Key Insights

The global dairy packaging carton market is experiencing robust growth, driven by increasing consumer demand for convenient and hygienic dairy products. With a current market size estimated at approximately $8.5 billion and a projected Compound Annual Growth Rate (CAGR) of around 7%, the market is poised for significant expansion throughout the forecast period of 2025-2033. This surge is primarily fueled by the rising consumption of yogurt and cheese, particularly in emerging economies, where evolving lifestyles and a growing middle class are leading to increased disposable incomes and a preference for convenient, single-serving packaging formats. The ≤200ml and 201-500ml carton segments are expected to dominate due to their appeal for on-the-go consumption and smaller household sizes. Furthermore, advancements in packaging technology, focusing on extended shelf life, recyclability, and enhanced barrier properties, are key drivers supporting market expansion. Major players are investing in sustainable packaging solutions, aligning with global environmental concerns and regulatory pushes towards eco-friendly alternatives.

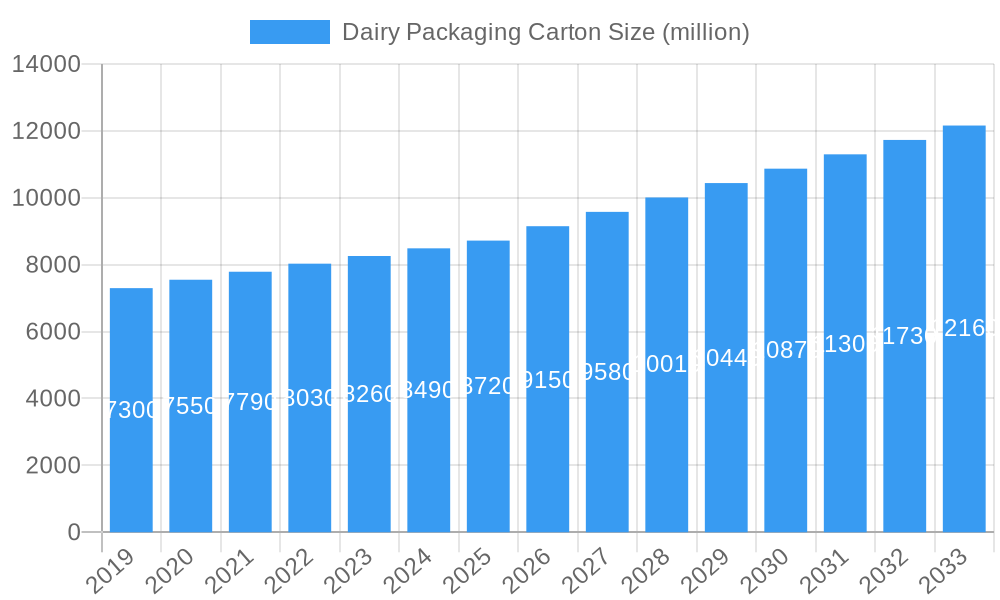

Dairy Packaging Carton Market Size (In Billion)

Despite the positive outlook, the market faces certain restraints, including fluctuating raw material prices, particularly for paperboard and aluminum, which can impact profit margins for manufacturers. Stringent regulatory frameworks concerning food packaging safety and environmental impact also present challenges, requiring continuous innovation and compliance. However, the overarching trend towards healthier eating habits and the convenience offered by carton packaging for various dairy products like cream and buttermilk, are expected to outweigh these challenges. The Asia Pacific region, led by China and India, is anticipated to be the fastest-growing market due to rapid urbanization, a burgeoning population, and increasing adoption of Western dietary habits. North America and Europe, while mature markets, continue to show steady growth driven by premiumization, innovation in product formats, and a strong focus on sustainability.

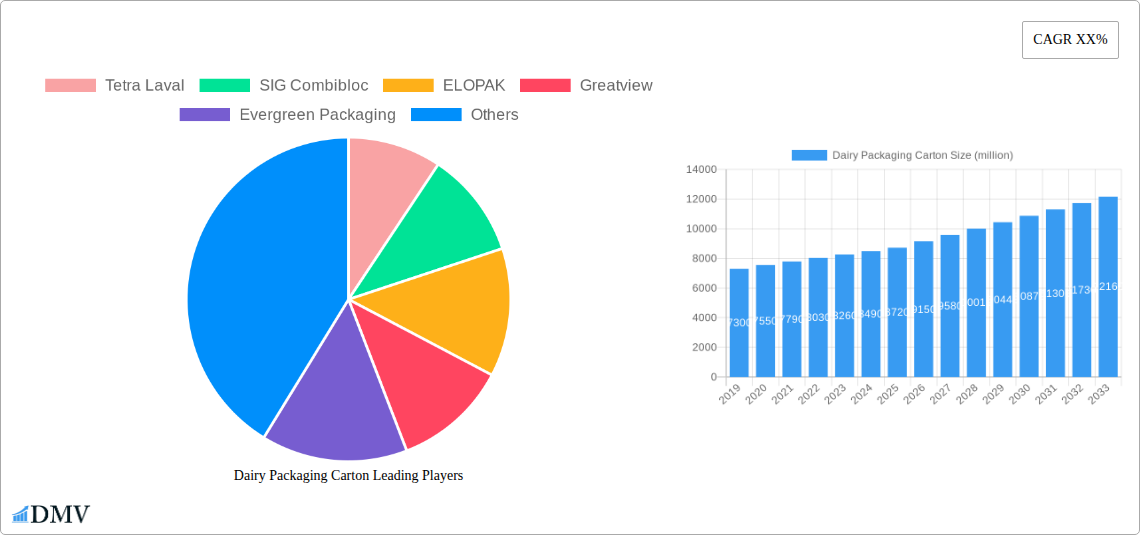

Dairy Packaging Carton Company Market Share

Dairy Packaging Carton Market Analysis: Growth, Innovations, and Future Outlook (2019-2033)

This comprehensive report delves deep into the global Dairy Packaging Carton market, offering an unparalleled analysis of its current landscape, historical trajectory, and future potential. We dissect market composition, identify key industry developments, and project future trends from 2019 through 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033. This report is an essential resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and make informed strategic decisions in the rapidly evolving dairy packaging sector.

Dairy Packaging Carton Market Composition & Trends

The global Dairy Packaging Carton market is characterized by a dynamic interplay of established players and emerging innovators, driven by increasing demand for convenient and sustainable dairy product consumption. Market concentration is moderate, with key companies like Tetra Laval, SIG Combibloc, and ELOPAK holding significant market shares, estimated at over 50% combined. Innovation catalysts are primarily focused on enhancing shelf life, improving barrier properties, and promoting eco-friendly materials. Regulatory landscapes, particularly concerning food safety and environmental sustainability, significantly influence product development and market entry strategies. Substitute products, such as plastic bottles and pouches, present competitive challenges, but the inherent benefits of carton packaging, including lightweight design and excellent recyclability, maintain its strong market position. End-user profiles range from large-scale dairy processors to smaller artisanal producers, each with specific packaging requirements. Mergers and acquisitions (M&A) activities are notable, with an estimated annual deal value exceeding 500 million. For instance, recent acquisitions have focused on companies with advanced material science or extended shelf-life technologies.

- Market Share Distribution (Estimated):

- Top 3 Players: >50%

- Top 5 Players: >65%

- Top 10 Players: >80%

- M&A Activity:

- Estimated Annual Deal Value: >500 million

- Focus Areas: Sustainable materials, advanced barrier technologies, filling line integration.

- Key Innovation Drivers:

- Lightweighting and material reduction.

- Enhanced recyclability and use of recycled content.

- Improved shelf-life extension technologies.

- Smart packaging solutions for traceability.

Dairy Packaging Carton Industry Evolution

The dairy packaging carton industry has witnessed remarkable evolution, driven by a confluence of technological advancements, shifting consumer preferences, and a growing global demand for dairy products. Over the historical period of 2019–2024, the market experienced a steady growth trajectory, with an average annual growth rate of approximately 5%. This growth was fueled by increasing per capita consumption of dairy products, particularly in developing economies, and a rise in demand for convenient, single-serving formats. The base year of 2025 sees the market consolidating its gains, with an estimated market size of XX million. Looking ahead, the forecast period of 2025–2033 anticipates a sustained growth rate of around 6% annually, projected to reach a market value of XX million by the end of the study period.

Technological advancements have been pivotal. The introduction of advanced barrier materials has significantly extended the shelf life of dairy products, reducing spoilage and waste. Innovations in printing and graphics have enhanced brand appeal and consumer engagement. Furthermore, the development of more efficient filling and sealing machinery has led to increased production speeds and reduced operational costs for manufacturers. The adoption of aseptic packaging technologies has been particularly transformative, enabling the distribution of long-life dairy products without refrigeration, thus expanding market reach and accessibility.

Shifting consumer demands have also played a crucial role. There is a growing preference for sustainable and environmentally friendly packaging solutions. Consumers are increasingly aware of the environmental impact of packaging waste, leading to a higher demand for recyclable and biodegradable cartons. Convenience remains a key factor, with a preference for smaller portion sizes and easy-to-open packaging. The rise of the health and wellness trend has also boosted demand for yoghurts, and functional dairy beverages, which are often packaged in cartons.

- Market Growth Trajectory:

- Historical CAGR (2019-2024): ~5%

- Estimated Market Size (2025): XX million

- Forecast CAGR (2025-2033): ~6%

- Projected Market Size (2033): XX million

- Technological Advancements:

- Barrier Technologies: Development of advanced multilayered materials for enhanced oxygen and moisture barrier properties. Adoption rate for advanced barrier cartons estimated at 70% by 2025.

- Aseptic Packaging: Increased adoption for extended shelf-life products, enabling distribution without refrigeration.

- Lightweighting: Reduction in material usage while maintaining structural integrity.

- Digital Printing: Enhanced customization and shorter production runs.

- Consumer Demand Shifts:

- Sustainability: Growing preference for recyclable, biodegradable, and reduced-plastic packaging.

- Convenience: Demand for single-serve, easy-to-open, and portable packaging formats.

- Health & Wellness: Increased consumption of yoghurts, milk, and functional dairy drinks.

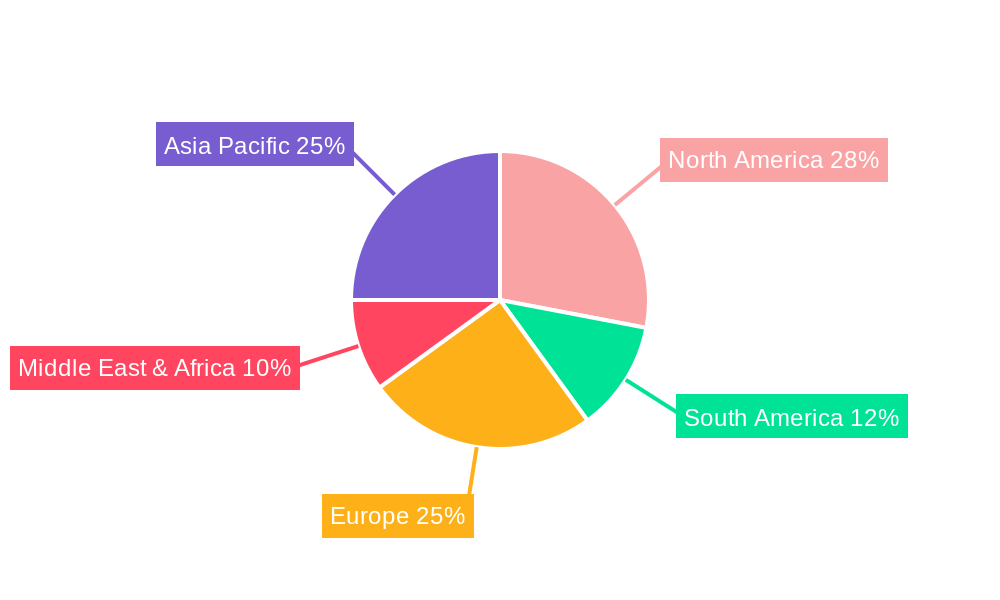

Leading Regions, Countries, or Segments in Dairy Packaging Carton

The global Dairy Packaging Carton market showcases distinct regional strengths and segment dominance, driven by varying consumption patterns, regulatory frameworks, and economic development. North America and Europe currently represent the most mature markets, characterized by high per capita dairy consumption and a strong emphasis on sustainable packaging solutions. Asia Pacific, however, is emerging as the fastest-growing region, propelled by rapid urbanization, a burgeoning middle class, and increasing adoption of Western dietary habits.

Within the Application segment, Yoghurt consistently leads the market, accounting for an estimated 40% of the total dairy packaging carton volume. This dominance is attributed to its widespread popularity across all age groups and its versatile consumption occasions, from breakfast to snacks. Cream and Cheese applications follow, with a combined share of approximately 30%. The demand for these products, particularly in convenient and portioned packaging, continues to grow. Buttermilk and Others (including flavored milk, plant-based dairy alternatives packaged in cartons, etc.) represent the remaining 30%, with the "Others" category showing significant growth potential due to the rise of innovative dairy-based beverages.

In terms of Types, the 201-500ml carton segment is the most dominant, holding an estimated 45% market share. This size is ideal for single servings and family consumption, aligning with convenience trends. The ≤200ml segment, popular for children's milk and single-serve yoghurts, accounts for approximately 25%. The 501-1000ml and ≥1000ml segments cater to larger household needs and institutional use, collectively representing 30% of the market.

Key drivers for regional dominance include:

- North America: Strong existing dairy infrastructure, high consumer awareness of sustainability, and robust regulatory support for recycling initiatives. Investment trends are focused on advanced material science and circular economy solutions, with annual investment in R&D estimated at 150 million.

- Europe: Strict environmental regulations (e.g., EU packaging directives) pushing for increased use of recycled content and reduced virgin plastic. Consumer demand for premium and eco-conscious products is high.

- Asia Pacific: Rapidly expanding middle class driving increased demand for packaged dairy products. Growing awareness of food safety and shelf-life extension is boosting aseptic carton adoption. Government initiatives promoting food processing and packaging also play a crucial role. Investment in new manufacturing facilities is projected to exceed 800 million over the forecast period.

The dominance of Yoghurt and the 201-500ml carton type reflects evolving consumer lifestyles, emphasizing portability, convenience, and portion control in dairy consumption.

Dairy Packaging Carton Product Innovations

Recent product innovations in dairy packaging cartons are focused on enhancing sustainability, functionality, and consumer appeal. Companies are developing cartons made from a higher percentage of renewable and recycled materials, aiming for full circularity. Innovations in barrier technology are leading to improved shelf-life extension without compromising recyclability, a key unique selling proposition. For instance, advanced coatings and materials allow for the elimination of aluminum layers in some applications, reducing the carbon footprint. Furthermore, the introduction of convenient features like tamper-evident seals, easy-pour spouts, and integrated straws addresses consumer demand for user-friendly packaging. Smart packaging solutions, incorporating QR codes for traceability and product information, are also gaining traction, offering enhanced consumer engagement and brand transparency.

Propelling Factors for Dairy Packaging Carton Growth

Several key factors are propelling the growth of the dairy packaging carton market. Firstly, the increasing global demand for dairy products, driven by rising populations and evolving dietary habits, directly translates into higher demand for packaging solutions. Secondly, technological advancements in material science and aseptic packaging are enabling longer shelf lives, reduced spoilage, and wider distribution networks, making dairy products more accessible. Thirdly, growing consumer awareness and preference for sustainable packaging are a significant catalyst, as cartons are often perceived as more environmentally friendly than traditional plastic alternatives due to their high recyclability rates and increasing use of renewable resources. Finally, regulatory support for recycling and waste reduction in many regions incentivizes the use of carton packaging.

Obstacles in the Dairy Packaging Carton Market

Despite its growth, the dairy packaging carton market faces several obstacles. Regulatory challenges related to the collection and effective recycling of composite cartons in certain regions can hinder widespread adoption and consumer perception. Supply chain disruptions, such as fluctuations in the availability and cost of raw materials like paperboard and polymers, can impact production costs and lead times, with an estimated impact of up to 10% on profitability during periods of volatility. Competitive pressures from alternative packaging formats, such as rigid plastic containers and flexible pouches, which may offer perceived advantages in specific applications or price points, also present a restraint. Furthermore, the capital investment required for advanced filling and packaging machinery can be a barrier for smaller dairy producers.

Future Opportunities in Dairy Packaging Carton

The future of the dairy packaging carton market is rife with opportunities. The expanding market for plant-based dairy alternatives presents a significant growth avenue, as cartons are well-suited for these products. Continued innovation in sustainable materials, including the development of fully compostable or bio-based cartons, will further enhance market appeal. The growing demand for premium and artisanal dairy products offers opportunities for customized and visually appealing packaging solutions. Furthermore, the expansion of e-commerce and food delivery services creates a need for robust and efficient packaging that ensures product integrity during transit. Investing in advanced recycling infrastructure and promoting consumer education on proper disposal will unlock further growth potential.

Major Players in the Dairy Packaging Carton Ecosystem

- Tetra Laval

- SIG Combibloc

- ELOPAK

- Greatview

- Evergreen Packaging

- Nippon Paper

- Likang Packing

- Stora Enso

- Weyerhaeuser

- Xinju Feng Pack

- Bihai Machinery

Key Developments in Dairy Packaging Carton Industry

- 2023 October: SIG Combibloc launches new generation of carton packs with enhanced recyclability and reduced material usage.

- 2023 September: Tetra Laval introduces innovative barrier technology for plant-based dairy alternatives, extending shelf life significantly.

- 2023 June: ELOPAK announces ambitious sustainability targets, aiming for 100% renewable or recycled materials in its packaging by 2030.

- 2022 December: Greatview expands its production capacity in Asia to meet growing regional demand for aseptic carton packaging.

- 2022 August: Evergreen Packaging invests in advanced recycling technologies to improve the circularity of its carton products.

- 2022 May: Nippon Paper develops a new paperboard grade with improved strength and reduced environmental impact.

- 2021 November: Stora Enso partners with a leading dairy producer to trial fully renewable carton packaging for yogurt.

- 2021 July: Likang Packing introduces a new range of smaller format dairy cartons targeting the convenience segment.

Strategic Dairy Packaging Carton Market Forecast

The strategic dairy packaging carton market forecast indicates a period of robust and sustained growth, driven by the increasing global consumption of dairy products and a pronounced shift towards sustainable packaging solutions. Key growth catalysts include ongoing technological advancements in material science and aseptic filling, which promise to enhance product shelf life and reduce waste, alongside supportive regulatory frameworks encouraging recycling and the use of renewable resources. The expanding market for plant-based alternatives and the rise of e-commerce present significant untapped opportunities. Strategic investments in R&D, capacity expansion, and circular economy initiatives will be crucial for players aiming to capitalize on the projected market potential, estimated to reach XX million by 2033.

Dairy Packaging Carton Segmentation

-

1. Application

- 1.1. Yoghurt

- 1.2. Cheese

- 1.3. Cream

- 1.4. Buttermilk

- 1.5. Others

-

2. Types

- 2.1. ≤200ml

- 2.2. 201-500ml

- 2.3. 501-1000ml

- 2.4. ≥1000ml

Dairy Packaging Carton Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dairy Packaging Carton Regional Market Share

Geographic Coverage of Dairy Packaging Carton

Dairy Packaging Carton REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Yoghurt

- 5.1.2. Cheese

- 5.1.3. Cream

- 5.1.4. Buttermilk

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. ≤200ml

- 5.2.2. 201-500ml

- 5.2.3. 501-1000ml

- 5.2.4. ≥1000ml

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Yoghurt

- 6.1.2. Cheese

- 6.1.3. Cream

- 6.1.4. Buttermilk

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. ≤200ml

- 6.2.2. 201-500ml

- 6.2.3. 501-1000ml

- 6.2.4. ≥1000ml

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Yoghurt

- 7.1.2. Cheese

- 7.1.3. Cream

- 7.1.4. Buttermilk

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. ≤200ml

- 7.2.2. 201-500ml

- 7.2.3. 501-1000ml

- 7.2.4. ≥1000ml

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Yoghurt

- 8.1.2. Cheese

- 8.1.3. Cream

- 8.1.4. Buttermilk

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. ≤200ml

- 8.2.2. 201-500ml

- 8.2.3. 501-1000ml

- 8.2.4. ≥1000ml

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Yoghurt

- 9.1.2. Cheese

- 9.1.3. Cream

- 9.1.4. Buttermilk

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. ≤200ml

- 9.2.2. 201-500ml

- 9.2.3. 501-1000ml

- 9.2.4. ≥1000ml

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Dairy Packaging Carton Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Yoghurt

- 10.1.2. Cheese

- 10.1.3. Cream

- 10.1.4. Buttermilk

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. ≤200ml

- 10.2.2. 201-500ml

- 10.2.3. 501-1000ml

- 10.2.4. ≥1000ml

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Tetra Laval

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 SIG Combibloc

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ELOPAK

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Greatview

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Evergreen Packaging

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Nippon Paper

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Likang Packing

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Stora Enso

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Weyerhaeuser

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Xinju Feng Pack

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bihai Machinery

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Tetra Laval

List of Figures

- Figure 1: Global Dairy Packaging Carton Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Dairy Packaging Carton Revenue (million), by Application 2025 & 2033

- Figure 3: North America Dairy Packaging Carton Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Dairy Packaging Carton Revenue (million), by Types 2025 & 2033

- Figure 5: North America Dairy Packaging Carton Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Dairy Packaging Carton Revenue (million), by Country 2025 & 2033

- Figure 7: North America Dairy Packaging Carton Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Dairy Packaging Carton Revenue (million), by Application 2025 & 2033

- Figure 9: South America Dairy Packaging Carton Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Dairy Packaging Carton Revenue (million), by Types 2025 & 2033

- Figure 11: South America Dairy Packaging Carton Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Dairy Packaging Carton Revenue (million), by Country 2025 & 2033

- Figure 13: South America Dairy Packaging Carton Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Dairy Packaging Carton Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Dairy Packaging Carton Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Dairy Packaging Carton Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Dairy Packaging Carton Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Dairy Packaging Carton Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Dairy Packaging Carton Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Dairy Packaging Carton Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Dairy Packaging Carton Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Dairy Packaging Carton Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Dairy Packaging Carton Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Dairy Packaging Carton Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Dairy Packaging Carton Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Dairy Packaging Carton Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Dairy Packaging Carton Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Dairy Packaging Carton Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Dairy Packaging Carton Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Dairy Packaging Carton Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Dairy Packaging Carton Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Dairy Packaging Carton Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Dairy Packaging Carton Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Dairy Packaging Carton Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Dairy Packaging Carton Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Dairy Packaging Carton Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Dairy Packaging Carton Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Dairy Packaging Carton Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Dairy Packaging Carton Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Dairy Packaging Carton Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dairy Packaging Carton?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Dairy Packaging Carton?

Key companies in the market include Tetra Laval, SIG Combibloc, ELOPAK, Greatview, Evergreen Packaging, Nippon Paper, Likang Packing, Stora Enso, Weyerhaeuser, Xinju Feng Pack, Bihai Machinery.

3. What are the main segments of the Dairy Packaging Carton?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dairy Packaging Carton," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dairy Packaging Carton report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dairy Packaging Carton?

To stay informed about further developments, trends, and reports in the Dairy Packaging Carton, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence