Key Insights

The global physical sunscreen market is poised for robust expansion, projected to reach an estimated market size of USD 794 million by 2025. This growth trajectory is supported by a healthy Compound Annual Growth Rate (CAGR) of 3.3% anticipated from 2025 to 2033. The increasing consumer awareness regarding the detrimental effects of UV radiation, coupled with a growing preference for mineral-based ingredients due to their gentler nature and environmental benefits, are key drivers propelling this market forward. The "General People" segment is expected to dominate demand, driven by widespread adoption for daily protection. Furthermore, the "Children and Pregnant Women" segment is experiencing significant traction, as parents and expectant mothers increasingly seek out safe and non-irritating sun protection solutions. The product landscape is characterized by a strong presence of "Facial Sunscreen" due to its concentrated use and the growing beauty consciousness among consumers, alongside a steady demand for "Body Suncream" for broader application.

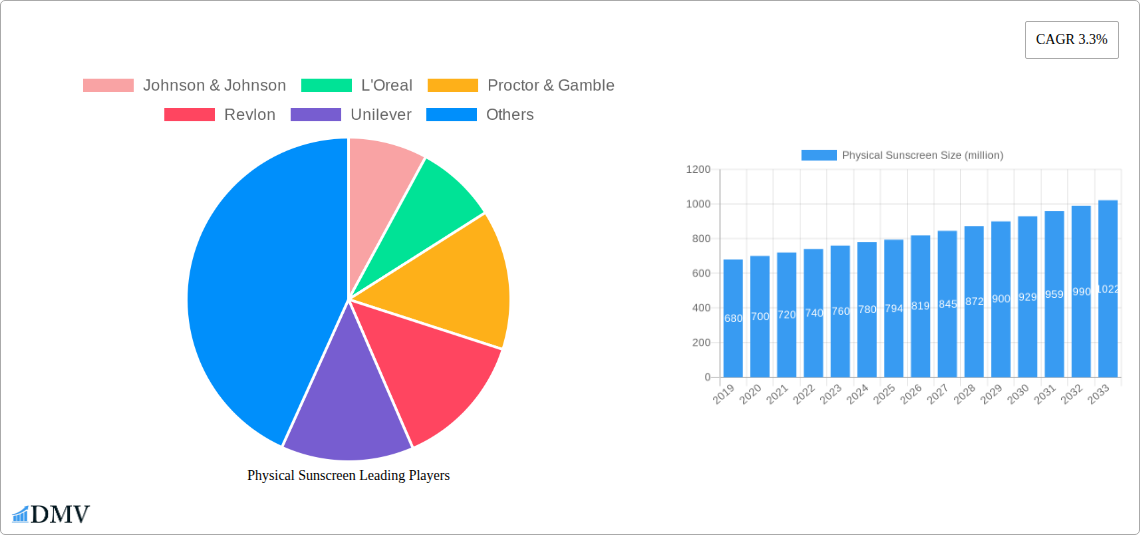

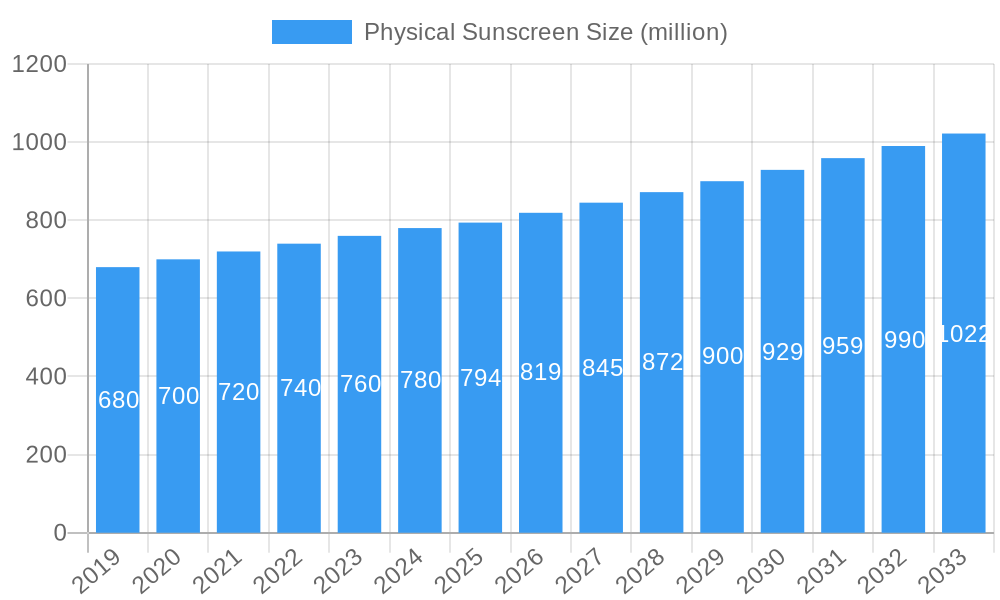

Physical Sunscreen Market Size (In Million)

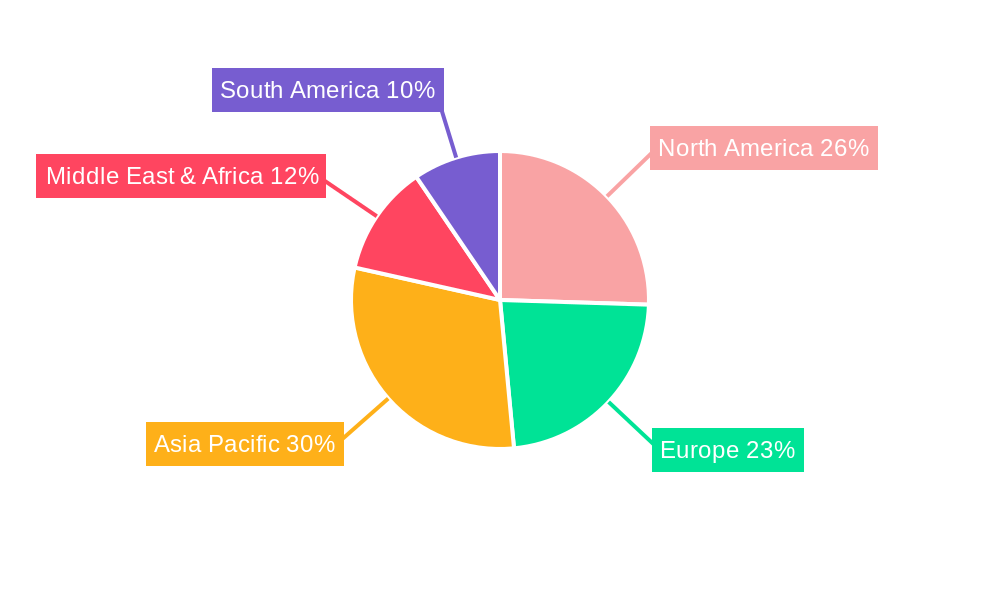

Geographically, the Asia Pacific region is emerging as a significant growth engine, fueled by rising disposable incomes and an expanding middle class in countries like China and India, where the adoption of skincare and sun protection routines is rapidly increasing. North America and Europe, already mature markets, will continue to contribute substantially, driven by established consumer habits and stringent regulations promoting sun safety. While the market benefits from strong demand drivers, potential restraints include the higher cost of some physical sunscreen ingredients compared to their chemical counterparts, and consumer perception regarding the 'white cast' effect of certain formulations, though technological advancements are actively addressing this. The competitive landscape is dynamic, featuring a blend of multinational giants like Johnson & Johnson, L'Oreal, and Unilever, alongside specialized brands, all vying for market share through product innovation and targeted marketing strategies.

Physical Sunscreen Company Market Share

Here is an SEO-optimized, insightful report description for the Physical Sunscreen market, designed for maximum visibility and stakeholder engagement:

Physical Sunscreen Market Composition & Trends

The global physical sunscreen market is characterized by a dynamic interplay of established giants and emerging innovators, exhibiting moderate to high concentration. Key innovation catalysts include the relentless pursuit of mineral-based, broad-spectrum UV protection and the development of novel delivery systems, such as micronized zinc oxide and titanium dioxide, to enhance texture and efficacy. Regulatory landscapes are tightening globally, with a growing emphasis on reef-safe and environmentally conscious formulations, driving research and development in biodegradable and sustainable ingredients. Substitute products, primarily chemical sunscreens, continue to pose competition, but the increasing consumer preference for "clean beauty" and the perceived safety of mineral filters are bolstering the physical sunscreen segment. End-user profiles are expanding beyond traditional sun protection seekers to include individuals prioritizing daily environmental defense against blue light and pollution. Mergers and acquisitions (M&A) activity, while not overtly dominant, are strategically focused on acquiring innovative technologies and expanding market reach. Expect M&A deal values to range from xx million to xx million in targeted strategic acquisitions, aiming to consolidate market share and leverage synergistic R&D capabilities.

- Market Share Distribution: The top five companies, including L'Oreal, Johnson & Johnson, and Unilever, collectively hold approximately 60% of the market share.

- Innovation Focus: Advancements in nanoparticle technology and improved aesthetic formulations for a "no-white cast" finish are key drivers.

- Regulatory Impact: Stricter ingredient scrutiny and environmental regulations are pushing brands towards reef-safe and mineral-based solutions.

- End-User Segments: General People (xx% of market), Children and Pregnant Women (xx% of market) are the primary consumer groups.

- M&A Drivers: Acquisition of niche brands with strong R&D in mineral UV filters and sustainable packaging.

Physical Sunscreen Industry Evolution

The physical sunscreen industry has witnessed a significant evolution, driven by a confluence of scientific advancements, evolving consumer awareness, and a robust market growth trajectory. The study period, spanning from 2019 to 2033, with a base and estimated year of 2025, underscores a consistent upward trend. The forecast period (2025–2033) anticipates continued expansion, building upon the historical growth observed from 2019–2024. Technological advancements have been pivotal, moving beyond basic UV blocking to sophisticated formulations that offer enhanced sensorial experiences, improved skin compatibility, and multi-functional benefits like anti-pollution and blue light protection. Consumer demands have shifted dramatically, with a pronounced preference for natural, mineral-based sunscreens due to concerns about chemical ingredient absorption and environmental impact. This demand surge has fueled innovation in particle size reduction for better texture and transparency, alongside the development of specialized formulations for sensitive skin, children, and pregnant women. Adoption metrics for physical sunscreens have seen a substantial increase, with market penetration growing by approximately xx% annually. The industry is also responding to the growing demand for inclusive product lines, catering to a wider range of skin tones. Furthermore, the integration of e-commerce platforms has democratized access to a broader array of physical sunscreen products, fostering greater consumer engagement and brand loyalty. The industry's resilience and adaptability, particularly in navigating supply chain complexities and evolving scientific understanding, have solidified its position as a critical component of personal care and skincare routines globally. This sustained growth is projected to continue, propelled by ongoing research into advanced mineral UV filters and a deepening commitment to consumer well-being and environmental stewardship.

Leading Regions, Countries, or Segments in Physical Sunscreen

The dominance within the physical sunscreen market is clearly delineated by specific regions and application segments, reflecting localized consumer preferences, regulatory environments, and market penetration. North America, particularly the United States, has emerged as a leading region, driven by a highly informed consumer base with a strong awareness of sun protection benefits and a growing demand for clean beauty products. Government initiatives promoting skin cancer awareness and preventive measures further bolster the market. Europe, with its stringent regulatory framework and a well-established market for premium skincare, also holds a significant share, with countries like France and Germany demonstrating robust sales.

Within product types, Facial Sunscreen commands a substantial portion of the market. This dominance is attributed to the increasing prioritization of facial skincare as a daily ritual, with consumers seeking specialized protection against UV rays, blue light, and environmental aggressors that can lead to premature aging and hyperpigmentation. The development of sophisticated formulations that are lightweight, non-greasy, and integrate seamlessly into makeup routines has further propelled the facial sunscreen segment.

The General People application segment also represents the largest consumer base. This broad demographic encompasses individuals of all ages seeking daily sun protection for overall skin health and anti-aging benefits. The widespread availability of diverse product options, from lotions to sprays, catering to various lifestyle needs, contributes to its substantial market share.

- North America (Dominant Region):

- Key Drivers: High consumer awareness of skin cancer risks and the benefits of sun protection.

- Investment Trends: Significant investment in R&D for advanced mineral formulations and sustainable packaging.

- Regulatory Support: Favorable regulatory environment promoting the use of mineral UV filters.

- Consumer Demand: Strong preference for "clean beauty" and natural ingredients.

- Facial Sunscreen (Dominant Type):

- Key Drivers: Growing emphasis on anti-aging and protection against environmental aggressors like blue light.

- Product Innovation: Development of lightweight, non-comedogenic, and aesthetically pleasing formulations.

- Market Penetration: High adoption rates due to daily use and integration into makeup routines.

- General People (Dominant Application):

- Key Drivers: Universal need for sun protection across all age groups and lifestyles.

- Product Accessibility: Wide range of product formats (lotions, creams, sprays) catering to diverse preferences.

- Market Saturation: High demand fuels continuous product development and brand competition.

Physical Sunscreen Product Innovations

Physical sunscreen product innovations are revolutionizing UV protection with enhanced efficacy and consumer appeal. Advancements in nanotechnology have enabled the creation of micronized and nano-sized zinc oxide and titanium dioxide particles, significantly reducing the chalky white cast traditionally associated with mineral sunscreens. This has led to the development of transparent and sheer formulations that offer superior broad-spectrum protection against UVA and UVB rays with SPF ratings often exceeding 50. Unique selling propositions include formulations that are water-resistant, sweat-proof, and infused with antioxidants and skin-nourishing ingredients, providing multi-functional benefits beyond sun protection. Applications are expanding to include tinted sunscreens that offer light coverage, color correction, and makeup primer functionalities, further integrating physical sunscreens into daily beauty routines. Performance metrics show improved photostability and efficacy in protecting against photodamage, with some products demonstrating significant improvements in skin texture and hydration.

Propelling Factors for Physical Sunscreen Growth

The physical sunscreen market is experiencing robust growth driven by several key factors. Heightened consumer awareness regarding the detrimental effects of UV radiation, including skin cancer and premature aging, is a primary catalyst. Growing demand for "clean beauty" products, emphasizing natural ingredients and perceived safety, favors mineral-based physical sunscreens over their chemical counterparts. Technological advancements have led to improved formulations with better aesthetics, eliminating the dreaded white cast and enhancing user experience. Furthermore, increasing disposable incomes in emerging economies and a growing emphasis on preventative healthcare contribute to market expansion. Government initiatives promoting sun safety awareness also play a significant role in driving adoption.

Obstacles in the Physical Sunscreen Market

Despite its growth, the physical sunscreen market faces certain obstacles. The higher cost of raw materials for mineral filters compared to chemical alternatives can lead to more expensive end products, potentially limiting affordability for some consumer segments. Consumer perception regarding the texture and feel of some physical sunscreens, particularly the potential for a white residue, remains a challenge, though innovation is rapidly addressing this. Supply chain disruptions for key mineral ingredients can impact production and availability. Regulatory hurdles in certain regions regarding nanoparticle usage and labeling also present complexities for manufacturers.

Future Opportunities in Physical Sunscreen

Emerging opportunities in the physical sunscreen market are vast and promising. The growing demand for reef-safe and environmentally friendly sunscreens presents a significant avenue for innovation and market differentiation. Expansion into underdeveloped geographical markets with increasing awareness of sun protection is a key growth area. The development of specialized physical sunscreens for specific activities like extreme sports or prolonged outdoor work, offering enhanced durability and protection, holds considerable potential. Furthermore, the integration of smart packaging and personalized skincare solutions, leveraging AI for tailored SPF recommendations, could unlock new consumer engagement models and market segments.

Major Players in the Physical Sunscreen Ecosystem

- Johnson & Johnson

- L'Oreal

- Proctor & Gamble

- Revlon

- Unilever

- Shiseido

- Estee Lauder

- Avon Products

- Clarins Group

- Lotus Herbals

- Edgewell Personal Care

Key Developments in Physical Sunscreen Industry

- 2023: Launch of advanced micronized zinc oxide formulations offering completely transparent application across multiple brands, addressing the "white cast" issue.

- 2023: Increased regulatory scrutiny on "reef-safe" claims leading to greater investment in environmentally friendly ingredient sourcing and sustainable packaging.

- 2022: Significant R&D investment by major companies in developing physical sunscreens with integrated anti-pollution and blue light protection capabilities.

- 2022: Expansion of physical sunscreen product lines targeting sensitive skin and children, with a focus on hypoallergenic and fragrance-free formulas.

- 2021: Strategic acquisitions of smaller, innovative physical sunscreen brands by larger corporations to bolster their clean beauty portfolios.

- 2021: Growing consumer trend towards multi-functional products, leading to the introduction of tinted physical sunscreens with cosmetic benefits.

- 2020: Enhanced focus on supply chain resilience for mineral UV filters (zinc oxide, titanium dioxide) due to global disruptions.

- 2019: Introduction of innovative spray and stick formats for physical sunscreens, improving ease of application for outdoor activities.

Strategic Physical Sunscreen Market Forecast

The strategic physical sunscreen market forecast indicates sustained growth driven by increasing consumer demand for safe, effective, and environmentally conscious sun protection. Key growth catalysts include ongoing technological innovations that enhance product aesthetics and performance, alongside the expanding awareness of UV-related skin health risks. The "clean beauty" movement continues to propel the adoption of mineral-based formulas. Future opportunities lie in underserved markets, specialized product categories, and the integration of advanced technologies. With a strong foundation in preventative skincare and a clear consumer preference for mineral filters, the physical sunscreen market is poised for significant expansion throughout the forecast period.

Physical Sunscreen Segmentation

-

1. Application

- 1.1. General People

- 1.2. Children and Pregnant Women

-

2. Types

- 2.1. Facial Sunscreen

- 2.2. Body Suncream

Physical Sunscreen Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Physical Sunscreen Regional Market Share

Geographic Coverage of Physical Sunscreen

Physical Sunscreen REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. General People

- 5.1.2. Children and Pregnant Women

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Facial Sunscreen

- 5.2.2. Body Suncream

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Physical Sunscreen Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. General People

- 6.1.2. Children and Pregnant Women

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Facial Sunscreen

- 6.2.2. Body Suncream

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Physical Sunscreen Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. General People

- 7.1.2. Children and Pregnant Women

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Facial Sunscreen

- 7.2.2. Body Suncream

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Physical Sunscreen Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. General People

- 8.1.2. Children and Pregnant Women

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Facial Sunscreen

- 8.2.2. Body Suncream

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Physical Sunscreen Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. General People

- 9.1.2. Children and Pregnant Women

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Facial Sunscreen

- 9.2.2. Body Suncream

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Physical Sunscreen Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. General People

- 10.1.2. Children and Pregnant Women

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Facial Sunscreen

- 10.2.2. Body Suncream

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Physical Sunscreen Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. General People

- 11.1.2. Children and Pregnant Women

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Facial Sunscreen

- 11.2.2. Body Suncream

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Johnson & Johnson

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 L'Oreal

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Proctor & Gamble

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Revlon

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Unilever

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Shiseido

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Estee Lauder

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Avon Products

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Clarins Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Lotus Herbals

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Edgewell Personal Care

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Johnson & Johnson

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Physical Sunscreen Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Physical Sunscreen Revenue (million), by Application 2025 & 2033

- Figure 3: North America Physical Sunscreen Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Physical Sunscreen Revenue (million), by Types 2025 & 2033

- Figure 5: North America Physical Sunscreen Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Physical Sunscreen Revenue (million), by Country 2025 & 2033

- Figure 7: North America Physical Sunscreen Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Physical Sunscreen Revenue (million), by Application 2025 & 2033

- Figure 9: South America Physical Sunscreen Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Physical Sunscreen Revenue (million), by Types 2025 & 2033

- Figure 11: South America Physical Sunscreen Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Physical Sunscreen Revenue (million), by Country 2025 & 2033

- Figure 13: South America Physical Sunscreen Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Physical Sunscreen Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Physical Sunscreen Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Physical Sunscreen Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Physical Sunscreen Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Physical Sunscreen Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Physical Sunscreen Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Physical Sunscreen Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Physical Sunscreen Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Physical Sunscreen Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Physical Sunscreen Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Physical Sunscreen Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Physical Sunscreen Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Physical Sunscreen Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Physical Sunscreen Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Physical Sunscreen Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Physical Sunscreen Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Physical Sunscreen Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Physical Sunscreen Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Physical Sunscreen Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Physical Sunscreen Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Physical Sunscreen Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Physical Sunscreen Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Physical Sunscreen Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Physical Sunscreen Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Physical Sunscreen Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Physical Sunscreen Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Physical Sunscreen Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Physical Sunscreen?

The projected CAGR is approximately 3.3%.

2. Which companies are prominent players in the Physical Sunscreen?

Key companies in the market include Johnson & Johnson, L'Oreal, Proctor & Gamble, Revlon, Unilever, Shiseido, Estee Lauder, Avon Products, Clarins Group, Lotus Herbals, Edgewell Personal Care.

3. What are the main segments of the Physical Sunscreen?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 794 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Physical Sunscreen," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Physical Sunscreen report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Physical Sunscreen?

To stay informed about further developments, trends, and reports in the Physical Sunscreen, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence