Key Insights

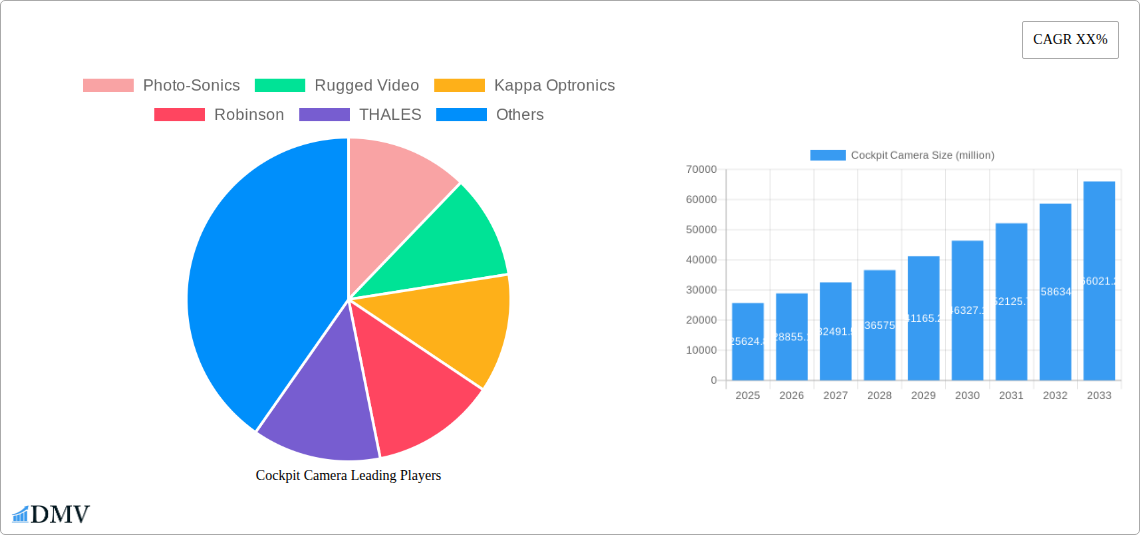

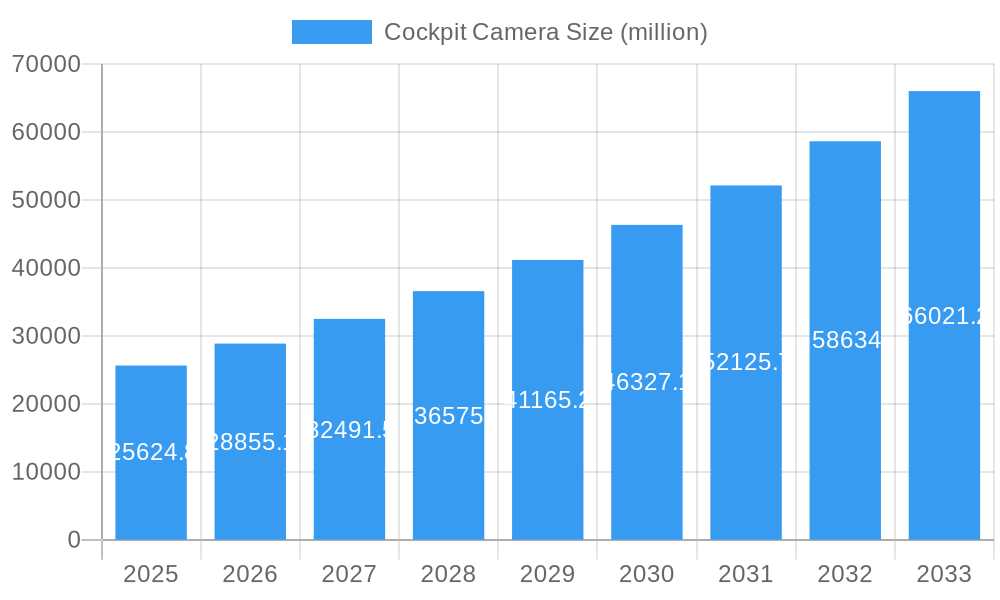

The global cockpit camera market is poised for robust expansion, projected to reach $25,624.8 million by 2025, driven by an impressive 12.6% CAGR. This significant growth is fueled by an escalating demand for enhanced aviation safety and operational efficiency. The inherent need for sophisticated surveillance and recording capabilities within aircraft cockpits, particularly in commercial aviation for incident analysis and pilot performance monitoring, forms a core driver. Furthermore, the increasing adoption of advanced avionics and the integration of AI-powered systems for real-time threat detection and data analysis are propelling market forward. Emerging applications in pilot training and simulator realism are also contributing to this upward trajectory, alongside the growing implementation of cockpit voice recorders (CVRs) and flight data recorders (FDRs) as mandatory safety equipment.

Cockpit Camera Market Size (In Billion)

The market segmentation reveals a balanced landscape between miniature and middle-sized cockpit cameras, catering to diverse aircraft types and regulatory requirements. While military applications, with their stringent security and surveillance needs, represent a substantial segment, the commercial aviation sector is exhibiting particularly strong growth due to evolving safety regulations and the drive for operational excellence. Key restraints, such as the high initial cost of sophisticated camera systems and the potential for data privacy concerns, are being addressed through technological advancements and standardized protocols. Innovations in miniaturization, enhanced image quality in low-light conditions, and robust data storage solutions are expected to mitigate these challenges. Leading players like Photo-Sonics, THALES, and Garmin are actively investing in research and development to introduce next-generation cockpit camera solutions.

Cockpit Camera Company Market Share

This in-depth market research report provides an exhaustive analysis of the global Cockpit Camera market, offering critical insights for stakeholders across the aviation and technology sectors. Covering the historical period from 2019 to 2024, the base year of 2025, and a forecast period extending to 2033, this report meticulously examines market dynamics, technological advancements, and future growth trajectories for cockpit camera systems. We delve into the intricacies of market composition, industry evolution, leading regional and segmental performance, product innovations, growth drivers, market obstacles, emerging opportunities, key players, and significant industry developments. This report is designed to empower strategic decision-making for manufacturers, suppliers, investors, and aviation industry professionals.

Cockpit Camera Market Composition & Trends

The global cockpit camera market exhibits a moderate to high concentration, with a few key players like Photo-Sonics, Rugged Video, and Kappa Optronics holding significant market share. The market is propelled by continuous innovation, driven by advancements in high-resolution imaging, miniaturization, and AI-powered analytics for enhanced flight safety and operational efficiency. Regulatory mandates, particularly for commercial aviation, are a crucial trend, requiring the implementation of advanced cockpit recording systems. The threat of substitute products, while present in the form of traditional flight data recorders, is diminishing as cockpit cameras offer richer, real-time visual data. End-user profiles range from commercial airlines and private aviation operators to military forces and drone manufacturers. Merger and acquisition (M&A) activities are notable, with companies like THALES and Robinson strategically acquiring smaller innovators to expand their product portfolios and market reach. Deal values in recent M&A activities have ranged from tens of millions to several hundred million dollars, reflecting the strategic importance of cockpit camera technology. The market is also seeing increased investment in ruggedized and radiation-hardened camera solutions for demanding military and aerospace applications. The trend towards integrated cockpit systems, where cameras are a core component, is also shaping market dynamics, leading to higher average selling prices for sophisticated solutions.

Cockpit Camera Industry Evolution

The cockpit camera industry has undergone a significant transformation, evolving from basic recording devices to sophisticated, integrated flight monitoring systems. Historically, the focus was primarily on capturing visual data for post-incident analysis. However, the Study Period (2019–2033), with a Base Year (2025) and Forecast Period (2025–2033), highlights a dramatic shift towards proactive safety enhancement and operational intelligence. During the Historical Period (2019–2024), adoption rates for cockpit cameras, especially in commercial aviation, saw a steady increase of approximately 5-7% annually. This growth was driven by evolving safety regulations and a growing awareness of the value of visual data.

The Estimated Year (2025) marks a pivotal point where technological advancements, such as the integration of artificial intelligence for real-time event detection and analysis, are becoming standard. The market growth trajectory is projected to accelerate in the Forecast Period (2025–2033), with an estimated Compound Annual Growth Rate (CAGR) of 8-10%. This acceleration is fueled by several key factors. Firstly, technological advancements are continuously pushing the boundaries of what cockpit cameras can do. This includes the development of cameras with wider fields of view, improved low-light performance, enhanced durability to withstand extreme environmental conditions, and the integration of advanced data processing capabilities. For instance, the adoption of 4K resolution and high dynamic range (HDR) imaging is becoming increasingly prevalent, offering unparalleled clarity and detail.

Secondly, shifting consumer demands, particularly from airlines and military operators, are driving the evolution. There's a growing demand for integrated solutions that go beyond simple recording, offering predictive maintenance insights, pilot behavior analysis, and enhanced situational awareness. This has led to increased investment in research and development by leading companies like TechFury and Appareo. Furthermore, the increasing complexity of modern aircraft and the rising emphasis on aviation safety worldwide are creating a sustained demand for sophisticated cockpit camera systems. The market is also witnessing a trend towards smaller, lighter, and more power-efficient camera modules, enabling easier integration into existing and new aircraft designs. The projected growth rate of over 10% in certain segments, particularly in military applications and emerging commercial aviation markets, underscores the strategic importance and expanding utility of cockpit camera technology.

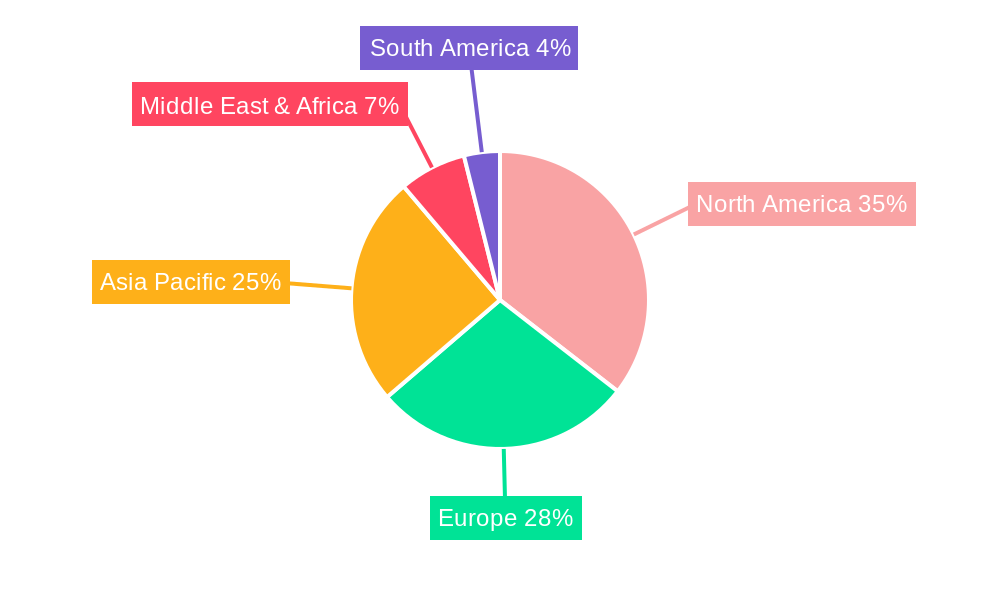

Leading Regions, Countries, or Segments in Cockpit Camera

The Military segment of the cockpit camera market is demonstrating robust dominance, driven by an escalating global defense budget and the increasing need for enhanced operational oversight and tactical intelligence. Countries with significant military expenditures, such as the United States, China, and several European nations, are key drivers of this segment's growth. Kappa Optronics and THALES are prominent players in supplying advanced, ruggedized camera systems for military aircraft and surveillance platforms. Investment trends in this segment are characterized by substantial government procurement contracts and a continuous push for cutting-edge technologies that offer superior performance in extreme environments. Regulatory support, while less publicly codified than in commercial aviation, is implicitly driven by national security imperatives, fostering rapid development and adoption of sophisticated cockpit camera solutions.

In contrast, the Commercial Use segment, while also growing, is influenced by different dynamics. Airlines are increasingly adopting cockpit cameras for safety enhancement, pilot training, and operational efficiency. The adoption rate in this segment is steadily increasing, projected to see a CAGR of approximately 7-9%. Key countries leading this adoption include those with large commercial airline fleets and stringent aviation safety regulations, such as the United States, European Union member states, and countries in the Asia-Pacific region like China and India. Garmin and Appareo are significant contributors to the commercial aviation cockpit camera market, offering solutions that comply with international aviation standards. Investment here is driven by fleet upgrades, new aircraft deliveries, and a proactive approach to risk management. Regulatory bodies like the FAA and EASA play a crucial role in mandating and standardizing the use of cockpit cameras.

Among the types, Middle-sized cockpit cameras currently hold a larger market share due to their versatility and widespread application in both military and commercial aircraft. These cameras offer a balance of advanced features and integration feasibility. However, the Miniature segment is experiencing rapid growth, fueled by the increasing use of drones and unmanned aerial vehicles (UAVs) for surveillance, reconnaissance, and delivery operations. Companies like MATRIX VISION are at the forefront of developing compact, high-performance miniature camera solutions. The demand for miniaturization is also driven by the need to integrate cameras into smaller aircraft and to minimize aerodynamic drag. The dominance of the military segment and the growing importance of miniature cameras for emerging applications highlight the diverse and dynamic nature of the cockpit camera market.

Cockpit Camera Product Innovations

Recent product innovations in the cockpit camera market are significantly enhancing aircraft safety and operational capabilities. Companies are focusing on developing ultra-high-definition (UHD) cameras with advanced low-light sensitivity and wide dynamic range (WDR) to capture critical details in challenging lighting conditions. For instance, JAI has introduced cameras with superior image processing algorithms for noise reduction and superior color rendition. Innovations also include the integration of artificial intelligence (AI) for real-time event detection, such as pilot fatigue monitoring or anomaly identification, as showcased by advancements from Isource. Furthermore, ruggedization techniques have been refined, leading to cameras that are resistant to extreme temperatures, vibration, and G-forces, a key USP for military applications from providers like Bad Wolf Technologies. The trend towards AI-enabled video analytics for predictive maintenance and crew performance optimization is a significant technological advancement.

Propelling Factors for Cockpit Camera Growth

The cockpit camera market is experiencing robust growth fueled by several key factors. Stricter aviation safety regulations worldwide, particularly those from bodies like the FAA and EASA, mandate the installation and recording capabilities of cockpit cameras, creating a consistent demand. Advancements in imaging technology, including higher resolution, improved low-light performance, and AI-driven analytics, are enhancing the value proposition of these systems, making them indispensable for modern aviation. The increasing adoption of cockpit cameras in commercial aviation for pilot training, performance monitoring, and incident investigation is a significant driver. Furthermore, the burgeoning defense sector's demand for enhanced situational awareness and intelligence gathering is contributing substantially to market expansion, with countries like China and its counterparts in the Beijing Emerging Eastern Aviation Equipment sector investing heavily.

Obstacles in the Cockpit Camera Market

Despite the growth, the cockpit camera market faces certain obstacles. High initial investment costs for sophisticated, certified cockpit camera systems can be a deterrent for smaller airlines and general aviation operators. Stringent certification processes and regulatory compliance requirements can lead to extended product development cycles and increased R&D expenses for manufacturers. Supply chain disruptions, exacerbated by global events, can impact the availability of critical components and lead to price volatility. Furthermore, concerns regarding data privacy and cybersecurity, especially with the increasing integration of AI and cloud connectivity, require robust solutions and can slow down adoption if not adequately addressed by companies like Voigtlander and TechFury. The competitive landscape, with established players and emerging innovators, also presents challenges in market penetration.

Future Opportunities in Cockpit Camera

The future of the cockpit camera market is ripe with opportunities. The integration of AI for predictive maintenance, anomaly detection, and pilot behavior analysis presents a significant growth avenue. The expanding market for unmanned aerial vehicles (UAVs) and electric vertical takeoff and landing (eVTOL) aircraft will create new demand for compact, advanced cockpit camera systems. The increasing focus on pilot training and performance optimization will drive the adoption of systems offering real-time feedback and post-flight debriefing capabilities. Furthermore, the development of cybersecurity-resilient camera solutions will be crucial as connectivity increases. Emerging markets in Asia-Pacific and Latin America, with their rapidly growing aviation sectors, offer substantial untapped potential, as seen with investments in companies like Isource.

Major Players in the Cockpit Camera Ecosystem

- Photo-Sonics

- Rugged Video

- Kappa Optronics

- Robinson

- THALES

- TechFury

- Appareo

- Bad Wolf Technologies

- Voigtlander

- MATRIX VISION

- JAI

- Tesla

- Garmin

- Beijing Emerging Eastern Aviation Equipment

- Isource

Key Developments in Cockpit Camera Industry

- 2023 Q4: Photo-Sonics launches a new generation of ruggedized cockpit cameras with enhanced AI capabilities for military drone applications.

- 2024 Q1: Rugged Video secures a multi-million dollar contract with a major aerospace manufacturer for its advanced cockpit video systems.

- 2024 Q2: Kappa Optronics unveils its latest miniature cockpit camera, achieving record-breaking miniaturization without compromising performance.

- 2024 Q3: THALES announces a strategic partnership with a leading avionics provider to integrate its cockpit camera solutions into next-generation aircraft.

- 2024 Q4: Appareo receives FAA certification for its latest cockpit recording system, enhancing data acquisition and analysis.

- 2025 Q1: Bad Wolf Technologies introduces a radiation-hardened cockpit camera designed for the extreme conditions of space exploration.

- 2025 Q2: MATRIX VISION announces significant advancements in image processing for its miniature cockpit camera offerings, improving real-time situational awareness.

- 2025 Q3: JAI introduces a new line of cockpit cameras featuring advanced low-light performance and extended dynamic range.

- 2025 Q4: Garmin expands its cockpit camera product portfolio to include solutions for general aviation and business jets, enhancing pilot safety.

Strategic Cockpit Camera Market Forecast

The strategic cockpit camera market forecast indicates substantial growth driven by an unwavering commitment to aviation safety, technological innovation, and evolving operational demands. Increased adoption in commercial aviation, propelled by regulatory pushes and the pursuit of operational efficiencies, will be a key catalyst. The defense sector will continue to be a significant contributor, with a growing emphasis on advanced surveillance and tactical intelligence. Emerging opportunities in the rapidly expanding drone and eVTOL markets, coupled with ongoing advancements in AI-powered analytics for predictive maintenance and pilot performance, are poised to redefine the scope and application of cockpit camera technology. Investment in miniaturization and ruggedization will remain critical for capturing niche segments and ensuring product applicability in diverse aerospace environments, promising a dynamic and expanding market landscape.

Cockpit Camera Segmentation

-

1. Application

- 1.1. Military

- 1.2. Commercial Use

-

2. Types

- 2.1. Miniature

- 2.2. Middle-sized

Cockpit Camera Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cockpit Camera Regional Market Share

Geographic Coverage of Cockpit Camera

Cockpit Camera REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. DMV Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Military

- 5.1.2. Commercial Use

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Miniature

- 5.2.2. Middle-sized

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Cockpit Camera Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Military

- 6.1.2. Commercial Use

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Miniature

- 6.2.2. Middle-sized

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Cockpit Camera Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Military

- 7.1.2. Commercial Use

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Miniature

- 7.2.2. Middle-sized

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Cockpit Camera Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Military

- 8.1.2. Commercial Use

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Miniature

- 8.2.2. Middle-sized

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Cockpit Camera Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Military

- 9.1.2. Commercial Use

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Miniature

- 9.2.2. Middle-sized

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Cockpit Camera Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Military

- 10.1.2. Commercial Use

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Miniature

- 10.2.2. Middle-sized

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Cockpit Camera Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Military

- 11.1.2. Commercial Use

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Miniature

- 11.2.2. Middle-sized

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Photo-Sonics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Rugged Video

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kappa Optronics

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Robinson

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 THALES

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TechFury

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Appareo

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bad Wolf Technologies

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Voigtlander

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 MATRIX VISION

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 JAI

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Tesla

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Garmin

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Beijing Emerging Eastern Aviation Equipment

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Isource

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Photo-Sonics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cockpit Camera Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Cockpit Camera Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Cockpit Camera Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cockpit Camera Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Cockpit Camera Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Cockpit Camera Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Cockpit Camera Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cockpit Camera Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Cockpit Camera Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cockpit Camera Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Cockpit Camera Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Cockpit Camera Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Cockpit Camera Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cockpit Camera Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Cockpit Camera Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cockpit Camera Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Cockpit Camera Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Cockpit Camera Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Cockpit Camera Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cockpit Camera Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cockpit Camera Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cockpit Camera Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Cockpit Camera Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Cockpit Camera Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cockpit Camera Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cockpit Camera Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Cockpit Camera Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cockpit Camera Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Cockpit Camera Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Cockpit Camera Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Cockpit Camera Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Cockpit Camera Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Cockpit Camera Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Cockpit Camera Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Cockpit Camera Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Cockpit Camera Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Cockpit Camera Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Cockpit Camera Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Cockpit Camera Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cockpit Camera Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cockpit Camera?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Cockpit Camera?

Key companies in the market include Photo-Sonics, Rugged Video, Kappa Optronics, Robinson, THALES, TechFury, Appareo, Bad Wolf Technologies, Voigtlander, MATRIX VISION, JAI, Tesla, Garmin, Beijing Emerging Eastern Aviation Equipment, Isource.

3. What are the main segments of the Cockpit Camera?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cockpit Camera," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cockpit Camera report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cockpit Camera?

To stay informed about further developments, trends, and reports in the Cockpit Camera, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence