Key Insights

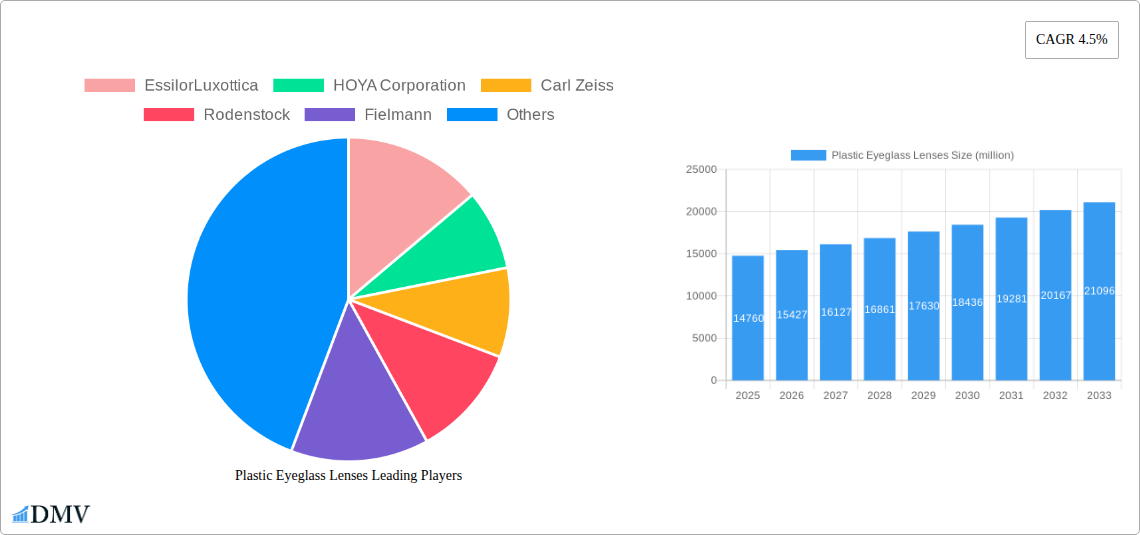

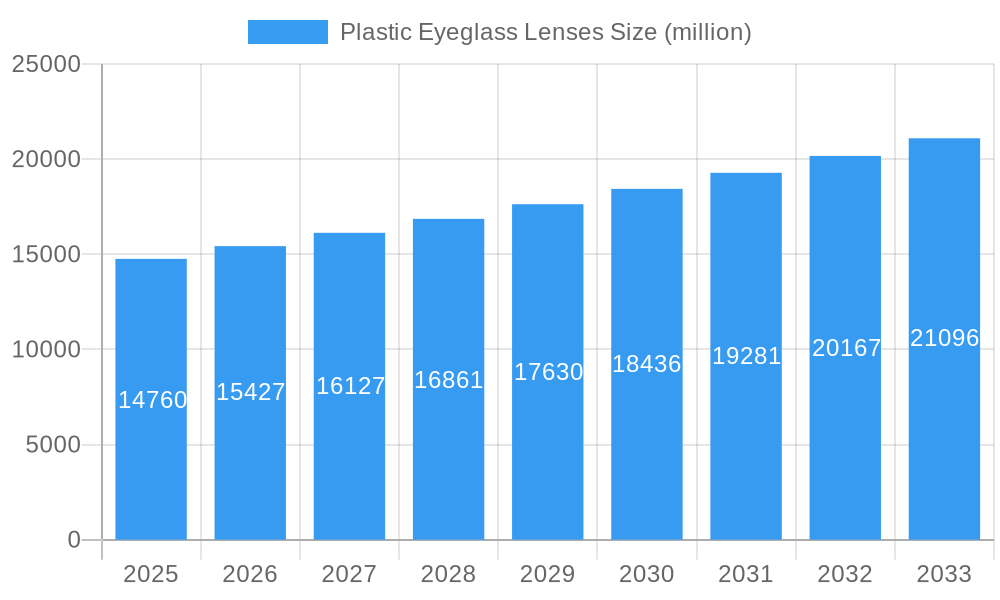

The global plastic eyeglass lens market is poised for robust expansion, projected to reach a significant valuation of approximately USD 14,760 million. This growth is underpinned by a healthy Compound Annual Growth Rate (CAGR) of 4.5%, indicating sustained momentum throughout the forecast period of 2025-2033. This upward trajectory is primarily driven by increasing global awareness of eye health, a rising prevalence of vision-related ailments, and the escalating demand for corrective eyewear. Furthermore, advancements in lens technology, including the development of thinner, lighter, and more scratch-resistant materials, are continuously enhancing product appeal and driving consumer adoption. The increasing disposable income in emerging economies also plays a crucial role, making corrective eyewear more accessible to a broader population and contributing to market expansion.

Plastic Eyeglass Lenses Market Size (In Billion)

The market landscape for plastic eyeglass lenses is characterized by a diverse range of applications, from everyday prescription glasses and specialized safety glasses to fashion-forward sunglasses. This broad applicability ensures a consistent demand across various consumer segments. Within the lens types, the market is segmented by refractive index, catering to a wide spectrum of visual needs. While normal and mid-refractive index lenses remain staples, there's a discernible trend towards higher refractive index materials (1.64-1.74 and above) due to their ability to create thinner and more aesthetically pleasing lenses for stronger prescriptions, addressing concerns about lens thickness and weight. Key players like EssilorLuxottica, HOYA Corporation, and Carl Zeiss are at the forefront, investing heavily in research and development to introduce innovative products and expand their global reach. However, factors such as the high cost of advanced lens materials and the potential for increased adoption of alternative vision correction methods like contact lenses or refractive surgery could present moderate challenges to the market's unhindered growth.

Plastic Eyeglass Lenses Company Market Share

Plastic Eyeglass Lenses Market Composition & Trends

The global plastic eyeglass lenses market is characterized by a dynamic interplay of innovation, strategic collaborations, and evolving consumer preferences. Market concentration is moderately high, with key players like EssilorLuxottica and HOYA Corporation commanding significant market shares, estimated at over 30% and 15% respectively. The market's growth is propelled by continuous technological advancements, particularly in lens materials and coatings, aimed at enhancing optical performance, durability, and wearer comfort. Regulatory landscapes, while varying by region, primarily focus on safety standards and material certifications, influencing product development and market entry strategies. Substitute products, such as glass lenses, hold a diminishing share due to the inherent advantages of plastic, including lighter weight, shatter resistance, and greater design flexibility. End-user profiles are diverse, encompassing individuals requiring vision correction (prescription glasses), those in hazardous environments (safety glasses), and consumers seeking UV protection and style (sunglasses). Mergers and acquisitions (M&A) activities, while not exhaustive, have played a role in consolidating market presence and expanding product portfolios. For instance, a recent M&A deal in the mid-refractive index segment involved a value of approximately 500 million, indicating strategic consolidation efforts. Understanding these interwoven factors is crucial for navigating the competitive terrain and capitalizing on emerging opportunities within the plastic eyeglass lenses industry.

Plastic Eyeglass Lenses Industry Evolution

The plastic eyeglass lenses industry has witnessed a remarkable evolution driven by a confluence of technological breakthroughs, escalating consumer demand for enhanced visual experiences, and a growing awareness of eye health. Over the study period from 2019 to 2033, this sector has consistently demonstrated robust growth trajectories. The base year of 2025 marks a significant point, with an estimated market value reaching over 25,000 million. This growth has been fueled by a persistent drive towards innovation in lens materials, including the development of lighter, thinner, and more impact-resistant plastics. Technological advancements have moved beyond basic refractive correction to incorporate sophisticated coatings that offer scratch resistance, anti-reflective properties, UV protection, and blue light filtering, directly addressing the increasing digital screen time of global populations.

Shifting consumer demands have been a primary catalyst for this evolution. Modern consumers are not only seeking improved vision but also demand aesthetically pleasing, comfortable, and technologically advanced eyewear. This has led to a surge in the popularity of high and ultra-high refractive index lenses, which allow for thinner and lighter lenses, particularly for individuals with strong prescriptions. The adoption metrics for these advanced lens types have seen a steady increase, with an estimated 15% year-over-year growth in the premium lens segment. Furthermore, the growing emphasis on preventative eye care and the increasing prevalence of refractive errors globally have bolstered the demand for prescription eyewear, a cornerstone application for plastic lenses.

The forecast period of 2025–2033 projects a continued upward trend, with an anticipated compound annual growth rate (CAGR) of approximately 7%. This sustained growth is expected to be driven by further innovations in material science, personalized lens designs based on individual visual needs and lifestyle, and the expanding reach of affordable and advanced eyewear solutions in emerging economies. The industry's ability to adapt to these evolving demands, coupled with ongoing research and development, ensures its continued dynamism and importance within the broader optical industry. The historical period from 2019 to 2024 has laid a strong foundation, marked by significant investments in research and a growing consumer appreciation for the benefits of plastic lenses.

Leading Regions, Countries, or Segments in Plastic Eyeglass Lenses

The plastic eyeglass lenses market is a global enterprise, but its dominance and growth drivers are concentrated in specific regions and segments. Among the applications, Prescription Glasses stand out as the largest and most influential segment, driven by the persistent global demand for vision correction. This segment alone accounted for an estimated 60% of the total market revenue in the base year of 2025, with a projected market size of over 15,000 million. The increasing prevalence of myopia, hyperopia, and astigmatism, coupled with an aging population experiencing presbyopia, directly fuels the demand for prescription lenses.

Within the Types of plastic eyeglass lenses, the Normal Refractive Index (1.48-1.54) segment currently holds a substantial market share due to its cost-effectiveness and widespread availability. However, the Mid Refractive Index (1.54-1.64) and High Refractive Index (1.64-1.74) segments are experiencing accelerated growth, driven by consumer preference for thinner, lighter, and more aesthetically pleasing lenses, especially for those with moderate to high prescriptions. The Ultra High Refractive Index (1.74 and above) segment, while smaller, represents the premium end of the market, catering to individuals with very high prescriptions who prioritize ultimate lens thinness and weight reduction. The growth in this segment is estimated to be around 10% annually.

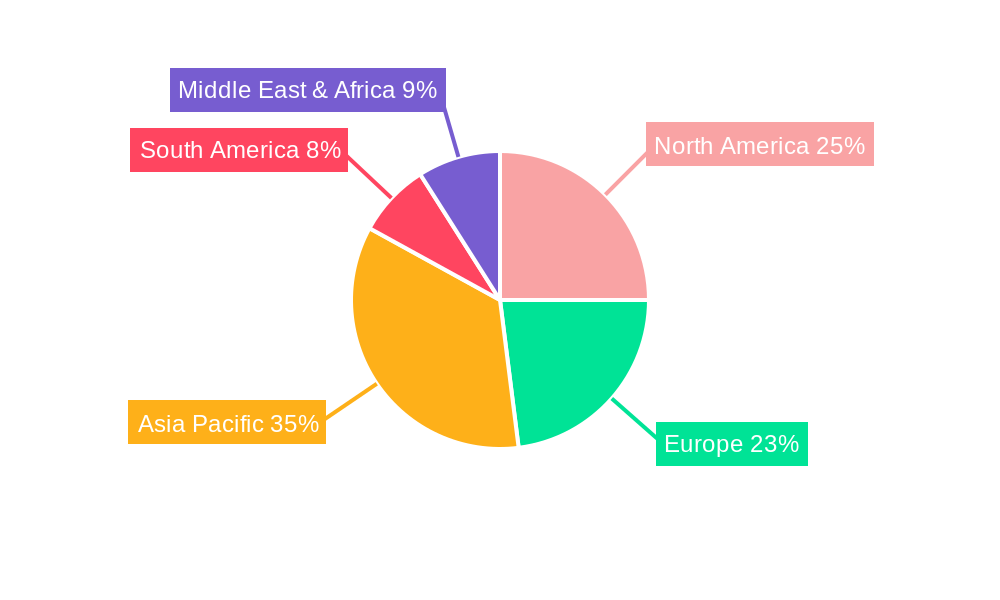

Geographically, North America and Europe have historically been dominant regions, characterized by high disposable incomes, a mature optical market, and a strong emphasis on advanced eyewear technology. These regions exhibit significant investment trends in research and development, leading to early adoption of new lens materials and coatings. Regulatory support for vision care, including insurance coverage for eyewear, further bolsters their market leadership.

However, the Asia-Pacific region is emerging as the fastest-growing market, projected to witness a CAGR of over 8% during the forecast period. This growth is propelled by a rapidly expanding middle class, increasing awareness of eye health, and a growing demand for corrective eyewear. Countries like China and India, with their large populations and increasing disposable incomes, are pivotal to this expansion. Investment trends in this region are shifting towards manufacturing capabilities and accessible pricing strategies.

Key drivers contributing to segment and regional dominance include:

- Technological Advancements: Continuous innovation in lens materials and coatings enhances performance and wearer comfort.

- Rising Disposable Incomes: Particularly in emerging economies, enabling greater spending on optical products.

- Increasing Prevalence of Vision Impairments: Driven by factors such as aging populations and increased digital screen usage.

- Government Initiatives & Healthcare Policies: Supporting eye care access and affordability.

- Growing Fashion Consciousness: Leading to demand for stylish and personalized eyewear.

Plastic Eyeglass Lenses Product Innovations

Product innovation in plastic eyeglass lenses is primarily focused on enhancing optical clarity, improving wearer comfort, and integrating advanced functionalities. Key developments include the introduction of thinner and lighter lens materials across all refractive index categories, particularly for high and ultra-high refractive index lenses, significantly reducing the aesthetic impact for individuals with strong prescriptions. The integration of advanced coatings, such as hydrophobic, oleophobic, and anti-fog treatments, has improved lens durability and ease of cleaning. Furthermore, the incorporation of blue light filtering technology into lenses is a significant innovation, addressing growing concerns about digital eye strain. Performance metrics have seen remarkable improvements, with enhanced scratch resistance surpassing 30% in new formulations and a reduction in lens weight by up to 20% for comparable prescriptions.

Propelling Factors for Plastic Eyeglass Lenses Growth

The plastic eyeglass lenses market is propelled by several key factors, including the escalating global prevalence of refractive errors such as myopia and presbyopia, driven by an aging population and increased screen time. Technological advancements in lens materials and coatings, offering superior optical clarity, durability, and comfort, are crucial growth catalysts. The rising disposable incomes in emerging economies are expanding the consumer base for corrective eyewear. Furthermore, increased awareness regarding eye health and preventative care encourages proactive adoption of eyeglasses. Regulatory support in various regions, promoting access to vision correction services, also contributes significantly to market expansion.

Obstacles in the Plastic Eyeglass Lenses Market

Despite robust growth, the plastic eyeglass lenses market faces certain obstacles. Intense competition among manufacturers, including numerous players like EssilorLuxottica, HOYA Corporation, Carl Zeiss, Rodenstock, and Fielmann, can lead to price pressures and reduced profit margins, especially in the commoditized normal refractive index segment. Supply chain disruptions, as seen in recent global events, can impact raw material availability and production costs, potentially affecting market stability. While plastic is generally safe, concerns regarding the environmental impact of plastic production and disposal can lead to regulatory scrutiny and consumer demand for more sustainable alternatives. Fluctuations in the cost of raw materials, such as polycarbonate and CR-39, can also present a financial challenge, with potential cost increases of up to 10% impacting profitability.

Future Opportunities in Plastic Eyeglass Lenses

Emerging opportunities in the plastic eyeglass lenses market are diverse and promising. The increasing demand for specialized lenses, such as those offering enhanced UV protection, blue light filtering for digital device users, and photochromic capabilities, presents significant growth potential. The expansion of e-commerce platforms for eyewear sales offers a wider reach to consumers, particularly in underserved regions. Technological advancements in personalized lens design, utilizing AI and advanced optics to create bespoke solutions for individual visual needs, represent a future frontier. Furthermore, the growing demand for lightweight, impact-resistant lenses for sports and safety applications continues to drive innovation and market penetration. The development of advanced antimicrobial coatings for lenses is also an emerging opportunity, addressing evolving hygiene concerns.

Major Players in the Plastic Eyeglass Lenses Ecosystem

- EssilorLuxottica

- HOYA Corporation

- Carl Zeiss

- Rodenstock

- Fielmann

- Chemiglas Corp

- Nikon

- Huiding Optical

- Tokai Optical

- GKB Ophthalmics

- Shanghai Conant Optical

- Shanghai Mingyue

- Jiangsu Wanxin Optics

- Jiangsu Hongchen Optical

Key Developments in Plastic Eyeglass Lenses Industry

- 2023/05: EssilorLuxottica launches a new range of high-index lenses with enhanced scratch resistance, aiming to capture a larger share of the premium market.

- 2023/11: HOYA Corporation announces a strategic partnership with a leading technology firm to develop AI-powered lens personalization solutions.

- 2024/01: Carl Zeiss introduces an advanced anti-fog coating for its eyeglass lenses, addressing a common consumer pain point.

- 2024/03: Rodenstock invests heavily in R&D for eco-friendly plastic lens manufacturing processes, signaling a commitment to sustainability.

- 2024/07: Fielmann expands its in-house lens production capabilities, aiming to reduce lead times and improve cost-efficiency.

- 2024/10: Chemiglas Corp develops a novel shatterproof plastic lens material, enhancing safety for prescription and safety glasses.

Strategic Plastic Eyeglass Lenses Market Forecast

The strategic plastic eyeglass lenses market forecast indicates sustained robust growth driven by innovation and increasing global demand for vision correction. The expanding market for prescription glasses, particularly with the rise of high and ultra-high refractive index lenses, will continue to be a primary revenue driver. Growth catalysts include the development of advanced lens coatings for enhanced functionality and durability, alongside a growing consumer focus on digital eye strain and blue light protection. Emerging economies are poised to become significant growth engines, fueled by rising disposable incomes and increased awareness of eye health. Strategic investments in research and development, coupled with efficient distribution networks, will be crucial for market players to capitalize on these opportunities and maintain a competitive edge in the dynamic global eyewear landscape.

Plastic Eyeglass Lenses Segmentation

-

1. Application

- 1.1. Prescription Glasses

- 1.2. Safety Glasses

- 1.3. Sunglasses

-

2. Types

- 2.1. Normal Refractive Index: 1.48-1.54

- 2.2. Mid Refractive Index: 1.54-1.64

- 2.3. High Refractive Index: 1.64-1.74

- 2.4. Ultra High Refractive Index: 1.74 and above

Plastic Eyeglass Lenses Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plastic Eyeglass Lenses Regional Market Share

Geographic Coverage of Plastic Eyeglass Lenses

Plastic Eyeglass Lenses REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Prescription Glasses

- 5.1.2. Safety Glasses

- 5.1.3. Sunglasses

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Normal Refractive Index: 1.48-1.54

- 5.2.2. Mid Refractive Index: 1.54-1.64

- 5.2.3. High Refractive Index: 1.64-1.74

- 5.2.4. Ultra High Refractive Index: 1.74 and above

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Prescription Glasses

- 6.1.2. Safety Glasses

- 6.1.3. Sunglasses

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Normal Refractive Index: 1.48-1.54

- 6.2.2. Mid Refractive Index: 1.54-1.64

- 6.2.3. High Refractive Index: 1.64-1.74

- 6.2.4. Ultra High Refractive Index: 1.74 and above

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Prescription Glasses

- 7.1.2. Safety Glasses

- 7.1.3. Sunglasses

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Normal Refractive Index: 1.48-1.54

- 7.2.2. Mid Refractive Index: 1.54-1.64

- 7.2.3. High Refractive Index: 1.64-1.74

- 7.2.4. Ultra High Refractive Index: 1.74 and above

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Prescription Glasses

- 8.1.2. Safety Glasses

- 8.1.3. Sunglasses

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Normal Refractive Index: 1.48-1.54

- 8.2.2. Mid Refractive Index: 1.54-1.64

- 8.2.3. High Refractive Index: 1.64-1.74

- 8.2.4. Ultra High Refractive Index: 1.74 and above

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Prescription Glasses

- 9.1.2. Safety Glasses

- 9.1.3. Sunglasses

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Normal Refractive Index: 1.48-1.54

- 9.2.2. Mid Refractive Index: 1.54-1.64

- 9.2.3. High Refractive Index: 1.64-1.74

- 9.2.4. Ultra High Refractive Index: 1.74 and above

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Plastic Eyeglass Lenses Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Prescription Glasses

- 10.1.2. Safety Glasses

- 10.1.3. Sunglasses

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Normal Refractive Index: 1.48-1.54

- 10.2.2. Mid Refractive Index: 1.54-1.64

- 10.2.3. High Refractive Index: 1.64-1.74

- 10.2.4. Ultra High Refractive Index: 1.74 and above

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 EssilorLuxottica

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 HOYA Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Carl Zeiss

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Rodenstock

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fielmann

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Chemiglas Corp

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nikon

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Huiding Optical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Tokai Optical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 GKB Ophthalmics

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shanghai Conant Optical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Shanghai Mingyue

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Jiangsu Wanxin Optics

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Jiangsu Hongchen Optical

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 EssilorLuxottica

List of Figures

- Figure 1: Global Plastic Eyeglass Lenses Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Plastic Eyeglass Lenses Revenue (million), by Application 2025 & 2033

- Figure 3: North America Plastic Eyeglass Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Plastic Eyeglass Lenses Revenue (million), by Types 2025 & 2033

- Figure 5: North America Plastic Eyeglass Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Plastic Eyeglass Lenses Revenue (million), by Country 2025 & 2033

- Figure 7: North America Plastic Eyeglass Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Plastic Eyeglass Lenses Revenue (million), by Application 2025 & 2033

- Figure 9: South America Plastic Eyeglass Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Plastic Eyeglass Lenses Revenue (million), by Types 2025 & 2033

- Figure 11: South America Plastic Eyeglass Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Plastic Eyeglass Lenses Revenue (million), by Country 2025 & 2033

- Figure 13: South America Plastic Eyeglass Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Plastic Eyeglass Lenses Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Plastic Eyeglass Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Plastic Eyeglass Lenses Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Plastic Eyeglass Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Plastic Eyeglass Lenses Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Plastic Eyeglass Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Plastic Eyeglass Lenses Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Plastic Eyeglass Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Plastic Eyeglass Lenses Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Plastic Eyeglass Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Plastic Eyeglass Lenses Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Plastic Eyeglass Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Plastic Eyeglass Lenses Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Plastic Eyeglass Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Plastic Eyeglass Lenses Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Plastic Eyeglass Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Plastic Eyeglass Lenses Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Plastic Eyeglass Lenses Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Plastic Eyeglass Lenses Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Plastic Eyeglass Lenses Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Plastic Eyeglass Lenses Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Plastic Eyeglass Lenses Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Plastic Eyeglass Lenses Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Plastic Eyeglass Lenses Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Plastic Eyeglass Lenses Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Plastic Eyeglass Lenses Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Plastic Eyeglass Lenses Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plastic Eyeglass Lenses?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Plastic Eyeglass Lenses?

Key companies in the market include EssilorLuxottica, HOYA Corporation, Carl Zeiss, Rodenstock, Fielmann, Chemiglas Corp, Nikon, Huiding Optical, Tokai Optical, GKB Ophthalmics, Shanghai Conant Optical, Shanghai Mingyue, Jiangsu Wanxin Optics, Jiangsu Hongchen Optical.

3. What are the main segments of the Plastic Eyeglass Lenses?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 14760 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plastic Eyeglass Lenses," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plastic Eyeglass Lenses report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plastic Eyeglass Lenses?

To stay informed about further developments, trends, and reports in the Plastic Eyeglass Lenses, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence