Key Insights

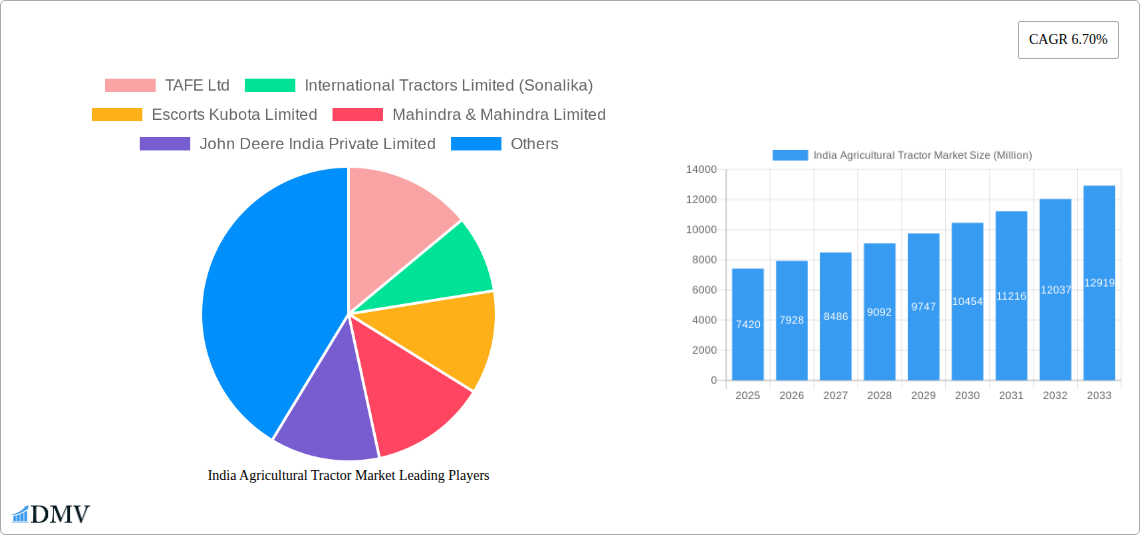

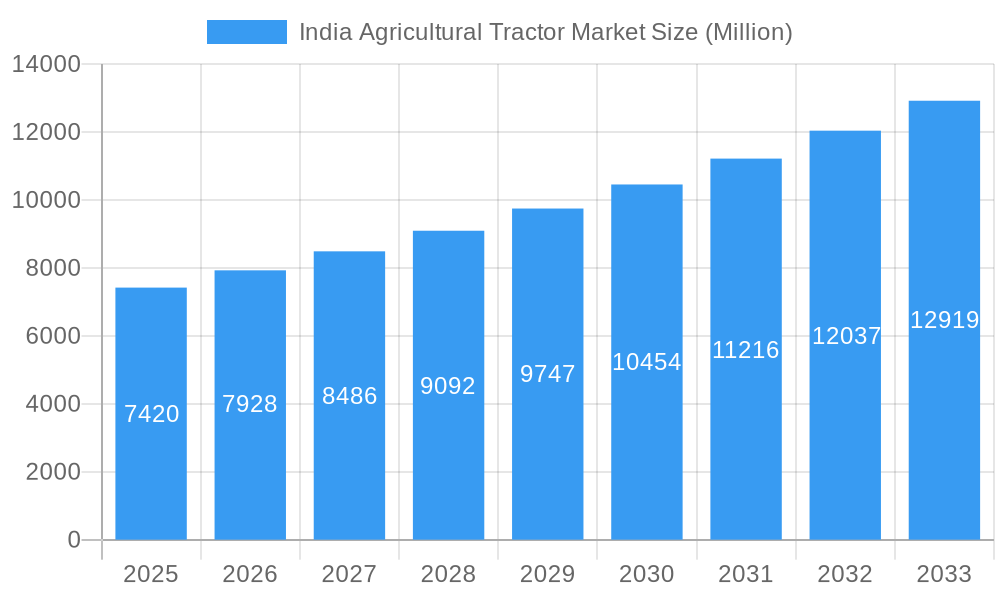

The India Agricultural Tractor Market is poised for significant expansion, demonstrating a powerful growth trajectory that is projected to achieve a market size of 7.42 Million by 2025. This robust growth is anticipated to continue with an impressive 6.70% Compound Annual Growth Rate (CAGR) extending through the forecast period to 2033. This substantial market momentum is primarily fueled by extensive government initiatives dedicated to bolstering farm mechanization and enhancing agricultural productivity across the nation. Schemes promoting subsidies, easier access to credit, and various agricultural development programs are actively encouraging farmers to invest in modern farm equipment. The imperative to increase agricultural output to meet the demands of a growing population, coupled with an escalating shortage of farm labor in rural areas, further accelerates the adoption of efficient mechanized farming solutions, making tractors indispensable assets for contemporary agricultural practices. Furthermore, a discernible rise in disposable income among farmers and continuous technological advancements, including smart features, GPS integration, and enhanced fuel efficiency in newer tractor models, are driving purchasing decisions and significantly contributing to overall market dynamism.

India Agricultural Tractor Market Market Size (In Million)

Looking ahead, the market is characterized by several evolving trends. There's a growing preference among farmers for higher horsepower utility and row crop tractors, particularly in the 40 HP to 150 HP range and even extending to 151 HP to 250 HP categories, to manage larger landholdings and perform diverse farming tasks more efficiently. The adoption of 4-wheel drive technology is also gaining traction, valued for its superior performance, traction, and versatility across varied terrains and challenging weather conditions. While traditional Internal Combustion Engine (ICE) models currently dominate the market landscape, a nascent yet growing interest in electric propulsion systems signals a future shift towards more sustainable and environmentally friendly agricultural practices. Leading manufacturers, including Mahindra & Mahindra Ltd., Deere & Company, Escorts Ltd., and Tractors and Farm Equipment Limited, are strategically investing in research and development, expanding their extensive authorized dealer networks, and providing comprehensive after-sales support and flexible financing options to cater to the evolving needs of Indian farmers. Despite potential challenges such as fluctuating agricultural commodity prices and the initial capital outlay for equipment, the robust underlying demand for food grains and consistent strategic support from governmental bodies ensure a resilient and promising future for the India Agricultural Tractor Market.

India Agricultural Tractor Market Company Market Share

India Agricultural Tractor Market Market Composition & Trends

The India agricultural tractor market is characterized by a dynamic interplay of established players and emerging innovators, leading to a moderately concentrated competitive landscape. Market concentration sees the top three companies, Mahindra & Mahindra Ltd., Escorts Ltd., and Tractors and Farm Equipment Limited, collectively commanding over 60% of the market share, driven by extensive dealer networks, diverse product portfolios, and strong brand loyalty among Indian farmers. Innovation catalysts are primarily centered around enhancing fuel efficiency, improving operator comfort, and integrating advanced technologies such as telematics, GPS, and precision farming capabilities. The push towards electric tractors, as evidenced by TAFE's recent introductions, signals a significant shift towards sustainable and technologically advanced farming solutions, with electric tractor sales projected to grow by an impressive 25% annually over the next five years.

Regulatory landscapes, including government subsidies for farm mechanization, favorable loan schemes for tractor purchases, and standards for emissions, significantly influence market dynamics. For instance, the government's focus on doubling farmer income is a major driver for increased adoption of modern agricultural machinery. Substitute products, while not a direct threat to tractor sales for large-scale farming, include traditional manual labor and animal-drawn implements, which still persist in smaller landholdings. However, the increasing labor scarcity and rising operational costs are steadily pushing even small farmers towards mechanization. End-user profiles vary from small and marginal farmers utilizing compact and utility tractors for basic tillage and haulage to large commercial farms requiring high-horsepower, specialized tractors for diverse applications. The average farm size in India, at 1.08 hectares, primarily drives demand for compact and utility segments.

M&A activities, though not as frequent as in some global markets, are strategically significant. Recent years have seen focused investments, such as Sonalika Tractors' USD 157.4 Million investment in new plants in Punjab, indicating inorganic growth strategies and capacity expansion to meet escalating demand. While specific M&A deal values in the past year might hover around USD xx Million, the trend is towards strategic alliances and joint ventures to leverage technological expertise and market reach. For example, collaborations between domestic manufacturers and international players like Deere & Company and CNH Industrial N.V. facilitate technology transfer and product localization. The market also observes an increasing push towards after-sales service and spare parts availability, which is crucial for customer retention in this capital-intensive sector. The shift towards 4 Wheel Drive (4WD) tractors, particularly in the 40 HP to 150 HP segment, reflects farmers' growing preference for enhanced traction and efficiency in diverse terrains.

India Agricultural Tractor Market Industry Evolution

The India agricultural tractor market is undergoing a profound industry evolution, marked by robust growth trajectories, significant technological advancements, and rapidly shifting consumer demands, all propelled by a concerted effort towards enhanced farm productivity and efficiency. Historically, the market has demonstrated resilience, even amidst economic fluctuations, with a compound annual growth rate (CAGR) of approximately 7.5% from 2019 to 2024, reaching an estimated market value of USD 15.8 Billion by 2025. This growth is primarily fueled by government initiatives promoting farm mechanization, increasing agricultural output requirements, and the gradual consolidation of fragmented landholdings in certain regions. The adoption rate of mechanization has steadily climbed, with tractor penetration reaching an estimated 50% of arable land, indicating substantial room for further expansion, particularly in eastern and central India.

Technological advancements are at the forefront of this evolution. Manufacturers are investing heavily in research and development to introduce tractors that are not only more powerful and fuel-efficient but also incorporate smart farming solutions. The introduction of electric tractors by Tractors and Farm Equipment Limited in January 2024, equipped with auto-steer and integrated farm management systems, exemplifies this trend. These innovations are critical for addressing the modern Indian farmer's need for precision agriculture, reduced operational costs, and environmental sustainability. Furthermore, the shift from purely mechanical systems to electronically controlled engines and hydraulic systems is enhancing the overall performance and versatility of tractors across various HP segments. The market has observed a remarkable increase in the adoption of tractors in the 40 HP to 150 HP range, which accounts for over 70% of total sales, reflecting the diverse operational needs of Indian agriculture from tilling to harvesting and haulage.

Shifting consumer demands are another pivotal aspect of the industry's evolution. Farmers are no longer merely seeking functional machinery; they demand multi-utility vehicles that offer comfort, advanced features, and improved uptime. This has led to a surge in demand for tractors with ergonomically designed cabins, advanced safety features, and robust after-sales support. The rising awareness about the benefits of 4 Wheel Drive (4WD) tractors for improved traction and productivity in challenging terrains has seen this segment grow at a CAGR of xx%, indicating a clear preference shift. Moreover, the increasing average income of farmers, coupled with easier access to credit, empowers them to invest in higher-value, more technologically advanced tractors. The market is also witnessing a burgeoning demand for specialized tractors, such as orchard and specialty tractors, particularly in states focusing on horticulture and high-value crops. This nuanced demand landscape compels manufacturers to innovate continuously and diversify their product offerings to cater to a broad spectrum of agricultural needs. The investment by Sonalika Tractors in new manufacturing facilities underscores the industry's commitment to scaling production and meeting the escalating and evolving demands of the Indian agricultural sector, anticipating a market value reaching USD 23.5 Billion by 2033.

Leading Regions, Countries, or Segments in India Agricultural Tractor Market

Within the diverse India agricultural tractor market, the 40 HP to 150 HP horsepower segment stands out as the dominant force, reflecting the core operational needs of a vast majority of Indian farmers. This segment not only accounts for the largest share of tractor sales but also demonstrates robust growth potential due to its versatility, affordability, and suitability for a wide array of agricultural tasks prevalent across the country.

Key Drivers for Dominance of 40 HP to 150 HP Segment:

- Versatility in Applications: Tractors within this horsepower range are ideally suited for a comprehensive range of agricultural operations, from primary tillage and sowing to inter-cultivation, spraying, and harvesting, making them indispensable for diversified farming practices in India. They efficiently power various implements like rotavators, cultivators, threshers, and trailers.

- Optimal Balance of Power and Fuel Efficiency: This segment strikes an optimal balance between sufficient power for demanding tasks and fuel efficiency, a critical factor for Indian farmers who operate under tight budgetary constraints. The operational cost per acre is often more favorable compared to higher horsepower categories, appealing to both small and medium-scale farmers.

- Investment Trends and Affordability: Government subsidies and financing schemes predominantly target tractors within this range, making them more accessible and affordable for a broader base of farmers. Financial institutions also show a preference for lending against these popular models, leading to easier credit availability.

- Farm Size and Cropping Patterns: Given the average farm size in India, and the prevalent cropping patterns which include cereals, pulses, and cash crops, tractors in the 40 HP to 150 HP category are perfectly matched to the scale and type of operations. They are neither over-powered for smaller plots nor under-powered for medium-sized landholdings.

- Manufacturer Focus and Product Innovation: Leading manufacturers like Mahindra & Mahindra Ltd., Escorts Ltd., and Tractors and Farm Equipment Limited heavily focus their R&D and product launches in this segment. This concentration leads to a wide variety of models, features, and price points, catering to diverse farmer preferences. The introduction of advanced features such as enhanced hydraulics, power steering, and comfortable operator cabins further solidifies its appeal.

- Dealer Network and After-Sales Support: The robust sales and service networks established by major players are most extensive for tractors in this horsepower category, ensuring easy access to spare parts, maintenance, and technical support, which is a crucial consideration for buyers.

- Regulatory Support: Policies promoting mechanization and modern agricultural practices indirectly bolster demand for this segment as it represents the entry point for many farmers transitioning from traditional methods.

The dominance of the 40 HP to 150 HP segment is further reinforced by the continuous evolution in tractor technology, making these machines more robust, durable, and capable of handling increasingly sophisticated implements. While the Less Than 40 HP segment caters to marginal farmers and niche applications, and the 151 HP to 250 HP segment targets larger commercial farms, the 40 HP to 150 HP range effectively bridges the gap, serving the largest demographic of agriculturalists. It encapsulates the sweet spot where technological advancement meets practical utility and economic viability for the majority of Indian agricultural operations. This segment is projected to maintain its leading position throughout the forecast period, driven by sustained farmer demand, supportive government policies, and ongoing product innovation.

India Agricultural Tractor Market Product Innovations

Product innovations in the India agricultural tractor market are rapidly transforming farming practices, with a strong emphasis on smart, efficient, and sustainable solutions. Leading the charge are electric tractors, exemplified by the models introduced by Tractors and Farm Equipment Limited (TAFE) in January 2024. These electric tractors boast advanced features like auto steer functionality for precise field operations, minimizing human error and maximizing efficiency. Integrated farm management systems provide real-time data on tractor performance, fuel consumption, and operational metrics, allowing farmers to optimize resource utilization and make informed decisions. Beyond electric propulsion, manufacturers are also enhancing traditional ICE tractors with improved engine efficiency, telematics for remote monitoring, and advanced hydraulic systems to handle a wider range of implements. The limited edition Swaraj Tractors, commemorating their 50th anniversary, showcase a blend of heritage with modern design elements and enhanced performance, highlighting customer appreciation and brand value. These innovations collectively offer unique selling propositions such as reduced operational costs, lower emissions, increased productivity, and enhanced operator comfort, propelling the adoption of next-generation agricultural machinery across India.

Propelling Factors for India Agricultural Tractor Market Growth

The India agricultural tractor market is experiencing significant growth propelled by several key factors. Technological advancements are paramount, with the introduction of fuel-efficient engines, precision farming features like GPS guidance, and the burgeoning segment of electric tractors enhancing productivity and reducing operational costs for farmers. Economically, rising disposable incomes in rural areas, coupled with supportive minimum support prices (MSPs) for various crops, enable farmers to invest in advanced farm machinery. Government initiatives, such as subsidies for farm mechanization, favorable credit schemes, and policies promoting agricultural development, play a crucial role in boosting tractor sales. For instance, schemes like the "Sub-Mission on Agricultural Mechanization" significantly reduce the upfront cost burden on farmers. The increasing scarcity of agricultural labor and the need for timely farm operations also drive demand for mechanization, solidifying tractors as indispensable assets for modern Indian agriculture.

Obstacles in the India Agricultural Tractor Market Market

Despite robust growth, the India agricultural tractor market faces several obstacles. Regulatory challenges, including fluctuating emission norms and varying state-level policies on subsidies, can create uncertainty for manufacturers and buyers. Supply chain disruptions, often exacerbated by global events or monsoon variability affecting agricultural output, can lead to increased input costs for raw materials and delays in production, impacting overall market stability. The highly competitive nature of the market, with numerous domestic and international players vying for market share, puts pressure on pricing and profit margins. Furthermore, the dependence on monsoon for a significant portion of agriculture makes the market susceptible to climatic variations, which can directly affect farmers' purchasing power and investment decisions. The relatively fragmented landholdings also pose a challenge for the adoption of higher horsepower and specialized tractors, limiting their market penetration in certain regions.

Future Opportunities in India Agricultural Tractor Market

The India agricultural tractor market is poised for significant future opportunities driven by several emerging trends. The increasing adoption of precision agriculture technologies, including IoT-enabled sensors and data analytics for smart farming, presents a vast potential for advanced tractor models with integrated solutions. New market segments, particularly in the rental economy for agricultural machinery, will cater to small and marginal farmers who cannot afford outright purchases, democratizing access to modern tractors. The shift towards sustainable agriculture is accelerating the demand for electric and alternative-fuelled tractors, creating a new niche for manufacturers. Furthermore, export opportunities to neighboring developing countries, leveraging India's manufacturing capabilities and cost-effectiveness, could expand market horizons. Focus on specialized tractors for horticulture and plantation crops, along with a growing emphasis on post-harvest mechanization, will unlock diverse revenue streams and foster sustained market expansion.

Major Players in the India Agricultural Tractor Market Ecosystem

- Escorts Ltd.

- Tractors and Farm Equipment Limited

- Mahindra & Mahindra Ltd.

- Deere & Company

- AGCO Corp.

- Iseki & Co. Ltd.

- Claas KGaA mbH

- Massey Ferguson

- New Holland

- Qilu Machinery

- Case IH

- International Tractors Ltd

- CNH Industrial N.V.

- Kubota Corp.

- Yanmar Co., Ltd.

- Others

Key Developments in India Agricultural Tractor Market Industry

- April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, features MS Dhoni's signature as a symbol of gratitude to the customers, boosting brand visibility and celebrating customer loyalty. This strategic move aims to enhance brand recall and potentially drive short-term sales through its unique collector's appeal.

- March 2024: Sonalika Tractors invested USD 157.4 Million for two new plants in Punjab. The company allocated USD 121.1 Million for a new tractor assembly plant and USD 36.3 Million for a high-pressure foundry. This significant investment is set to increase manufacturing capacity, reduce reliance on external suppliers for critical components, and strengthen Sonalika's competitive position in the rapidly expanding Indian agricultural tractor market.

- January 2024: Tractors and Farm Equipment Limited (TAFE) introduced electric tractors at the Tamil Nadu Global Investors Meet (TN GIM) 2024. These tractors are equipped with auto steer and a farm management system. This innovation marks a crucial step towards sustainable and smart farming in India, addressing evolving industry demands for eco-friendly solutions and advanced agricultural technology, thereby diversifying product offerings and tapping into future market trends.

Strategic India Agricultural Tractor Market Market Forecast

The India agricultural tractor market is poised for sustained robust growth, driven by an unwavering commitment to farm mechanization and technological innovation. Future opportunities are abundant, particularly in the realm of precision agriculture and electric tractors, which promise enhanced efficiency and environmental sustainability. Government initiatives, coupled with improving rural incomes, will continue to act as significant growth catalysts, facilitating easier adoption of advanced machinery. The shift towards higher horsepower and specialized tractors, alongside the expansion of efficient sales and service networks, will unlock new market potential. As farming practices evolve, the market is set to witness increased integration of digital solutions and a greater focus on cost-effective, multi-utility models, ensuring a dynamic and prosperous future for the India agricultural tractor industry.

India Agricultural Tractor Market Segmentation

-

1. Type

- 1.1. Compact Tractors

- 1.2. Utility Tractors

- 1.3. Row Crop Tractors

- 1.4. Orchard Tractors

- 1.5. Specialty Tractors

-

2. Horse power

- 2.1. Less Than 40 HP

- 2.2. 40 HP to 150 HP

- 2.3. 151 HP to 250 HP

- 2.4. 251 HP to 350 HP

- 2.5. More Than 350 HP

-

3. Drive Type

- 3.1. 2 Wheel Drive

- 3.2. 4 Wheel Drive

-

4. Propulsion

- 4.1. Electric

- 4.2. ICE

-

5. Sales Channel

- 5.1. Direct Sales

- 5.2. Authorized Dealers and Distributors

India Agricultural Tractor Market Segmentation By Geography

- 1. India

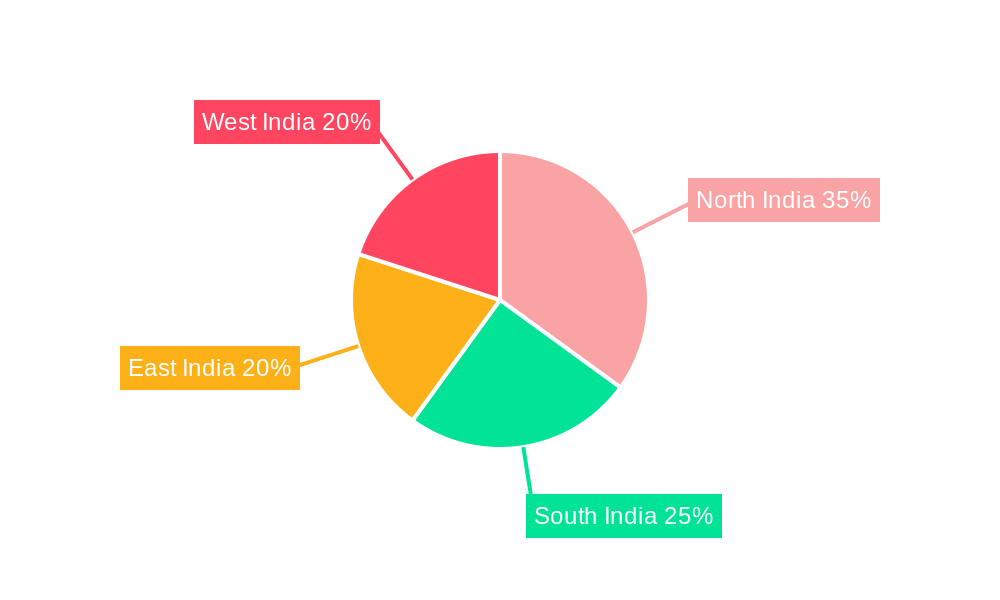

India Agricultural Tractor Market Regional Market Share

Geographic Coverage of India Agricultural Tractor Market

India Agricultural Tractor Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Compact Tractors

- 5.1.2. Utility Tractors

- 5.1.3. Row Crop Tractors

- 5.1.4. Orchard Tractors

- 5.1.5. Specialty Tractors

- 5.2. Market Analysis, Insights and Forecast - by Horse power

- 5.2.1. Less Than 40 HP

- 5.2.2. 40 HP to 150 HP

- 5.2.3. 151 HP to 250 HP

- 5.2.4. 251 HP to 350 HP

- 5.2.5. More Than 350 HP

- 5.3. Market Analysis, Insights and Forecast - by Drive Type

- 5.3.1. 2 Wheel Drive

- 5.3.2. 4 Wheel Drive

- 5.4. Market Analysis, Insights and Forecast - by Propulsion

- 5.4.1. Electric

- 5.4.2. ICE

- 5.5. Market Analysis, Insights and Forecast - by Sales Channel

- 5.5.1. Direct Sales

- 5.5.2. Authorized Dealers and Distributors

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Agricultural Tractor Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Compact Tractors

- 6.1.2. Utility Tractors

- 6.1.3. Row Crop Tractors

- 6.1.4. Orchard Tractors

- 6.1.5. Specialty Tractors

- 6.2. Market Analysis, Insights and Forecast - by Horse power

- 6.2.1. Less Than 40 HP

- 6.2.2. 40 HP to 150 HP

- 6.2.3. 151 HP to 250 HP

- 6.2.4. 251 HP to 350 HP

- 6.2.5. More Than 350 HP

- 6.3. Market Analysis, Insights and Forecast - by Drive Type

- 6.3.1. 2 Wheel Drive

- 6.3.2. 4 Wheel Drive

- 6.4. Market Analysis, Insights and Forecast - by Propulsion

- 6.4.1. Electric

- 6.4.2. ICE

- 6.5. Market Analysis, Insights and Forecast - by Sales Channel

- 6.5.1. Direct Sales

- 6.5.2. Authorized Dealers and Distributors

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Escorts Ltd.

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Tractors and Farm Equipment Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Mahindra & Mahindra Ltd.

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Deere & Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AGCO Corp.

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Iseki & Co. Ltd.

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Claas KGaA mbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Massey Ferguson

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 New Holland

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Qilu Machinery

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Case IH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 International Tractors Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 CNH Industrial N.V.

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Kubota Corp.

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Yanmar Co. Ltd.

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Others

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.1 Escorts Ltd.

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Agricultural Tractor Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: India Agricultural Tractor Market Share (%) by Company 2025

List of Tables

- Table 1: India Agricultural Tractor Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: India Agricultural Tractor Market Revenue Million Forecast, by Horse power 2020 & 2033

- Table 3: India Agricultural Tractor Market Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 4: India Agricultural Tractor Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 5: India Agricultural Tractor Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 6: India Agricultural Tractor Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: India Agricultural Tractor Market Revenue Million Forecast, by Type 2020 & 2033

- Table 8: India Agricultural Tractor Market Revenue Million Forecast, by Horse power 2020 & 2033

- Table 9: India Agricultural Tractor Market Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 10: India Agricultural Tractor Market Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 11: India Agricultural Tractor Market Revenue Million Forecast, by Sales Channel 2020 & 2033

- Table 12: India Agricultural Tractor Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Agricultural Tractor Market?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the India Agricultural Tractor Market?

Key companies in the market include Escorts Ltd., Tractors and Farm Equipment Limited, Mahindra & Mahindra Ltd., Deere & Company, AGCO Corp., Iseki & Co. Ltd., Claas KGaA mbH, Massey Ferguson, New Holland, Qilu Machinery, Case IH, International Tractors Ltd, CNH Industrial N.V., Kubota Corp., Yanmar Co., Ltd., Others.

3. What are the main segments of the India Agricultural Tractor Market?

The market segments include Type, Horse power, Drive Type, Propulsion, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.42 Million as of 2022.

5. What are some drivers contributing to market growth?

Mechanization Trend in Agriculture Sector; Trend of Custom Hiring of Tractors.

6. What are the notable trends driving market growth?

30-50 HP Tractors Are Widely Preferred.

7. Are there any restraints impacting market growth?

Lack of Awareness and Skilled Manpower; Poor Economic Condition of Farmers.

8. Can you provide examples of recent developments in the market?

April 2024: Swaraj Tractors introduced five variants in a limited edition on its 50th anniversary. This edition, available for two months, has MS Dhoni's signature as a symbol of gratitude to the customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Agricultural Tractor Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Agricultural Tractor Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Agricultural Tractor Market?

To stay informed about further developments, trends, and reports in the India Agricultural Tractor Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence