Key Insights

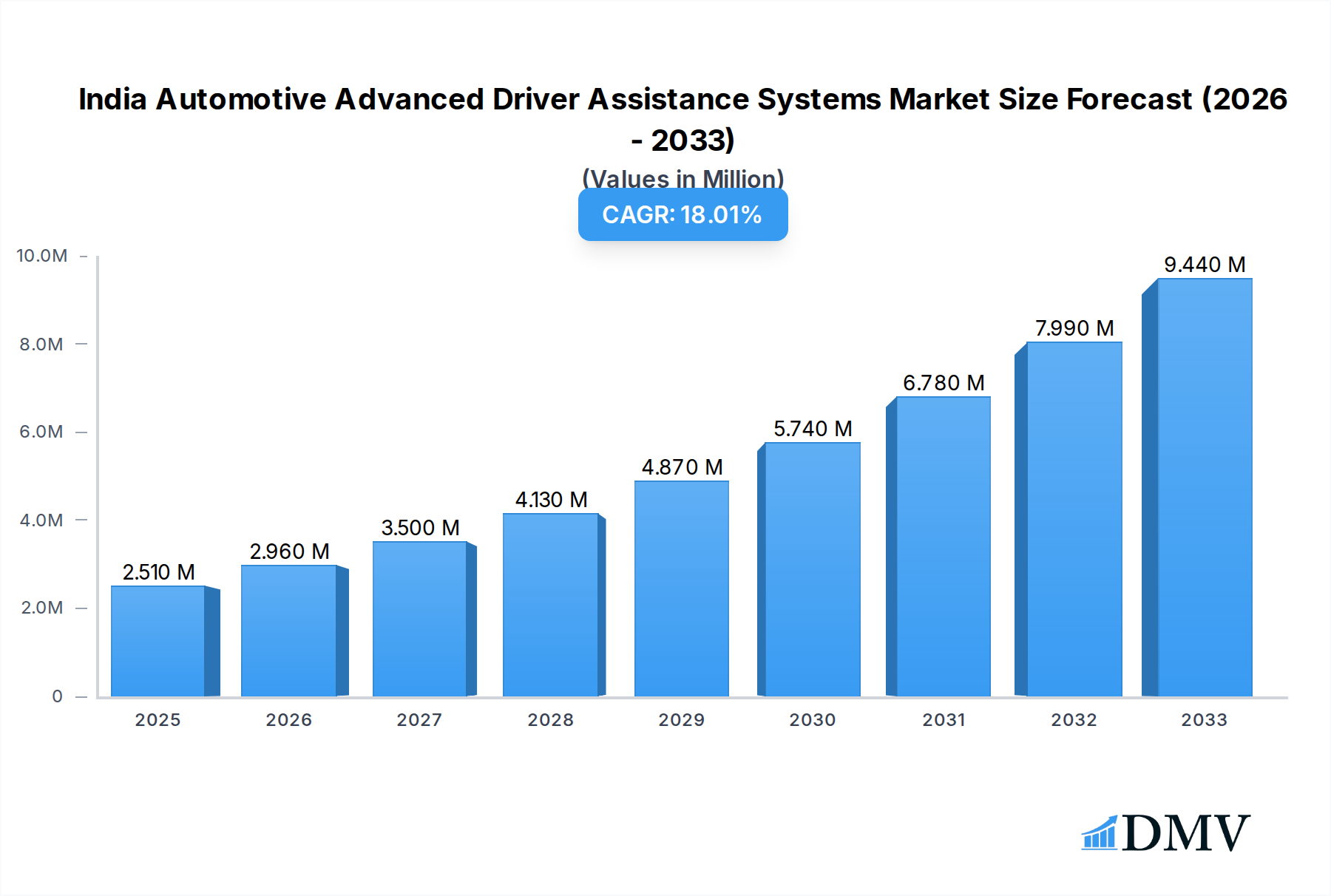

The Indian automotive market is poised for significant growth in Advanced Driver Assistance Systems (ADAS), driven by an increasing focus on road safety and the adoption of sophisticated vehicle technologies. The market, valued at 2.51 Million in 2025, is projected to expand at a robust Compound Annual Growth Rate (CAGR) of 18.33% during the forecast period of 2025-2033. This rapid expansion is fueled by a confluence of factors, including government initiatives promoting safer vehicles, rising consumer awareness regarding ADAS benefits, and the growing demand for premium features in passenger cars. Key ADAS features like Parking Assist Systems (including Night Vision Systems, Blind Spot Detection, Advanced Automatic Emergency Braking Systems, Collision Warning, Driver Drowsiness Alerts, Traffic Sign Recognition, Lane Departure Warning, and Adaptive Cruise Control) are becoming integral to new vehicle manufacturing. The integration of advanced technologies such as Radar, LiDAR, and Cameras is further accelerating this trend, enabling vehicles to perceive and react to their environment more effectively.

India Automotive Advanced Driver Assistance Systems Market Market Size (In Million)

The growth trajectory is further bolstered by the increasing production of passenger cars, which constitute a major segment within the Indian automotive landscape. While the overall market demonstrates a strong upward momentum, certain challenges, such as the relatively high cost of initial ADAS implementation and a need for greater consumer education, need to be addressed to ensure widespread adoption. However, with continued technological advancements, economies of scale in production, and supportive regulatory frameworks, the Indian ADAS market is expected to witness a transformative period, establishing it as a crucial hub for automotive innovation and safety. The market is primarily driven by the desire for enhanced safety and comfort, with automakers actively incorporating these systems to meet evolving customer expectations and stricter safety regulations.

India Automotive Advanced Driver Assistance Systems Market Company Market Share

This in-depth report provides a meticulous analysis of the India Automotive Advanced Driver Assistance Systems (ADAS) Market, a rapidly evolving sector crucial for enhancing vehicle safety and driving experience. Covering a comprehensive study period from 2019 to 2033, with a base and estimated year of 2025, and a detailed forecast period of 2025–2033, this report offers critical insights for stakeholders seeking to understand current trends and future trajectories. We delve into the intricate market composition, industry evolution, leading segments, product innovations, growth drivers, obstacles, opportunities, and the major players shaping the Indian ADAS market. Leveraging high-ranking keywords such as "ADAS India," "Automotive Safety," "Connected Cars," "Autonomous Driving Technology," "Vehicle Electronics," and "Smart Mobility India," this report is optimized for maximum search visibility and stakeholder engagement.

India Automotive Advanced Driver Assistance Systems Market Market Composition & Trends

The India Automotive ADAS Market is characterized by a dynamic and increasingly competitive landscape, driven by a confluence of factors including stringent safety regulations, rising consumer awareness, and increasing per capita income. Market concentration is moderate, with a few dominant players holding significant shares while a growing number of innovative startups contribute to a vibrant ecosystem. Innovation catalysts include the relentless pursuit of advanced safety features, the integration of AI and machine learning for predictive capabilities, and the development of cost-effective solutions for the Indian automotive industry. The regulatory landscape, though still maturing, is steadily moving towards mandating advanced safety technologies, thereby fueling adoption. Substitute products, such as aftermarket safety devices, exist but are increasingly being overshadowed by integrated OEM solutions. End-user profiles are diversifying, ranging from safety-conscious individuals and families to fleet operators prioritizing operational efficiency and risk mitigation. Mergers & Acquisition (M&A) activities, while not yet at peak levels, are anticipated to increase as larger players seek to consolidate their market position and acquire specialized technological expertise.

- Market Share Distribution: Dominated by key ADAS technology providers and automotive OEMs.

- Innovation Catalysts: AI/ML integration, sensor fusion, V2X communication development.

- Regulatory Landscape: Government mandates for passive and active safety features.

- Substitute Products: Aftermarket safety systems, manual driver vigilance.

- End-User Profiles: Individual car owners, commercial fleet operators, ride-sharing services.

- M&A Activities: Strategic acquisitions for technology integration and market expansion.

India Automotive Advanced Driver Assistance Systems Market Industry Evolution

The India Automotive ADAS Market has witnessed a remarkable transformation, evolving from niche applications in luxury vehicles to becoming an integral part of mass-market offerings. Historically, the initial phases of ADAS adoption in India were driven by premium segments and a growing awareness of global safety standards. However, the historical period (2019-2024) saw a significant acceleration in the integration of basic ADAS features like Parking Assist Systems, Collision Warning, and Lane Departure Warning due to increasing consumer demand for enhanced safety and convenience. This period was marked by strategic collaborations between technology providers and Indian automotive manufacturers, aiming to localize and adapt these technologies for the unique Indian driving conditions.

The base year (2025) represents a pivotal point where ADAS has transitioned from a luxury add-on to a mainstream feature. The forecast period (2025–2033) is projected to witness exponential growth, propelled by several key trends. Firstly, technological advancements, particularly in sensor technology (Radar, LiDAR, Camera), have led to more accurate and reliable ADAS functionalities. The miniaturization and cost reduction of these components have made them accessible for a wider range of vehicles. Secondly, a growing emphasis on accident reduction and road safety by the Indian government, coupled with evolving consumer preferences for sophisticated and safe vehicles, is acting as a strong market pull. The increasing adoption of Connected Car solutions, often integrated with ADAS, further enhances the value proposition. By 2025, we anticipate a substantial portion of new vehicle sales in India to be equipped with at least one ADAS feature. The growth rate of the Indian ADAS market is expected to surpass the overall automotive market growth, indicating a strong surge in adoption. This evolution is also influenced by the increasing complexity of vehicle architectures and the need for advanced control systems, paving the way for semi-autonomous and eventually autonomous driving capabilities in the long term.

Leading Regions, Countries, or Segments in India Automotive Advanced Driver Assistance Systems Market

The India Automotive ADAS Market exhibits strong regional disparities and segment dominance, primarily driven by economic factors, consumer preferences, and the presence of automotive manufacturing hubs.

Dominant Segment by Vehicle Type: Passenger Cars

Passenger cars currently represent the largest and fastest-growing segment within the Indian ADAS market. This dominance is attributed to several interwoven factors:

- Rising Disposable Incomes: An expanding middle class with increased purchasing power is more inclined to invest in vehicles equipped with advanced safety and convenience features.

- Consumer Awareness & Demand: Growing awareness of the benefits of ADAS, such as improved safety, reduced driver fatigue, and enhanced driving experience, is directly translating into higher demand for these features in passenger vehicles. This awareness is often fueled by media coverage, global trends, and the availability of such features in premium models.

- OEM Strategy: Automotive manufacturers are increasingly incorporating ADAS as standard or optional features across a wider spectrum of their passenger car models, from compact SUVs to sedans, to remain competitive and cater to evolving customer expectations. This strategic push by OEMs is a significant driver of adoption.

- Urbanization and Traffic Congestion: In densely populated urban areas, features like Parking Assist System, Blind Spot Detection, and Adaptive Cruise Control offer significant advantages in navigating congested traffic and parking scenarios, making them highly desirable for city dwellers.

Dominant Segment by Technology: Camera

While Radar and LiDAR are crucial components of sophisticated ADAS, Camera technology currently holds a dominant position in the Indian market due to a combination of factors:

- Cost-Effectiveness: Camera-based ADAS solutions are generally more affordable than those relying heavily on Radar or LiDAR, making them more viable for mass-market adoption in price-sensitive India.

- Versatility and Information Richness: Cameras can capture a wide range of visual information, enabling functionalities such as Traffic Sign Recognition, Lane Departure Warning, and Driver Drowsiness Alert, which are crucial for Indian road conditions. They are also instrumental in many Parking Assist Systems.

- Technological Maturity and Integration: Camera technology is well-established and can be seamlessly integrated into existing vehicle electronic architectures. The development of advanced image processing algorithms further enhances their capabilities.

- Synergy with Other Technologies: Cameras often work in conjunction with other sensors, such as radar, in sensor fusion architectures. However, in many entry-level and mid-range ADAS applications, cameras serve as the primary sensing modality.

Key Drivers for Dominance:

- Investment Trends: Significant R&D investments by global and Indian component manufacturers in camera-based ADAS solutions.

- Regulatory Support: While not directly mandated for cameras, safety regulations indirectly push for visual sensing capabilities.

- Technological Advancements: Continuous improvements in camera resolution, low-light performance, and AI-powered image processing.

India Automotive Advanced Driver Assistance Systems Market Product Innovations

The India Automotive ADAS Market is witnessing a surge in product innovations focused on enhancing safety, convenience, and driver awareness. Key advancements include the development of more sophisticated Parking Assist Systems utilizing high-resolution cameras and ultrasonic sensors for precise maneuvering in tight spaces. Innovations in Blind Spot Detection are improving real-time monitoring and alert systems. Furthermore, Advanced Automatic Emergency Braking Systems are becoming more intelligent, capable of detecting a wider range of obstacles and responding faster. The integration of AI in Driver Drowsiness Alert systems is enabling personalized and predictive warnings. Technologies like Traffic Sign Recognition are becoming more accurate in diverse lighting and weather conditions. The performance metrics are continuously improving, with enhanced detection ranges, reduced false alarm rates, and faster processing speeds, making ADAS solutions more reliable and user-friendly for the Indian automotive landscape.

Propelling Factors for India Automotive Advanced Driver Assistance Systems Market Growth

The India Automotive ADAS Market is propelled by a robust combination of technological, economic, and regulatory influences.

- Technological Advancements: Continuous innovation in sensor technology (Radar, LiDAR, Cameras), AI algorithms, and processing power is leading to more capable and cost-effective ADAS solutions.

- Government Initiatives & Regulations: The Indian government's increasing focus on road safety, coupled with potential future mandates for advanced safety features, is a significant catalyst.

- Rising Consumer Demand for Safety: Growing awareness among Indian consumers about the benefits of ADAS in preventing accidents and enhancing driving comfort is a key demand driver.

- Increasing Per Capita Income and Vehicle Affordability: As incomes rise, more consumers can afford vehicles equipped with advanced technologies.

- Growth of the Automotive Industry: The overall expansion of the Indian automotive sector, including the increasing production of passenger and commercial vehicles, naturally boosts the adoption of ADAS.

Obstacles in the India Automotive Advanced Driver Assistance Systems Market Market

Despite the promising growth trajectory, the India Automotive ADAS Market faces several significant obstacles.

- High Cost of Advanced Technologies: While costs are decreasing, the initial investment for sophisticated ADAS features can still be prohibitive for a large segment of the Indian car-buying population, limiting mass adoption.

- Infrastructure Limitations: Inadequate road infrastructure, poor lane markings, and unpredictable driving behaviors in certain regions can challenge the effective functioning and reliability of some ADAS features, particularly those relying heavily on precise lane keeping or object recognition.

- Consumer Awareness and Understanding: A segment of the consumer base still lacks complete understanding or trust in ADAS technologies, leading to hesitant adoption.

- Skilled Workforce Shortage: A lack of skilled technicians for installation, maintenance, and repair of complex ADAS systems can pose a challenge for service providers.

- Data Security and Privacy Concerns: As ADAS systems collect and process more data, concerns around data security and privacy may emerge as a factor influencing consumer acceptance.

Future Opportunities in India Automotive Advanced Driver Assistance Systems Market

The India Automotive ADAS Market presents several exciting future opportunities.

- Expansion into Commercial Vehicles: The potential for ADAS in improving safety and efficiency in commercial fleets, including trucks and buses, is immense.

- Development of Affordable ADAS Solutions: Innovations leading to lower-cost ADAS packages can unlock significant growth in the mass-market passenger vehicle segment.

- Integration with Connectivity and IoT: The convergence of ADAS with connected car technologies and the Internet of Things (IoT) will enable advanced features like V2X communication and predictive maintenance.

- Autonomous Driving Aspirations: As India moves towards higher levels of vehicle automation, ADAS will serve as the foundational technology for future autonomous driving systems.

- Aftermarket Customization and Retrofitting: Opportunities exist for specialized players to offer retrofitted ADAS solutions for older vehicles.

Major Players in the India Automotive Advanced Driver Assistance Systems Market Ecosystem

- Hyundai Mobis

- Mobileye

- Infineon Technologies

- Delphi Automotive

- Aisin Seiki Co Ltd

- Continental AG

- Robert Bosch GmbH

- Hella KGAA Hueck & Co

- Magna International

- DENSO Corporation

- WABCO Vehicle Control Services

- ZF Friedrichshafen AG

Key Developments in India Automotive Advanced Driver Assistance Systems Market Industry

- January 2024: Mobileye announced a partnership with Mahindra & Mahindra Ltd to provide multiple solutions based on Mobileye's next-generation EyeQ 6 systems-on-chip and sensing and mapping software, intending to build a full-stack autonomous driving system.

- January 2023: Kia Motors introduced UVO, an advanced, dynamic, and innovative connected car solution that seamlessly integrates smartphone, car, and its infotainment system into a single unit to provide a secure, convenient, and joyful experience.

- June 2022: In India, ZF Group inaugurated its new Tech center facility in Hyderabad. The Tech Center India is critical for ZF Group in the technology domains of e-mobility, ADAS, integrated safety, vehicle motion control, and digitalization.

Strategic India Automotive Advanced Driver Assistance Systems Market Market Forecast

The strategic forecast for the India Automotive ADAS Market anticipates sustained and robust growth, driven by a synergistic interplay of technological advancements, proactive government policies, and evolving consumer expectations. The increasing emphasis on road safety, coupled with the successful integration of ADAS features into a wider array of vehicle models, will act as primary growth catalysts. Investments in research and development for more affordable and contextually relevant ADAS solutions, particularly those addressing Indian road conditions and driving behaviors, will further unlock market potential. The burgeoning electric vehicle segment is also expected to be a significant adopter of ADAS, presenting a dual growth opportunity. The market is poised to transition from a focus on basic driver assistance to more sophisticated, semi-autonomous functionalities, positioning India as a key emerging market in the global ADAS landscape.

India Automotive Advanced Driver Assistance Systems Market Segmentation

-

1. Type

-

1.1. Parking Assist System

- 1.1.1. Night Vision System

- 1.1.2. Blind Spot Detection

- 1.1.3. Advanced Automatic Emergency Braking System

- 1.1.4. Collision Warning

- 1.1.5. Driver Drowsiness Alert

- 1.1.6. Traffic Sign Recognition

- 1.1.7. Lane Departure Warning

- 1.1.8. Adaptive Cruise Control

-

1.2. By Technology

- 1.2.1. Radar

- 1.2.2. LiDAR

- 1.2.3. Camera

-

1.3. By Vehicle Type

- 1.3.1. Passenger Cars

- 1.3.2. Commercial Vehicles

-

1.1. Parking Assist System

India Automotive Advanced Driver Assistance Systems Market Segmentation By Geography

- 1. India

India Automotive Advanced Driver Assistance Systems Market Regional Market Share

Geographic Coverage of India Automotive Advanced Driver Assistance Systems Market

India Automotive Advanced Driver Assistance Systems Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.33% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Parking Assist System

- 5.1.1.1. Night Vision System

- 5.1.1.2. Blind Spot Detection

- 5.1.1.3. Advanced Automatic Emergency Braking System

- 5.1.1.4. Collision Warning

- 5.1.1.5. Driver Drowsiness Alert

- 5.1.1.6. Traffic Sign Recognition

- 5.1.1.7. Lane Departure Warning

- 5.1.1.8. Adaptive Cruise Control

- 5.1.2. By Technology

- 5.1.2.1. Radar

- 5.1.2.2. LiDAR

- 5.1.2.3. Camera

- 5.1.3. By Vehicle Type

- 5.1.3.1. Passenger Cars

- 5.1.3.2. Commercial Vehicles

- 5.1.1. Parking Assist System

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Automotive Advanced Driver Assistance Systems Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Parking Assist System

- 6.1.1.1. Night Vision System

- 6.1.1.2. Blind Spot Detection

- 6.1.1.3. Advanced Automatic Emergency Braking System

- 6.1.1.4. Collision Warning

- 6.1.1.5. Driver Drowsiness Alert

- 6.1.1.6. Traffic Sign Recognition

- 6.1.1.7. Lane Departure Warning

- 6.1.1.8. Adaptive Cruise Control

- 6.1.2. By Technology

- 6.1.2.1. Radar

- 6.1.2.2. LiDAR

- 6.1.2.3. Camera

- 6.1.3. By Vehicle Type

- 6.1.3.1. Passenger Cars

- 6.1.3.2. Commercial Vehicles

- 6.1.1. Parking Assist System

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Hyundai Mobis*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mobileye

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Infineon Technologies

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Delphi Automotive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Aisin Seiki Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Continental AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Robert Bosch GmbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Hella KGAA Hueck & Co

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Magna International

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 DENSO Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 WABCO Vehicle Control Services

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 ZF Friedrichshafen AG

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Hyundai Mobis*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Automotive Advanced Driver Assistance Systems Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Automotive Advanced Driver Assistance Systems Market Share (%) by Company 2025

List of Tables

- Table 1: India Automotive Advanced Driver Assistance Systems Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: India Automotive Advanced Driver Assistance Systems Market Revenue Million Forecast, by Region 2020 & 2033

- Table 3: India Automotive Advanced Driver Assistance Systems Market Revenue Million Forecast, by Type 2020 & 2033

- Table 4: India Automotive Advanced Driver Assistance Systems Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Automotive Advanced Driver Assistance Systems Market?

The projected CAGR is approximately 18.33%.

2. Which companies are prominent players in the India Automotive Advanced Driver Assistance Systems Market?

Key companies in the market include Hyundai Mobis*List Not Exhaustive, Mobileye, Infineon Technologies, Delphi Automotive, Aisin Seiki Co Ltd, Continental AG, Robert Bosch GmbH, Hella KGAA Hueck & Co, Magna International, DENSO Corporation, WABCO Vehicle Control Services, ZF Friedrichshafen AG.

3. What are the main segments of the India Automotive Advanced Driver Assistance Systems Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.51 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Concerns About Road Safety and Government Initiatives To Enhance Demand In The Market?; Growing Adoption of New Technologies?.

6. What are the notable trends driving market growth?

Growing Demand For ADAS Features In Vehicles.

7. Are there any restraints impacting market growth?

High Cost and Limited Penetration Rate?.

8. Can you provide examples of recent developments in the market?

January 2024: Mobileye announced a partnership with Mahindra & Mahindra Ltd to provide multiple solutions based on Mobileye's next-generation EyeQ 6 systems-on-chip and sensing and mapping software, intending to build a full-stack autonomous driving system.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Automotive Advanced Driver Assistance Systems Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Automotive Advanced Driver Assistance Systems Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Automotive Advanced Driver Assistance Systems Market?

To stay informed about further developments, trends, and reports in the India Automotive Advanced Driver Assistance Systems Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence