Key Insights

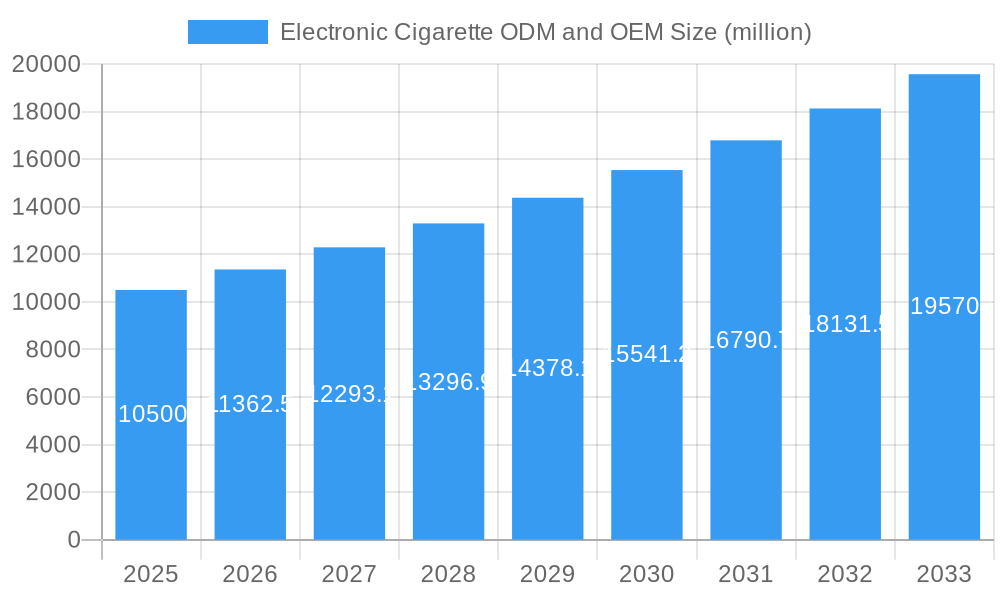

The global Electronic Cigarette ODM (Original Design Manufacturer) and OEM (Original Equipment Manufacturer) market is poised for significant expansion, estimated to reach approximately USD 10,500 million in 2025, with a projected Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This robust growth is primarily fueled by the burgeoning demand for sophisticated vaping devices and a notable shift towards Heat-Not-Burn (HNB) electronic cigarettes. The increasing acceptance of e-cigarettes as a less harmful alternative to traditional tobacco products, coupled with evolving consumer preferences for personalized and technologically advanced vaping experiences, are key market drivers. Furthermore, regulatory landscapes, while varied across regions, are generally leaning towards clearer frameworks, encouraging innovation and investment within the ODM/OEM sector. Manufacturers are increasingly focusing on product differentiation through advanced features like temperature control, variable wattage, and longer battery life, directly catering to a discerning consumer base. The segment of vaping electronic cigarettes continues to dominate, but the rapid innovation and potential health benefits associated with HNB devices are rapidly closing the gap, presenting a significant growth opportunity for ODM and OEM providers.

Electronic Cigarette ODM and OEM Market Size (In Billion)

The electronic cigarette ODM and OEM market is characterized by intense competition and continuous innovation. Key trends include the rise of specialized design houses that offer end-to-end solutions, from conceptualization and design to manufacturing and quality control. This has empowered both established brands and emerging players to bring new products to market efficiently. Geographically, Asia Pacific, particularly China, remains the manufacturing powerhouse, benefiting from established supply chains and skilled labor. However, North America and Europe are significant consumption hubs, driving demand for premium and innovative devices. Restraints to the market include evolving and sometimes stringent regulatory policies across different countries, concerns regarding product safety and potential health risks associated with e-cigarette use, and the ongoing debate about their role in tobacco harm reduction. Despite these challenges, the increasing disposable income globally and the desire for alternative smoking methods are expected to sustain the market's upward trajectory, encouraging ODM and OEM companies to invest in research and development and expand their production capabilities.

Electronic Cigarette ODM and OEM Company Market Share

<!DOCTYPE html>

<html lang="en">

<head>

<meta charset="UTF-8">

<meta name="viewport" content="width=device-width, initial-scale=1.0">

<title>Electronic Cigarette ODM and OEM Market Analysis Report</title>

<meta name="description" content="In-depth report on the Electronic Cigarette ODM and OEM market. Explore market share, industry evolution, regional dominance, product innovations, growth drivers, obstacles, opportunities, key players like Philip Morris International, RELX, and JUUL, and future market forecasts from 2019-2033. Analyze Vaping and Heat-Not-Burn segments.">

<meta name="keywords" content="Electronic Cigarette ODM, Electronic Cigarette OEM, Vaping Electronic Cigarettes, Heat-Not-Burn Electronic Cigarettes, ODM manufacturing, OEM manufacturing, vape device market, e-cigarette industry, Philip Morris International, SMOOKE, FIRST UNION GROUP, SIGELEI, RELX, YOOZ, JUUL, NJOY, MOTI, Imperial Tobacco, JTI, BYD, Joyetech holding limited, Geekvape, Kangertech, Jinjia TECHNOLOGIES, Jasper Enterprise Management Consulting, Shenzhen GreenSound Technology, Alpha Electronic Technology, JOUZ, Itron Electronics, ATOM, VGOD, Sigelei, market analysis, industry trends, market forecast, growth drivers, market obstacles, emerging opportunities, product innovation, regional analysis">

</head>

<body>

<h1>Electronic Cigarette ODM and OEM Market Analysis Report: Trends, Forecasts & Key Players (2019–2033)</h1>

<p>This comprehensive report provides a deep dive into the global Electronic Cigarette Original Design Manufacturer (ODM) and Original Equipment Manufacturer (OEM) market. Spanning the historical period of 2019-2024, with a base year of 2025 and a robust forecast period extending to 2033, this analysis is essential for stakeholders seeking to understand market dynamics, growth trajectories, and competitive landscapes. The study meticulously examines both Vaping Electronic Cigarettes and Heat-Not-Burn Electronic Cigarettes applications, offering granular insights into ODM and OEM service models. We analyze market concentration, innovation catalysts, regulatory shifts, substitute products, end-user profiles, and crucial Mergers & Acquisitions (M&A) activities, projecting a market size of over one million for key segments. Discover the strategic evolution of this dynamic industry, regional dominance, groundbreaking product innovations, and the propelling factors and obstacles shaping its future. Identify major players like Philip Morris International, RELX, JUUL, and many more, and gain a strategic outlook on market forecasts. This report is tailored for manufacturers, suppliers, investors, and industry analysts navigating the complexities of the e-cigarette manufacturing sector.</p>

<h2>Electronic Cigarette ODM and OEM Market Composition & Trends</h2>

<p>The Electronic Cigarette ODM and OEM market exhibits a dynamic composition characterized by a moderate to high concentration, with leading players like Philip Morris International, RELX, and JUUL dominating significant market share, estimated to be over 50% collectively. Innovation remains a key catalyst, driven by relentless R&D in battery technology, heating elements, and user interface design, fueling the adoption of both Vaping Electronic Cigarettes and Heat-Not-Burn Electronic Cigarettes. The regulatory landscape is complex and constantly evolving, with stricter controls in some regions contrasted by more permissive environments elsewhere, directly influencing manufacturing strategies and market entry. Substitute products, including traditional tobacco and nicotine patches, continue to pose a challenge, yet the perceived benefits of e-cigarettes, such as reduced harm and diverse flavor profiles, drive consumer demand. End-user profiles are diversifying, encompassing traditional smokers seeking alternatives, younger demographics, and existing vapers looking for advanced devices. Mergers and Acquisitions (M&A) activities are prevalent as larger entities seek to expand their product portfolios, technological capabilities, and market reach. Deal values in M&A are projected to exceed one million for significant acquisitions within the forecast period, reflecting the strategic importance and consolidation within the industry.</p>

<ul>

<li>Market Share Distribution: Leading players collectively hold over 50% of the market.</li>

<li>Innovation Focus: Battery technology, heating elements, and user experience are key R&D areas.</li>

<li>Regulatory Impact: Evolving regulations significantly shape manufacturing and market access.</li>

<li>End-User Diversification: From traditional smokers to tech-savvy vapers.</li>

<li>M&A Activity: Driven by portfolio expansion and market consolidation, with deal values exceeding one million.</li>

</ul>

<h2>Electronic Cigarette ODM and OEM Industry Evolution</h2>

<p>The Electronic Cigarette ODM and OEM industry has undergone a significant transformation since 2019, evolving from niche products to mainstream consumer goods. The historical period (2019-2024) witnessed exponential growth, primarily fueled by the rapid adoption of Vaping Electronic Cigarettes, driven by perceived harm reduction compared to traditional cigarettes and a wide array of appealing flavors. This surge in demand propelled the ODM and OEM sectors, enabling numerous manufacturers like SMOOKE, FIRST UNION GROUP, and SIGELEI to scale their operations and refine their production processes. Technological advancements have been central to this evolution, with continuous improvements in battery efficiency, pod systems, and heating coil designs leading to more sophisticated and user-friendly devices. For instance, the transition from basic e-go style devices to advanced pod mod systems and sleek, discreet disposables has been a hallmark of this period. The emergence and subsequent refinement of Heat-Not-Burn Electronic Cigarettes, championed by industry giants like Philip Morris International, introduced a new category, attracting a different consumer segment seeking a more traditional smoking experience with potentially reduced risks. This has spurred innovation in heating chamber technology and device aesthetics. Consumer demands have shifted considerably, moving from basic functionality to a preference for sleek design, long battery life, consistent vapor production, and ease of use. The rise of established brands like RELX, YOOZ, and JUUL, often leveraging robust ODM/OEM partnerships, demonstrates the importance of brand building and product differentiation. Market growth rates during the historical period averaged an impressive xx%, with adoption metrics for e-cigarettes reaching over xx% in key demographics. The industry's trajectory is marked by an increasing focus on product safety, quality control, and regulatory compliance, as governments worldwide grapple with regulating this rapidly expanding market. The base year of 2025 signifies a period of maturing growth, where innovation continues, but market strategies are increasingly focused on sustainability and market share defense, especially in light of evolving global regulations and the introduction of novel nicotine delivery systems.</p>

<h2>Leading Regions, Countries, or Segments in Electronic Cigarette ODM and OEM</h2>

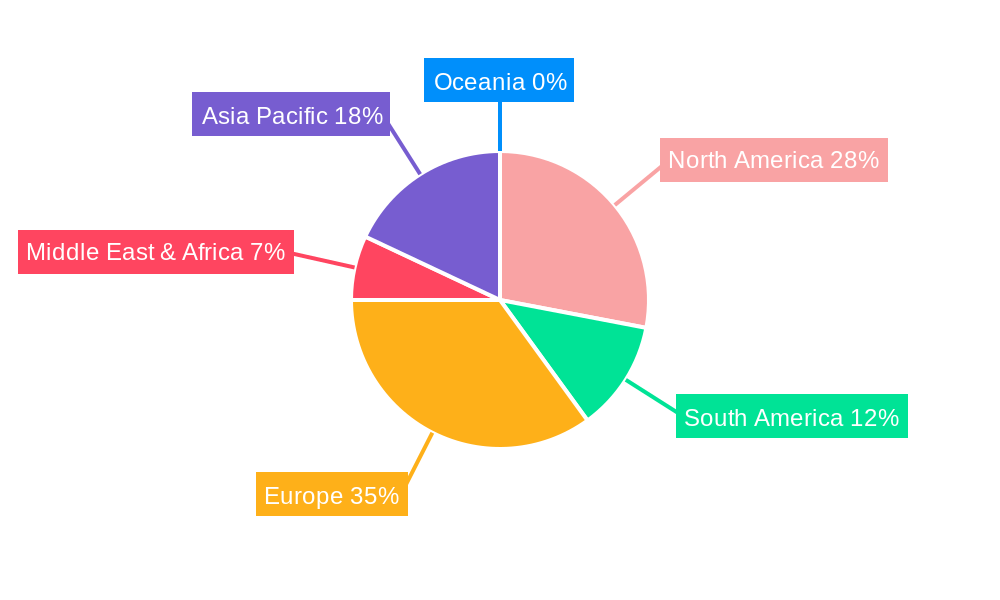

<p>Asia, particularly China, has consistently emerged as the dominant region in the Electronic Cigarette ODM and OEM market. This dominance is propelled by several interconnected factors, including a robust manufacturing infrastructure, a skilled workforce, lower production costs, and a high concentration of leading e-cigarette brands and component suppliers. Countries like China are home to a vast network of ODM and OEM providers, ranging from large conglomerates like BYD to specialized manufacturers such as Joyetech holding limited, Kangertech, and Shenzhen GreenSound Technology, catering to both domestic and international demand for Vaping Electronic Cigarettes and Heat-Not-Burn Electronic Cigarettes. The segment of Vaping Electronic Cigarettes remains the largest by volume, driven by a global consumer base seeking diverse flavor options and portable devices. However, the Heat-Not-Burn Electronic Cigarettes segment is experiencing significant growth, particularly in markets with stricter regulations on combustible cigarettes and a demand for perceived harm reduction, with companies like Philip Morris International heavily invested in this area.</p>

<ul>

<li><strong>Dominant Region:</strong> Asia (primarily China)</li>

<li><strong>Key Countries:</strong> China, United States, United Kingdom, South Korea</li>

<li><strong>Dominant Application Segment:</strong> Vaping Electronic Cigarettes</li>

<li><strong>Growing Segment:</strong> Heat-Not-Burn Electronic Cigarettes</li>

<li><strong>Dominant Service Type:</strong> ODM services often preferred by emerging brands and startups for end-to-end product development and manufacturing.</li>

<li><strong>OEM Significance:</strong> Crucial for established brands requiring high-volume, cost-effective production, often involving established players like JTI and Imperial Tobacco.</li>

<li><strong>Investment Trends:</strong> Significant foreign direct investment into Asian manufacturing hubs, and increasing investment in R&D for next-generation devices.</li>

<li><strong>Regulatory Support:</strong> While regulations vary, supportive industrial policies in some Asian nations have fostered manufacturing growth.</li>

<li><strong>Market Penetration:</strong> High adoption rates in developed markets and emerging markets present vast opportunities for both ODM and OEM services.</li>

</ul>

<h2>Electronic Cigarette ODM and OEM Product Innovations</h2>

<p>Product innovation within the Electronic Cigarette ODM and OEM sector is intensely focused on enhancing user experience, safety, and device performance. Advancements include sophisticated temperature control systems for Vaping Electronic Cigarettes, preventing dry hits and optimizing flavor delivery, alongside the development of more compact and longer-lasting battery technologies, with capacities now exceeding one million milliampere-hours in some experimental designs. For Heat-Not-Burn Electronic Cigarettes, innovations center on precise heating mechanisms that mimic the sensory experience of smoking without combustion, using ceramic or induction heating elements for consistent results. The integration of smart features, such as app connectivity for usage tracking and personalized settings, and the development of leak-proof pod designs and child-resistant mechanisms, are also prominent selling propositions, enhancing both functionality and safety for consumers worldwide. The performance metrics increasingly emphasize puff count, battery life, charging speed, and flavor consistency, with ODM and OEM partners playing a crucial role in bringing these cutting-edge designs to market efficiently.</p>

<h2>Propelling Factors for Electronic Cigarette ODM and OEM Growth</h2>

<p>The growth of the Electronic Cigarette ODM and OEM market is propelled by several key factors. Technologically, continuous innovation in battery life, heating element efficiency, and device miniaturization drives product development. Economically, the lower manufacturing costs in key Asian production hubs make ODM and OEM services attractive for global brands seeking competitive pricing. Regulatory shifts, while sometimes challenging, also create opportunities for compliant and innovative products. For example, the increasing global acceptance of Heat-Not-Burn Electronic Cigarettes as a harm reduction alternative to traditional cigarettes presents a significant market expansion potential. Furthermore, the growing consumer demand for personalized and discreet vaping devices fuels the need for flexible ODM and OEM solutions that can cater to diverse design specifications and quality standards.</p>

<h2>Obstacles in the Electronic Cigarette ODM and OEM Market</h2>

<p>Despite robust growth, the Electronic Cigarette ODM and OEM market faces significant obstacles. The primary challenge lies in the fragmented and evolving regulatory landscape, with varying restrictions on ingredients, marketing, and sales in different countries, impacting international manufacturing strategies. Supply chain disruptions, as witnessed in recent global events, can lead to increased costs and lead times for components, affecting production schedules. Furthermore, intense competition among numerous ODM and OEM providers, particularly in Asia, can lead to price wars and pressure on profit margins. Concerns regarding product safety and potential long-term health effects, though debated, also cast a shadow, leading to increased scrutiny and potential market contractions in certain regions. The intellectual property landscape can also be complex, with frequent patent disputes adding to market uncertainty.</p>

<h2>Future Opportunities in Electronic Cigarette ODM and OEM</h2>

<p>Emerging opportunities in the Electronic Cigarette ODM and OEM market are abundant, driven by technological advancements and shifting consumer preferences. The development of next-generation nicotine delivery systems, including advanced pod mods with AI-driven user experiences and highly customizable Heat-Not-Burn devices, presents significant growth avenues. Expansion into emerging markets in Africa and Southeast Asia, where e-cigarette adoption is still nascent, offers substantial untapped potential for both ODM and OEM partners. Furthermore, the growing demand for sustainable manufacturing practices and eco-friendly materials creates opportunities for companies that can innovate in these areas. The increasing focus on regulated markets and the demand for premium, high-quality devices also present opportunities for ODM and OEM providers that can meet stringent quality control and compliance standards.</p>

<h2>Major Players in the Electronic Cigarette ODM and OEM Ecosystem</h2>

<ul>

<li>Philip Morris International</li>

<li>SMOOKE</li>

<li>FIRST UNION GROUP</li>

<li>SIGELEI</li>

<li>RELX</li>

<li>YOOZ</li>

<li>JUUL</li>

<li>NJOY</li>

<li>MOTI</li>

<li>Imperial Tobacco</li>

<li>JTI</li>

<li>BYD</li>

<li>Joyetech holding limited</li>

<li>Geekvape</li>

<li>Kangertech</li>

<li>Jinjia TECHNOLOGIES</li>

<li>Jasper Enterprise Management Consulting</li>

<li>Shenzhen GreenSound Technology</li>

<li>Alpha Electronic Technology</li>

<li>JOUZ</li>

<li>Itron Electronics</li>

<li>ATOM</li>

<li>VGOD</li>

<li>Sigelei</li>

</ul>

<h2>Key Developments in Electronic Cigarette ODM and OEM Industry</h2>

<ul>

<li><strong>2023/Q4:</strong> Increased focus on R&D for advanced ceramic heating elements in Heat-Not-Burn devices.</li>

<li><strong>2023/Q3:</strong> Emergence of new ODM partners specializing in modular and customizable e-cigarette designs.</li>

<li><strong>2023/Q2:</strong> Stricter flavor ban regulations in select markets prompting innovation in unflavored nicotine solutions by OEM manufacturers.</li>

<li><strong>2023/Q1:</strong> Significant investment in automation and AI for quality control in large-scale OEM production lines.</li>

<li><strong>2022/Q4:</strong> Growing demand for disposable Vaping Electronic Cigarettes with extended puff counts and improved battery life.</li>

<li><strong>2022/Q3:</strong> Mergers and acquisitions consolidating smaller ODM players into larger manufacturing groups.</li>

<li><strong>2022/Q2:</strong> Introduction of smart features and app connectivity in premium e-cigarette models produced by ODM partners.</li>

<li><strong>2022/Q1:</strong> Enhanced focus on child-resistant designs and tamper-evident packaging by OEM suppliers.</li>

<li><strong>2021/Q4:</strong> Expansion of Heat-Not-Burn device options beyond traditional tobacco flavors.</li>

<li><strong>2021/Q3:</strong> Supply chain resilience becoming a key differentiator for ODM and OEM providers.</li>

</ul>

<h2>Strategic Electronic Cigarette ODM and OEM Market Forecast</h2>

<p>The strategic Electronic Cigarette ODM and OEM market forecast for the period 2025–2033 indicates continued robust growth, driven by innovation in product development and evolving consumer preferences. Key growth catalysts include the expanding global adoption of Vaping Electronic Cigarettes and Heat-Not-Burn Electronic Cigarettes, supported by ongoing R&D in device technology and nicotine delivery systems. The increasing demand for personalized and high-quality vaping experiences will further fuel the need for sophisticated ODM and OEM solutions. Market potential is significant, particularly in emerging economies and through the continuous refinement of existing product categories to meet evolving regulatory standards and consumer expectations for safety and efficacy.</p>

</body>

</html>

Electronic Cigarette ODM and OEM Segmentation

-

1. Application

- 1.1. Vaping Electronic Cigarettes

- 1.2. Heat-Not-Burn Electronic Cigarettes

-

2. Types

- 2.1. ODM

- 2.2. OEM

Electronic Cigarette ODM and OEM Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electronic Cigarette ODM and OEM Regional Market Share

Geographic Coverage of Electronic Cigarette ODM and OEM

Electronic Cigarette ODM and OEM REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Vaping Electronic Cigarettes

- 5.1.2. Heat-Not-Burn Electronic Cigarettes

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. ODM

- 5.2.2. OEM

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Vaping Electronic Cigarettes

- 6.1.2. Heat-Not-Burn Electronic Cigarettes

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. ODM

- 6.2.2. OEM

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Vaping Electronic Cigarettes

- 7.1.2. Heat-Not-Burn Electronic Cigarettes

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. ODM

- 7.2.2. OEM

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Vaping Electronic Cigarettes

- 8.1.2. Heat-Not-Burn Electronic Cigarettes

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. ODM

- 8.2.2. OEM

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Vaping Electronic Cigarettes

- 9.1.2. Heat-Not-Burn Electronic Cigarettes

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. ODM

- 9.2.2. OEM

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electronic Cigarette ODM and OEM Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Vaping Electronic Cigarettes

- 10.1.2. Heat-Not-Burn Electronic Cigarettes

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. ODM

- 10.2.2. OEM

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Philip Morris International

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 SMOOKE

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 FIRST UNION GROUP

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 SIGELEI

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 RELX

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 YOOZ

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 JUUL

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 NJOY

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 MOTI

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Imperial Tobacco

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 JTI

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 BYD

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Joyetech holding limited

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Geekvape

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Kangertech

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Jinjia TECHNOLOGIES

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Jasper Enterprise Management Consulting

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Shenzhen GreenSound Technology

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Alpha Electronic Technology

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 JOUZ

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Itron Electronics

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 ATOM

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 VGOD

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Sigelei

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.1 Philip Morris International

List of Figures

- Figure 1: Global Electronic Cigarette ODM and OEM Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Electronic Cigarette ODM and OEM Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Electronic Cigarette ODM and OEM Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Electronic Cigarette ODM and OEM Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Electronic Cigarette ODM and OEM Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Electronic Cigarette ODM and OEM Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Electronic Cigarette ODM and OEM Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Electronic Cigarette ODM and OEM Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Electronic Cigarette ODM and OEM Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Electronic Cigarette ODM and OEM Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Electronic Cigarette ODM and OEM Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Electronic Cigarette ODM and OEM Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Electronic Cigarette ODM and OEM Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Electronic Cigarette ODM and OEM Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Electronic Cigarette ODM and OEM Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Electronic Cigarette ODM and OEM Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Electronic Cigarette ODM and OEM Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Electronic Cigarette ODM and OEM Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Electronic Cigarette ODM and OEM Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Electronic Cigarette ODM and OEM Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Electronic Cigarette ODM and OEM Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Electronic Cigarette ODM and OEM Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Electronic Cigarette ODM and OEM Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Electronic Cigarette ODM and OEM Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Electronic Cigarette ODM and OEM Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Electronic Cigarette ODM and OEM Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Electronic Cigarette ODM and OEM Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Electronic Cigarette ODM and OEM Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Electronic Cigarette ODM and OEM Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Electronic Cigarette ODM and OEM Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Electronic Cigarette ODM and OEM Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Electronic Cigarette ODM and OEM Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Electronic Cigarette ODM and OEM Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electronic Cigarette ODM and OEM?

The projected CAGR is approximately 8.4%.

2. Which companies are prominent players in the Electronic Cigarette ODM and OEM?

Key companies in the market include Philip Morris International, SMOOKE, FIRST UNION GROUP, SIGELEI, RELX, YOOZ, JUUL, NJOY, MOTI, Imperial Tobacco, JTI, BYD, Joyetech holding limited, Geekvape, Kangertech, Jinjia TECHNOLOGIES, Jasper Enterprise Management Consulting, Shenzhen GreenSound Technology, Alpha Electronic Technology, JOUZ, Itron Electronics, ATOM, VGOD, Sigelei.

3. What are the main segments of the Electronic Cigarette ODM and OEM?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electronic Cigarette ODM and OEM," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electronic Cigarette ODM and OEM report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electronic Cigarette ODM and OEM?

To stay informed about further developments, trends, and reports in the Electronic Cigarette ODM and OEM, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence