Key Insights

The global fresh dog food market is projected for substantial growth, expected to reach $51.27 billion by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 6%. This expansion is primarily attributed to increasing consumer focus on pet nutrition and well-being. Owners are actively seeking high-quality, natural, and minimally processed food options for their dogs, aligning with human dietary trends. Key growth drivers include rising pet adoption rates, increased disposable income enabling premium pet care, and greater awareness of the health benefits of fresh, whole-ingredient dog food. The proliferation of direct-to-consumer (DTC) models and subscription services further enhances accessibility and convenience.

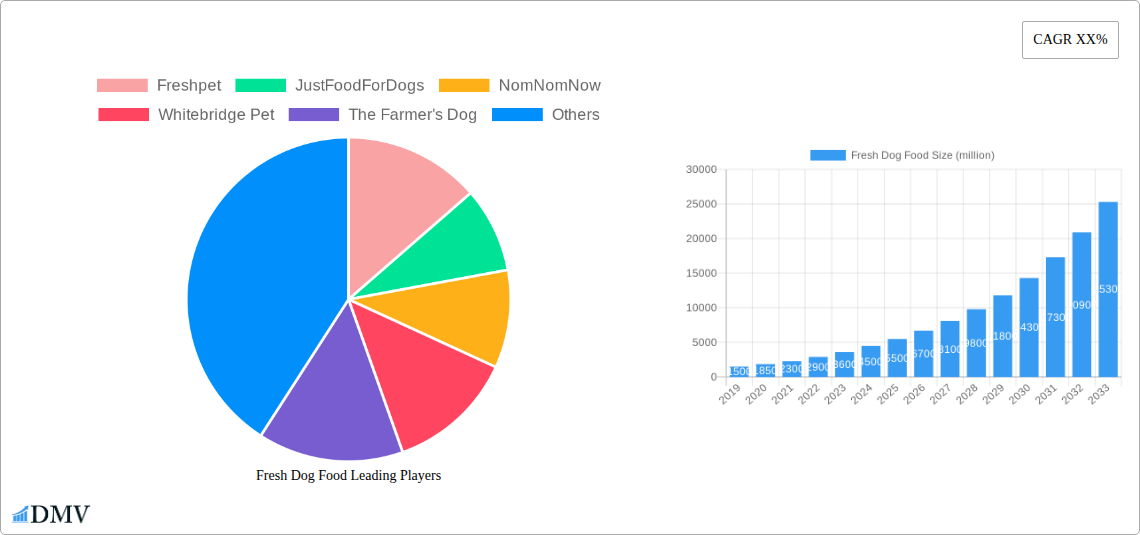

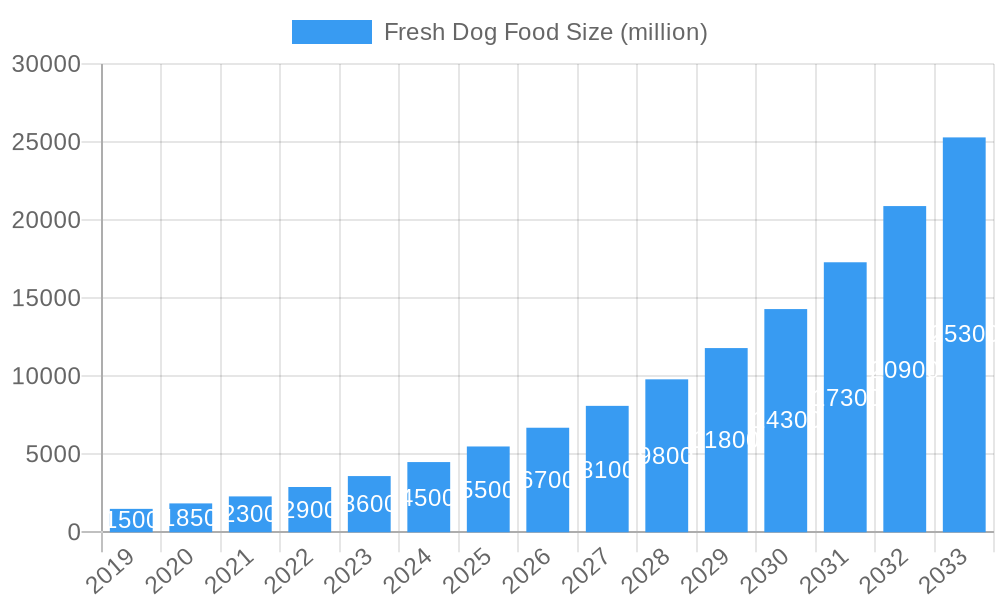

Fresh Dog Food Market Size (In Billion)

Market segmentation spans various distribution channels, with supermarkets and hypermarkets leading, followed by pet specialty stores and veterinary clinics. Product categories include puppy and adult dog food, addressing specific life stages and nutritional requirements. Leading companies are innovating with diverse recipes and sustainable packaging. However, challenges such as the higher price point of fresh dog food and logistical complexities related to maintaining product freshness may temper growth. Despite these restraints, strong consumer demand and strategic innovation point to a promising future for the fresh dog food industry.

Fresh Dog Food Company Market Share

Fresh Dog Food Market Research Report: 2025-2033

This comprehensive fresh dog food market research report offers an in-depth analysis of the rapidly evolving premium dog food sector, projecting significant growth and uncovering key opportunities. With a study period spanning from 2019 to 2033, this report provides invaluable insights into market dynamics, consumer preferences, and the competitive landscape. Our base year analysis for 2025 and forecast period from 2025 to 2033 meticulously detail future trends and market potential. Leveraging historical data from 2019-2024, we present a robust and data-driven outlook for stakeholders seeking to capitalize on the booming human-grade dog food and natural dog food markets.

Fresh Dog Food Market Composition & Trends

The fresh dog food market is characterized by a dynamic blend of established players and emerging innovators, driving a constant influx of novel product offerings. Market concentration varies across regions, with some areas exhibiting a more consolidated structure dominated by a few key brands, while others showcase a fragmented landscape with numerous niche providers. Innovation is a primary catalyst, fueled by a growing consumer demand for healthy dog food alternatives to traditional kibble. This includes advancements in ingredient sourcing, formulation, and preservation techniques to ensure optimal nutrition and palatability. The regulatory landscape plays a crucial role, with evolving guidelines around pet food safety and labeling influencing product development and market entry. Substitute products, such as high-quality dry kibble and raw diets, continue to pose a competitive challenge, though the perceived benefits of freshly prepared dog food are increasingly winning over pet owners. End-user profiles are diverse, ranging from health-conscious millennials and Gen Z pet parents to owners seeking specialized diets for pets with health conditions. Mergers and acquisitions (M&A) activity is a significant trend, with larger pet food conglomerates acquiring promising direct-to-consumer (DTC) dog food brands to expand their market reach and product portfolios. The global fresh dog food market share is projected to witness substantial expansion, with estimated M&A deal values reaching several hundred million dollars in the coming years.

- Market Share Distribution: The market is witnessing a gradual shift, with premium brands capturing a growing percentage of the overall pet food expenditure.

- Innovation Catalysts: Focus on ethically sourced ingredients, reduced processing, and customizable meal plans are key drivers.

- Regulatory Landscapes: Stringent quality control and transparent ingredient sourcing are becoming paramount for market acceptance.

- Substitute Products: High-quality, limited-ingredient dry foods and freeze-dried options remain strong competitors.

- End-User Profiles: Owners prioritizing their pet's long-term health and seeking convenient, high-quality meal solutions.

- M&A Activities: Strategic acquisitions aimed at expanding product lines and market penetration.

Fresh Dog Food Industry Evolution

The fresh dog food industry has undergone a remarkable transformation, evolving from a niche segment to a mainstream contender in the global pet food market. This evolution is fundamentally driven by a seismic shift in consumer perception, with pet owners increasingly viewing their canine companions as integral family members who deserve the same nutritional quality as humans. This anthropomorphic trend has propelled the demand for human-grade dog food, leading to significant market growth trajectories. The fresh dog food market size is anticipated to reach billions in the coming years, a testament to its burgeoning popularity. Technological advancements have been instrumental in this evolution. Innovations in food processing, packaging, and subscription-based delivery models have made healthy dog food more accessible and convenient than ever before. Companies have invested heavily in research and development to create scientifically formulated meals that cater to specific dietary needs, life stages, and health concerns of dogs. This includes the development of grain-free dog food, limited ingredient dog food, and hypoallergenic dog food options. The adoption of these advanced formulations is a key metric, with growth rates in this area consistently outperforming traditional pet food segments. Furthermore, the rise of e-commerce and DTC dog food models has democratized access to premium pet nutrition, allowing smaller brands to reach a wider audience and compete effectively with established players. Shifting consumer demands are a continuous influence, pushing brands to offer greater transparency in ingredient sourcing, sustainable packaging solutions, and personalized meal plans. The increasing awareness of the impact of diet on canine health, from gut health to chronic disease prevention, further fuels the demand for natural dog food and freshly prepared dog food. This sustained demand, coupled with ongoing innovation, paints a picture of a vibrant and continuously evolving industry.

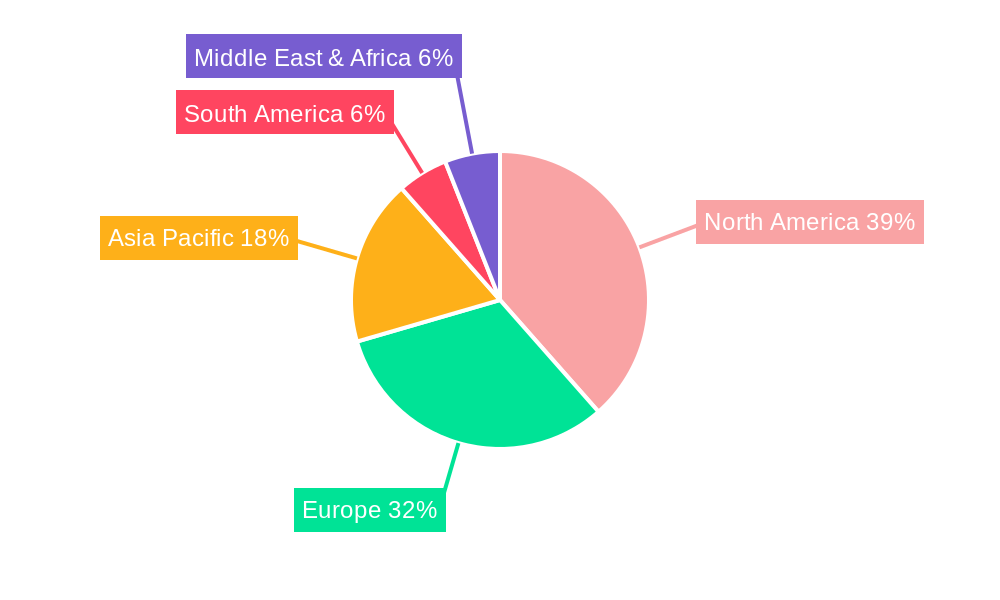

Leading Regions, Countries, or Segments in Fresh Dog Food

The fresh dog food market exhibits distinct regional leadership and segment dominance, driven by a confluence of economic prosperity, heightened pet humanization, and supportive regulatory frameworks. In terms of application, Pet Specialty Stores and Vet Clinics currently lead the charge, accounting for a significant portion of market share. This dominance is attributed to their ability to offer expert advice, specialized product ranges, and build trust with pet owners seeking premium and therapeutic dietary solutions. The inherent credibility of veterinary recommendations and the curated selections available in these outlets make them prime destinations for purchasing healthy dog food. However, Supermarkets and Hypermarkets are rapidly gaining traction, fueled by increasing shelf space dedicated to fresh dog food brands and the convenience they offer to a broader consumer base. The growing adoption of subscription models and direct-to-consumer (DTC) offerings is also reshaping the landscape, potentially elevating the 'Others' segment in the future.

Geographically, North America, particularly the United States, remains a dominant region, characterized by high disposable incomes, a deeply ingrained pet culture, and a pioneering spirit in adopting new pet care trends. Investment trends in R&D and marketing by major players have been substantial in this region, solidifying its leadership. European countries, with their growing awareness of pet wellness and increasing demand for natural and organic products, are also emerging as significant markets.

Within product types, Adult Dog Food currently holds the largest market share, reflecting the majority of the canine population. However, the Puppies Dog Food segment is witnessing exceptional growth, driven by a proactive approach from owners to provide the best nutrition from the earliest stages of a puppy's life. This surge is supported by an understanding of the critical role nutrition plays in early development and the prevention of future health issues. Regulatory support, while varying by country, generally leans towards ensuring the safety and efficacy of pet food products, creating a stable environment for growth.

Key Drivers for Pet Specialty Stores & Vet Clinics:

- Expert guidance and personalized recommendations.

- Trust and credibility associated with veterinary professionals.

- Access to specialized and therapeutic diets.

- Higher perceived quality of products.

Key Drivers for Supermarkets & Hypermarkets:

- Convenience and accessibility for a broader consumer base.

- Increasing variety of fresh dog food options on shelves.

- Competitive pricing strategies.

- Growing consumer demand for one-stop shopping.

Dominant Geographic Region (North America):

- High disposable income and spending on pets.

- Strong pet humanization trends.

- Early adoption of premium and innovative pet products.

- Significant investment by leading brands.

Dominant Product Type (Adult Dog Food):

- Largest segment of the canine population.

- Established market with a wide range of options.

High Growth Product Type (Puppies Dog Food):

- Proactive pet parenting focus on early nutrition.

- Emphasis on developmental health and long-term well-being.

- Increasing availability of puppy-specific formulations.

Fresh Dog Food Product Innovations

Product innovation in the fresh dog food market is relentlessly focused on enhancing nutritional completeness, palatability, and convenience. Manufacturers are leveraging advanced food science to create whole dog food recipes that mimic a dog's ancestral diet, utilizing high-quality, single-source proteins and a diverse array of nutrient-rich vegetables and fruits. Unique selling propositions often revolve around the use of human-grade ingredients, free from artificial preservatives, colors, and fillers, directly addressing consumer concerns about the quality and safety of pet food. Technological advancements in flash-freezing and vacuum-sealing technologies have been crucial in preserving the freshness and nutritional integrity of these meals, extending shelf life without compromising on quality. Performance metrics are increasingly being tracked, with brands highlighting improvements in canine health indicators such as coat shininess, digestive regularity, and energy levels, providing tangible evidence of the benefits of their freshly prepared dog food offerings.

Propelling Factors for Fresh Dog Food Growth

The surge in fresh dog food demand is propelled by several interconnected factors. Economically, rising disposable incomes and increased pet expenditure globally enable more owners to invest in premium nutrition. Technologically, advancements in food preservation, personalized nutrition platforms, and efficient DTC dog food delivery systems have made these products more accessible and convenient. Regulatory frameworks, while evolving, are increasingly focused on consumer safety and ingredient transparency, inadvertently favoring brands that adhere to higher quality standards. Furthermore, a significant cultural shift towards pet humanization has elevated the importance of canine health and well-being, driving owners to seek out healthier, more natural alternatives like freshly made dog food. The growing awareness of the link between diet and long-term health outcomes for dogs, including issues like obesity, allergies, and digestive sensitivities, further fuels the adoption of premium dog food solutions.

Obstacles in the Fresh Dog Food Market

Despite its robust growth, the fresh dog food market faces several formidable obstacles. Regulatory hurdles, particularly concerning novel ingredients and varying labeling requirements across different regions, can complicate market entry and expansion for new and existing players. Supply chain disruptions, amplified by the perishable nature of fresh ingredients, pose a significant challenge in ensuring consistent product availability and minimizing spoilage. The high cost of production, stemming from premium ingredient sourcing and specialized processing, often translates to higher retail prices, making affordable fresh dog food a persistent aspiration rather than a widespread reality for many pet owners. Competitive pressures are also intense, with both established pet food giants launching their own fresh lines and a multitude of agile DTC dog food startups vying for market share, leading to a crowded marketplace.

Future Opportunities in Fresh Dog Food

The future of the fresh dog food market is brimming with opportunities. Emerging technologies in fermentation and personalized nutrition offer pathways to create even more targeted and beneficial canine diets. The untapped potential of emerging markets in Asia and Latin America, where pet ownership is rapidly increasing, presents significant growth avenues for natural dog food brands. E-commerce and subscription models will continue to evolve, offering greater customization and convenience for consumers seeking healthy dog food delivered directly to their homes. Furthermore, the growing consumer demand for sustainable and ethically sourced products provides an opportunity for brands to differentiate themselves through transparent practices and eco-friendly packaging, catering to the increasingly conscious pet owner seeking eco-friendly dog food.

Major Players in the Fresh Dog Food Ecosystem

- Freshpet

- JustFoodForDogs

- NomNomNow

- Whitebridge Pet

- The Farmer's Dog

- Evermore

- Market Fresh Pet Foods

- Ollie

- Xiaoxianliang

- PetPlate

- Grocery Pup

Key Developments in Fresh Dog Food Industry

- 2024 January: Freshpet launches new line of gently cooked meals targeting specific health concerns, increasing market penetration in vet clinics.

- 2023 December: NomNomNow announces expansion of its delivery network to reach xx million new households, enhancing its DTC reach.

- 2023 October: The Farmer's Dog secures an additional xx million in funding to scale production and invest in further research for personalized nutrition.

- 2023 August: Whitebridge Pet Food acquires a minority stake in a sustainable ingredient supplier, bolstering its commitment to eco-friendly sourcing.

- 2023 June: Ollie introduces a new puppy-specific meal plan, addressing the growing demand for specialized nutrition from birth.

- 2023 April: JustFoodForDogs expands its retail presence within xx major supermarket chains, increasing accessibility to its premium products.

- 2022 December: Evermore expands its product offerings to include xx new limited-ingredient recipes, catering to dogs with sensitivities.

- 2022 September: PetPlate launches a new educational campaign highlighting the benefits of fresh ingredients for canine longevity.

- 2022 July: Xiaoxianliang experiences rapid growth in the Chinese market, driven by increasing pet humanization trends.

- 2022 May: Grocery Pup partners with xx veterinary nutritionists to co-develop innovative meal plans.

- 2022 March: Market Fresh Pet Foods announces significant investment in expanding its cold chain logistics to improve product freshness nationwide.

Strategic Fresh Dog Food Market Forecast

The strategic fresh dog food market forecast indicates a period of sustained and robust growth, driven by an escalating demand for healthy dog food and the increasing acceptance of premium dog food as a dietary standard. Key growth catalysts include the unwavering trend of pet humanization, coupled with significant advancements in DTC dog food delivery models and personalized nutrition. The market's future potential lies in its ability to cater to specific dietary needs, offer enhanced transparency in ingredient sourcing, and embrace sustainable practices. The projected expansion of the global fresh dog food market presents lucrative opportunities for innovation and investment, solidifying its position as a vital and thriving segment within the broader pet care industry.

Fresh Dog Food Segmentation

-

1. Application

- 1.1. Supermarkets and Hypermarkets

- 1.2. Pet Specialty Stores and Vet Clinics

- 1.3. Convenience Stores

- 1.4. Others

-

2. Types

- 2.1. Puppies Dog Food

- 2.2. Adult Dog Food

Fresh Dog Food Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fresh Dog Food Regional Market Share

Geographic Coverage of Fresh Dog Food

Fresh Dog Food REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarkets and Hypermarkets

- 5.1.2. Pet Specialty Stores and Vet Clinics

- 5.1.3. Convenience Stores

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Puppies Dog Food

- 5.2.2. Adult Dog Food

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarkets and Hypermarkets

- 6.1.2. Pet Specialty Stores and Vet Clinics

- 6.1.3. Convenience Stores

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Puppies Dog Food

- 6.2.2. Adult Dog Food

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarkets and Hypermarkets

- 7.1.2. Pet Specialty Stores and Vet Clinics

- 7.1.3. Convenience Stores

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Puppies Dog Food

- 7.2.2. Adult Dog Food

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarkets and Hypermarkets

- 8.1.2. Pet Specialty Stores and Vet Clinics

- 8.1.3. Convenience Stores

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Puppies Dog Food

- 8.2.2. Adult Dog Food

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarkets and Hypermarkets

- 9.1.2. Pet Specialty Stores and Vet Clinics

- 9.1.3. Convenience Stores

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Puppies Dog Food

- 9.2.2. Adult Dog Food

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Fresh Dog Food Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarkets and Hypermarkets

- 10.1.2. Pet Specialty Stores and Vet Clinics

- 10.1.3. Convenience Stores

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Puppies Dog Food

- 10.2.2. Adult Dog Food

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Freshpet

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 JustFoodForDogs

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 NomNomNow

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Whitebridge Pet

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 The Farmer's Dog

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Evermore

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Market Fresh Pet Foods

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ollie

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Xiaoxianliang

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 PetPlate

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Grocery Pup

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Freshpet

List of Figures

- Figure 1: Global Fresh Dog Food Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Fresh Dog Food Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Fresh Dog Food Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Fresh Dog Food Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Fresh Dog Food Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Fresh Dog Food Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Fresh Dog Food Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Fresh Dog Food Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Fresh Dog Food Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Fresh Dog Food Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Fresh Dog Food Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Fresh Dog Food Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Fresh Dog Food Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Fresh Dog Food Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Fresh Dog Food Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Fresh Dog Food Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Fresh Dog Food Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Fresh Dog Food Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Fresh Dog Food Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Fresh Dog Food Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Fresh Dog Food Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Fresh Dog Food Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Fresh Dog Food Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Fresh Dog Food Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Fresh Dog Food Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Fresh Dog Food Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Fresh Dog Food Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Fresh Dog Food Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Fresh Dog Food Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Fresh Dog Food Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Fresh Dog Food Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Fresh Dog Food Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Fresh Dog Food Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Fresh Dog Food Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Fresh Dog Food Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Fresh Dog Food Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Fresh Dog Food Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Fresh Dog Food Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Fresh Dog Food Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Fresh Dog Food Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fresh Dog Food?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Fresh Dog Food?

Key companies in the market include Freshpet, JustFoodForDogs, NomNomNow, Whitebridge Pet, The Farmer's Dog, Evermore, Market Fresh Pet Foods, Ollie, Xiaoxianliang, PetPlate, Grocery Pup.

3. What are the main segments of the Fresh Dog Food?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 51.27 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fresh Dog Food," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fresh Dog Food report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fresh Dog Food?

To stay informed about further developments, trends, and reports in the Fresh Dog Food, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence