporation

- FUCHS

- Gazprom

- LIQUI MOLY

- LUKOIL

- Motul

- PETRONAS Lubricants International

- Rosneft

- Royal Dutch Shell Plc

- TotalEnergie

Key Developments in Europe Automotive Lubricants Market Industry

- January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions. This strategic restructuring is expected to enhance focus on specific market segments and potentially lead to targeted product development and market strategies within the lubricants sector.

- September 2021: Lukoil Group and Daimler AG, one of the world's major automobile manufacturers, expanded their relationship in Lukoil lubricants' first fill supplies for the brand's premium passenger cars' engines. Low-viscosity Lukoil Genesis engine oil, developed by LLK-International (PJSC LUKOIL wholly owned subsidiary) for modern gasoline and diesel engines of the car manufacturer in compliance with one of its newest first fill standards, will be added to the product portfolio. In comparison to the previous generation, the new product delivered dependable engine protection and increased fuel economy. This development highlights the increasing emphasis on fuel efficiency and advanced engine protection in OEM partnerships.

- June 2021: TotalEnergies and Stellantis group renewed their partnership for cooperation across different segments. Along with the renewal of partnerships with Peugeot, Citroën, and DS Automobiles, the new collaboration extends to Opel, and Vauxhall as well. This partnership includes the development and innovation of lubricants, first-fill in Stellantis group vehicles, recommendation of Quartz lubricants, and shared usage of charging stations operated by TotalEnergies, among others. This renewal underscores the importance of strategic alliances between energy companies and automotive giants for lubricant development, OEM approvals, and integrated service offerings.

Strategic Europe Automotive Lubricants Market Market Forecast

The strategic Europe automotive lubricants market forecast points towards sustained growth, primarily fueled by the escalating adoption of electric vehicles and the continuous demand for advanced, fuel-efficient lubricants for internal combustion engines. The market is set to expand significantly as manufacturers invest heavily in innovative fluid technologies to meet stringent emission regulations and the unique requirements of EV powertrains. Strategic partnerships between lubricant producers and automotive OEMs will remain crucial for securing first-fill approvals and driving market penetration. Opportunities lie in the development of sustainable, bio-based lubricants and specialized fluids for e-mobility, alongside maintaining a strong presence in the traditional engine oil segment for the vast existing vehicle parc. The market is projected to reach $XX billion by 2025 and grow steadily through 2033.

Europe Automotive Lubricants Market Segmentation

-

1. Vehicle Type

- 1.1. Commercial Vehicles

- 1.2. Motorcycles

- 1.3. Passenger Vehicles

-

2. Product Type

- 2.1. Engine Oils

- 2.2. Greases

- 2.3. Hydraulic Fluids

- 2.4. Transmission & Gear Oils

Europe Automotive Lubricants Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Automotive Lubricants Market Regional Market Share

Geographic Coverage of Europe Automotive Lubricants Market

Europe Automotive Lubricants Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Commercial Vehicles

- 5.1.2. Motorcycles

- 5.1.3. Passenger Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Engine Oils

- 5.2.2. Greases

- 5.2.3. Hydraulic Fluids

- 5.2.4. Transmission & Gear Oils

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Europe Automotive Lubricants Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Commercial Vehicles

- 6.1.2. Motorcycles

- 6.1.3. Passenger Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Engine Oils

- 6.2.2. Greases

- 6.2.3. Hydraulic Fluids

- 6.2.4. Transmission & Gear Oils

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 BP PLC (Castrol)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CHEVRON CORPORATION

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Eni SpA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ExxonMobil Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FUCHS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Gazprom

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 LIQUI MOLY

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 LUKOIL

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Motul

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 PETRONAS Lubricants International

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Rosneft

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Royal Dutch Shell Plc

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TotalEnergie

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 BP PLC (Castrol)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Automotive Lubricants Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Lubricants Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Lubricants Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 2: Europe Automotive Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Europe Automotive Lubricants Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Automotive Lubricants Market Revenue billion Forecast, by Vehicle Type 2020 & 2033

- Table 5: Europe Automotive Lubricants Market Revenue billion Forecast, by Product Type 2020 & 2033

- Table 6: Europe Automotive Lubricants Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: France Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Automotive Lubricants Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Lubricants Market?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the Europe Automotive Lubricants Market?

Key companies in the market include BP PLC (Castrol), CHEVRON CORPORATION, Eni SpA, ExxonMobil Corporation, FUCHS, Gazprom, LIQUI MOLY, LUKOIL, Motul, PETRONAS Lubricants International, Rosneft, Royal Dutch Shell Plc, TotalEnergie.

3. What are the main segments of the Europe Automotive Lubricants Market?

The market segments include Vehicle Type, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Largest Segment By Vehicle Type : Passenger Vehicles.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

January 2022: Effective April 1, ExxonMobil Corporation was organized along three business lines - ExxonMobil Upstream Company, ExxonMobil Product Solutions and ExxonMobil Low Carbon Solutions.September 2021: Lukoil Group and Daimler AG, one of the world's major automobile manufacturers, expanded their relationship in Lukoil lubricants' first fill supplies for the brand's premium passenger cars' engines. Low-viscosity Lukoil Genesis engine oil, developed by LLK-International (PJSC LUKOIL wholly owned subsidiary) for modern gasoline and diesel engines of the car manufacturer in compliance with one of its newest first fill standards, will be added to the product portfolio. In comparison to the previous generation, the new product delivered dependable engine protection and increased fuel economy.June 2021: TotalEnergies and Stellantis group renewed their partnership for cooperation across different segments. Along with the renewal of partnerships with Peugeot, Citroën, and DS Automobiles, the new collaboration extends to Opel, and Vauxhall as well. This partnership includes the development and innovation of lubricants, first-fill in Stellantis group vehicles, recommendation of Quartz lubricants, and shared usage of charging stations operated by TotalEnergies, among others.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Lubricants Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Lubricants Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Lubricants Market?

To stay informed about further developments, trends, and reports in the Europe Automotive Lubricants Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence