Key Insights

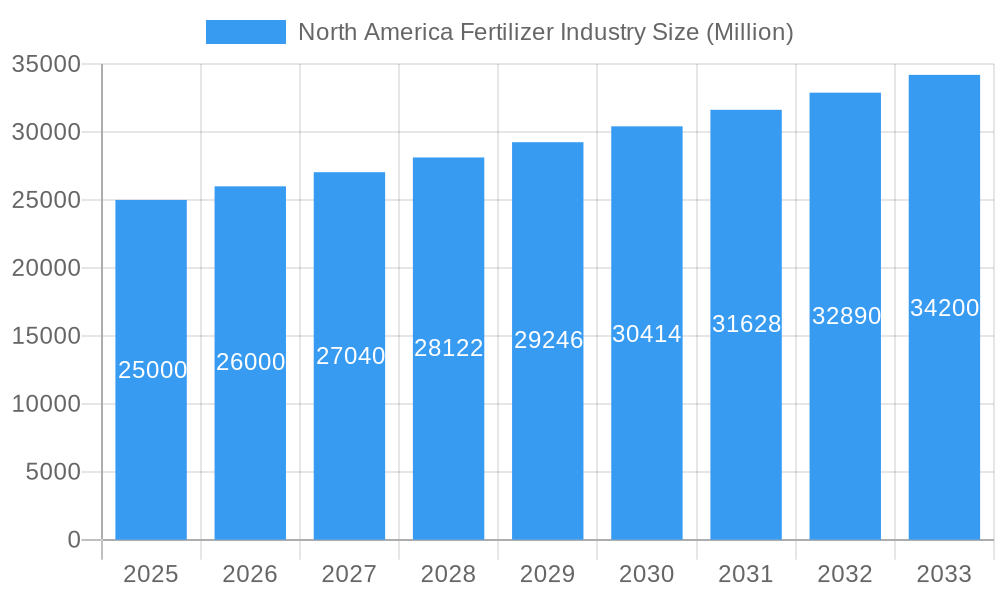

The North America fertilizer industry is poised for significant expansion, projected to reach a market valuation of $63.76 billion in 2025, demonstrating a robust Compound Annual Growth Rate (CAGR) of 5.13% from 2025 to 2033. This impressive growth is fundamentally driven by the escalating global demand for food, necessitating higher agricultural productivity and improved crop yields across the region. Farmers in the United States, Canada, and Mexico are increasingly adopting advanced agricultural practices, including precision farming techniques and efficient nutrient management strategies, to maximize output and enhance soil health. The rising adoption of high-efficiency fertilizers, coupled with government initiatives promoting sustainable agriculture and food security, further propels market expansion. Furthermore, the growing awareness regarding the benefits of balanced crop nutrition, encompassing nitrogen, phosphate, potash, and micronutrient applications, is encouraging investment in innovative fertilizer solutions. The shift towards specialty and organic fertilizers also contributes to market dynamism, catering to evolving consumer preferences for sustainably produced food and environmentally friendly farming methods.

North America Fertilizer Industry Market Size (In Billion)

Key trends shaping the North American fertilizer market include the increasing integration of digital technologies for optimized fertilizer application, such as sensor-based nutrient monitoring and drone technology, enhancing precision and reducing waste. There is also a notable surge in demand for liquid and controlled-release formulations, which offer superior nutrient uptake and minimize environmental impact. However, the industry faces challenges primarily related to the volatility of raw material prices, particularly for natural gas, phosphates, and potash, which can impact production costs and market stability. Stringent environmental regulations aimed at reducing nutrient runoff and greenhouse gas emissions also present a complex landscape for manufacturers, pushing for continuous innovation in product development and sustainable practices. Major industry players like Nutrien Ltd., CF Industries Holdings, Inc., The Mosaic Company, and Yara International ASA are at the forefront of this evolution, investing heavily in research and development to introduce advanced fertilizer products and expand their market footprint. The competitive environment is characterized by strategic collaborations, mergers, and acquisitions, all aimed at strengthening product portfolios and meeting the diverse needs of the agricultural sector across North America.

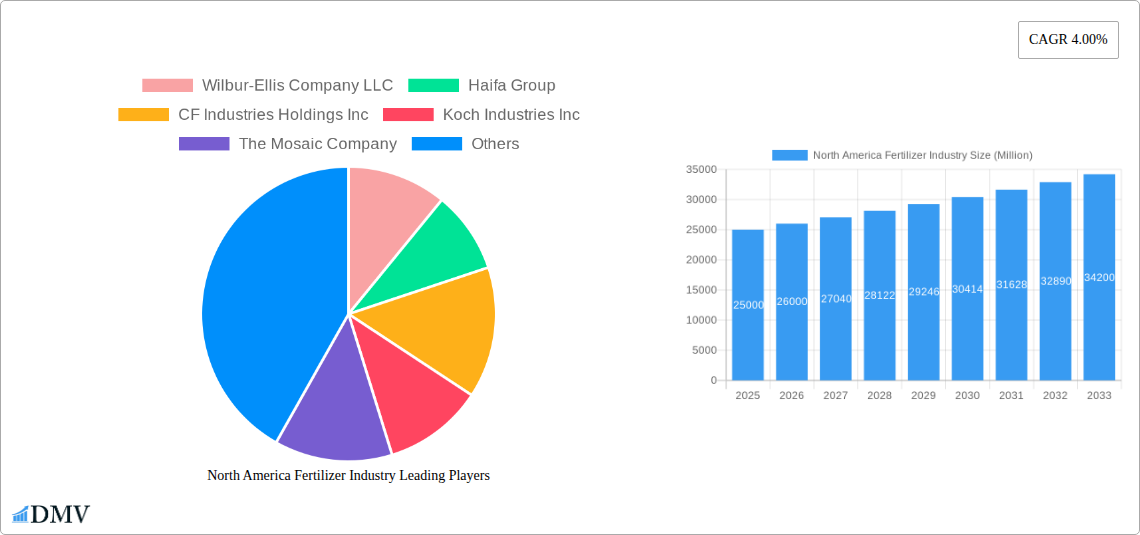

North America Fertilizer Industry Company Market Share

This comprehensive report provides an unparalleled examination of the North America Fertilizer Industry, offering critical insights into market dynamics, growth trajectories, and strategic opportunities from 2019 to 2033. Leveraging a robust methodology, with 2025 as the base and estimated year, and a forecast period extending to 2033, this analysis delves into the pivotal trends shaping agricultural productivity and sustainability across the region. Stakeholders seeking to navigate the evolving landscape of nitrogen fertilizers, phosphate fertilizers, potash fertilizers, micronutrient fertilizers, and organic fertilizers will find invaluable data on market size, segmentation, competitive strategies, and future projections. Unlock strategic intelligence to capitalize on the increasing demand for enhanced crop yields, sustainable farming practices, and innovative nutrient management solutions in this dynamic North American market.

North America Fertilizer Industry Market Composition & Trends

The North America Fertilizer Industry exhibits a moderately concentrated market structure, characterized by a few dominant players alongside a vibrant ecosystem of specialized providers. Top-tier companies like Nutrien Ltd., CF Industries Holdings, Inc., and The Mosaic Company collectively command an estimated xx billion in market value, holding approximately 60% of the total market share, particularly in commodity fertilizers like nitrogen and potash. This oligopolistic structure fosters intense competition in innovation and market reach. Innovation catalysts are increasingly driven by the imperative for sustainable agriculture, with significant R&D investments in enhanced efficiency fertilizers (EEFs), bio-fertilizers, and precision nutrient delivery systems. Companies are developing solutions that minimize environmental impact, such as reduced nutrient runoff, while maximizing crop uptake and yield.

Regulatory landscapes play a crucial role, with environmental policies concerning nutrient management and emissions heavily influencing product development and application practices. Governments in the U.S. and Canada are promoting sustainable farming through incentives and regulations, leading to a surge in demand for environmentally friendly formulations. Substitute products, while not direct replacements for primary nutrient sources, include soil amendments and cover crops that enhance soil health and nutrient cycling, indirectly influencing fertilizer consumption patterns. End-user profiles range from large-scale row crop operations in the Midwest and Canadian Prairies, which require bulk commodity fertilizers, to smaller specialized horticulture and gardening segments demanding custom blends and organic options. The market also sees varied adoption of advanced technologies, with larger farms more readily integrating precision agriculture tools for optimized fertilizer application.

M&A activities remain a key feature of the industry, as companies seek to consolidate market share, expand product portfolios, and enhance their distribution networks. For instance, The Andersons' acquisition of Mote Farm Service, Inc. in October 2022, though a regional move, underscores the ongoing strategy to strengthen retail farm center networks and direct sales capabilities. Similarly, strategic partnerships, such as ICL's agreement with General Mills in January 2023 for specialty phosphate solutions, highlight a trend towards vertical integration and customized supply agreements. While specific M&A deal values in the last five years have collectively reached an estimated xx billion, reflecting a robust drive for strategic expansion and operational efficiencies, this dynamic environment ensures continuous shifts in market composition and competitive advantage. The focus on sustainability and technological integration is expected to further drive strategic alliances and investments across the value chain.

North America Fertilizer Industry Industry Evolution

The North America Fertilizer Industry is undergoing a significant transformation, marked by dynamic market growth trajectories, groundbreaking technological advancements, and rapidly shifting consumer demands. Historically, from 2019 to 2024, the market experienced a steady growth, fueled by consistent agricultural demand and stable commodity prices, achieving an estimated historical CAGR of xx%. However, the forecast period from 2025 to 2033 projects an accelerated expansion, with an estimated CAGR of yy%, primarily driven by the confluence of global food security imperatives, the adoption of precision agriculture, and increasing regulatory pressures for sustainable farming practices. The market's evolution is inherently tied to the broader agricultural sector's need to produce more with fewer resources, leading to an intensified focus on efficiency and environmental stewardship.

Technological advancements are at the heart of this evolution. The industry has seen a substantial shift from traditional bulk fertilizers to more sophisticated formulations such as slow-release and enhanced efficiency fertilizers (EEFs). These innovations are designed to optimize nutrient uptake, reduce leaching and volatilization, and minimize environmental impact. For example, the adoption rate of EEFs in major crop-producing regions has increased by an estimated xx% in the last five years, reflecting growers' willingness to invest in solutions that offer both economic and environmental benefits. Digital agriculture platforms, including satellite imagery, AI-powered analytics, and drone technology, are revolutionizing how fertilizers are prescribed and applied. These tools enable hyper-localized application, saving costs and improving nutrient management, with an estimated zz% of large-scale farms in North America now integrating some form of precision farming technology into their operations. The development of bio-fertilizers, derived from microorganisms, also represents a burgeoning segment, offering organic and sustainable alternatives that enhance soil health and nutrient availability.

Shifting consumer demands are profoundly influencing the industry's product development and marketing strategies. There is a growing consumer preference for organically grown produce, pushing demand for organic fertilizers and sustainable agricultural practices. This trend is not limited to specialty markets but is increasingly impacting mainstream agriculture. Furthermore, farmers are seeking customized nutrient solutions tailored to specific crop needs and soil conditions, moving away from a one-size-fits-all approach. This demand for personalization is facilitated by advancements in soil testing and data analytics, allowing for precise fertilizer recommendations. The emphasis on transparency and traceability in the food supply chain also extends to fertilizer inputs, with stakeholders increasingly scrutinizing the environmental footprint of agricultural production. This holistic shift towards sustainability, efficiency, and customized solutions is not merely a trend but a fundamental reorientation of the North America Fertilizer Industry, promising continued innovation and strategic growth throughout the forecast period.

Leading Regions, Countries, or Segments in North America Fertilizer Industry

The North America Fertilizer Industry exhibits distinct leadership across its diverse segments, driven by unique agricultural landscapes, technological adoption rates, and regulatory environments.

Dominant Type Segment: Nitrogen Fertilizers

- Key Drivers:

- Extensive Crop Cultivation: North America's vast corn, wheat, and canola fields, which are highly nitrogen-intensive, drive immense demand.

- Agricultural Practices: Common agricultural practices, including rotation systems and high-yield farming, necessitate significant nitrogen inputs.

- Investment Trends: Substantial investments in nitrogen production capacity, such as Koch's USD 30 million expansion in Kansas to increase UAN production, underscore its strategic importance.

- Market Size: The nitrogen fertilizer segment is projected to hold the largest market share, valued at over xx billion by 2033, due to its indispensable role in enhancing crop protein content and overall plant growth.

- Key Drivers:

Dominant Formulation Segment: Granular Fertilizers

- Key Drivers:

- Ease of Application: Granular fertilizers are widely favored for their ease of handling, storage, and mechanized application across large agricultural lands.

- Controlled Release Potential: Advancements in coating technologies enable the development of slow-release and enhanced efficiency granular fertilizers, aligning with sustainability goals.

- Cost-Effectiveness: Generally more cost-effective for large-scale application compared to liquid formulations, particularly for broadacre crops.

- Established Infrastructure: The extensive infrastructure for bulk storage and distribution of granular products across North America further solidifies its dominance.

- Key Drivers:

Dominant Application Segment: Agriculture

- Key Drivers:

- Food Security Imperative: The fundamental need to feed a growing global population drives intensive agricultural production.

- Economic Contribution: Agriculture remains a cornerstone of the North American economy, with massive land areas dedicated to crop cultivation.

- Technological Integration: Rapid adoption of precision agriculture technologies primarily by large agricultural enterprises optimizes fertilizer use in farming.

- Scale of Operations: The sheer scale of commercial farming operations in countries like the U.S. and Canada dwarfs demand from horticulture or gardening.

- Key Drivers:

Dominant Sales Channel Segment: Distributors and Wholesalers

- Key Drivers:

- Extensive Reach: These channels provide critical logistical support and market penetration to a vast network of farms, especially in rural areas.

- Value-Added Services: Distributors often offer agronomic advice, blending services, and financing options, making them indispensable partners for growers.

- Established Relationships: Long-standing relationships and trust between farmers and local distributors facilitate consistent sales.

- Inventory Management: They manage significant inventory, ensuring timely supply during peak planting seasons.

- Key Drivers:

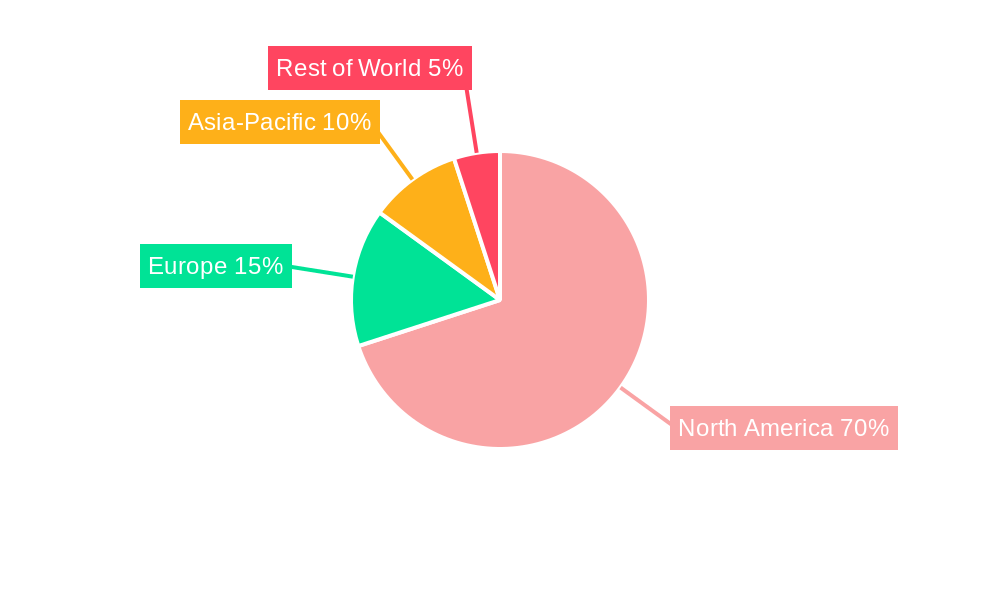

Geographically, the United States stands as the dominant country within North America, accounting for an estimated 75% of the regional market, driven by its expansive agricultural land, diverse crop portfolio, and high adoption of advanced farming technologies. Canada follows, contributing significantly, particularly in potash production and grain cultivation. These countries benefit from robust research and development activities, supportive government policies, and strong economic infrastructures that facilitate investment in fertilizer production and distribution. The leadership of Nitrogen Fertilizers stems from their essential role in staple crop production, while Granular formulations provide efficiency for large-scale operations. The Agriculture application segment is the undisputed driver due to the foundational importance of food production, and Distributors and Wholesalers are the critical conduits connecting manufacturers to a widespread farmer base, ensuring market efficiency and reach. These factors collectively highlight a mature yet dynamic market where strategic positioning within these dominant segments is key to sustained success.

North America Fertilizer Industry Product Innovations

The North America Fertilizer Industry is experiencing a wave of product innovations focused on enhancing efficiency, reducing environmental impact, and tailoring nutrient delivery. New product lines include advanced slow-release and enhanced efficiency fertilizers (EEFs) that minimize nutrient loss through volatilization and leaching, ensuring optimal nutrient availability throughout the crop growth cycle. Unique selling propositions revolve around higher nutrient use efficiency, leading to improved yields with less product, reduced labor, and a smaller carbon footprint. Technological advancements incorporate nanotechnology for precision nutrient delivery, bio-fertilizers leveraging beneficial microbes for improved soil health and nutrient cycling, and customized blends of micronutrients designed for specific crop types and soil deficiencies. These innovations, driven by the demand for sustainable agriculture and precision farming, are setting new performance metrics for nutrient uptake and environmental stewardship.

Propelling Factors for North America Fertilizer Industry Growth

Several powerful forces are propelling the North America Fertilizer Industry forward. Technologically, the rapid adoption of precision agriculture and smart farming solutions, including GPS-guided application and variable-rate technology, optimizes fertilizer use, enhancing efficiency and driving demand for advanced formulations. The continuous development of enhanced efficiency fertilizers (EEFs) and bio-fertilizers offers superior nutrient management, aligning with sustainability goals and increasing market potential. Economically, a burgeoning global population necessitates higher food production, directly escalating demand for fertilizers to boost crop yields. Rising crop prices and farm incomes, coupled with government subsidies and policies promoting agricultural productivity, further incentivize fertilizer consumption. Regulatory influences, particularly policies advocating for reduced environmental impact and sustainable farming practices, are stimulating investment in innovative, eco-friendly fertilizer products, ensuring long-term market expansion.

Obstacles in the North America Fertilizer Industry Market

The North America Fertilizer Industry faces significant obstacles that can impact its growth trajectory. Regulatory challenges, particularly stringent environmental regulations concerning nitrogen and phosphorus runoff, lead to increased compliance costs, estimated at xx billion annually, and restrict certain application methods, demanding continuous R&D into less impactful formulations. Supply chain disruptions, often triggered by geopolitical events or extreme weather, create price volatility for critical raw materials like natural gas (for nitrogen) and potash, impacting profit margins by an estimated xx% in volatile periods. This volatility forces companies to absorb higher input costs or pass them on to farmers. Furthermore, intense competitive pressures, including price wars and market consolidation among major players, can squeeze smaller participants. Growing public and consumer demand for organic farming and a heightened focus on environmental concerns also pose challenges, pushing the industry to innovate rapidly towards more sustainable and often costlier solutions.

Future Opportunities in North America Fertilizer Industry

The North America Fertilizer Industry is poised for significant future opportunities driven by evolving agricultural practices and technological innovation. Emerging markets within specialty crops, controlled environment agriculture (CEA), and urban farming present new avenues for highly specialized and customized nutrient solutions. Technological advancements in next-generation bio-fertilizers, offering improved soil health and reduced chemical dependency, are set to capture a larger market share. The development of carbon-neutral fertilizer production methods and integration with digital platforms for AI-driven nutrient management systems represent substantial growth areas. Furthermore, the increasing consumer trend towards sustainable and organic produce will continue to fuel demand for environmentally friendly and certified organic fertilizer products, opening up lucrative niche markets and fostering innovation across the value chain.

Major Players in the North America Fertilizer Industry Ecosystem

- Nutrien Ltd.

- CF Industries Holdings, Inc.

- The Mosaic Company

- Yara International ASA

- The Andersons, Inc.

- ICL Group Ltd.

- Koch Industries, Inc.

- Haifa Group

- Sociedad Química y Minera de Chile (SQM)

- Wilbur-Ellis Company LLC

- Compass Minerals

- OCP Group

- Others

Key Developments in North America Fertilizer Industry Industry

- January 2023: ICL has entered into a strategic partnership agreement with General Mills. This long-term agreement positions ICL as the supplier of strategic specialty phosphate solutions to General Mills, with a focus on international expansion. This development signifies a trend towards integrated supply chains and customized nutrient solutions, strengthening ICL's market position in specialty phosphates and potentially influencing product innovation for food manufacturers.

- October 2022: The Andersons, Inc. entered into an agreement to acquire the assets of Mote Farm Service, Inc. This acquisition aims to expand The Andersons' retail farm center network, enhancing their direct sales capabilities and market reach within key agricultural regions. Such strategic acquisitions contribute to market consolidation and improved distribution efficiency, allowing major players to serve a broader customer base directly.

- August 2022: Koch Industries, Inc. invested around USD 30 million in its Kansas nitrogen plant. This significant investment is projected to increase UAN (urea ammonium nitrate) production by 35,000 tons per year. The expansion directly addresses the growing UAN demand across western Kansas and eastern Colorado, showcasing the industry's commitment to boosting domestic production capacity and meeting regional agricultural needs for vital nitrogen fertilizers.

Strategic North America Fertilizer Industry Market Forecast

The strategic forecast for the North America Fertilizer Industry from 2025 to 2033 indicates robust growth, primarily fueled by the imperative for enhanced food security and the widespread adoption of sustainable agricultural practices. Key growth catalysts include continuous innovation in enhanced efficiency and bio-fertilizers, the expansion of precision agriculture technologies, and favorable government policies promoting eco-friendly farming. Future opportunities lie in customizing nutrient solutions for specialized crops, developing carbon-neutral production processes, and leveraging digital platforms for optimized nutrient management. The market potential is vast, driven by consistent demand from the agricultural sector, technological advancements, and a strong emphasis on environmental stewardship, positioning North America as a leading region for fertilizer innovation and sustainable agricultural solutions in the coming decade.

North America Fertilizer Industry Segmentation

-

1. Type

- 1.1. Nitrogen Fertilizers

- 1.2. Phosphate Fertilizers

- 1.3. Potash Fertilizers

- 1.4. Micronutrient Fertilizers

- 1.5. Organic Fertilizers

-

2. Formulation

- 2.1. Liquid

- 2.2. Granular

- 2.3. Powder

- 2.4. Pellets

-

3. Application

- 3.1. Agriculture

- 3.2. Horticulture

- 3.3. Gardening

- 3.4. Others

-

4. Sales Channel

- 4.1. Direct Sales

- 4.2. Distributors and Wholesalers

- 4.3. Online

- 4.4. Others

North America Fertilizer Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Fertilizer Industry Regional Market Share

Geographic Coverage of North America Fertilizer Industry

North America Fertilizer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Nitrogen Fertilizers

- 5.1.2. Phosphate Fertilizers

- 5.1.3. Potash Fertilizers

- 5.1.4. Micronutrient Fertilizers

- 5.1.5. Organic Fertilizers

- 5.2. Market Analysis, Insights and Forecast - by Formulation

- 5.2.1. Liquid

- 5.2.2. Granular

- 5.2.3. Powder

- 5.2.4. Pellets

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Agriculture

- 5.3.2. Horticulture

- 5.3.3. Gardening

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors and Wholesalers

- 5.4.3. Online

- 5.4.4. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Fertilizer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Nitrogen Fertilizers

- 6.1.2. Phosphate Fertilizers

- 6.1.3. Potash Fertilizers

- 6.1.4. Micronutrient Fertilizers

- 6.1.5. Organic Fertilizers

- 6.2. Market Analysis, Insights and Forecast - by Formulation

- 6.2.1. Liquid

- 6.2.2. Granular

- 6.2.3. Powder

- 6.2.4. Pellets

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Agriculture

- 6.3.2. Horticulture

- 6.3.3. Gardening

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors and Wholesalers

- 6.4.3. Online

- 6.4.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Nutrien Ltd.

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CF Industries Holdings Inc.

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 The Mosaic Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yara International ASA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 The Andersons Inc.

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ICL Group Ltd.

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Koch Industries Inc.

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Haifa Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sociedad Química y Minera de Chile (SQM)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Wilbur-Ellis Company LLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Compass Minerals

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 OCP Group

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Others

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Nutrien Ltd.

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Fertilizer Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Fertilizer Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Fertilizer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Fertilizer Industry Revenue billion Forecast, by Formulation 2020 & 2033

- Table 3: North America Fertilizer Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: North America Fertilizer Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 5: North America Fertilizer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Fertilizer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 7: North America Fertilizer Industry Revenue billion Forecast, by Formulation 2020 & 2033

- Table 8: North America Fertilizer Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: North America Fertilizer Industry Revenue billion Forecast, by Sales Channel 2020 & 2033

- Table 10: North America Fertilizer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico North America Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Fertilizer Industry?

The projected CAGR is approximately 5.13%.

2. Which companies are prominent players in the North America Fertilizer Industry?

Key companies in the market include Nutrien Ltd., CF Industries Holdings, Inc., The Mosaic Company, Yara International ASA, The Andersons, Inc., ICL Group Ltd., Koch Industries, Inc., Haifa Group, Sociedad Química y Minera de Chile (SQM), Wilbur-Ellis Company LLC, Compass Minerals, OCP Group, Others.

3. What are the main segments of the North America Fertilizer Industry?

The market segments include Type, Formulation, Application, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 63.76 billion as of 2022.

5. What are some drivers contributing to market growth?

Awareness of Landscaping Maintenance; Technological Advancements.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shortage of Skilled Labor; Wastage of High Amount of Water For Irrigating Lawns.

8. Can you provide examples of recent developments in the market?

January 2023: ICL has entered into a strategic partnership agreement with General Mills, in which it will be the supplier of strategic specialty phosphate solutions to General Mills. The long-term agreement will also focus on international expansion.October 2022: The Andersons entered into an agreement to acquire the assets of Mote Farm Service, Inc. to expand thier retail farm center network.August 2022: Koch invested around USD 30 million in the Kansas nitrogen plant to increase UAN production by 35,000 tons per year to meet growing UAN demand across western Kansas and eastern Colorado.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Fertilizer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Fertilizer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Fertilizer Industry?

To stay informed about further developments, trends, and reports in the North America Fertilizer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence